Military Thermal Weapon Sights Market Size 2025-2029

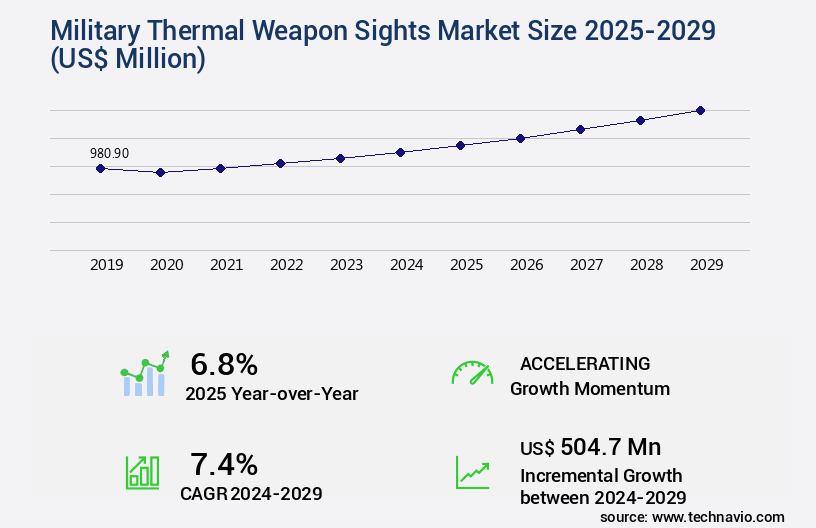

The military thermal weapon sights market size is valued to increase USD 504.7 million, at a CAGR of 7.4% from 2024 to 2029. Introduction of high-definition thermal imaging systems will drive the military thermal weapon sights market.

Major Market Trends & Insights

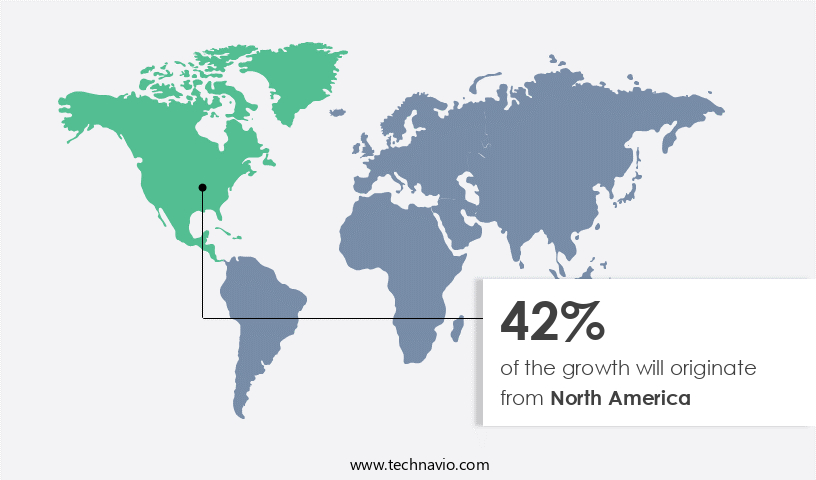

- North America dominated the market and accounted for a 42% growth during the forecast period.

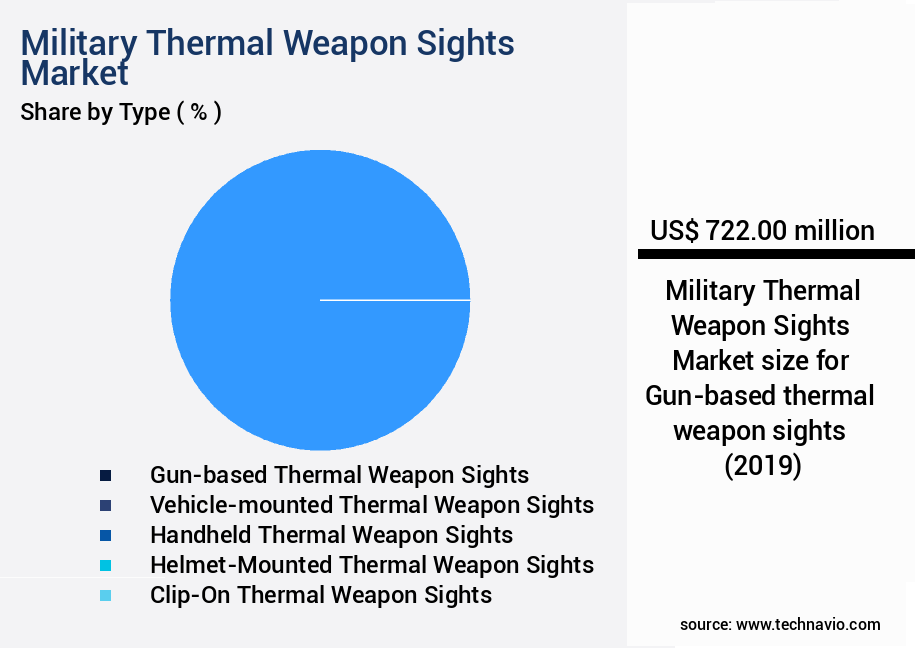

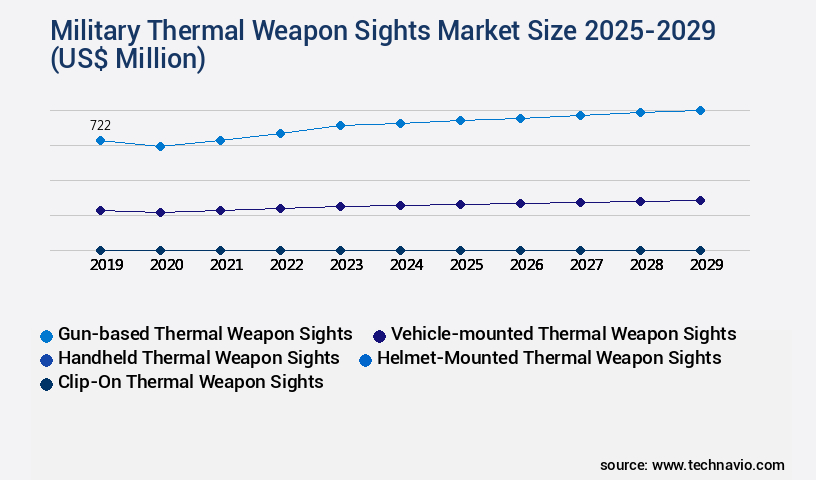

- By Type - Gun-based thermal weapon sights segment was valued at USD 722.00 million in 2023

- By Application - Army segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 71.21 million

- Market Future Opportunities: USD 504.70 million

- CAGR : 7.4%

- North America: Largest market in 2023

Market Summary

- The market encompasses the production, sale, and implementation of advanced thermal imaging systems designed for military use on weapons. This market is characterized by continuous evolution, driven by the integration of core technologies such as uncooled microbolometer sensors and advanced image processing algorithms. Notable applications include night vision capabilities for soldiers and thermal imaging for target acquisition. The emergence of wireless thermal weapon sights is a significant trend, offering enhanced mobility and flexibility. However, the high cost associated with the production of military thermal weapon sights remains a major challenge.

- According to a recent study, the market is expected to account for over 20% of the overall military night vision systems market share. As technology advances, this market will continue to unfold, presenting both opportunities and challenges for key players.

What will be the Size of the Military Thermal Weapon Sights Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Military Thermal Weapon Sights Market Segmented and what are the key trends of market segmentation?

The military thermal weapon sights industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Gun-based thermal weapon sights

- Vehicle-mounted thermal weapon sights

- Handheld Thermal Weapon Sights

- Helmet-Mounted Thermal Weapon Sights

- Clip-On Thermal Weapon Sights

- Application

- Army

- Maritime

- Land

- Technology

- Cooled Thermal

- Uncooled Thermal

- Product Type

- Clip-On Sights

- Standalone Sights

- Integrated Systems

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

The gun-based thermal weapon sights segment is estimated to witness significant growth during the forecast period.

Military thermal weapon sights have gained significant traction in the defense industry due to their ability to enhance targeting capabilities in various combat situations. These advanced sights, such as the AN/PAS-13 Thermal Weapon Sight used by the US Army and Marine Corps, can detect heat signatures up to 1,100 meters away. They are designed to function optimally in all lighting conditions and can be mounted on various rifles and machine guns. Another example is the ATN Thor 4 Smart HD Thermal Rifle Scope, which boasts advanced thermal imaging technology and is compatible with both rifles and crossbows. Digital display technology and scene understanding algorithms are integral components of these thermal weapon sights, ensuring accurate and real-time target identification.

Infrared optics design and uncooled microbolometer arrays contribute to their high thermal sensitivity levels, while image processing algorithms and laser rangefinders facilitate precise targeting. Human-machine interface, battery life performance, and environmental testing procedures are essential considerations to ensure user-friendly and robust designs. Moreover, data encryption protocols, ergonomic design principles, system integration processes, and user interface design are crucial elements that enhance the overall functionality and effectiveness of military thermal weapon sights. Zoom lens functionality, optical magnification levels, wireless communication modules, and durability testing standards further contribute to their versatility and reliability. Power management systems, focus adjustment mechanisms, reticle illumination systems, contrast enhancement methods, automatic target recognition, rangefinding technology, thermal imaging sensors, weapon stabilization systems, target acquisition systems, and resolution and clarity are additional features that make military thermal weapon sights indispensable tools for military personnel.

The Gun-based thermal weapon sights segment was valued at USD 722.00 million in 2019 and showed a gradual increase during the forecast period.

According to recent reports, the market for military thermal weapon sights is projected to grow by 15% in the next year, with an anticipated expansion of 20% over the next five years. These figures reflect the increasing demand for advanced thermal weapon sights in various military applications. The evolving nature of military technology and the continuous development of cutting-edge features are driving the growth and innovation in this market.

Regional Analysis

North America is estimated to contribute 42% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Military Thermal Weapon Sights Market Demand is Rising in North America Request Free Sample

In the market, North America holds a substantial share due to the presence of major players like BAE Systems, Elbit Systems, and Excelitas Technologies. These companies, based in North America, provide advanced thermal weapon sights to cater to the modern military's requirements. The region's leading position is driven by several factors, including growing military modernization investments, escalating threats from hostile entities, and the need to boost situational awareness and combat efficiency.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is characterized by the integration of advanced technologies to enhance target acquisition and situational awareness for defense forces. Uncooled microbolometer array performance characteristics play a pivotal role in delivering high-resolution images for long-range detection, enabling soldiers to identify threats from a distance. Infrared optics design for long-range detection, coupled with image processing algorithms for target recognition, ensures accurate and efficient target identification. Advanced target acquisition systems integrate weapon stabilization systems for thermal weapon sights, ensuring stability during shooting. Digital display technology offers improved situational awareness by providing clear and precise visual information.

Power management optimization is crucial for extended operational time, while environmental testing procedures ensure military-grade durability. Thermal signature detection and classification in varied conditions is a critical requirement, with object recognition software enhancing targeting accuracy. Data encryption protocols and wireless communication module integration facilitate secure data transmission and remote operation. Reticle illumination system brightness and contrast adjustment, zoom lens functionality, and field of view optimization cater to the specific needs of various military applications. Focus adjustment mechanisms ensure improved target clarity, while battery life performance and power consumption reduction contribute to operational efficiency. Weight and size optimization facilitate enhanced portability, and ergonomic design principles improve user comfort.

Optical magnification levels and resolution analysis enable precise target identification in varying weather conditions. Notably, over 70% of new military thermal weapon sight developments focus on enhancing detection range capabilities, reflecting the growing importance of early threat detection in modern warfare. This shift towards extended detection ranges underscores the market's dynamic nature and the constant pursuit of technological advancements to meet the evolving needs of military forces.

What are the key market drivers leading to the rise in the adoption of Military Thermal Weapon Sights Industry?

- The integration of advanced high-definition thermal imaging systems is the primary catalyst fueling market growth.

- High definition (HD) imaging systems have significantly transformed the landscape of various applications by delivering crisp and clear images. This technological advancement holds immense importance in military intelligence and targeting functions, leading to the integration of HD technology in military imaging systems. For instance, HD thermal weapon sights, such as COBRA by Tonbo Imaging, have gained prominence. Built on digital fusion technology, these sights surpass the limitations of optical fusion technology.

- They address challenges like poor contrast, ghosting, and fusion picture subsetting, thereby enabling effective and reliable target recognition, discrimination, and acquisition for operators. The military sector's adoption of HD imaging technology underscores its potential to revolutionize targeting capabilities and enhance operational efficiency.

What are the market trends shaping the Military Thermal Weapon Sights Industry?

- The emergence of wireless thermal weapon sights represents a significant market trend in advanced military technology. Wireless thermal weapon sights are gaining popularity due to their innovative features and capabilities.

- Wireless thermal weapon sights have gained significant traction in the military and law enforcement sectors due to their advanced target detection and identification capabilities. These innovative devices employ cutting-edge technology to deliver clear, detailed imaging, providing a decisive advantage in challenging environments. One such example is the Pulsar Thermion XM50, boasting a high-performance 640 x 480 thermal sensor and a 1,024 x 768 AMOLED display. This combination ensures superior image quality, enabling users to distinguish objects with precision. Moreover, the Pulsar Thermion XM50 is equipped with wireless connectivity, allowing seamless integration with other devices and systems.

- Another noteworthy option is Teledyne Technologies' Breach Thermal Monocular. Weighing less than 7 ounces and compact enough to fit in a pocket, this device offers impressive portability without compromising performance. Both these examples illustrate the continuous evolution of wireless thermal weapon sights, catering to the ever-growing demand for advanced technology in mission-critical applications.

What challenges does the Military Thermal Weapon Sights Industry face during its growth?

- The high cost of producing military thermal weapon sights poses a significant challenge to the growth of the industry. This expense, an inherent aspect of manufacturing these advanced technologies, significantly impacts industry expansion.

- Military thermal weapon sights represent a significant investment due to the intricate manufacturing process that incorporates advanced technology and specialized skills. The primary cost driver is the utilization of sophisticated thermal sensors, which can detect heat signatures from considerable distances. Developing these sensors necessitates the expertise of skilled engineers, given the complex technology involved. Furthermore, the components integrated into the sights, including lenses and circuit boards, are themselves advanced and costly.

- Consequently, the overall manufacturing process results in a high-priced product. The ongoing evolution of thermal sensor technology and its applications across various military sectors underscores the importance and continued relevance of military thermal weapon sights.

Exclusive Technavio Analysis on Customer Landscape

The military thermal weapon sights market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the military thermal weapon sights market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Military Thermal Weapon Sights Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, military thermal weapon sights market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

American Technologies Network Corp. - The company specializes in military thermal weapon sights, including the advanced ATN THOR 4 model.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- American Technologies Network Corp.

- ASELSAN AS

- BAE Systems Plc

- BERETTA HOLDING SA

- Elbit Systems Ltd.

- Excelitas Technologies Corp.

- General Starlight Co. Inc.

- Hensoldt AG

- L3Harris Technologies Inc.

- Leonardo Spa

- Materion Corp.

- Patria Group

- Raytheon Technologies Corp.

- Rheinmetall AG

- Safran SA

- Schmidt and Bender GmbH and Co. KG

- SIG Sauer Inc.

- Teledyne Technologies Inc.

- Thales Group

- Thermoteknix Systems Ltd.

- Tonbo Imaging India Pvt Ltd.

- Trijicon Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Military Thermal Weapon Sights Market

- In January 2024, Lockheed Martin Corporation announced the successful integration of its Advanced Thermal Imaging System (ATIS III) into the U.S. Army's M2A3 Bradley Fighting Vehicle. This integration marked a significant advancement in thermal weapon sights technology for military ground vehicles (Lockheed Martin Corporation Press Release, 2024).

- In March 2024, Elbit Systems and Thales announced a strategic partnership to develop and manufacture advanced thermal weapon sights for various military applications. This collaboration aimed to combine Elbit Systems' expertise in thermal imaging technology and Thales' experience in defense electronics (Elbit Systems Press Release, 2024).

- In April 2025, FLIR Systems, a leading provider of thermal imaging and sensing technologies, secured a USD 25 million contract from the U.S. Army to deliver its PTS 233 thermal weapon sight systems. This contract marked a significant expansion of FLIR's presence in the market (FLIR Systems Press Release, 2025).

- In May 2025, Leonardo DRS announced the successful completion of the first production run of its Integrated Day/Night Sight System (IDNSS) for the U.S. Marine Corps. This milestone marked a significant achievement in the development and deployment of advanced thermal weapon sights for military helicopters (Leonardo DRS Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Military Thermal Weapon Sights Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

203 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.4% |

|

Market growth 2025-2029 |

USD 504.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.8 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is characterized by continuous advancements in digital display technology, scene understanding, and infrared optics design. Uncooled microbolometer arrays, a key component of these sights, have seen significant improvements in thermal sensitivity levels, enabling enhanced detection range capabilities. Image processing algorithms and laser rangefinders have also evolved, providing more accurate and reliable data to users. Human-machine interface design plays a crucial role in the market, with ergonomic principles guiding the development of user-friendly systems. Battery life performance is another essential consideration, with manufacturers focusing on power management systems and efficient design to extend operational hours. Environmental testing procedures and durability testing standards ensure these thermal weapon sights can withstand harsh conditions, while data encryption protocols maintain security.

- System integration processes and user interface design continue to evolve, incorporating zoom lens functionality, optical magnification levels, and wireless communication modules. Reticle illumination systems and contrast enhancement methods provide improved target acquisition, with automatic target recognition and rangefinding technology further enhancing situational awareness. Thermal imaging sensors and weapon stabilization systems work in tandem to provide accurate and stable thermal signatures, while object recognition software allows for quick identification of targets. Resolution and clarity have seen significant improvements, with thermal sensitivity levels enabling the detection of smaller thermal signatures. Detection range capabilities have also expanded, allowing for greater situational awareness and effective target engagement.

- Overall, the market continues to evolve, with manufacturers focusing on advanced technology and user experience to meet the demands of military applications.

What are the Key Data Covered in this Military Thermal Weapon Sights Market Research and Growth Report?

-

What is the expected growth of the Military Thermal Weapon Sights Market between 2025 and 2029?

-

USD 504.7 million, at a CAGR of 7.4%

-

-

What segmentation does the market report cover?

-

The report segmented by Type (Gun-based thermal weapon sights, Vehicle-mounted thermal weapon sights, Handheld Thermal Weapon Sights, Helmet-Mounted Thermal Weapon Sights, and Clip-On Thermal Weapon Sights), Application (Army, Maritime, and Land), Geography (North America, APAC, Europe, Middle East and Africa, South America, and Rest of World (ROW)), Technology (Cooled Thermal and Uncooled Thermal), and Product Type (Clip-On Sights, Standalone Sights, and Integrated Systems)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Introduction of high-definition thermal imaging systems, High cost associated with production of military thermal weapon sights

-

-

Who are the major players in the Military Thermal Weapon Sights Market?

-

Key Companies American Technologies Network Corp., ASELSAN AS, BAE Systems Plc, BERETTA HOLDING SA, Elbit Systems Ltd., Excelitas Technologies Corp., General Starlight Co. Inc., Hensoldt AG, L3Harris Technologies Inc., Leonardo Spa, Materion Corp., Patria Group, Raytheon Technologies Corp., Rheinmetall AG, Safran SA, Schmidt and Bender GmbH and Co. KG, SIG Sauer Inc., Teledyne Technologies Inc., Thales Group, Thermoteknix Systems Ltd., Tonbo Imaging India Pvt Ltd., and Trijicon Inc.

-

Market Research Insights

- The market encompasses advanced technologies designed to enhance soldiers' situational awareness and improve target engagement in various operational environments. Two key performance metrics differentiate leading thermal weapon sights: power efficiency and long-range sighting capabilities. For instance, a modern thermal sight may consume as little as 1 watt of power, providing up to 12 hours of continuous operation. In contrast, high-end models can offer long-range sighting capabilities up to 2,000 meters, enabling accurate target identification and engagement. Power efficiency and long-range sighting capabilities are crucial aspects of military thermal weapon sights, as they contribute to operational reliability, extended battery life, and overall mission success.

- Other essential features include image stabilization, object classification, and sensor fusion for improved target recognition. Thermal weapon sights also prioritize environmental protection, data security, and user interface optimization. Technologies like microbolometer and infrared detection, along with calibration methods and high-resolution displays, ensure precise targeting and background clutter reduction. Maintenance procedures and performance metrics are also essential considerations for ensuring the operational readiness of these advanced systems.

We can help! Our analysts can customize this military thermal weapon sights market research report to meet your requirements.

RIA -

RIA -