North America Wood Coatings Market Size 2024-2028

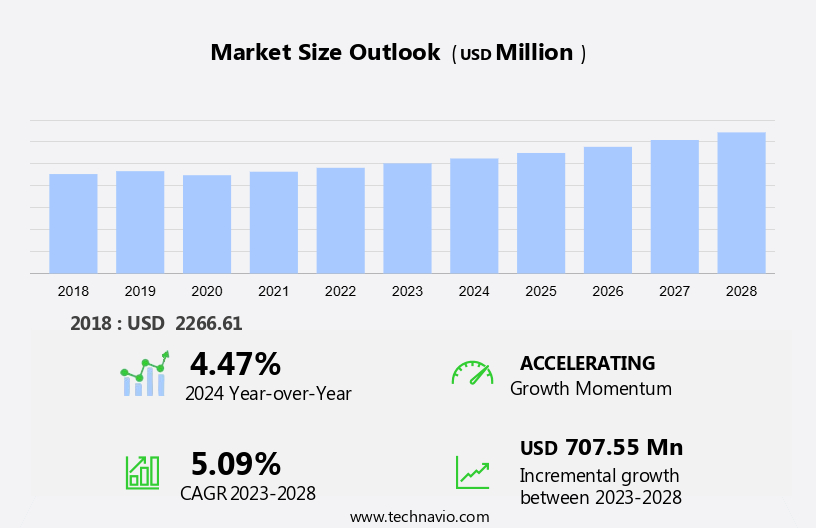

The North America wood coatings market size is forecast to increase by USD 707.55 million at a CAGR of 5.09% between 2023 and 2028.

- In the dynamic wood coatings market, three key drivers are shaping its growth trajectory. Firstly, the increasing adoption of renewable and sustainable raw materials is a significant trend, as environmental concerns gain prominence. Secondly, user-friendly DIY wood coating products are gaining traction due to their convenience and cost-effectiveness. These coatings offer benefits like moisture resistance, UV protection, and resistance to air pollution, ensuring the longevity of furniture in residential spaces, hotels, corporate offices, and the furniture rental industry. Lastly, constantly evolving standards and regulations for wood coatings necessitate continuous innovation and compliance. These factors, in conjunction, present both opportunities and challenges for market participants. Adhering to regulatory requirements while maintaining product quality and affordability is a delicate balance that requires strategic planning and agility. Consequently, the market is poised for growth, driven by these evolving market dynamics.

What will be the size of the North America Wood Coatings Market during the forecast period?

- The market plays a significant role In the furniture industry, enhancing the visual appeal of various furniture items such as beds, chairs, shelves, tables, cabinets, and more. Wood coating technologies, including nanotechnology, UV-curable coatings, and water-based coatings, contribute to the production of durable and aesthetically pleasing furniture. The furniture manufacturing sector relies heavily on wood coatings for housing construction and office furniture production. Traditional solvent-based coatings have been commonly used, but the market is shifting towards eco-friendly and health-conscious alternatives due to concerns about adverse health effects and transportation disruptions. The market is expected to grow, driven by the increasing demand for sustainable and high-performance coatings.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Stains and varnishes

- Shellacs

- Wood preservatives

- Others

- Technology

- Solvent-based

- Water-based

- Others

- Geography

- North America

- Canada

- Mexico

- US

- North America

By Product Insights

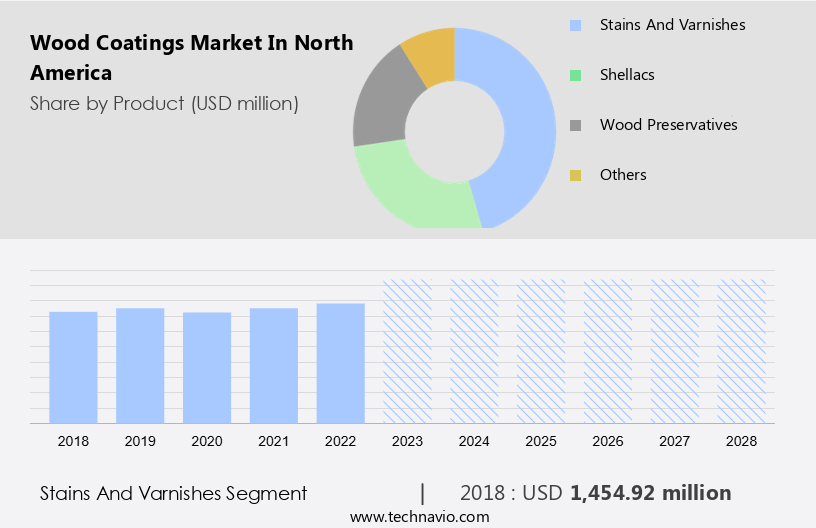

- The stains and varnishes segment is estimated to witness significant growth during the forecast period. The indoor air quality consciousness of consumers in North America fuels the growth of the market, particularly in home renovation projects. DIY enthusiasts also contribute to the demand in the production and manufacturing of wood furniture and interior decoration projects. Aesthetic appeal and visual appeal are significant factors driving the preference for various colors and finishes in wooden furniture, including high-traffic environments such as hotels, corporate offices, and residential spaces. Moisture resistance and UV protection are essential features of wood coatings, making them indispensable in furniture production and manufacturing.

- Temperature fluctuations and durability are also critical considerations In the selection of protective layers for wooden products, including cupboards, dining sets, beds, chairs, shelves, tables, and cabinets. The market caters to various industries, including furniture stores and rental industries, where the demand for office furniture, household furniture, and wooden products remains high. High-rise buildings and other commercial constructions also require wood coatings for their wooden surfaces, ensuring their longevity and resistance to wear and tear. In summary, the market is thriving due to the increasing demand for customized and personalized home decor, the importance of indoor air quality, and the need for moisture resistance, UV protection, and durability in wooden furniture and surfaces.

Get a glance at the market share of various segments Request Free Sample

- The stains and varnishes segment was valued at USD 1.45 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of North America Wood Coatings Market?

- The growing use of renewable and sustainable raw materials is the key driver of the market. The market is witnessing significant advancements as manufacturers focus on developing eco-friendly formulations to combat rot, decay, and wear and tear in outdoor applications. These innovative coatings cater to various sectors, including fences, decks, home décor, and flooring and decking In the wooden decking market.

- By incorporating bio-based resins and low-volatile organic compound (VOC) waterborne coatings, manufacturers ensure superior performance characteristics without compromising the environment. In North America, companies successfully integrating sustainable raw materials into their products can distinguish themselves, as eco-friendly labels and certifications, such as GreenGuard, LEED, and others, boost brand reputation and attract environmentally conscious consumers and businesses. Technological progress has led to the creation of bio-based resins, solvents, and additives derived from renewable sources, like plants, algae, and biomass, further enhancing the market's growth.

What are the market trends shaping the North America Wood Coatings Market?

- Growing adoption of user-friendly DIY wood coating products is the upcoming trend in the market. The market is experiencing significant growth due to the increasing trend of DIY home improvement projects. Consumers are seeking out wood coating solutions that are simple to apply, even for those without extensive experience in woodworking or painting. Clear instructions on packaging, user-friendly application methods such as brushing or spraying, and minimal prep work requirements are essential selling points. Moreover, the demand for wood coatings extends beyond structural applications like fences and decks, as they are also used for enhancing home décor and aesthetics. In the flooring and decking sector, the wooden decking market is a significant contributor to the demand for wood coatings.

- Outdoor applications, particularly in regions with harsh weather conditions, require wood coatings with superior performance characteristics. Resin-based, solvent-borne coatings have traditionally been popular for their durability against rot, decay, and wear and tear. However, the shift towards eco-friendly and low-odor alternatives, such as water-borne paints and coatings, is gaining momentum. These coatings offer self-priming properties and one-coat coverage, making them ideal for smaller-scale DIY projects like refinishing furniture or painting cabinets. Wood coating manufacturers in North America are catering to this trend by introducing dedicated lines of DIY wood coatings with features that ensure faster project completion and excellent results.

What challenges does North America Wood Coatings Market face during the growth?

- Constantly changing standards and regulations for wood coatings is a key challenge affecting the market growth. The wood coatings market is subject to rigorous regulations aimed at limiting Volatile Organic Compound (VOC) emissions, with organizations such as the Environmental Protection Agency (EPA) and Environment and Climate Change Canada (ECCC) enforcing these standards. These regulations necessitate the innovation and development of low-VOC or VOC-free formulations to prevent rot, decay, and wear and tear in outdoor applications, including fences, decks, and home décor.

- As sustainability criteria expand, manufacturers must also consider the use of renewable resources, recyclability, and overall environmental impact. Certifications like Leadership in Energy and Environmental Design (LEED) further influence product development. Superior performance characteristics, such as resistance to water and UV light, are essential for flooring and decking In the wooden decking market. Resin-based, solvent-borne paints and coatings are being replaced with water-borne alternatives to meet these evolving requirements and ensure the continued safety and health of consumers.

Exclusive North America Wood Coatings Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Akzo Nobel NV

- Arkema Group

- Axalta Coating Systems Ltd.

- BASF SE

- Berkshire Hathaway Inc.

- Cabot Corp.

- Dow Chemical Co.

- Eastman Chemical Co.

- Engineered Polymer Solutions and Color Corporation of America

- Evonik Industries AG

- Kansai Paint Co. Ltd.

- Katilac Coatings

- Koppers Holdings Inc.

- Lanxess AG

- Nippon Paint Holdings Co. Ltd.

- PPG Industries Inc.

- RPM International Inc.

- SAICOS Canada

- The Sherwin Williams Co.

- W. R. Grace and Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The wood coatings market encompasses the production, sale, and application of coatings used to protect and enhance the aesthetic value of various wood types. These coatings are essential In the construction, furniture, and decor industries. The demand for wood coatings is driven by factors such as increasing urbanization, rising disposable income, and growing awareness of the importance of maintaining the durability and appearance of wood surfaces. Wood coatings come in various types, including water-based, solvent-based, and powder coatings. Each type offers unique benefits, such as ease of application, quick drying time, and high resistance to wear and tear. The choice of coating type depends on the specific application and desired properties.

The global Wood Coatings market is expected to grow significantly due to the increasing demand for sustainable and eco-friendly coatings. The use of renewable raw materials and the development of advanced technologies to improve the performance and durability of wood coatings are key trends driving market growth. Wood coatings are applied through various methods, including brushing, rolling, spraying, and dipping. The choice of application method depends on the size and complexity of the project, as well as the desired finish and coating thickness. Thus, the Wood Coatings market is a dynamic and growing industry, driven by the increasing demand for high-performance, sustainable, and eco-friendly coatings. The market offers various types and application methods to cater to the diverse needs of the construction, furniture, and decor industries.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

169 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.09% |

|

Market growth 2024-2028 |

USD 707.55 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.47 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -