Optical Biometry Devices Market Size 2026-2030

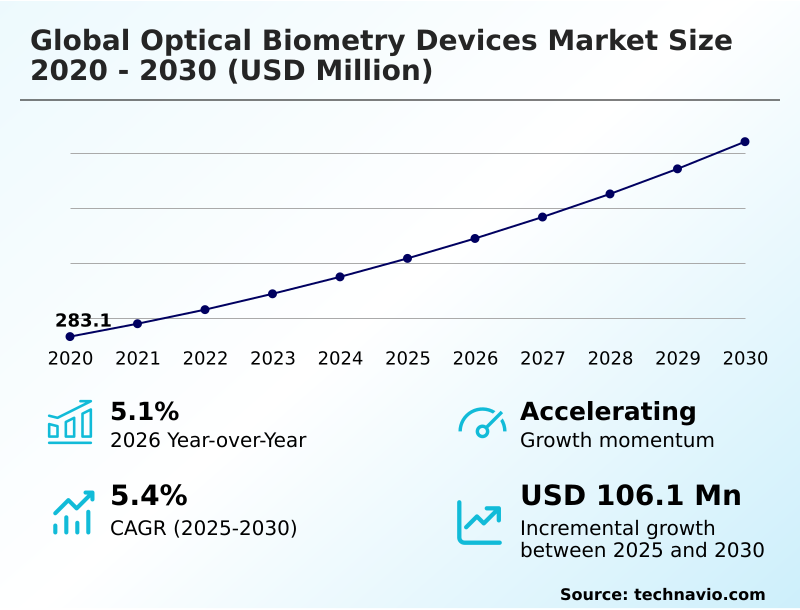

The optical biometry devices market size is valued to increase by USD 106.1 million, at a CAGR of 5.4% from 2025 to 2030. Rise in prevalence of cataract among geriatric population will drive the optical biometry devices market.

Major Market Trends & Insights

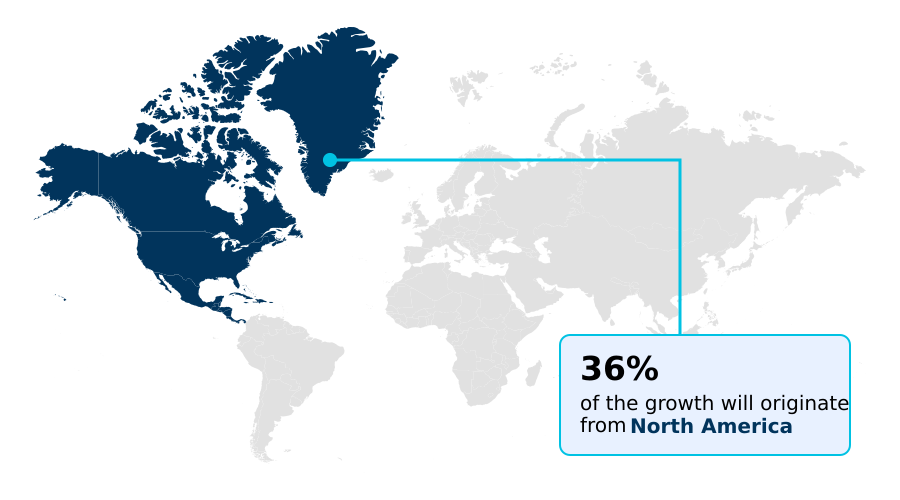

- North America dominated the market and accounted for a 35.6% growth during the forecast period.

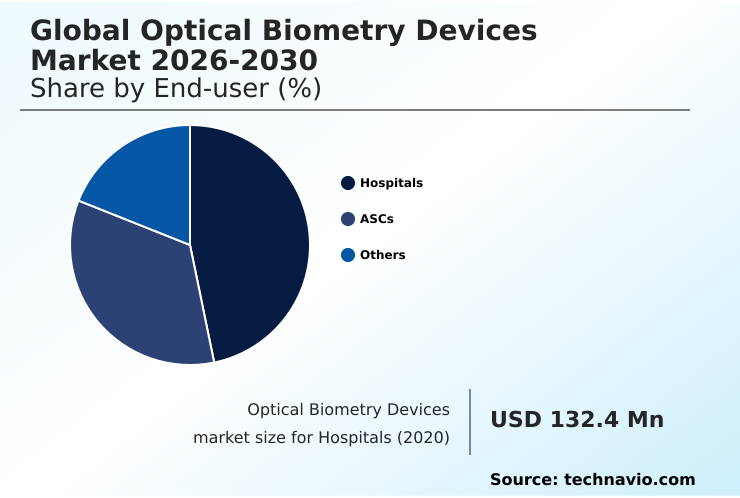

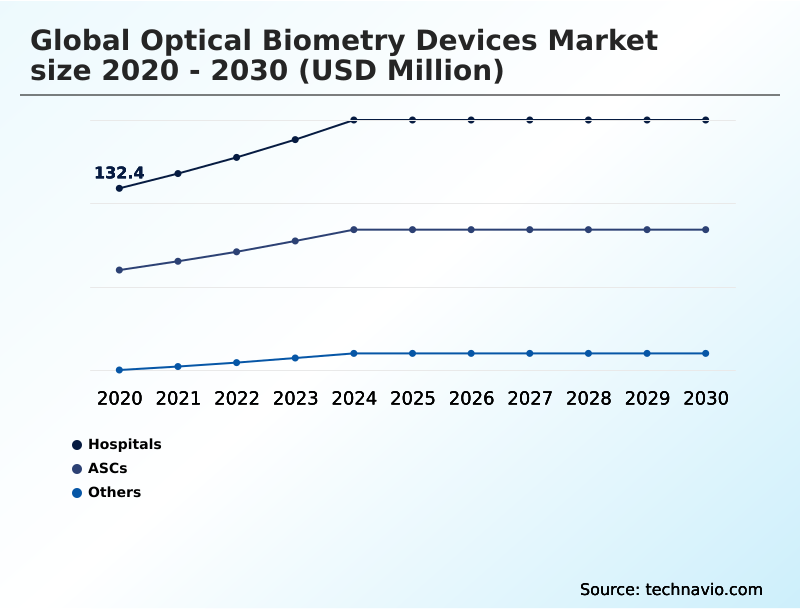

- By End-user - Hospitals segment was valued at USD 162 million in 2024

- By Product - SS-OCT-based optical biometers segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 177.2 million

- Market Future Opportunities: USD 106.1 million

- CAGR from 2025 to 2030 : 5.4%

Market Summary

- The optical biometry devices market is defined by the pursuit of surgical precision and improved clinical workflows. A primary driver is the increasing volume of cataract surgeries, which demands accurate preoperative assessments to meet patient expectations for excellent visual outcomes, especially with premium intraocular lenses.

- Technological evolution is a dominant trend, with a clear migration from traditional ultrasound methods to non-contact optical technologies that offer superior accuracy and patient comfort. Devices now integrate multiple functionalities, moving beyond simple measurements to provide comprehensive ocular analysis.

- For instance, a high-volume ambulatory surgical center must weigh the investment in a new biometer against its ability to streamline patient flow, reduce measurement time, and provide the robust data needed for complex refractive calculations, thereby ensuring both operational efficiency and clinical excellence.

- However, the market is not without its challenges; supply chain vulnerabilities for critical optical components and the inherent limitations of technology in eyes with dense media opacities constrain universal adoption and create pressures on manufacturing and pricing.

What will be the Size of the Optical Biometry Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Optical Biometry Devices Market Segmented?

The optical biometry devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hospitals

- ASCs

- Others

- Product

- SS-OCT-based optical biometers

- OLCR-based optical biometers

- PCI-based optical biometers

- Product type

- Non-contact type

- Contact type

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

Hospitals represent a cornerstone of the optical biometry devices market, driven by high surgical volumes and the need for precision in complex cases.

These facilities require robust systems for accurate intraocular lens calculation and phacoemulsification planning to ensure optimal postoperative refractive outcome. The integration of high-resolution cross-sectional imaging and automated keratometry supports superior refractive error analysis and toric IOL alignment.

Advanced biometric data management platforms are essential for handling measurements like axial length measurement, corneal curvature, anterior chamber depth, lens thickness measurement, and white-to-white distance.

By leveraging precise intraocular lens calculation, facilities report a reduction in postoperative refractive surprises by up to 30%, improving both patient satisfaction and operational efficiency within ophthalmology departments.

The Hospitals segment was valued at USD 162 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Optical Biometry Devices Market Demand is Rising in North America Get Free Sample

The market's geographic landscape is led by North America, which is projected to contribute over 35% of incremental growth, driven by advanced healthcare infrastructure and high adoption of technologies like swept-source optical coherence tomography.

Europe shows a strong growth trajectory, expanding faster than North America, with a focus on non-contact tonometry and wavefront aberrometry.

Meanwhile, Asia is emerging as a high-growth region due to rising healthcare expenditure and a focus on improving ocular surface analysis and pachymetry mapping.

Across regions, there is a consistent demand for precise pupil diameter measurement and tools to assess posterior corneal astigmatism, reflecting a global push for higher standards in ophthalmic diagnostics.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Achieving optimal surgical outcomes in the global optical biometry devices market 2026-2030 hinges on addressing nuanced clinical challenges. The accuracy of non-contact optical biometry is paramount, particularly for optical biometry for premium iol selection, where even minor errors can impact patient satisfaction.

- A key industry debate involves comparing ss-oct and olcr biometry, with facilities evaluating which technology best manages the challenges in dense cataract biometry. Furthermore, the growing population of patients with prior refractive surgery makes optical biometry in post-lasik eyes a critical capability, requiring specialized calculation formulas.

- Workflow efficiency with automated biometers is a major consideration for high-volume clinics, as is the continuous need for intraocular lens constant optimization to refine results. Specialized applications, such as biometry for pediatric ophthalmology, demand unique instrument features and operator skill. The role of ai in iol power calculation is transformative, aiming to significantly reduce the incidence of postoperative refractive surprise.

- Success in reducing refractive surprise with biometry depends on a holistic approach that includes ss-oct versus pci accuracy comparison for different cases, precise planning for biometry for toric lens implantation, and effectively managing irregular corneas with biometry. Clinicians must also account for the impact of dry eye on biometry.

- The ability to perform posterior capsule opacification measurement and integrate biometry with femtosecond lasers represents the next frontier. Ultimately, biometry data for refractive surgery planning underscores the technology's expanding scope. Facilities adopting comprehensive biometric data analysis report up to 50% greater consistency in surgical outcomes.

- The cost-effectiveness of advanced biometers, the potential of tele-ophthalmology and remote biometry, and the constant need for validating new iol calculation formulas will continue to shape procurement and clinical practice.

What are the key market drivers leading to the rise in the adoption of Optical Biometry Devices Industry?

- The rising prevalence of cataracts among the geriatric population is a key driver for the optical biometry devices market.

- A key driver is the pursuit of superior surgical precision, supported by advanced software and algorithms. The adoption of ray tracing technology and sophisticated point spread function analysis is improving the refractive predictability enhancement of modern biometers.

- These systems are moving beyond legacy haigis and srk/t formulas to incorporate newer models like the barrett universal ii formula and olsen formula, which are refined by machine learning algorithms.

- This evolution facilitates a more streamlined diagnostic workflow, with integrated electronic medical record connectivity improving data management.

- The emphasis on measurement repeatability and preoperative assessment precision helps reduce optical signal attenuation issues, leading to a 20% improvement in measurement success rates in challenging eyes.

What are the market trends shaping the Optical Biometry Devices Industry?

- A significant market trend is the rise in technological advances within optical biometry devices. These innovations are enhancing measurement accuracy and streamlining clinical workflows.

- Technological advancements are a primary trend, with a notable shift toward systems utilizing partial coherence interferometry and optical low-coherence reflectometry. These platforms offer enhanced astigmatism analysis and precise z-axis position tracking. Innovations in corneal topography integration and anterior segment tomography provide comprehensive ocular assessments, including retinal thickness analysis and measurement of lens tilt and decentration.

- The focus on operator-independent alignment and dynamic cyclotorsion compensation has improved high-speed data acquisition, with some systems achieving a 15% faster scan time. Furthermore, superior signal-to-noise ratio optimization and digital imaging integration are streamlining workflows, contributing to more efficient and reliable diagnostics in modern ophthalmology practices.

What challenges does the Optical Biometry Devices Industry face during its growth?

- Supply chain disruptions and stringent quality control requirements present key challenges affecting industry growth.

- Key market challenges stem from technological limitations and data management complexities. Overcoming issues related to ocular media opacity remains a hurdle for many interferometry-based systems, requiring frequent biometry device calibration to maintain accuracy. The increasing reliance on AI-assisted diagnostics and complex signal processing algorithms necessitates stringent biometric data validation and automated quality check protocols.

- Ensuring patient data security is a growing concern as more clinical decision support tools become cloud-connected. Furthermore, achieving accurate aqueous depth measurement, central corneal thickness, and vitreous length calculation in all patient types is an ongoing R&D challenge, with IOL constant personalization requiring extensive surgical outcome analysis and robust data sets for optimization.

Exclusive Technavio Analysis on Customer Landscape

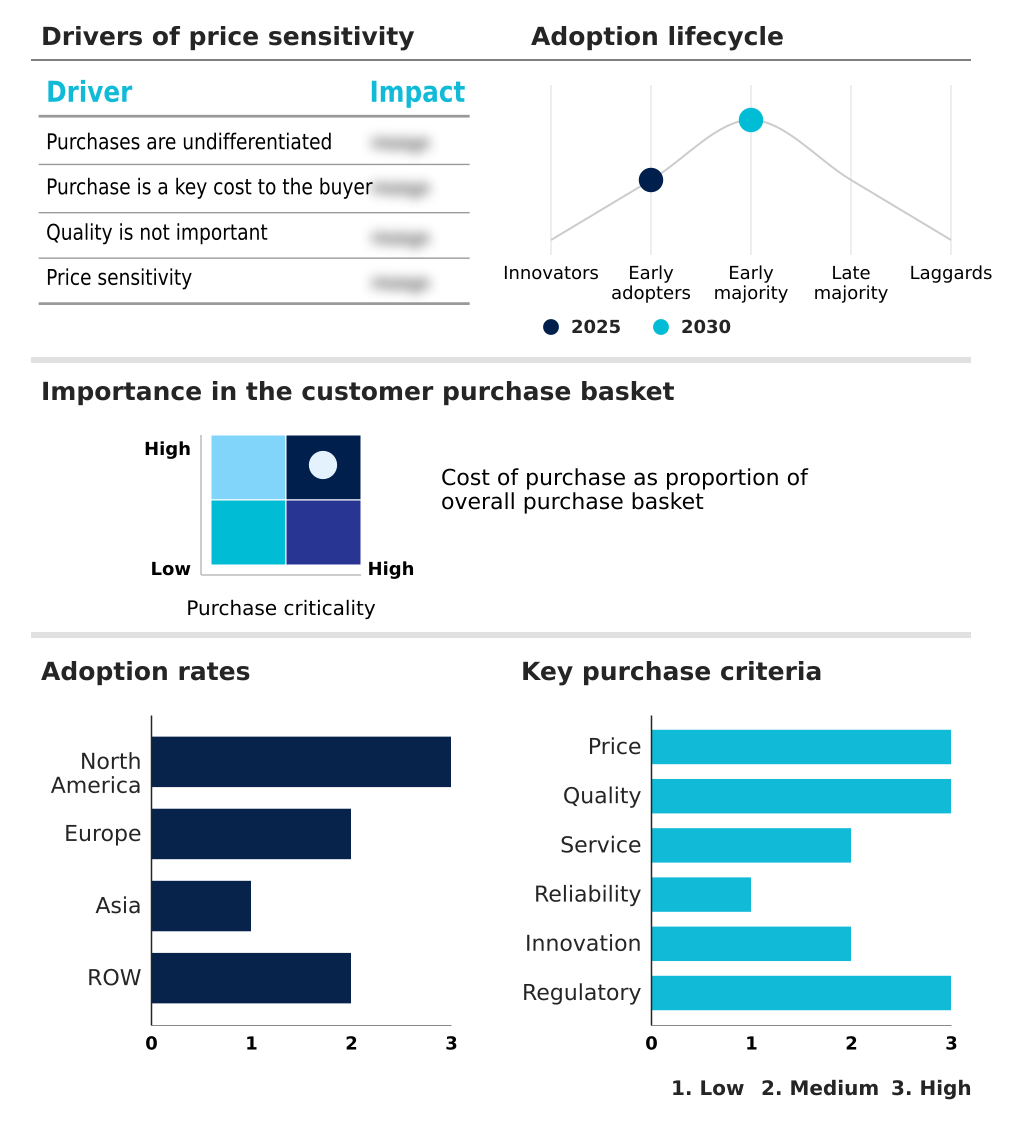

The optical biometry devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the optical biometry devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Optical Biometry Devices Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, optical biometry devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AMETEK Inc. - The vendor landscape features specialized firms and diversified corporations delivering advanced instruments for precise ocular measurements, which enhance surgical planning and improve clinical outcomes in ophthalmology.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AMETEK Inc.

- Bausch Lomb Corp.

- Baxter International Inc.

- Canon Inc.

- Carl Zeiss AG

- Haag Streit AG

- HEINE Optotechnik GmbH

- HOYA CORP.

- Metall Zug AG

- Nidek Co. Ltd.

- OCULUS Optikgerate GmbH

- Optovue Inc.

- Revenio Group Oyj

- Santec Corp.

- Tomey Corp.

- Topcon Corp.

- US Ophthalmic LLC

- VISIONIX USA INC.

- Ziemer Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Optical biometry devices market

- In January 2025, Heidelberg Engineering introduced an upgraded biometry platform that incorporates faster optical coherence scanning, an improved keratometry module, and advanced AI-based refractive calculations designed to support modern cataract surgery planning.

- In March 2025, Nidek expanded its ophthalmic portfolio by introducing a compact biometry system optimized for ASC environments, delivering faster measurement cycles and intuitive touch screen interfaces that support high patient turnover.

- In March 2025, Haag Streit reported increased installations of its optical biometry systems across European surgical centers, citing strong demand for improved efficiency over conventional ultrasound-based diagnostics.

- In April 2025, Topcon Healthcare noted an increase in demand for its devices in regions where updated reimbursement schedules for cataract diagnostics were implemented, demonstrating how financial policy changes support adoption trends.

- In May 2025, Ziemer Group encountered increased competitive pressure in key Asian markets from newly introduced biometry systems offered at lower price points, prompting the company to expand distributor partnerships.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Optical Biometry Devices Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 291 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.4% |

| Market growth 2026-2030 | USD 106.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, India, Japan, South Korea, Thailand, Indonesia, Brazil, Saudi Arabia, Argentina, UAE, Colombia, Turkey, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The core of the optical biometry devices market is the shift toward high-precision diagnostics. Boardroom decisions on capital expenditure now center on acquiring platforms featuring swept-source optical coherence tomography and interferometry-based systems for superior anterior segment tomography. These devices enable not just basic biometry but also retinal thickness analysis, pachymetry mapping, and ocular surface analysis using high-resolution cross-sectional imaging.

- The integration of corneal topography integration and wavefront aberrometry is critical for phacoemulsification planning and accurate toric IOL alignment, addressing posterior corneal astigmatism and dynamic cyclotorsion compensation. Advanced software leverages ray tracing technology, point spread function analysis, and modern gaussian optics formulas like the barrett universal ii formula and olsen formula, departing from older haigis and srk/t formulas.

- AI-assisted diagnostics and machine learning algorithms drive biometric data validation and improve refractive error analysis. These platforms have demonstrated a reduction in prediction error by over 20% in challenging cases.

- Functionalities extend to non-contact tonometry, pupil diameter measurement, central corneal thickness assessment, aqueous depth measurement, and vitreous length calculation, all managed via sophisticated biometric data management systems with automated quality check and advanced signal processing algorithms to measure lens tilt and decentration.

What are the Key Data Covered in this Optical Biometry Devices Market Research and Growth Report?

-

What is the expected growth of the Optical Biometry Devices Market between 2026 and 2030?

-

USD 106.1 million, at a CAGR of 5.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals, ASCs, and Others), Product (SS-OCT-based optical biometers, OLCR-based optical biometers, and PCI-based optical biometers), Product Type (Non-contact type, and Contact type) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rise in prevalence of cataract among geriatric population, Supply chain and quality control issues

-

-

Who are the major players in the Optical Biometry Devices Market?

-

AMETEK Inc., Bausch Lomb Corp., Baxter International Inc., Canon Inc., Carl Zeiss AG, Haag Streit AG, HEINE Optotechnik GmbH, HOYA CORP., Metall Zug AG, Nidek Co. Ltd., OCULUS Optikgerate GmbH, Optovue Inc., Revenio Group Oyj, Santec Corp., Tomey Corp., Topcon Corp., US Ophthalmic LLC, VISIONIX USA INC. and Ziemer Group

-

Market Research Insights

- Market dynamics are shaped by the need for enhanced diagnostic precision and operational efficiency. The integration of advanced surgical planning software improves biometric measurement accuracy, which is critical for emmetropia targeting and successful post-refractive surgery calculation. Non-contact systems with reliable patient fixation monitoring are gaining favor, as they can achieve dense cataract penetration more effectively than older technologies.

- This focus on advanced technology is delivering tangible results, with some facilities reporting a 25% reduction in postoperative refractive surprises. Furthermore, the ability to streamline preoperative assessments contributes to an improvement in clinical throughput by up to 40%, optimizing resource allocation in high-volume surgical centers.

We can help! Our analysts can customize this optical biometry devices market research report to meet your requirements.

RIA -

RIA -