Packaging Materials Market Size 2026-2030

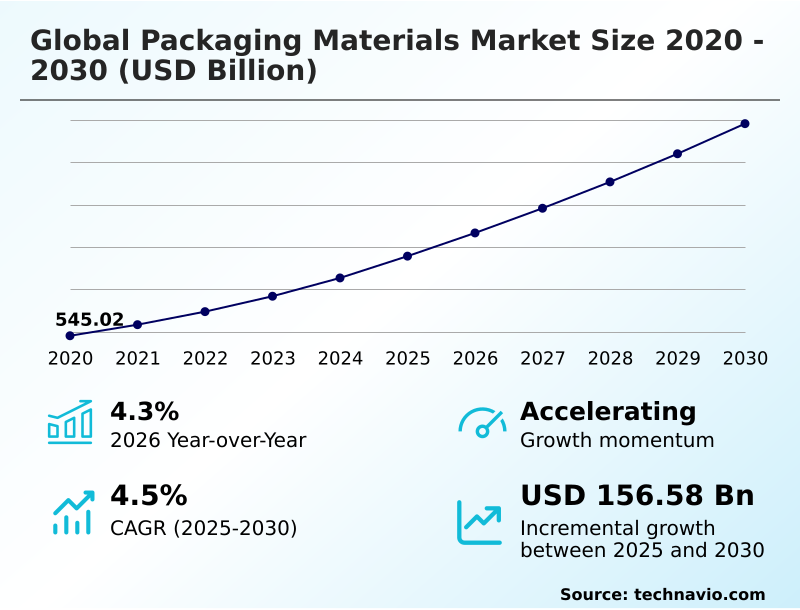

The packaging materials market size is valued to increase by USD 156.58 billion, at a CAGR of 4.5% from 2025 to 2030. Expansion of electronic commerce and direct retail channels will drive the packaging materials market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 45.2% growth during the forecast period.

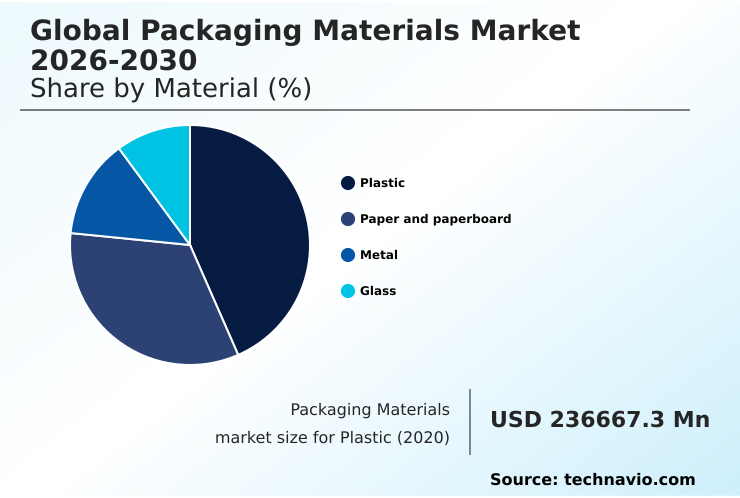

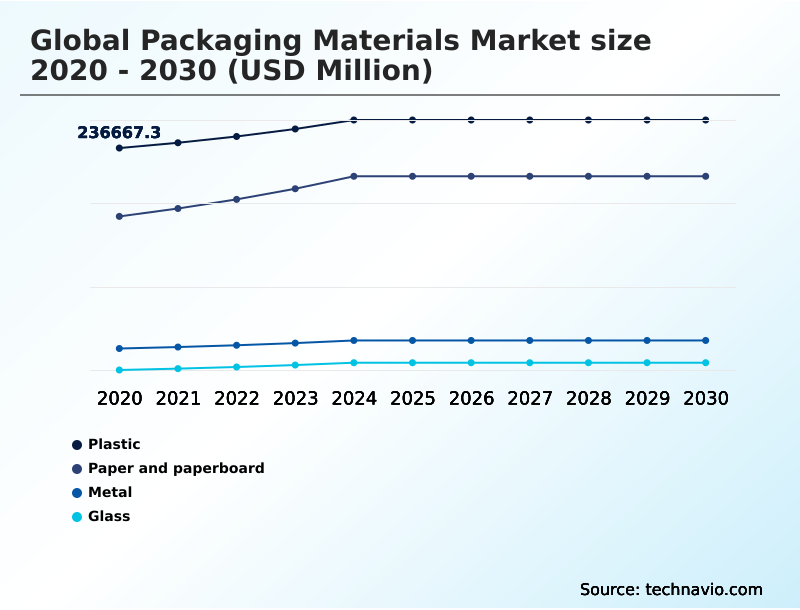

- By Material - Plastic segment was valued at USD 259.62 billion in 2024

- By End-user - Rigid packaging segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 250.67 billion

- Market Future Opportunities: USD 156.58 billion

- CAGR from 2025 to 2030 : 4.5%

Market Summary

- The packaging materials market is foundational to global commerce, defined by a continuous drive for innovation in product protection, sustainability, and logistical efficiency. Demand is shaped by the growth of e-commerce, which requires robust corrugated board and protective interior coatings to withstand complex transit routes.

- Concurrently, a profound shift toward environmental responsibility is accelerating the adoption of renewable fiber-based materials and advanced bio-based polymers. In a typical business scenario, a major consumer goods enterprise re-engineers its supply chain to use lightweight packaging solutions made from high-impact engineered plastics, reducing transportation costs and aligning with corporate sustainability goals.

- This transition involves navigating challenges such as securing a stable supply of post-consumer recycled content and ensuring new mono-material flexible films meet stringent food contact material safety standards. Key materials like aseptic carton packaging for liquids and aluminum beverage containers for drinks continue to evolve, with manufacturers focusing on material science innovation to improve recyclability and reduce environmental footprints.

- The integration of smart packaging technologies further enhances traceability and consumer engagement, making the material itself an interactive part of the product experience.

What will be the Size of the Packaging Materials Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Packaging Materials Market Segmented?

The packaging materials industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Material

- Plastic

- Paper and paperboard

- Metal

- Glass

- End-user

- Rigid packaging

- Flexible packaging

- Application

- Boxes and cartons

- Bottles and jars

- Bags and pouches

- Cans

- Others

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Turkey

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Material Insights

The plastic segment is estimated to witness significant growth during the forecast period.

The market is segmented by material, with plastics playing a pivotal role in consumer goods packaging due to their versatility. Innovations are focused on sustainability, with a significant push toward increasing post-consumer recycled content in both rigid and flexible formats.

Food-grade packaging materials and pharmaceutical grade packaging often require active packaging solutions that incorporate antimicrobial agents to ensure product safety, a feature now found in advanced engineered plastics.

For cold chain packaging solutions, materials like molded fiber and specialized foams are critical. The use of industrial stretch films is essential for pallet stability in logistics.

Meanwhile, categories like aluminum aerosols and products made from specialty extruded film materials serve niche but high-value applications, with some firms seeing a 15% reduction in product spoilage.

The Plastic segment was valued at USD 259.62 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 45.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Packaging Materials Market Demand is Rising in APAC Get Free Sample

The APAC region is the primary growth engine, contributing over 45% of the market's incremental growth, driven by its expansive manufacturing sector requiring advanced industrial packaging solutions.

This has spurred investment in advanced manufacturing technologies for producing containerboard solutions and reinforced corrugated boards at scale.

In North America, where the market is maturing, the focus is on automation; implementing automated packaging systems has improved warehouse throughput by over 20%. European markets prioritize sustainability, widely adopting returnable transit packaging and shelf-ready packaging to meet stringent regulations.

Across regions, the use of digital printing on packaging for pressure-sensitive labels and extruded plastic tubes allows for rapid customization, while high-impact engineered plastics and coated recycled paperboard address needs for both durability and circularity.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Navigating the complexities of the packaging materials market requires a deep understanding of specific use cases and trade-offs. For instance, comparing plastic vs paper packaging sustainability reveals nuanced lifecycle impacts that influence corporate strategy. The benefits of lightweight materials in logistics are clear, directly impacting fuel consumption and shipping costs.

- The role of smart packaging in pharmaceuticals is growing, offering unprecedented traceability and temperature monitoring. A major industry focus is addressing the challenges in recycling multi-layer plastics, which drives research into new polymers and recovery methods. The impact of e-commerce on corrugated box demand has reshaped the paper industry, pushing innovations in strength and design.

- Active packaging technologies for food preservation, such as oxygen scavengers, are becoming standard for extending shelf life. Advancements in biodegradable polymer research promise to reduce plastic pollution, though a cost-benefit analysis of modular packaging shows that reusability can offer more immediate environmental wins. Firms face regulatory hurdles for new packaging materials, slowing market entry.

- The search for sustainable alternatives to single-use plastics is universal, with a focus on implementing circular economy for glass packaging and improving barrier properties of flexible films. Innovations in aluminum can lightweighting continue to reduce material use, while consumer perception of sustainable packaging now directly affects sales, with brands seeing a near 2:1 preference for eco-labeled products.

- Businesses must also manage supply chain risks from raw material volatility. The role of digital printing in packaging customization and the need for optimizing packaging for automated warehouses are key operational trends. Finally, understanding extended producer responsibility scheme effectiveness and the technical requirements for cold chain packaging is crucial for compliance and performance.

- These long-tail considerations define the strategic landscape for all market participants.

What are the key market drivers leading to the rise in the adoption of Packaging Materials Industry?

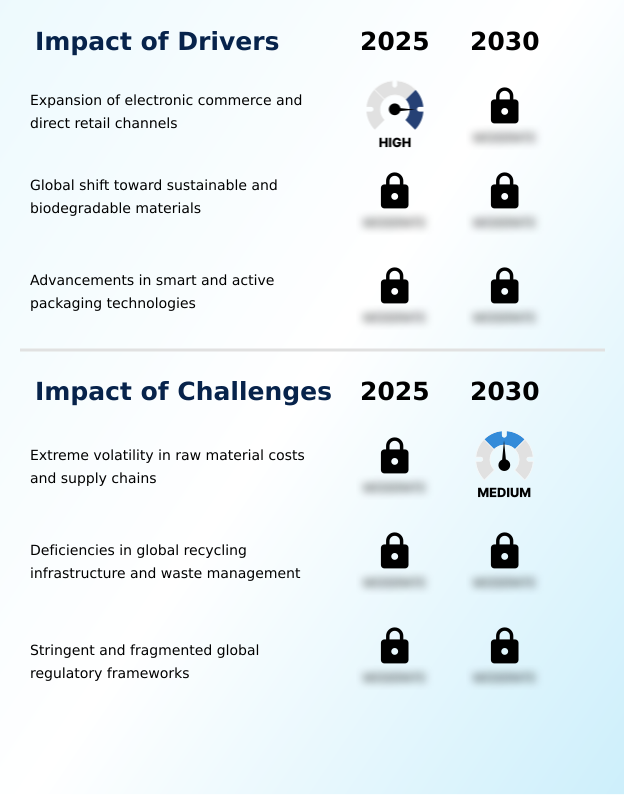

- The expansion of electronic commerce and direct-to-consumer retail channels is a key driver accelerating demand across the market.

- The expansion of e-commerce is a primary driver, accelerating demand for specialized e-commerce packaging solutions that enhance the unboxing experience design.

- This has led to a surge in the use of corrugated board and protective interior coatings, with companies reporting a 25% decrease in transit-related damages.

- The global push for sustainability propels the market for sustainable packaging materials like molded pulp packaging and glass packaging materials.

- Consumers and regulators are demanding biodegradable packaging solutions and the adoption of circular economy models, spurring the development of mono-material flexible films from high density polyethylene.

- Furthermore, the integration of smart packaging technologies offers enhanced product traceability and safety, transforming passive flexible plastic packaging into an interactive brand touchpoint.

What are the market trends shaping the Packaging Materials Industry?

- The increasing adoption of lightweight materials for logistics optimization represents a significant upcoming market trend. This shift is driven by the need to reduce shipping costs and environmental impact.

- Market trends are driven by a focus on logistical efficiency and sustainability. The adoption of lightweight packaging solutions has enabled firms to achieve a 12% reduction in shipping costs. Innovations in material science innovation are leading to advanced high-performance barrier coatings that extend product shelf life, a critical factor for both paperboard cartons and rigid plastic packaging.

- There is a clear shift toward modular packaging designs and multi-purpose packaging designs that improve supply chain optimization and reduce waste. Renewable fiber-based materials and recyclable aluminum beverage containers are gaining traction, supported by extended producer responsibility schemes.

- The use of specialized materials, including specialty nonwoven fabrics and pressure-sensitive labeling materials, also continues to grow, adapting to new product forms and retail demands.

What challenges does the Packaging Materials Industry face during its growth?

- Extreme volatility in the cost and availability of raw materials, coupled with supply chain disruptions, presents a key challenge to industry growth.

- Significant market challenges stem from material complexity and inadequate infrastructure. The raw material sourcing for bio-based polymers and compostable polymers remains volatile, impacting production costs. While materials like aseptic carton packaging offer excellent protection, their multi-layer polymer films, often containing ethylene vinyl alcohol, complicate end-of-life material recovery.

- The industry’s ability to scale is hindered by deficiencies in waste management infrastructure, which is often unequipped to process these advanced materials, leading to less than 40% of such plastics being effectively recycled in some areas.

- Adherence to a fragmented regulatory compliance framework for food contact material safety is another major hurdle, particularly concerning the use of oxygen scavengers and moisture absorbers. These factors collectively create barriers to achieving a fully circular system.

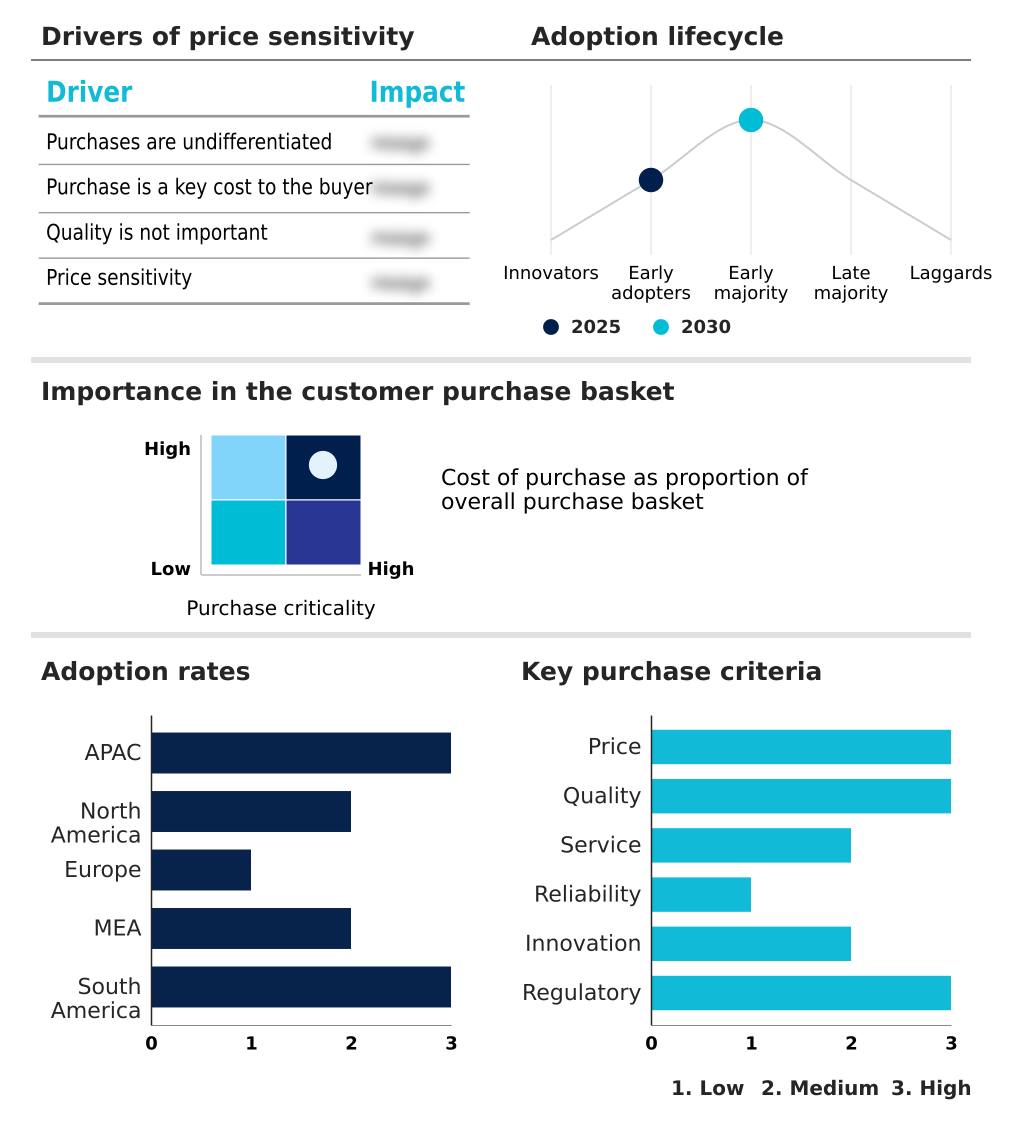

Exclusive Technavio Analysis on Customer Landscape

The packaging materials market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the packaging materials market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Packaging Materials Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, packaging materials market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amcor Plc - Provides a portfolio of flexible and rigid materials, including plastics, foils, and paper-based solutions, engineered for the consumer goods and healthcare sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amcor Plc

- AptarGroup Inc.

- Ardagh Group SA

- Avery Dennison Corp.

- Ball Corp.

- Berry Global Inc.

- CCL Industries Inc.

- Crown Holdings Inc.

- DS Smith Plc

- Graphic Packaging Holding Co.

- Huhtamaki Oyj

- International Paper Co.

- Mondi Plc

- O I Glass Inc.

- Oji Holdings Corp.

- Packaging Corp. of America

- Sealed Air Corp.

- Smurfit Westrock plc

- Sonoco Products Co.

- Tetra Pak International SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Packaging materials market

- In March 2025, LyondellBasell introduced Pro-fax EP649U, a new polypropylene impact copolymer specifically designed to enhance performance in the rigid packaging sector.

- In May 2025, Ball Corporation partnered with Acai Motion to launch a new beverage can certified by the Aluminium Stewardship Initiative, promoting responsible aluminum sourcing.

- In July 2025, WinCup, Inc. announced its acquisition of ConverPack Inc., a move set to expand its manufacturing capabilities in paper-based hot and cold cups.

- In September 2025, Cosmo Plastech showcased its latest innovations in rigid packaging at the World of Ice Cream Expo, highlighting its portfolio of IML films and thermoformed containers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Packaging Materials Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.5% |

| Market growth 2026-2030 | USD 156582.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.3% |

| Key countries | China, India, Japan, South Korea, Indonesia, Australia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Turkey, Saudi Arabia, South Africa, UAE, Israel, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The packaging materials market is evolving rapidly, driven by dual imperatives of performance and sustainability. Core materials like rigid plastic packaging, paperboard cartons, and aluminum beverage containers are being re-engineered to be lighter and more recyclable.

- For boardroom-level strategy, the adoption of renewable fiber-based materials is no longer optional but a core component of risk management and brand positioning, directly impacting extended producer responsibility compliance. The development of high-performance barrier coatings and protective interior coatings is critical for reducing food waste, a key operational metric.

- Innovations in mono-material flexible films and specialty nonwoven fabrics address the challenge of creating circular solutions for flexible formats. As a result of these material advancements, some sectors have documented a 20% improvement in product shelf-life stability. The integration of pressure-sensitive labeling materials and high density polyethylene with higher recycled content underscores the industry-wide commitment to circularity.

What are the Key Data Covered in this Packaging Materials Market Research and Growth Report?

-

What is the expected growth of the Packaging Materials Market between 2026 and 2030?

-

USD 156.58 billion, at a CAGR of 4.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Material (Plastic, Paper and paperboard, Metal, and Glass), End-user (Rigid packaging, and Flexible packaging), Application (Boxes and cartons, Bottles and jars, Bags and pouches, Cans, and Others) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Expansion of electronic commerce and direct retail channels, Extreme volatility in raw material costs and supply chains

-

-

Who are the major players in the Packaging Materials Market?

-

Amcor Plc, AptarGroup Inc., Ardagh Group SA, Avery Dennison Corp., Ball Corp., Berry Global Inc., CCL Industries Inc., Crown Holdings Inc., DS Smith Plc, Graphic Packaging Holding Co., Huhtamaki Oyj, International Paper Co., Mondi Plc, O I Glass Inc., Oji Holdings Corp., Packaging Corp. of America, Sealed Air Corp., Smurfit Westrock plc, Sonoco Products Co. and Tetra Pak International SA

-

Market Research Insights

- The packaging materials market is defined by a dynamic interplay of efficiency and sustainability. The increasing adoption of lightweight packaging solutions and modular packaging designs enables companies to optimize logistics, with some achieving a 15% reduction in freight costs. A significant driver is the shift toward circular economy models, where end-of-life material recovery is paramount.

- This has accelerated innovation in sustainable packaging materials, including biodegradable packaging solutions and those with high post-consumer recycled content. In response to consumer demand and regulations, over 60% of major brands have committed to improving their e-commerce packaging solutions within the next cycle.

- Technologies like smart packaging technologies and digital printing on packaging are also transforming the industry, allowing for better supply chain optimization and enhanced consumer engagement.

We can help! Our analysts can customize this packaging materials market research report to meet your requirements.

RIA -

RIA -