US Packaged Food Market Size 2025-2029

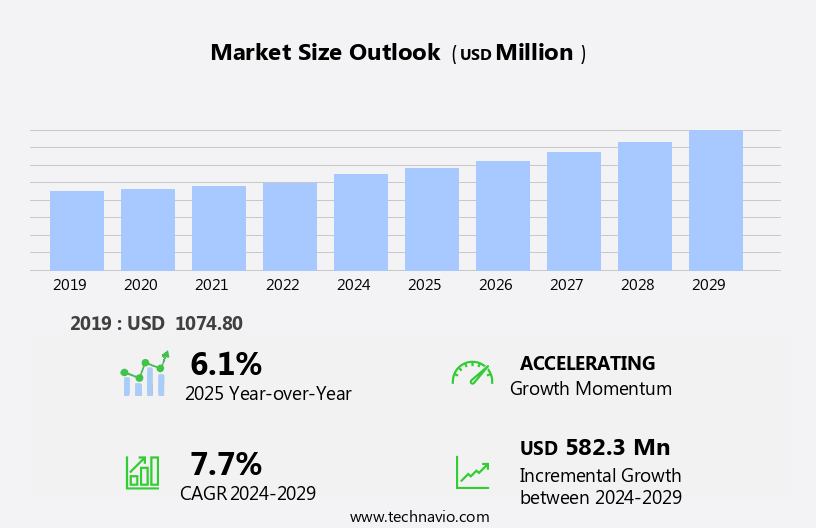

The US packaged food market size is forecast to increase by USD 582.3 million at a CAGR of 7.7% between 2024 and 2029.

- The Packaged Food Market is experiencing significant growth, driven by the increasing demand for food products with longer shelf lives and the rising consumer awareness towards clean-label products. This trend is particularly prominent in the US market, where strict food regulations ensure a high level of consumer safety and trust. However, companies operating in this market face challenges such as increasing competition and the need to comply with evolving regulatory requirements. To capitalize on these opportunities, companies must focus on innovation and product differentiation, leveraging clean labeling and extended shelf life technologies. This trend is particularly evident in the demand for functional foods, which offer health benefits beyond basic nutrition.

- Strategic partnerships and collaborations can also help companies navigate the complex regulatory landscape and expand their reach in the market. Overall, the Packaged Food Market presents a compelling opportunity for companies seeking to meet evolving consumer preferences and regulatory requirements while navigating a competitive landscape.

What will be the size of the US Packaged Food Market during the forecast period?

- The packaged food market encompasses a wide range of products, including convenience foods, organic offerings, ready-to-eat meals, frozen foods, snack items, dairy products, meat alternatives, plant-based options, gluten-free items, and various specialty and ethnic foods. This market continues to evolve, driven by consumer preferences for healthier, more convenient, and more diverse food choices. Key trends include a growing focus on food labeling and nutritional information, as well as the rise of functional foods catering to specific health needs. Food allergies and dietary restrictions have also fueled demand for gluten-free and other specialty products. These include fortified dairy products, meat alternatives, and plant-based offerings.

- The packaged food industry's size is substantial, with continued growth driven by the convenience and versatility these products offer. As consumers prioritize health and wellness, there is a growing emphasis on food quality and brand loyalty. The supply chain remains critical to ensuring the timely delivery of these products, with logistical challenges and sustainability concerns shaping industry discussions. Overall, the packaged food market is dynamic and diverse, reflecting the evolving needs and preferences of consumers worldwide.

How is this market segmented?

The market report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

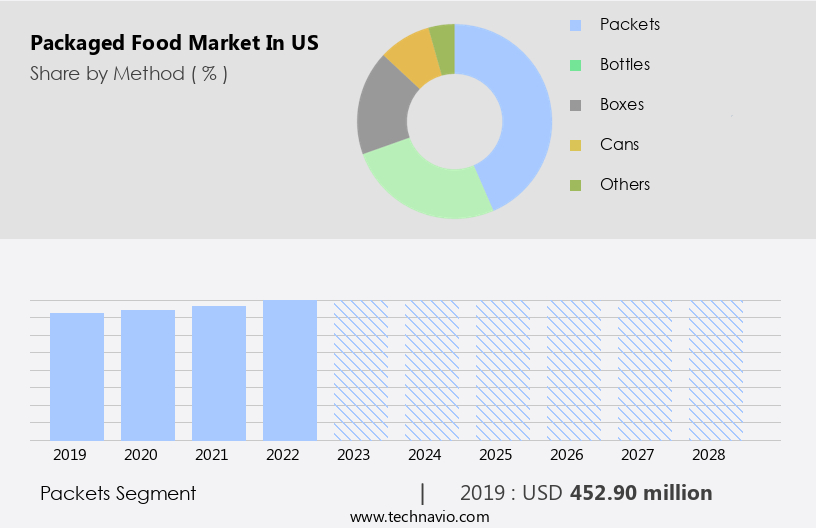

- Method

- Packets

- Bottles

- Boxes

- Cans

- Others

- Distribution Channel

- Offline

- Online

- Type

- Bakery and cereals

- Dairy products

- Snacks and nutritional bars

- Beverages

- Others

- Geography

- US

By Method Insights

The packet segment is estimated to witness significant growth during the forecast period. Packaged food continues to be a significant market, catering to consumers' demand for convenience, portability, and extended shelf life. The trend toward single-serve and individualized packaging has gained momentum, driven by consumers' preference for smaller portions and minimized waste. This is particularly prevalent in categories such as condiments, sauces, and snacks. For instance, single-serve coffee packets from brands like Folgers, a subsidiary of J.M. Smucker, have gained popularity for their quick and convenient brewing. Food safety, sustainability, and health and wellness are key factors influencing the packaged food market. Sustainable packaging solutions, such as eco-friendly materials, are increasingly being adopted to reduce waste and promote environmental responsibility. This trend has also led to the growth of private labels, as retailers seek to differentiate themselves and offer unique, high-quality options. The packaged food market encompasses various categories, including convenience foods, ready-to-eat meals, frozen foods, snack foods, dairy products, meat products, plant-based foods, and specialty foods. Efficient and effective logistics are essential for ensuring freshness and minimizing waste.

Functional foods, organic options, and dietary needs catering to various health concerns are also driving market growth. Consumers seek transparency in food labeling and nutritional information, which has led to an increased focus on clean labeling and natural flavors. The packaged food market encompasses various categories, including convenience foods, ready-to-eat meals, frozen foods, snack foods, dairy products, meat products, plant-based foods, and specialty foods. Food preservation techniques and shelf life extension methods are essential to maintaining product freshness and quality. Packaging materials play a crucial role in ensuring food safety and extending shelf life. Brand loyalty and consumer choice are essential factors in the competitive landscape, with food manufacturers and private labels vying for market share through innovation, quality, and consumer appeal.

Food additives and flavor enhancements are used to improve product taste and shelf life, while waste reduction and changing lifestyles continue to shape market trends. Food security and digital marketing are also key considerations in the packaged food industry.

Get a glance at the market share of various segments Request Free Sample

The Packets segment was valued at USD 452.90 million in 2019 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of US Packaged Food Market?

- Increasing demand for food products with longer shelf lives is the key driver of the market. Packaged foods cater to the demands of modern consumers, offering convenience, longer shelf life, and sustainability. With increasing numbers of dual-income households and hectic lifestyles, ready-to-eat meals and snacks have become essential. Food safety is a priority, and packaged foods ensure freshness through advanced preservation techniques and innovative packaging materials. Sustainability is a significant concern, leading to the growth of sustainable packaging solutions. Consumers prefer organic foods, plant-based options, and functional foods, which are often available in packaged formats. Nutritional information and food labeling are crucial for health-conscious consumers, and packaged foods provide clear and concise labeling. Food manufacturers and private labels offer a wide range of products, including convenience meals, single-serve packs, health snacks, nutritional bars, meal kits, and portioned meals. Organic foods, health and wellness, convenience, and specialty offerings are key areas of growth. Transparency, food quality, and brand loyalty are essential for success in this competitive industry.

-

These products cater to various dietary needs, such as gluten-free, vegan, and low-calorie options. Food innovation continues to drive the market, with new product launches in areas like clean label, natural flavors, fortified foods, and eco-packaging. Food allergies and specialty foods are also gaining popularity, requiring manufacturers to provide clear labeling and cater to specific dietary requirements. The supply chain is a critical aspect of the packaged food market, ensuring food quality, freshness, and timely delivery. The growth of the packets segment can be attributed to the increasing popularity of single-serve or individualized packaging. Food preservation techniques, such as freeze-drying and vacuum packing, help maintain food quality and extend shelf life. Digital marketing and health regulations play a significant role in consumer choice, with companies investing in innovative marketing strategies and adhering to stringent food safety regulations. The packaged food market is dynamic and evolving, driven by consumer preferences, sustainability, and convenience. Packaged foods offer a solution to the demands of modern consumers, providing a wide range of options that cater to various dietary needs, lifestyle choices, and sustainability concerns.

What are the market trends shaping the US Packaged Food Market?

- Increasing consumer awareness about clean-label products is the upcoming trend in the market. In the US market, there is a growing demand for packaged foods that prioritize food safety, sustainability, and health. Consumers are increasingly concerned about the transparency of food labels, seeking out organic options, functional foods, and cleaner ingredients. This trend is driving innovation in the industry, with companies introducing ready-to-eat meals, frozen foods, snack foods, dairy products, and meat alternatives that cater to these preferences. Food safety and preservation are key considerations, with many companies focusing on longer shelf life and freshness seals to maintain product quality. Consumers prefer smaller portions to minimize waste and have better control over their food intake, particularly in categories such as condiments, sauces, and snacks. Sustainable packaging is also a priority, with eco-friendly materials and waste reduction strategies gaining popularity.

-

Specialty foods, including ethnic and dietary options, are in high demand, as are meal kits, meal solutions, and portion-controlled snacks. Functional foods, such as nutritional bars and hydration drinks, are popular choices for health-conscious consumers. Natural flavor enhancements and fortified foods are also gaining traction, as are vegan and dairy-free alternatives. Food manufacturers and private labels are responding to these trends by offering a wide range of options to meet consumer preferences and dietary needs. The food industry is also adapting to changing lifestyles and food security concerns, with digital marketing and health regulations playing a role in shaping consumer choices. Consumers value convenience and portability, with single-serve packs and meal solutions in high demand. The market for packaged foods is expected to continue growing, as consumers seek out products that align with their health and wellness goals.

What challenges does the US Packaged Food Market face during its growth?

- Strict food regulations in US is a key challenge affecting the market growth. The US packaged food market faces regulatory challenges due to stringent food safety regulations. The Food and Drug Administration (FDA) enforces nutrition labeling and health claims, requiring accurate and transparent information on serving sizes, calories, and nutrient content. In 2024, the FDA continued to enforce these requirements, impacting product formulations and potentially hindering new product introductions. Other regulatory factors include food safety, sustainable packaging, and food allergies. Food manufacturers must comply with these regulations to maintain brand loyalty and ensure food quality, preservation, and shelf life.

-

Consumer preferences for organic foods, health and wellness, ready-to-eat meals, frozen foods, snack foods, dairy products, meat products, plant-based foods, and functional foods drive market innovation. Key packaging trends include food labeling, nutritional information, eco-friendly packaging, and portion control. Meeting these regulations while catering to changing lifestyles, dietary needs, and consumer choice remains a priority for the packaged food industry.

How can Technavio assist you in making critical decisions?

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- B and G Foods Inc.

- Campbell Soup Co.

- Cargill Inc.

- Conagra Brands Inc.

- General Mills Inc.

- Hormel Foods Corp.

- JBS SA

- Kellogg Co.

- Mars Inc.

- McCormick and Co. Inc.

- Mondelez International Inc.

- Nestle SA

- PepsiCo Inc.

- The Coca Cola Co.

- The Hershey Co.

- The J.M. Smucker Co.

- The Kraft Heinz Co.

- Tyson Foods Inc.

- Unilever PLC

- WH Group Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The packaged food market encompasses a wide array of products designed to cater to consumers' evolving needs and preferences. This sector continues to experience significant growth, driven by various market dynamics. Food safety remains a top priority for consumers, leading to increased demand for transparent labeling and clear nutritional information. Sustainable packaging is another key trend, as consumers express growing concerns about the environmental impact of food production and waste. Convenience continues to be a significant factor in the packaged food market, with consumers seeking ready-to-eat meals, snack packs, and meal kits that cater to their busy lifestyles.

Health and wellness trends have also influenced the market, with an emphasis on organic foods, functional foods, and plant-based options. Dairy products and meat alternatives have gained popularity due to dietary needs and ethical considerations. Food manufacturers have responded by introducing fortified foods, vegan options, and dairy alternatives to meet this demand. Food labeling and nutritional information are crucial for consumers, who want to make informed choices about their diet. Clean label and natural flavor trends have emerged, as consumers seek to avoid artificial additives and preservatives. The supply chain plays a critical role in the packaged food market, with food manufacturers and private labels working to ensure food quality, freshness, and shelf life.

Food preservation techniques and innovative packaging materials have been instrumental in extending the shelf life of perishable items. Brand loyalty is a significant factor in the packaged food market, with consumers developing strong preferences for certain brands and product lines. Digital marketing and health regulations have become essential tools for food manufacturers to reach consumers and maintain regulatory compliance. Food innovation continues to be a driving force in the packaged food market, with companies introducing new products and flavors to cater to changing consumer preferences. Waste reduction and eco-friendly packaging are also becoming essential considerations for food manufacturers, as consumers demand more sustainable solutions.

The packaged food market is diverse and dynamic, with various trends and factors shaping its growth. From health and wellness to convenience and sustainability, food manufacturers must stay attuned to consumer needs and preferences to remain competitive.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

185 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.7% |

|

Market growth 2025-2029 |

USD 582.3 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.1 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth analysis and market forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge of market growth and forecasting

We can help! Our analysts can customize this market report to meet your requirements Get in touch

RIA -

RIA -