Photosensitive Semiconductor Device Market Size 2026-2030

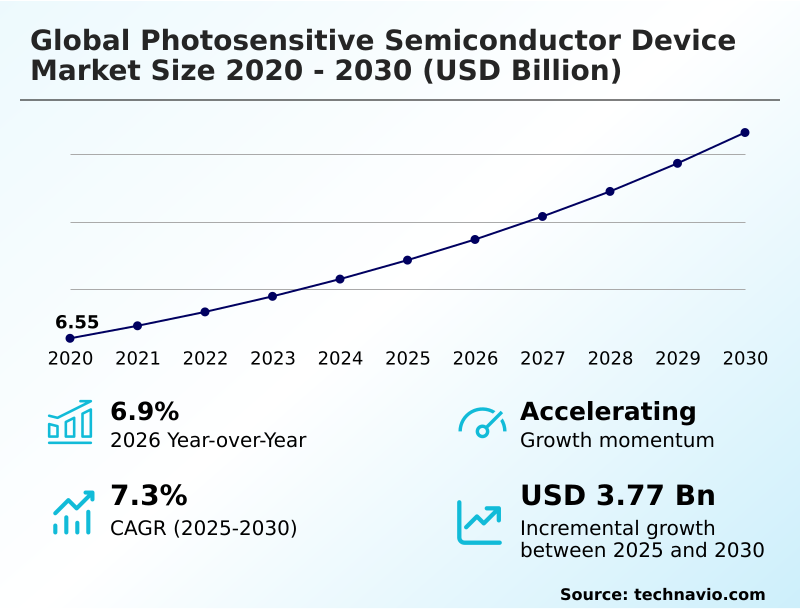

The photosensitive semiconductor device market size is valued to increase by USD 3.77 billion, at a CAGR of 7.3% from 2025 to 2030. Acceleration of autonomous mobility and advanced vehicular sensing will drive the photosensitive semiconductor device market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 62.2% growth during the forecast period.

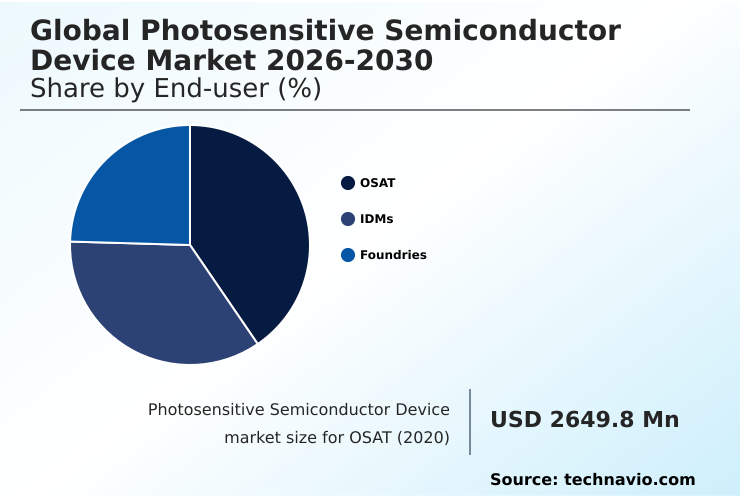

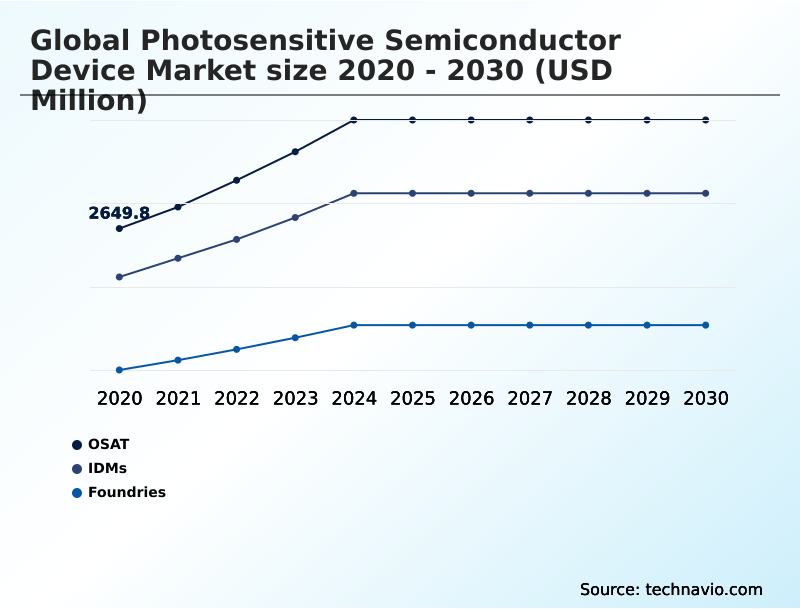

- By End-user - OSAT segment was valued at USD 3.45 billion in 2024

- By Form Factor - Chips segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 6.08 billion

- Market Future Opportunities: USD 3.77 billion

- CAGR from 2025 to 2030 : 7.3%

Market Summary

- The photosensitive semiconductor device market is undergoing a significant transformation, driven by its critical role in converting light into electrical signals across a spectrum of advanced applications. These devices, including photodiodes and image sensors, are fundamental to the expansion of industrial automation, sophisticated automotive safety systems, and the continuing evolution of consumer electronics.

- Growth is fueled by the increasing need for high-precision optical data acquisition and environmental sensing. A key trend is the integration of intelligence at the sensor level, which reduces data transmission and power consumption.

- For instance, in automated manufacturing, a smart sensor can perform on-the-spot quality control, flagging defects in real-time without sending vast amounts of image data to a central processor, improving line efficiency. However, the industry faces challenges from a geographically concentrated supply chain, making it vulnerable to geopolitical shifts.

- The market's trajectory remains robust as innovations in materials and digital logic unlock new capabilities for optical detection.

What will be the Size of the Photosensitive Semiconductor Device Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Photosensitive Semiconductor Device Market Segmented?

The photosensitive semiconductor device industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- OSAT

- IDMs

- Foundries

- Form factor

- Chips

- Packaged sensors

- Modules

- Others

- Product type

- Photodiodes

- Photovoltaic cells

- Photoresistors

- Light-sensitive transistors

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By End-user Insights

The osat segment is estimated to witness significant growth during the forecast period.

Outsourced semiconductor assembly and test (OSAT) providers are crucial to the photosensitive semiconductor device market, offering specialized packaging and verification for complex optical sensors.

These providers manage the intricate integration of optoelectronic components, such as micro-lenses and filters, using advanced fan-out wafer-level packaging and through-silicon via techniques essential for compact, high-performance photodetector assemblies.

The demand for industrial automation and sophisticated power system management in electric vehicles drives the need for robust photoelectric sensor modules made from materials like gallium nitride and silicon carbide.

OSATs enable fabless companies to scale production for remote sensing applications and automated quality control without massive capital expenditure, with specialized testing improving final device yields by over 15% through enhanced optical data processing and handling of materials like high-purity quartz.

The OSAT segment was valued at USD 3.45 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 62.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Photosensitive Semiconductor Device Market Demand is Rising in APAC Get Free Sample

APAC dominates the market, accounting for over 62% of the incremental growth, driven by its vast concentration of semiconductor fabrication facilities.

Nations like China, Japan, and South Korea lead in producing high-performance photodiodes with superior quantum efficiency and spectral response, which are critical for machine vision systems and medical diagnostic equipment.

The region's integrated supply chain supports the massive scale needed for consumer electronics and automotive sectors. Regional expertise in mass-producing components leveraging the photovoltaic effect enables cost-efficiencies unmatched elsewhere.

The rapid adoption of 5G is also boosting demand for components enabling high-speed fiber optic communication, including advanced optical receivers and optical frequency combs, solidifying the region's role as the primary engine for innovation in light-to-electricity conversion and precision photonics instruments.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic application of specialized photosensitive semiconductors is reshaping key industries by enabling unprecedented levels of automation and precision. A photosensitive semiconductor for autonomous vehicles is no longer a simple component but a critical system for environmental perception, integrating data from multiple sensors to ensure safety.

- In communications, the demand for higher bandwidth is met by the high-speed photodiode for fiber optic testing, which verifies network performance with extreme accuracy. Similarly, the cmos image sensor for industrial automation has become the cornerstone of smart factories, where it drives quality control and robotics, leading to operational efficiency gains that can surpass previous benchmarks by double-digit percentages.

- In healthcare, the near-infrared detector for medical imaging allows for non-invasive diagnostics with greater clarity and depth. Inside next-generation vehicles, the time-of-flight sensor for smart cabin applications enhances user experience and safety by enabling gesture control and monitoring occupant status.

- These targeted innovations underscore a market-wide shift from general-purpose components to highly optimized solutions that solve specific, high-value industry problems, defining the next wave of technological integration and competitive advantage.

What are the key market drivers leading to the rise in the adoption of Photosensitive Semiconductor Device Industry?

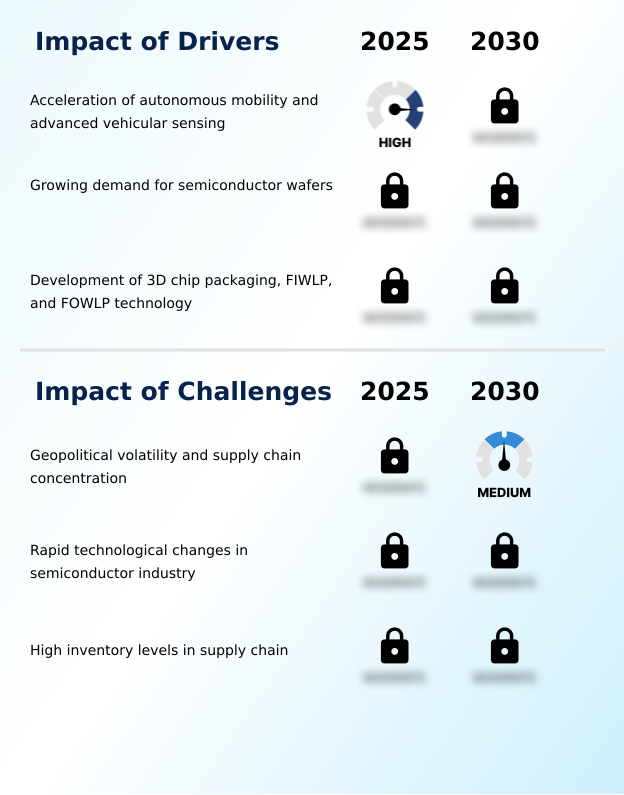

- A key driver for the market is the acceleration of autonomous mobility, which relies on advanced vehicular sensing for environmental perception and safety.

- The acceleration of autonomous mobility is a primary market driver, escalating demand for advanced vehicular sensing components. Modern vehicles require a suite of sensors, including silicon photomultipliers and avalanche photodiodes for precise light detection and ranging (LiDAR), alongside high-dynamic-range cameras.

- The development of sub-micron photosensitive sensors and advanced phototransistors enhances object detection for functions like steering and position sensing. Infrared photodetectors are critical for real-time traffic monitoring in all weather conditions, with some systems processing environmental data with 99% accuracy.

- Innovations in materials, such as perovskite structures and tandem cell architectures, are improving sensor performance, while the supply of noble gases remains critical for manufacturing.

What are the market trends shaping the Photosensitive Semiconductor Device Industry?

- The convergence of artificial intelligence with edge processing in optical sensing architectures represents a key market trend. This integration enables on-device data analysis, which reduces latency and bandwidth requirements.

- The migration of computational logic directly into the sensor is a defining trend, enabling on-device pixel-level processing and real-time object classification. This shift toward heterogeneous integration is creating intelligent light-sensitive transistors and CMOS image sensors that reduce latency in applications like biometric authentication and driver fatigue tracking.

- Advanced back-illuminated sensor designs improve performance, allowing for features like seamless background blurring in video. The development of event-based vision, where a photodetector only records environmental changes, optimizes energy efficiency by up to 40%. This on-chip intelligence supports sophisticated human presence detection for smart cabin environments and aids smart traffic management, making devices more responsive and autonomous.

What challenges does the Photosensitive Semiconductor Device Industry face during its growth?

- Geopolitical volatility and the high concentration of the supply chain pose a significant challenge to the industry's growth and stability.

- Geopolitical volatility and supply chain concentration create significant challenges. The reliance on a few regions for manufacturing processes like photolithography and chemical vapor deposition exposes the market to disruption. This centralization impacts the production of components from single-junction silicon cells to complex electro-optic modulators, affecting optical detection systems globally.

- A shortage in key materials can halt production, increasing dark current noise in lower-grade alternatives and impacting performance. This vulnerability affects applications from industrial security cameras to environmental monitoring and real-time facial recognition.

- The high capital cost to diversify fabrication facilities, which require specialized tools like femtosecond lasers, acts as a barrier, with setting up a new plant costing over 25% more outside of established hubs.

Exclusive Technavio Analysis on Customer Landscape

The photosensitive semiconductor device market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the photosensitive semiconductor device market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Photosensitive Semiconductor Device Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, photosensitive semiconductor device market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Albis Optoelectronics AG - Key offerings include high-performance photodiodes, image sensors, and optoelectronic components engineered for precision industrial, automotive, and communication applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Albis Optoelectronics AG

- Asahi Kasei Corp.

- Beijing Rofea Optoelectronics Ltd.

- CoorsTek Inc.

- Core Electronics.

- FUJIFILM Holdings Corp.

- Hamamatsu Photonics KK

- Menlo Systems GmbH

- Omch

- Ophir Optronics Solutions Ltd.

- OSI Systems Inc.

- Thorlabs Inc.

- Utmel Electronics

- Vishay Intertechnology Inc.

- Winsen Electronics Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Photosensitive semiconductor device market

- In September, 2024, First Solar Inc. announced the commissioning of a new production facility utilizing an advanced thin-film semiconductor layering process to achieve record conversion efficiency for commercial-grade modules.

- In November, 2024, Sony Semiconductor Solutions Corporation released a new series of CMOS image sensors designed for industrial equipment, featuring a global shutter function to eliminate distortion in high-speed production lines.

- In January, 2025, Infineon Technologies AG launched a new generation of silicon photomultipliers that provide enhanced sensitivity for long-range light detection and ranging systems in autonomous vehicles.

- In March, 2025, Sony Semiconductor Solutions Corporation announced the mass production of a high-speed image sensor incorporating a dedicated digital signal processor capable of performing real-time object classification on-chip.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Photosensitive Semiconductor Device Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.3% |

| Market growth 2026-2030 | USD 3769.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.9% |

| Key countries | China, Japan, South Korea, Taiwan, India, Indonesia, US, Canada, Mexico, Germany, France, UK, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The photosensitive semiconductor device market is characterized by rapid innovation in both materials and architecture, fundamentally altering how machines perceive the world. Core components like photodiodes, phototransistors, and advanced CMOS image sensors are seeing significant performance gains.

- Advances in manufacturing, such as precision photolithography and chemical vapor deposition, are enabling the creation of back-illuminated sensor designs with superior quantum efficiency and minimal dark current noise. Boardroom decisions are increasingly influenced by the capabilities of these devices; for example, adopting silicon photomultipliers in autonomous vehicle platforms is a strategic investment in safety compliance and market differentiation.

- This has led to a 20% improvement in object detection accuracy in low-light conditions. Technologies like through-silicon via and fan-out wafer-level packaging are crucial for miniaturization, while new materials like gallium nitride and silicon carbide are expanding application possibilities beyond traditional silicon.

What are the Key Data Covered in this Photosensitive Semiconductor Device Market Research and Growth Report?

-

What is the expected growth of the Photosensitive Semiconductor Device Market between 2026 and 2030?

-

USD 3.77 billion, at a CAGR of 7.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (OSAT, IDMs, and Foundries), Form Factor (Chips, Packaged sensors, Modules, and Others), Product Type (Photodiodes, Photovoltaic cells, Photoresistors, and Light-sensitive transistors) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Acceleration of autonomous mobility and advanced vehicular sensing, Geopolitical volatility and supply chain concentration

-

-

Who are the major players in the Photosensitive Semiconductor Device Market?

-

Albis Optoelectronics AG, Asahi Kasei Corp., Beijing Rofea Optoelectronics Ltd., CoorsTek Inc., Core Electronics., FUJIFILM Holdings Corp., Hamamatsu Photonics KK, Menlo Systems GmbH, Omch, Ophir Optronics Solutions Ltd., OSI Systems Inc., Thorlabs Inc., Utmel Electronics, Vishay Intertechnology Inc. and Winsen Electronics Co. Ltd.

-

Market Research Insights

- Market dynamics are shaped by a convergence of technological advancement and evolving end-user demands. The push for autonomous mobility and enhanced safety in vehicles drives the need for precise advanced vehicular sensing technologies, including light detection and ranging systems and high-dynamic-range cameras.

- In industrial settings, the adoption of machine vision systems for automated quality control has improved defect detection rates by over 30%. Concurrently, the consumer electronics sector leverages photosensitive devices for features like biometric authentication and background blurring. The development of smart cabin environments in cars uses time-of-flight sensor technology for human presence detection, increasing responsiveness.

- These applications demonstrate a shift toward embedded intelligence, reducing system-level power consumption by as much as 40% in certain IoT devices.

We can help! Our analysts can customize this photosensitive semiconductor device market research report to meet your requirements.

RIA -

RIA -