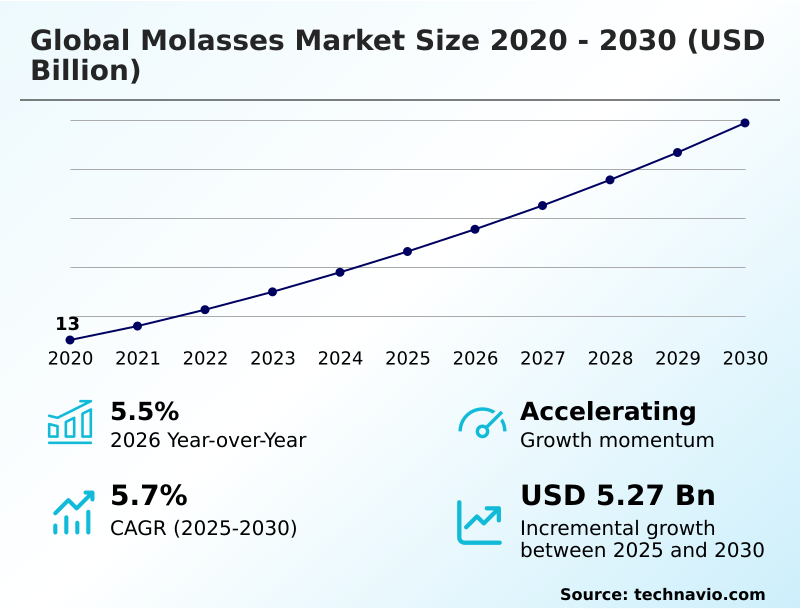

Molasses Market Size 2026-2030

The molasses market size is valued to increase by USD 5.27 billion, at a CAGR of 5.7% from 2025 to 2030. Rising global demand for bioethanol and renewable fuel mandates will drive the molasses market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 63.1% growth during the forecast period.

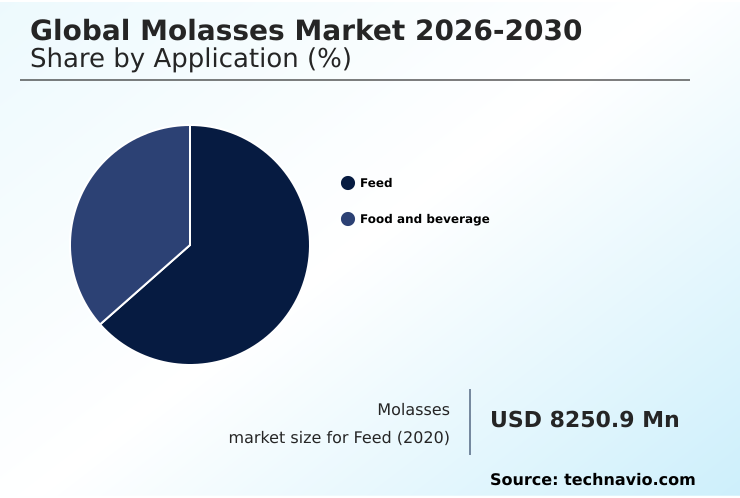

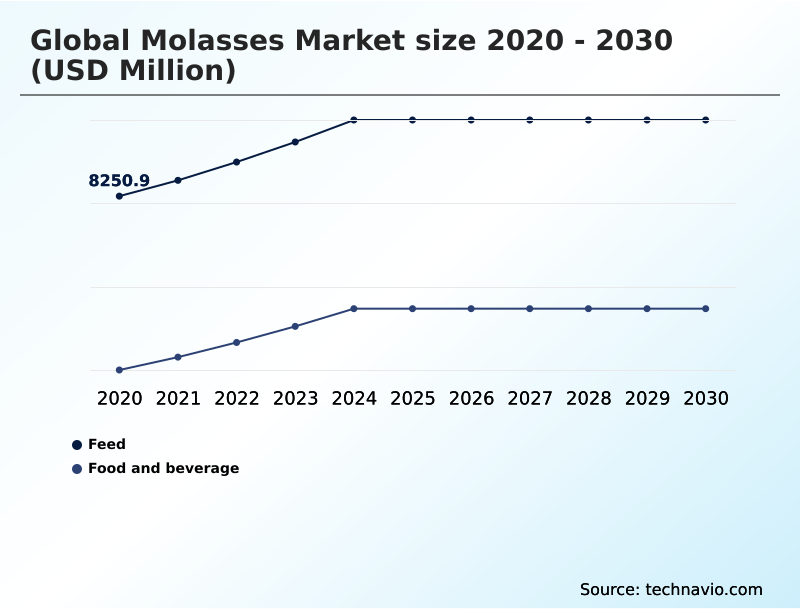

- By Application - Feed segment was valued at USD 9.79 billion in 2024

- By Type - Blackstrap molasses segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 8.89 billion

- Market Future Opportunities: USD 5.27 billion

- CAGR from 2025 to 2030 : 5.7%

Market Summary

- The molasses market is shaped by its integral role as a byproduct in sugar refining and its diverse applications across industries. A primary driver is the global push for renewable energy, where molasses serves as a critical bioethanol feedstock for biofuel production. Concurrently, the animal feed sector relies on it as a palatability enhancer and energy supplement.

- A key trend involves the market's bifurcation, with high-value, food-grade molasses for clean-label food processing decoupling from the commodity feed-grade market. However, the industry faces challenges from climatic volatility impacting sugarcane yields and regulatory policies that divert supply toward government-mandated fuel programs.

- For instance, a business focused on the circular bioeconomy might leverage specialty molasses streams in precision fermentation to produce high-margin bioplastics, navigating supply chain risks by securing long-term contracts for organic molasses certified material. This strategy turns a traditional commodity into a cornerstone of sustainable industrial innovation, highlighting the market's shift toward value-added derivatives and advanced bio-manufacturing.

What will be the Size of the Molasses Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Molasses Market Segmented?

The molasses industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Feed

- Food and beverage

- Type

- Blackstrap molasses

- Regular molasses

- Source

- Sugarcane

- Sugar

- Others

- Geography

- APAC

- India

- China

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Application Insights

The feed segment is estimated to witness significant growth during the forecast period.

The molasses market is segmented by its core applications, with animal feed representing the dominant segment. The use of molasses as an animal feed supplement is driven by its function as a feed palatability enhancer and a liquid feed binder.

Its high brix content offers a cost-effective energy source in ruminant nutrition, improving digestion. While APAC accounts for 63.1% of market opportunities, North America's robust livestock industry creates substantial demand. Manufacturers utilize feed-grade molasses as a pelleting process aid.

This versatile sugarcane byproduct, including specific types like beet molasses, is essential for optimizing feed formulations, acting as a refined sugar substitute and ensuring consistent nutritional intake for livestock, making sustainable molasses sourcing a key consideration for industrial buyers.

The Feed segment was valued at USD 9.79 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

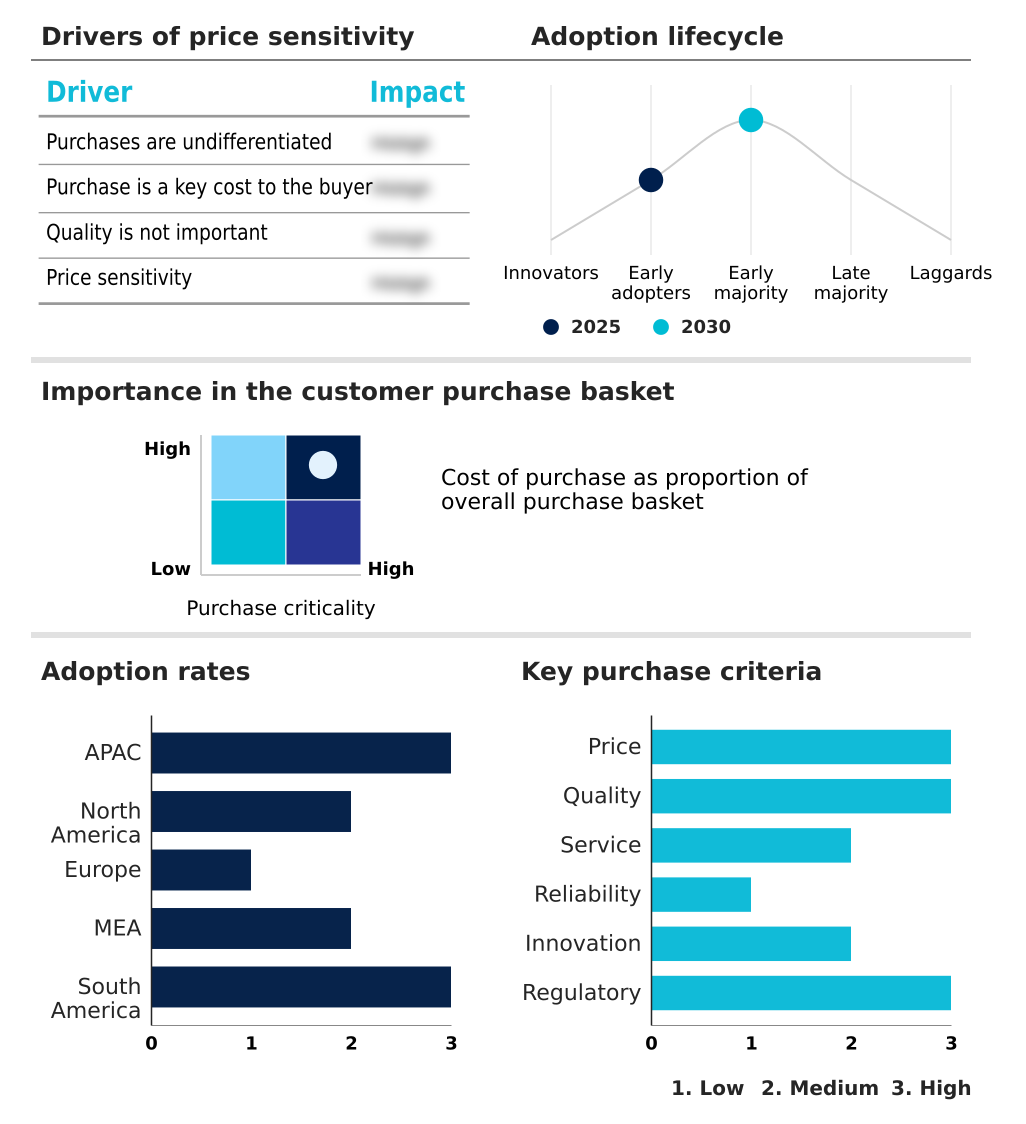

APAC is estimated to contribute 63.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Molasses Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the molasses market is dominated by APAC, which represents 63.1% of the global opportunity, driven by large-scale sugarcane cultivation in countries like India and Thailand.

In this region, molasses is a critical bioethanol feedstock, supporting national renewable energy programs. North America, representing 23.64% of the opportunity, is a major consumption market, primarily using molasses as an animal feed supplement and liquid feed binder.

Europe is focused on high-value applications, integrating beet molasses and cane molasses into its circular bioeconomy as a green chemistry feedstock and a key component in precision fermentation. The molasses mineral profile makes it valuable in organic feed formulations globally.

This regional specialization influences molasses import-export flows, with molasses storage and handling logistics being critical for connecting production hubs with consumption centers.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global molasses market is defined by a complex interplay of grades, sources, and applications, influencing everything from industrial processes to consumer products. Understanding the nuances when comparing blackstrap vs regular molasses is critical for procurement, as each offers different levels of fermentable sugars and mineral content.

- Using molasses in animal feed remains the largest volume application, where its impact on feed palatability is a key purchasing driver. Molasses as a bioethanol feedstock is a major driver, with government mandates creating dedicated demand streams. Meanwhile, the benefits of organic molasses are being leveraged in premium food and health markets.

- Fluctuations in molasses price per metric ton are closely watched by buyers in sectors from baking to chemical production. The impact of molasses on soil health is an emerging application in sustainable agriculture. For food producers, using food grade molasses for baking offers a clean-label sweetener solution.

- Molasses sourcing from sugarcane is the dominant production method, but industrial uses of beet molasses are crucial in temperate climates. Its role in rum production is historical and continues in the craft spirits sector. Sustainable sourcing of molasses is becoming a key differentiator, alongside best practices for molasses storage to maintain quality.

- As a clean-label sweetener, it replaces refined sugars, though regulatory impact on molasses supply can create volatility. For industrial biotechnology, it serves as a preferred fermentation substrate. Companies continually evaluate molasses alternatives in animal feed, while producers invest in advanced molasses clarification techniques.

- Ultimately, the market is trending toward molasses for high-value bio-manufacturing, transforming it from a simple byproduct into a strategic industrial input.

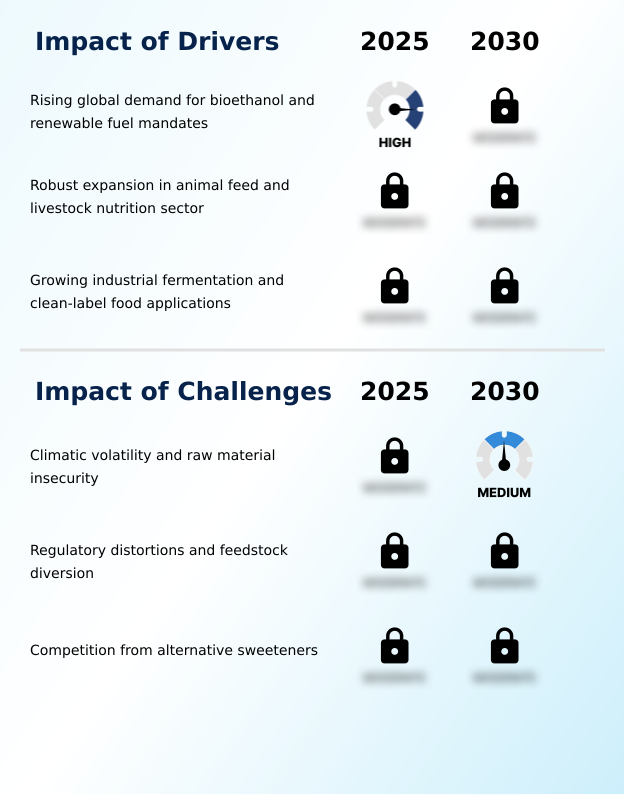

What are the key market drivers leading to the rise in the adoption of Molasses Industry?

- The rising global demand for bioethanol, driven by mandates for renewable fuels, serves as a key driver for the market.

- The market's growth is primarily driven by government-led renewable energy mandates and sustained demand from the livestock industry.

- The mandated blending of bioethanol with gasoline, which can improve fuel octane ratings by up to 3%, has positioned molasses as a strategic bioethanol feedstock.

- Major economies are aggressively pursuing targets, with some aiming for a 20% ethanol blend, creating a massive, reliable demand channel for fermentable sugars. Simultaneously, the animal nutrition sector's reliance on molasses as a key animal feed supplement remains robust.

- Its use as a feed palatability enhancer contributes to improved livestock health and productivity, with feedlot operators consistently procuring it despite price surges.

- This dual demand from energy and agriculture, which includes its use as a soil microbial stimulant, solidifies the market's strong foundation.

What are the market trends shaping the Molasses Industry?

- The market is witnessing a significant trend toward the integration of precision fermentation. This shift is driving the adoption of advanced bio-manufacturing processes for high-value applications.

- A primary trend is the market's bifurcation into commodity and specialty segments. While molasses for potable alcohol remains a high-volume application, the growth is in high-value uses. The demand for specialty molasses streams in clean-label food processing is surging, with premium molasses blends commanding prices over ten times higher than standard feed-grade molasses.

- This is driven by their use as a natural sweetener and natural food coloring, aligning with consumer preferences. Concurrently, the integration of molasses in bio-manufacturing and precision fermentation is transforming it into a strategic industrial input.

- This shift is supported by significant capital injections, with one recent initiative dedicating substantial funding to scale up fermentation infrastructure, reducing dependency on petrochemical-based products by over 15%. This trend influences traditional sweetener applications and molasses for craft beverages.

What challenges does the Molasses Industry face during its growth?

- Climatic volatility, which leads to raw material insecurity, poses a key challenge to the industry's growth.

- The most significant market challenge is supply chain vulnerability stemming from climatic volatility and regulatory distortions. Unpredictable weather patterns directly impact sugarcane yields and the total recoverable sugar (atr) content, with a 5% drop in tons of cane per hectare (tch) in a major producing region creating immediate global supply tightness.

- This agricultural uncertainty is compounded by government policies that divert blackstrap molasses toward biofuel production to meet blending targets, such as a 20% mandate. This policy-driven demand creates artificial scarcity for traditional users in the food and feed industries, forcing them to compete with a price floor set by the energy sector.

- Consequently, users of molasses for yeast production nutrient or as a high-fructose corn syrup alternative face heightened price volatility and raw material insecurity, impacting production costs.

Exclusive Technavio Analysis on Customer Landscape

The molasses market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the molasses market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Molasses Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, molasses market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Archer Daniels Midland Co. - Offerings include diverse molasses grades, such as cane and beet molasses, catering to industrial fermentation, animal nutrition, and food and beverage applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Archer Daniels Midland Co.

- Associated British Foods Plc

- B and G Foods Inc.

- Cargill Inc.

- Cora Texas Manufacturing Co.

- Cosan SA

- Cosun Beet Co.

- Crosby Molasses Co. Ltd.

- Florida Crystals Corp.

- Imperial Sugar Co.

- Louis Dreyfus Co. BV

- Malt Products Corp.

- Michigan Sugar Co.

- Mitr Phol Group

- Nordzucker AG

- Sudzucker AG

- Tereos SCA

- Wilmar International Ltd.

- Zook AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Molasses market

- In August, 2024, the government of India relaxed restrictions, allowing sugar mills to produce ethanol from sugarcane juice and various molasses grades to advance its 20% blending objective.

- In February, 2025, Nordzucker AG successfully concluded an extended 2024-2025 production campaign in Germany, achieving high beet yields that ensured a stable supply of molasses for feed and fermentation industries.

- In April, 2025, Brazil's National Supply Company (Conab) released its initial forecast for the 2025-2026 crop cycle, indicating a strategic focus on ethanol output despite challenging weather conditions.

- In May, 2025, Tereos announced its Brazilian operations maintained stable sugarcane crushing volumes for the 2024-2025 harvest, matching previous records and securing molasses availability for export markets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Molasses Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.7% |

| Market growth 2026-2030 | USD 5267.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.5% |

| Key countries | India, China, Thailand, Japan, South Korea, Australia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Saudi Arabia, South Africa, Egypt, UAE, Nigeria, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The molasses market operates as a critical nexus between agriculture and industry, with its value derived from its role as a versatile sugarcane byproduct. Key applications include its use as a bioethanol feedstock and an essential animal feed supplement. The industry is navigating a structural shift, where this viscous byproduct refining is increasingly seen as a circular bioeconomy input.

- For instance, a regulatory change in one region mandating a shift in allocation from 19% to 25% for potable alcohol production directly impacts the availability of this green chemistry feedstock for other sectors, a risk factor that must be addressed in corporate strategic planning. The composition, including sucrose concentration and total recoverable sugar (atr), dictates its utility.

- From its role as a rum distillation substrate to a bioplastic precursor, the applications are expanding. Boardroom decisions are increasingly focused on supply chain resilience, considering factors like heated storage terminals and tons of cane per hectare (tch) yields. The push for clean-label ingredients is elevating certain grades as a high-fructose corn syrup alternative.

- This dynamic requires a sophisticated understanding of everything from its function as a dust suppressant agent to its classification as an organic molasses certified product.

What are the Key Data Covered in this Molasses Market Research and Growth Report?

-

What is the expected growth of the Molasses Market between 2026 and 2030?

-

USD 5.27 billion, at a CAGR of 5.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Feed, and Food and beverage), Type (Blackstrap molasses, and Regular molasses), Source (Sugarcane, Sugar, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rising global demand for bioethanol and renewable fuel mandates, Climatic volatility and raw material insecurity

-

-

Who are the major players in the Molasses Market?

-

Archer Daniels Midland Co., Associated British Foods Plc, B and G Foods Inc., Cargill Inc., Cora Texas Manufacturing Co., Cosan SA, Cosun Beet Co., Crosby Molasses Co. Ltd., Florida Crystals Corp., Imperial Sugar Co., Louis Dreyfus Co. BV, Malt Products Corp., Michigan Sugar Co., Mitr Phol Group, Nordzucker AG, Sudzucker AG, Tereos SCA, Wilmar International Ltd. and Zook AG

-

Market Research Insights

- Market dynamics are increasingly influenced by the dual demand for both high-volume industrial feedstocks and high-value food ingredients. The utilization of molasses for biofuel production is a significant factor, with its efficiency in fermentation processes showing a 10% higher yield compared to some grain-based alternatives.

- Concurrently, the demand for molasses in artisanal foods and craft beverages is reshaping procurement strategies, as food-grade molasses can command a price premium of over 25% compared to feed-grade molasses. This price differential is driving a focus on molasses quality parameters and sustainable molasses sourcing.

- End-users are also exploring molasses in aquaculture and as a soil amendment, expanding its application profile. The molasses regulatory framework continues to evolve, influencing molasses supply chain and price dynamics globally, particularly in organic feed formulations where traceability is paramount.

We can help! Our analysts can customize this molasses market research report to meet your requirements.

RIA -

RIA -