Personal AI Assistant Market Size 2026-2030

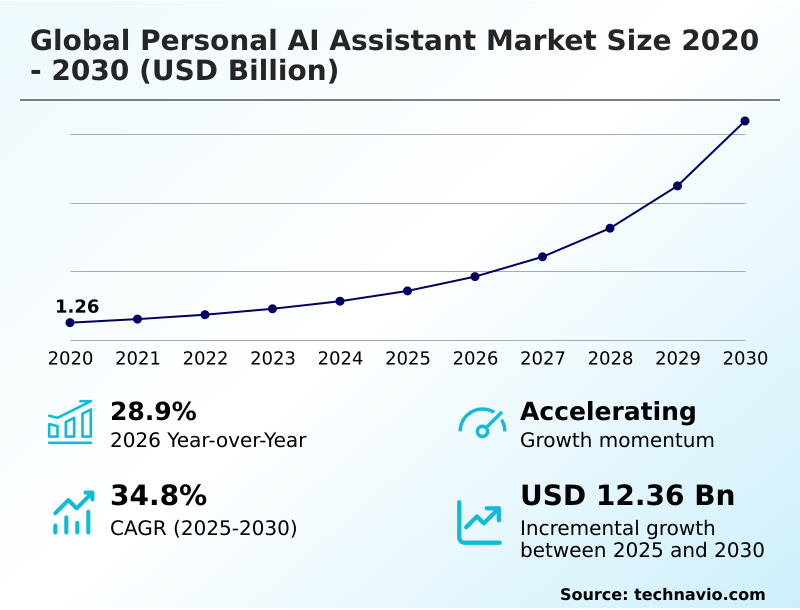

The personal ai assistant market size is valued to increase by USD 12.36 billion, at a CAGR of 34.8% from 2025 to 2030. Proliferation of multimodal large language models will drive the personal ai assistant market.

Major Market Trends & Insights

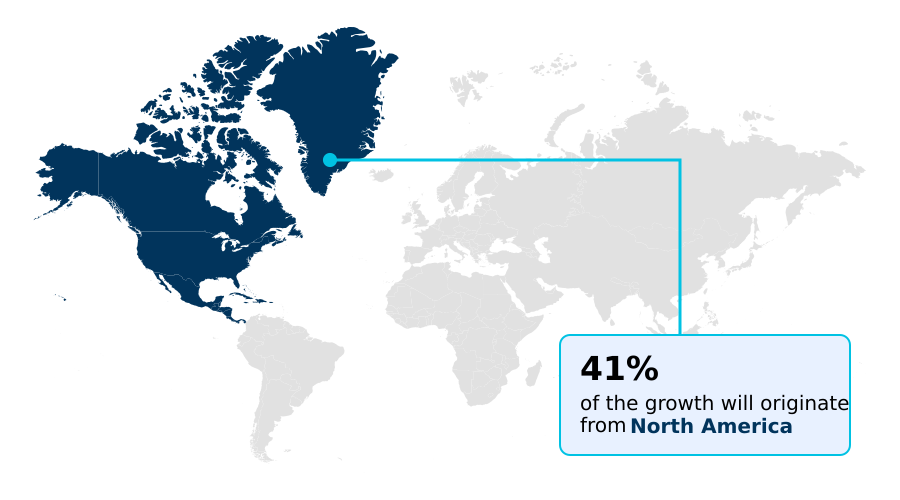

- North America dominated the market and accounted for a 40.6% growth during the forecast period.

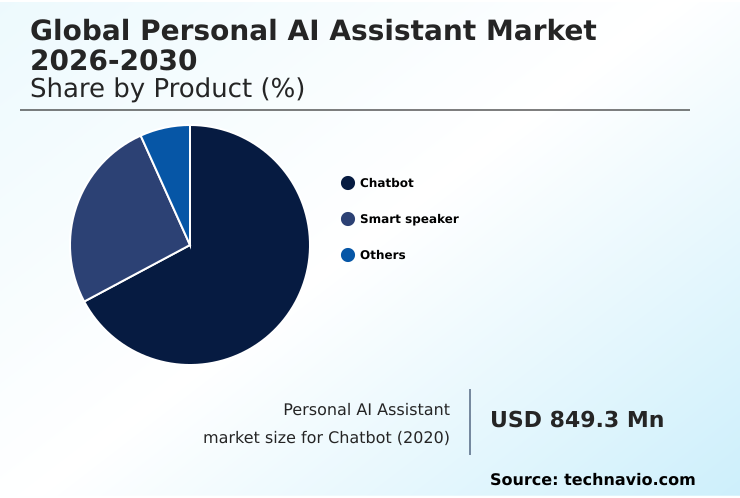

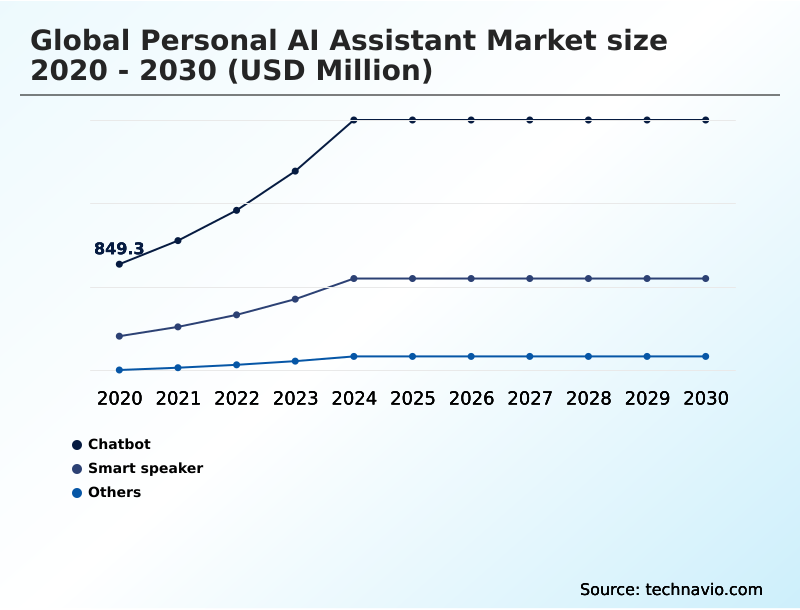

- By Product - Chatbot segment was valued at USD 1.89 billion in 2024

- By Technology - Natural language processing segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 14.67 billion

- Market Future Opportunities: USD 12.36 billion

- CAGR from 2025 to 2030 : 34.8%

Market Summary

- The personal AI assistant market is defined by the development of sophisticated software agents that leverage natural language processing and machine learning to execute diverse tasks for individual users. These systems function by synthesizing vast data quantities, learning user preferences over time to deliver proactive recommendations and streamline task execution.

- Key applications include administrative scheduling, smart home integration, and complex information retrieval. By utilizing neural networks, these assistants provide significant advantages in operational efficiency and cognitive offloading, enabling users to delegate repetitive processes to an intelligent interface.

- In a business context, this translates to tangible productivity gains; for example, an assistant can autonomously monitor project timelines, flag potential delays by analyzing communications, and schedule resolution meetings, freeing up managerial resources for strategic decision-making. As these systems evolve from reactive tools to predictive partners, they become essential assets for enhancing productivity.

- The market is a cornerstone for future advancements in ambient intelligence and hyper-personalized consumer technology, representing a critical shift toward human-centric computing.

What will be the Size of the Personal AI Assistant Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Personal AI Assistant Market Segmented?

The personal ai assistant industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Chatbot

- Smart speaker

- Others

- Technology

- Natural language processing

- Machine learning

- Text-based

- Deployment

- Cloud-based

- On-premises

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Product Insights

The chatbot segment is estimated to witness significant growth during the forecast period.

The chatbot sub-segment is evolving from simple interfaces into sophisticated agentic systems capable of complex reasoning and multi-step task execution. These digital assistants are integrated into mobile apps and enterprise communication platforms, serving as a primary touchpoint for digital interaction.

Modern chatbots leverage generative artificial intelligence to provide nuanced responses, transitioning from reactive tools to proactive digital companions.

Through deep personalization, these conversational AI services learn behavioral patterns to anticipate needs, powering enterprise automation and delivering AI-driven insights that improve workflow efficiency by over 25%.

The scalability of chatbot software allows for immediate deployment of updates, ensuring advancements are available to a global user base and enabling unified communications for seamless cross-platform experiences, whether through voice interaction or text for task automation.

The Chatbot segment was valued at USD 1.89 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Personal AI Assistant Market Demand is Rising in North America Get Free Sample

The market exhibits distinct regional dynamics. North America leads in adoption, driven by mature smart home ecosystems and a focus on cognitive offloading, with over 60% of users leveraging assistants for productivity. The region pioneers hyper-personalized digital experiences.

In APAC, the focus is on mobile-first applications and voice-first interfaces that support linguistic diversity, with some markets seeing a 50% year-over-year increase in text-based interaction for e-commerce.

Europe prioritizes consumer data protection, favoring assistants with strong privacy controls and low-latency performance.

The development of robotic companions in Japan and smart city integration in China showcase the diverse applications of the technology, from enhancing situational awareness to enabling complex multi-step task execution.

This global digital transformation is supported by both cloud-based deployment and localized processing.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The adoption of a personal AI assistant for productivity is accelerating as users seek to automate administrative tasks and enhance efficiency. The move toward agentic AI for task management allows these systems to operate with greater independence, coordinating complex workflows across multiple applications.

- This evolution is particularly impactful for enterprise use of personal assistants, where AI task orchestration across apps can streamline operations. A key area of innovation is in on-device AI for data privacy, which addresses security concerns by processing sensitive information locally.

- This technology is central to privacy-first personal AI solutions and is often deployed through edge AI in wearable devices, creating a seamless user experience. The integration of AI for hyper-personalized experiences is another critical factor, with assistants learning individual preferences to offer tailored suggestions.

- This is enabled by advances in both natural language processing for assistants and machine learning in personal AI. The debate between cloud vs on-premise AI assistants continues, with each model offering distinct benefits in scalability and security.

- In consumer technology, multimodal AI in smart glasses and AI assistants in connected vehicles are becoming more common, while the AI assistant for smart homes market matures. A primary challenge remains in reducing algorithmic hallucination in AI and overcoming AI ecosystem fragmentation to create a truly unified experience.

- For instance, integrated supply chain platforms using agentic AI have demonstrated a greater than 35% improvement in forecast accuracy compared to siloed legacy systems by enabling generative AI for cognitive offloading and leveraging localized intelligence in AI assistants through ambient intelligence and IoT integration.

What are the key market drivers leading to the rise in the adoption of Personal AI Assistant Industry?

- The proliferation of multimodal large language models that process diverse data formats is a primary driver for the personal AI assistant market.

- The proliferation of multimodal large language models is a primary market driver, enabling intelligent automation and sophisticated task orchestration. These models, powered by machine learning and generative artificial intelligence, can synthesize information from text, audio, and visual data.

- This facilitates ambient integration into daily life, providing a continuous stream of support. The expansion of edge AI processing supports autonomous agent capabilities with enhanced user-centric security protocols, allowing for complex computations directly on user devices.

- This approach improves performance by over 30% in response time for critical applications.

- Advancements in reinforcement learning and zero-shot learning are expanding assistant functionalities into new domains, such as personal finance management, without requiring explicit training, further cementing their role as indispensable tools.

What are the market trends shaping the Personal AI Assistant Industry?

- A prominent market trend is the shift toward agentic autonomy, where personal assistants evolve from passive tools to proactive entities capable of independent task orchestration.

- The market is shifting toward agentic autonomy, with proactive digital companions evolving beyond simple commands. This trend is fueled by advances in natural language processing and the integration of persistent memory, allowing for more nuanced interactions. A parallel movement is the rise of privacy-first localized intelligence and data sovereignty, with on-device processing reducing reliance on the cloud and enhancing security.

- This approach mitigates risks like algorithmic hallucination. The convergence of multimodal capabilities is evident in new form factors like augmented reality glasses, which provide real-time contextual information. These systems enable new agent-to-agent communication protocols, paving the way for hyper-realistic AI assistants.

- In some sectors, this shift has led to subscription-based revenue models for advanced features, with firms reporting up to a 15% increase in customer retention for premium AI-driven insights.

What challenges does the Personal AI Assistant Industry face during its growth?

- Navigating complex data privacy regulations and ensuring stringent regulatory compliance represents a key challenge for the personal AI assistant market.

- A significant market challenge is ecosystem fragmentation, where proprietary silos prevent seamless interoperability and a unified user experience. While the agentic AI moment promises great efficiency, this fragmentation hinders progress. The development of small language models designed for on-premises deployment on dedicated neural processing units offers a solution by enabling powerful on-device processing.

- This approach, which supports agentic creativity tools and low-code development, ensures low-latency performance and enhanced security. However, it requires significant investment in privacy-enhancing technologies. The complexity is compounded by the technical need for advanced semantic understanding and unsupervised learning techniques to make these local models effective.

- Organizations adopting on-device strategies have reported a 40% reduction in data transmission costs but face higher initial hardware expenditures.

Exclusive Technavio Analysis on Customer Landscape

The personal ai assistant market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the personal ai assistant market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Personal AI Assistant Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, personal ai assistant market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alibaba Group Holding Ltd. - Key offerings focus on deploying sophisticated software agents that utilize natural language processing and machine learning for hyper-personalized task execution and cognitive offloading for individual users.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alibaba Group Holding Ltd.

- Amazon.com Inc.

- Anthropic

- Apple Inc.

- Baidu Inc.

- Cerence Inc.

- Google LLC

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Infosys Ltd.

- LG Electronics Inc.

- Microsoft Corp.

- NAVER CORP.

- Orange SA

- Samsung Electronics Co. Ltd.

- SK Telecom Co. Ltd.

- Sony Group Corp.

- SoundHound AI Inc.

- Yandex NV

- Zapier Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Personal ai assistant market

- In May 2025, Mistral AI announced the launch of its new Agents API, a major advancement designed to transform traditional language models into action-oriented AI systems capable of interacting with real-world applications.

- In February 2025, Amazon.com Inc introduced Alexa Plus, the next generation of its personal artificial intelligence assistant, powered by generative AI to enable more conversational and task-oriented interactions for users.

- In February 2025, French startup Mistral AI launched 'Le Chat,' a new mobile application for its generative AI assistant, positioning it as a strong alternative to existing AI tools with high-speed response capabilities.

- In June 2025, Apple Inc set an internal target of spring 2026 for releasing its long-delayed Siri artificial intelligence upgrade, aiming to deliver deeper app integration and more natural interactions across its device ecosystem.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Personal AI Assistant Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 34.8% |

| Market growth 2026-2030 | USD 12360.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 28.9% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The personal AI assistant market is undergoing a significant architectural shift from reactive tools to proactive partners. This evolution is driven by advancements in multimodal processing and ambient intelligence, which allow assistants to understand user context with greater depth.

- The integration of conversational intelligence platforms into everyday applications provides enhanced productivity assistance, moving beyond simple voice interaction to handle complex task automation. For corporate leadership, this transition presents a strategic choice regarding investment in proprietary ecosystems versus open, interoperable web-based service models. The decision directly impacts long-term data strategy and customer retention.

- For instance, systems that enable deep personalization by learning user behavior have shown the ability to reduce customer service escalations by over 20%, demonstrating a clear return on investment. As assistants become more embedded in workflows, their role expands from mere convenience to a critical component of operational efficiency and a key driver of competitive differentiation.

What are the Key Data Covered in this Personal AI Assistant Market Research and Growth Report?

-

What is the expected growth of the Personal AI Assistant Market between 2026 and 2030?

-

USD 12.36 billion, at a CAGR of 34.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Chatbot, Smart speaker, and Others), Technology (Natural language processing, Machine learning, and Text-based), Deployment (Cloud-based, and On-premises) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of multimodal large language models, Data privacy and stringent regulatory compliance

-

-

Who are the major players in the Personal AI Assistant Market?

-

Alibaba Group Holding Ltd., Amazon.com Inc., Anthropic, Apple Inc., Baidu Inc., Cerence Inc., Google LLC, Huawei Technologies Co. Ltd., IBM Corp., Infosys Ltd., LG Electronics Inc., Microsoft Corp., NAVER CORP., Orange SA, Samsung Electronics Co. Ltd., SK Telecom Co. Ltd., Sony Group Corp., SoundHound AI Inc., Yandex NV and Zapier Inc.

-

Market Research Insights

- The market is evolving through the rapid integration of autonomous agent capabilities, which enable assistants to perform complex workflows with minimal user intervention, increasing task completion rates by up to 40%. A focus on hyper-personalized digital experiences is driving adoption, as machine learning models create deeply tailored user interactions.

- Demand for robust user-centric security protocols is also shaping development, with on-device processing reducing data vulnerability. The pursuit of seamless cross-platform experiences remains a central goal, although it presents technical challenges.

- In specialized applications like personal finance management, AI-driven insights have demonstrated a 15% improvement in identifying savings opportunities for users, underscoring the technology's practical value and alignment with consumer data protection standards.

We can help! Our analysts can customize this personal ai assistant market research report to meet your requirements.

RIA -

RIA -