Ortho Pediatric Devices Market Size 2025-2029

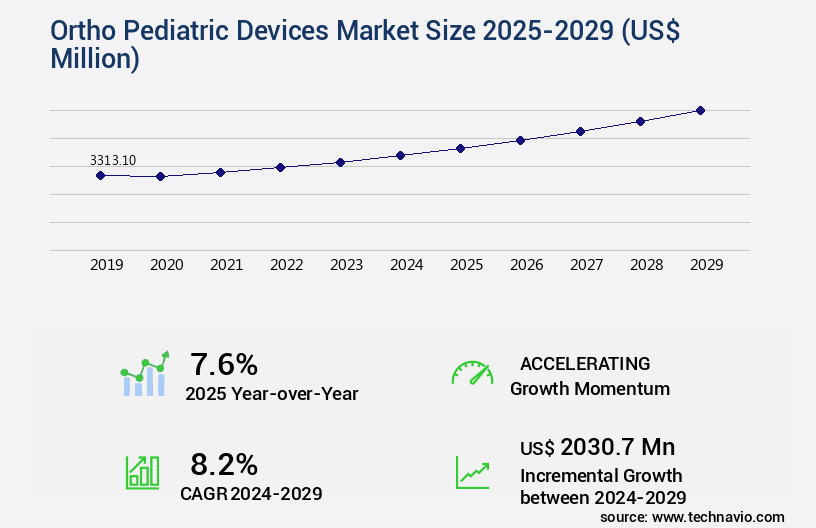

The ortho pediatric devices market size is valued to increase USD 2.03 billion, at a CAGR of 8.2% from 2024 to 2029. Increasing incidence of pediatric orthopedic injuries will drive the ortho pediatric devices market.

Major Market Trends & Insights

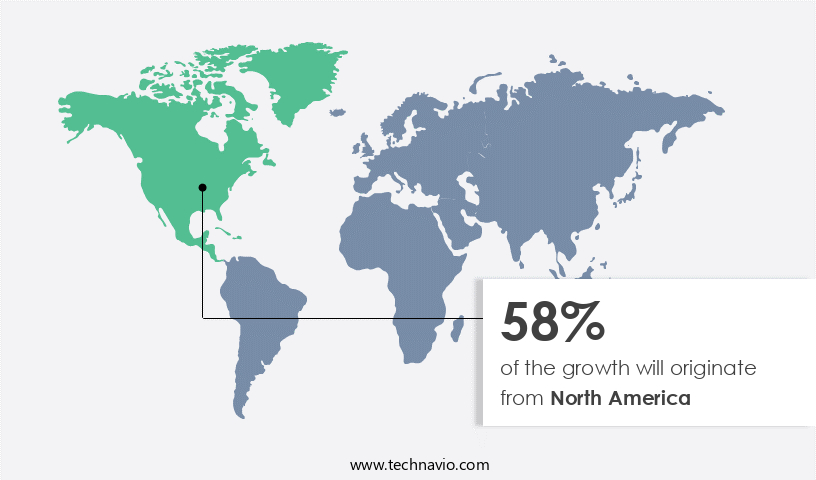

- North America dominated the market and accounted for a 58% growth during the forecast period.

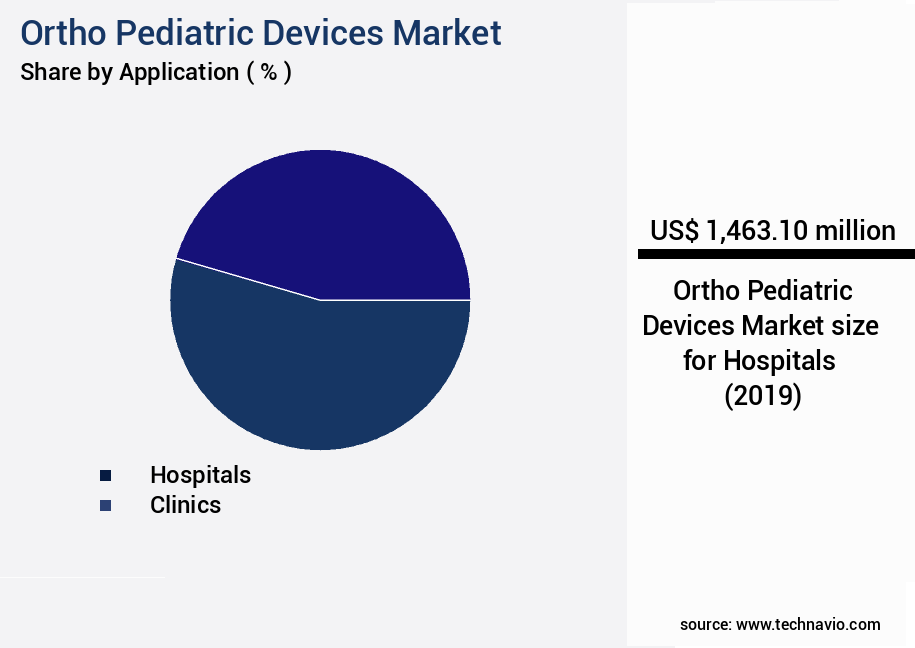

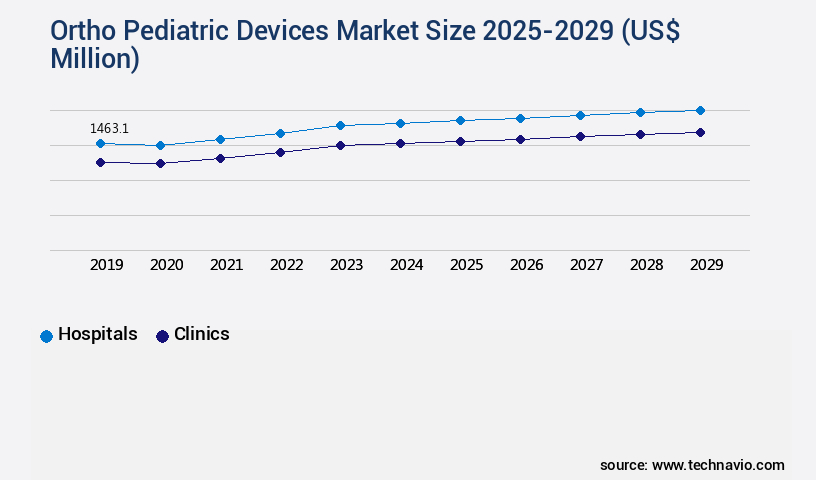

- By Application - Hospitals segment was valued at USD 1.46 billion in 2023

- By Product - Trauma and deformities segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 88.06 million

- Market Future Opportunities: USD 2030.70 million

- CAGR from 2024 to 2029 : 8.2%

Market Summary

- The market is experiencing significant growth due to the increasing incidence of pediatric orthopedic injuries. The global market for orthopedic devices is projected to reach a value of USD 62.3 billion by 2027. This expansion is driven by the global adoption of advanced treatment solutions, which offer improved patient outcomes and faster recovery times. However, the high costs associated with these devices and surgeries remain a challenge for many families and healthcare systems. Orthopedic devices for pediatric use include braces, orthoses, implants, and prosthetics. These devices cater to various conditions such as scoliosis, clubfoot, and cerebral palsy.

- The development of minimally invasive surgical techniques and the integration of robotics and 3D printing technologies are expected to further drive market growth. Additionally, the increasing awareness of early intervention and the availability of insurance coverage for pediatric orthopedic treatments are also contributing factors. Despite these opportunities, the market faces challenges such as regulatory approvals, reimbursement policies, and the need for customized solutions for individual patients. In conclusion, the market is poised for continued growth due to the increasing incidence of pediatric orthopedic injuries and the adoption of advanced treatment solutions. While the market presents opportunities for innovation and growth, it also faces challenges related to costs, regulatory approvals, and customization.

- The integration of emerging technologies and the focus on early intervention are expected to shape the future direction of the market.

What will be the Size of the Ortho Pediatric Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Ortho Pediatric Devices Market Segmented?

The ortho pediatric devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Hospitals

- Clinics

- Others

- Product

- Trauma and deformities

- Smart implants

- Spine

- Sports medicine

- Technology

- 3D-printed orthopedic devices

- Smart wearable orthopedic devices

- Robot-assisted surgical devices

- Biodegradable implants

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By Application Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant growth due to the increasing prevalence of orthopedic disorders and associated risk factors in children. With a focus on post-surgical rehabilitation and regulatory compliance, the market is witnessing continuous advancements in fracture fixation devices, bone grafting materials, patient-specific implants, and 3D-printed implants. Technological innovations like minimally invasive surgery, physical therapy modalities, and surgical navigation systems are gaining popularity, leading to improved functional outcome measures. The market is also witnessing a surge in the adoption of motion capture technology, bone growth stimulators, and surgical implants for various orthopedic procedures, including arthroscopy, spinal instrumentation, and joint replacement surgery.

The Hospitals segment was valued at USD 1.46 billion in 2019 and showed a gradual increase during the forecast period.

According to a study, the pediatric orthopedics market is projected to grow at a CAGR of 5.5% during the forecast period. This growth can be attributed to the increasing demand for orthopedic biomaterials, growth plate injuries, scoliosis correction, and limb lengthening surgery. Additionally, the adoption of image-guided surgery, device sterilization methods, and surgical complications management is driving market growth. Despite these advancements, patient satisfaction metrics remain a critical factor in market success. Innovations in infection control protocols, osteotomy techniques, biomechanical testing, and gait analysis are essential to maintaining patient safety and improving overall patient outcomes.

Regional Analysis

North America is estimated to contribute 58% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Ortho Pediatric Devices Market Demand is Rising in North America Request Free Sample

The market in North America is experiencing steady expansion due to several driving factors. The increasing prevalence of injuries in children, coupled with product launches and initiatives by organizations, fuels market growth. These efforts aim to ensure effective treatment and insurance coverage for pediatric patients. Additionally, the growing number of offerings from key industry players is expected to further propel market expansion during the forecast period.

The market in North America is poised for significant progress, driven by these influential factors.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is witnessing significant growth due to the increasing prevalence of pediatric orthopedic conditions and advancements in technology. Pediatric orthopedic implant design considerations are crucial in catering to the unique biomechanical properties of pediatric bone. These considerations include growth plate preservation techniques and the development of new materials with optimal biocompatibility for interacting with growing tissues. Minimally invasive techniques in pediatric orthopedics, such as surgical navigation systems for pediatric spine surgery, are gaining popularity due to their potential to reduce complications and improve functional outcomes following corrective surgery. Advanced imaging techniques, including 3D printing applications in pediatric orthopaedic devices, are revolutionizing diagnosis and treatment planning, enabling more precise and personalized care.

Reconstructive surgery techniques for pediatric fractures and management strategies for pediatric scoliosis are also driving market expansion. Infection prevention strategies and risk factors for revision surgery in pediatric orthopedics are critical areas of focus, with the need for continuous innovation to minimize complications and improve patient outcomes. Telehealth applications for post-operative pediatric care are increasingly being adopted to enhance patient engagement and facilitate remote monitoring, contributing to the market's growth. Performance evaluation of pediatric implants and patient reported outcome measures are essential for assessing the effectiveness of orthopedic devices and guiding future product development. Compared to traditional methods, the adoption of advanced technologies in pediatric orthopedics is seeing rapid growth.

For instance, more than 80% of new product developments in the field are focusing on incorporating these technologies to improve patient care and outcomes. This trend is expected to continue, further fueling the expansion of the market.

What are the key market drivers leading to the rise in the adoption of Ortho Pediatric Devices Industry?

- The rising prevalence of pediatric orthopedic injuries serves as the primary market driver.

- The escalating prevalence of orthopedic conditions among children, including sports-related injuries, spinal deformities, tendon injuries, and hip, shoulder, and spine fractures, is fueling the demand for orthopedic pediatric devices. According to the Centers for Disease Control and Prevention (CDC), unintentional injuries are a leading cause of emergency department (ED) visits among American children. Data from the CDC's Web-based Injury Statistics Query and Reporting System (WISQARS) reveals that males aged 1-19 years consistently exhibit higher nonfatal injury rates compared to their female counterparts in the same age group.

- This underscores the importance of advanced orthopedic solutions tailored to pediatric populations. The orthopedic devices market encompasses a wide range of products, including braces, prosthetics, implants, and orthoses, catering to the diverse needs of children with orthopedic conditions. This market is characterized by continuous innovation and growth, driven by technological advancements, increasing awareness, and the rising burden of orthopedic conditions among children.

What are the market trends shaping the Ortho Pediatric Devices Industry?

- Advanced treatment solutions are increasingly being adopted on a global scale. This market trend reflects the growing demand for innovative healthcare technologies.

- In the realm of healthcare diagnostics, the adoption of in-vitro diagnostic tools for managing and testing cancer, cardiovascular diseases (CVD), and infectious kidney diseases through immunoassay and molecular diagnostic devices is experiencing a significant surge. This trend is driven by the availability of advanced treatment care, leading to increased acceptance among healthcare providers. For example, Siemens' Xprecia Stride Coagulation Analyzer is a handheld device that delivers high accuracy in ProTime INR (PT/INR) tests. Despite the high volume of routine diagnostic testing, the growth of specialty testing in esoteric, pathology, and genetic testing areas is predicted to outpace the overall market.

- As a result, laboratories are increasingly opting for bulk purchases from a single trusted partner to procure individual analyzers. This shift towards specialty testing underscores the evolving nature of the diagnostics market and its applications across various sectors.

What challenges does the Ortho Pediatric Devices Industry face during its growth?

- The escalating costs linked to orthopedic devices and surgeries represent a significant challenge to the industry's growth trajectory.

- Ortho pediatric devices, essential for diagnosing and treating various orthopedic conditions in pediatric patients, come with significant costs that hinder market expansion. The expenses related to these devices can increase the financial burden on both end-users and patients. The cost of orthopedic equipment varies based on its applications and features. For example, in 2024, the average cost for a pedicle screw implant in the United States was approximately 923 units' worth. The overall cost of an orthopedic procedure includes the expenses for the devices, procedure charges, consultation fees, medications, and consumables.

- This financial burden can deter potential customers from seeking necessary treatments. Despite these challenges, the market for ortho pediatric devices continues to evolve, with advancements in technology leading to more cost-effective and efficient solutions.

Exclusive Technavio Analysis on Customer Landscape

The ortho pediatric devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ortho pediatric devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Ortho Pediatric Devices Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ortho pediatric devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Apex Ortho and Surgical - The TightRope implant is a notable orthopedic device the company provides, catering to pediatric patients.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Apex Ortho and Surgical

- Arthrex Inc.

- Auxein Medical Inc.

- Johnson and Johnson Services Inc

- Madison Ortho

- Medtronic Plc

- Merete GmbH

- Mighty Oak Medical

- Narang Medical Ltd.

- NuVasive Inc.

- Orthofix Medical Inc.

- OrthoPediatrics Corp.

- Smith and Nephew plc

- Stryker Corp.

- Total Joint Orthopedics Inc.

- TREACE MEDICAL CONCEPTS INC.

- Trendlines Group Ltd.

- TST Tibbi Aletler

- WishBone Medical Inc.

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ortho Pediatric Devices Market

- In January 2024, Stryker Corporation, a leading medical technology company, announced the launch of their new pediatric orthopedic device, the Reef Pediatric Hip System. This system is designed to address the unique needs of growing children and aims to improve their quality of life (Stryker Corporation Press Release, 2024).

- In March 2024, Medtronic plc and Boston Children's Hospital entered into a strategic collaboration to develop pediatric orthopedic devices using 3D printing technology. This partnership is expected to result in innovative solutions tailored to individual children's needs (Medtronic Press Release, 2024).

- In May 2024, Smith & Nephew plc completed the acquisition of Osiris Therapeutics, a regenerative medicine company. This acquisition expanded Smith & Nephew's portfolio to include orthopedic devices for pediatric applications using cellular therapy (Smith & Nephew Press Release, 2024).

- In April 2025, the US Food and Drug Administration (FDA) granted 510(k) clearance to Zimmer Biomet Holdings for its new pediatric orthopedic device, the Dynasys Pediatric Nail System. This system offers improved implant fixation and flexibility for children with complex fractures (Zimmer Biomet Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ortho Pediatric Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

229 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.2% |

|

Market growth 2025-2029 |

USD 2030.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.6 |

|

Key countries |

US, Canada, Germany, China, UK, Mexico, France, Italy, Japan, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the realm of pediatric healthcare, the market continues to evolve, driven by advancements in technology and a growing demand for innovative solutions. This sector encompasses a diverse range of products, from fracture fixation devices and bone grafting materials to patient-specific implants and 3D-printed orthotics. Post-surgical rehabilitation is a critical aspect of the market, with a focus on regulatory compliance and infection control protocols ensuring the highest standards of patient care. Fracture fixation devices, such as surgical implants and plate systems, play a pivotal role in the healing process. Meanwhile, bone grafting materials facilitate the regeneration of bone tissue, contributing to improved functional outcome measures.

- The integration of minimally invasive surgery and physical therapy modalities, like gait analysis and motion capture technology, has revolutionized orthopedic procedures. Additionally, advancements in medical device certifications, such as image-guided surgery and surgical navigation systems, enable more precise interventions. One notable trend is the increasing adoption of patient-specific implants and tissue engineering scaffolds, which offer personalized solutions for children with unique orthopedic needs. These innovations, coupled with the development of biomechanical testing and spinal instrumentation, are transforming the landscape of pediatric orthopedics. Despite these advancements, challenges persist, including the high revision surgery rates associated with certain orthopedic procedures and the need for effective device sterilization methods to minimize surgical complications.

- As the market continues to evolve, the focus remains on delivering solutions that prioritize patient satisfaction, safety, and optimal functional outcomes. Among the various orthopedic devices, fracture fixation devices accounted for approximately 40% of the total market value in 2020. This segment's dominance can be attributed to its wide application in addressing various orthopedic conditions, ensuring a robust demand for these devices in the pediatric population.

What are the Key Data Covered in this Ortho Pediatric Devices Market Research and Growth Report?

-

What is the expected growth of the Ortho Pediatric Devices Market between 2025 and 2029?

-

USD 2.03 billion, at a CAGR of 8.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Hospitals, Clinics, and Others), Product (Trauma and deformities, Smart implants, Spine, and Sports medicine), Technology (3D-printed orthopedic devices, Smart wearable orthopedic devices, Robot-assisted surgical devices, and Biodegradable implants), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing incidence of pediatric orthopedic injuries, High costs associated with orthopedic devices and surgeries

-

-

Who are the major players in the Ortho Pediatric Devices Market?

-

Apex Ortho and Surgical, Arthrex Inc., Auxein Medical Inc., Johnson and Johnson Services Inc, Madison Ortho, Medtronic Plc, Merete GmbH, Mighty Oak Medical, Narang Medical Ltd., NuVasive Inc., Orthofix Medical Inc., OrthoPediatrics Corp., Smith and Nephew plc, Stryker Corp., Total Joint Orthopedics Inc., TREACE MEDICAL CONCEPTS INC., Trendlines Group Ltd., TST Tibbi Aletler, WishBone Medical Inc., and Zimmer Biomet Holdings Inc.

-

Market Research Insights

- The market encompasses a diverse range of medical technologies designed to address the unique needs of pediatric patients with conditions such as congenital anomalies and spinal deformities. Two key drivers fueling this expansion are the increasing prevalence of surgical techniques for correcting pediatric deformities and the growing adoption of advanced materials like titanium alloys and hydroxyapatite coatings. For instance, the use of risk assessment tools and surgical training simulators has streamlined surgical procedures, leading to improved implant stability and bone remodeling.

- Furthermore, telehealth applications, patient registry data, and remote patient monitoring have facilitated better pediatric trauma care and post-operative pain management. Despite these advancements, challenges persist, including adverse event reporting, fatigue testing, and device failure analysis. To mitigate these risks, manufacturers are investing in quality assurance measures, biocompatibility standards, and clinical trial data to ensure the safety and efficacy of their products. Longitudinal studies and evidence-based medicine are also playing a crucial role in understanding the long-term effects of ortho pediatric devices, particularly in managing conditions like cerebral palsy and growth disorders.

We can help! Our analysts can customize this ortho pediatric devices market research report to meet your requirements.

RIA -

RIA -