Polysomnography Devices Market Size 2024-2028

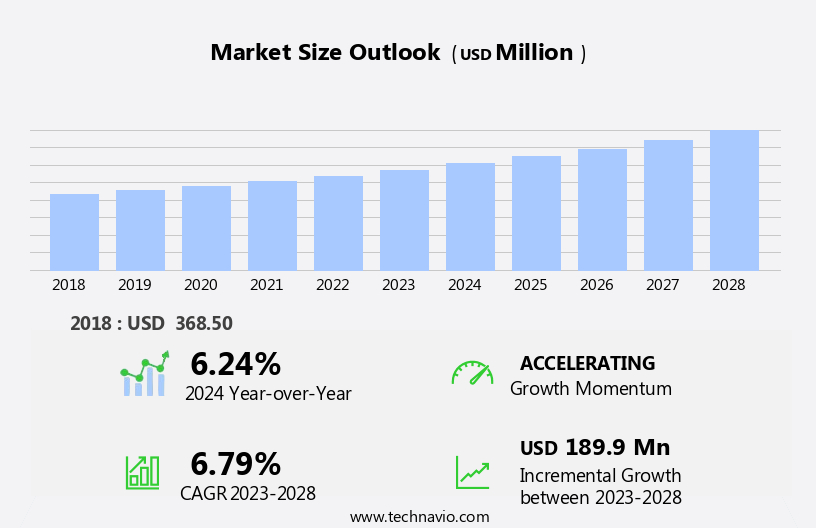

The polysomnography devices market size is forecast to increase by USD 189.9 million at a CAGR of 6.79% between 2023 and 2028.

- The market is poised for significant growth, driven by favorable reimbursement scenarios and advancements in technology. Reimbursement policies, particularly in developed regions, continue to improve, enabling wider access to diagnostic sleep studies. This trend is expected to boost market expansion, particularly in the home sleep testing segment. Moreover, technological innovations, such as portable and wireless devices, are transforming the polysomnography landscape. These advancements offer greater convenience, accuracy, and patient comfort, making them increasingly popular alternatives to traditional lab-based tests.

- However, challenges persist, including the high cost of devices and the need for specialized training to operate them effectively. These factors may limit market penetration, particularly in developing regions. Companies seeking to capitalize on market opportunities must focus on cost reduction strategies and developing user-friendly devices to address these challenges effectively.

What will be the Size of the Polysomnography Devices Market during the forecast period?

- The market continues to evolve, driven by advancements in technology and growing applications across various sectors. Digital health solutions, including CPAP therapy, diagnostic testing, data analysis, home sleep testing, and at-home sleep studies, are revolutionizing the diagnosis and treatment of sleep disorders. The integration of remote monitoring, wearable technology, and cloud computing enables real-time patient data collection and analysis, leading to improved clinical outcomes. Sleep disorders, such as obstructive and central sleep apnea, restless legs syndrome, and sleep-wake disorders, are increasingly being addressed through these innovative technologies. Patient engagement is enhanced through patient education, lifestyle modifications, and mobile health applications.

- Data security and privacy remain critical concerns, with regulatory compliance and machine learning algorithms ensuring the protection of sensitive patient information. Biometric sensors, pulse rate, oxygen saturation, and respiratory airflow data are seamlessly integrated into sleep staging and sleep scoring systems, providing healthcare providers with valuable insights for treatment recommendations. The ongoing development of sensor fusion, artificial intelligence, and big data analytics continues to unfold, offering the potential for more accurate diagnosis and personalized treatment plans. Oral appliances and bipap therapy are also gaining popularity as alternative treatments for sleep-disordered breathing. In the home healthcare setting, the use of polysomnography devices is expanding, enabling patients to receive accurate diagnoses and ongoing monitoring from the comfort of their own homes.

- Sleep hygiene, body position, and sleep architecture are essential considerations in the effective use of these devices. The market is characterized by its continuous dynamism, with new innovations and applications emerging regularly. The integration of these technologies into clinical practice is improving patient satisfaction, quality of life, and overall healthcare outcomes.

How is this Polysomnography Devices Industry segmented?

The polysomnography devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Hospitals

- Sleep clinics and diagnostic laboratories

- ASCs

- Homecare

- Type

- Ambulatory polysomnography devices

- Clinical polysomnography devices

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

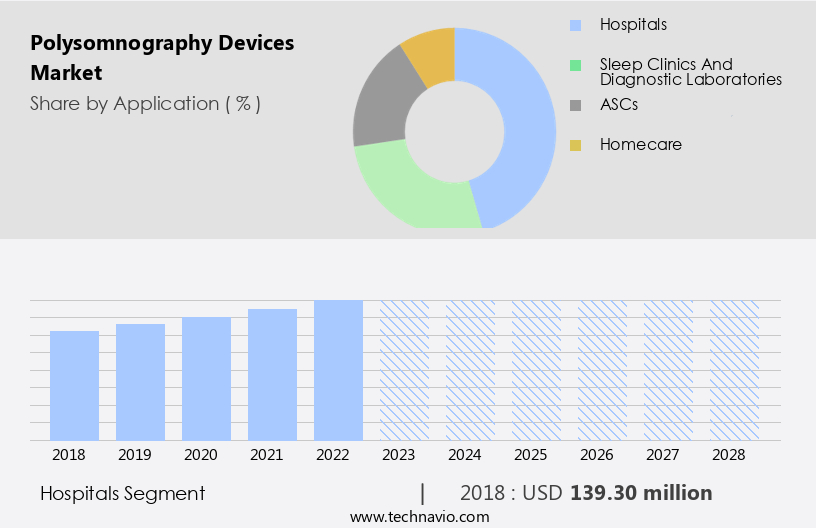

By Application Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

In the realm of healthcare, hospitals serve as vital institutions for diagnosing and treating various sleep disorders. Hospital-based sleep facilities, also known as sleep labs or clinics, offer advanced diagnostic testing and specialized care for patients with sleep issues, often co-existing with more complex health conditions. These facilities, situated within hospital campuses, are staffed with skilled technicians and equipped with state-of-the-art polysomnography devices. Patient engagement is a crucial aspect of sleep disorder management. Hospital-based sleep centers provide an immersive experience, emphasizing patient education and sleep hygiene. Patients receive comprehensive treatment recommendations, including lifestyle modifications, CPAP therapy, BIPAP therapy, oral appliances, and sleep position adjustments.

Data security is a significant concern in the digital health landscape. Cloud computing and data analysis play a pivotal role in ensuring data privacy and regulatory compliance. Advanced technologies like machine learning and artificial intelligence are employed to analyze sleep data, providing healthcare providers with valuable insights for accurate diagnosis and treatment plans. Remote patient monitoring, home sleep testing, and wearable technology enable continuous monitoring and early detection of sleep-disordered breathing, obstructive sleep apnea, central sleep apnea, restless legs syndrome, and other sleep disorders. These solutions promote better patient satisfaction and improve clinical outcomes. Mobile health applications and biometric sensors contribute to remote monitoring and data collection, providing real-time information on pulse rate, oxygen saturation, and sleep architecture.

This data is analyzed using big data analytics and sensor fusion, allowing healthcare providers to make informed decisions regarding patient care. Incorporating data analysis and patient education into sleep disorder management enhances treatment effectiveness and overall quality of life. Sleep centers prioritize patient satisfaction, ensuring harmonious and striking experiences, emphasizing the importance of sleep hygiene and addressing individual needs.

The Hospitals segment was valued at USD 139.30 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

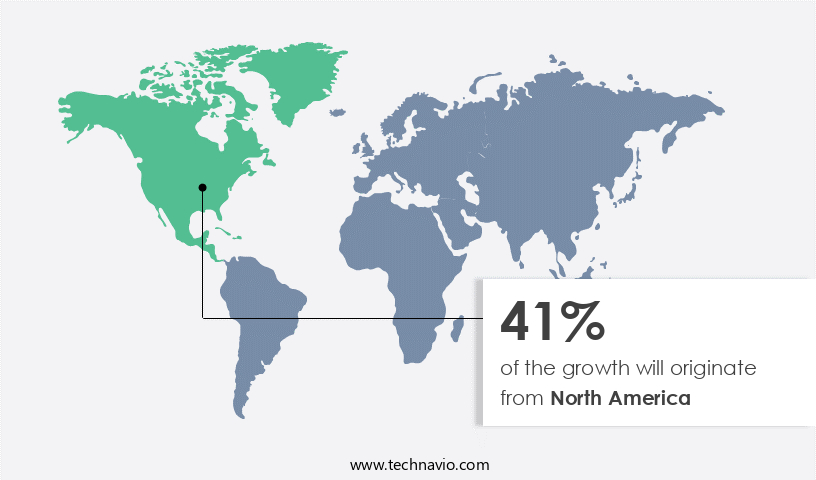

North America is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in the US is experiencing significant growth due to the rising prevalence of sleep apnea, particularly obstructive sleep apnea (OSA). Undiagnosed sleep apnea imposes a substantial economic burden on healthcare, with estimates suggesting that the annual cost in the US is around USD149 billion, in addition to an extra USD20-40 billion for additional medical expenses and healthcare utilization. Factors such as aging and obesity increase the risk of developing OSA, and the growing geriatric population in North America, projected to reach over 71 million by 2030, poses a considerable challenge to the public health system. Patients' engagement and education are crucial in managing sleep disorders, leading to the increasing adoption of digital health solutions, mobile health applications, and wearable technology for remote patient monitoring and at-home sleep studies.

Data security and privacy are essential considerations in the digital health landscape, with cloud computing and big data analytics playing a significant role in enhancing data security and facilitating data analysis. Advanced technologies like machine learning and artificial intelligence are transforming diagnostic testing and sleep scoring, enabling more accurate and efficient analysis of sleep architecture and sleep staging. Regulatory compliance and treatment recommendations are essential components of effective sleep disorder management, with various therapies such as CPAP, BiPAP, and oral appliances offering effective solutions for sleep-disordered breathing. Lifestyle modifications, such as sleep hygiene and body position, can also significantly impact sleep quality and contribute to better clinical outcomes.

The market is also witnessing the emergence of advanced technologies like sensor fusion and biometric sensors, which offer improved accuracy and patient satisfaction. Healthcare providers are increasingly embracing these technologies to enhance patient care and improve quality of life for those suffering from sleep disorders.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Polysomnography Devices Industry?

- The favorable reimbursement scenario serves as the primary catalyst for market growth. In this dynamic business environment, understanding and navigating reimbursement policies effectively is crucial for market success.

- Polysomnography devices play a crucial role in diagnosing sleep-disordered breathing conditions, such as obstructive sleep apnea (OSA), by continuously recording various physiological parameters during sleep. Regulatory compliance is essential for the market's growth, ensuring the devices meet specific safety and efficacy standards. Advancements in technology have led to the integration of artificial intelligence (AI), biometric sensors, machine learning, and big data analytics in polysomnography devices. These innovations enhance diagnostic accuracy and improve patient comfort. Sensor fusion is another significant development, allowing the simultaneous measurement of multiple physiological parameters, such as oxygen saturation, pulse rate, and brain activity. Healthcare providers increasingly rely on polysomnography devices to improve patient quality of life by accurately diagnosing and treating sleep disorders.

- Reimbursements and coverage for these devices have been favorable, making diagnostic testing more accessible to individuals who require it. For instance, attended full-channel nocturnal polysomnography is necessary for individuals with suspected OSA if previous home sleep apnea tests (HSAT) results are negative, technically inadequate, or indeterminate. Additionally, individuals under 18 years old, those with comorbid medical conditions, or those with documented ongoing epileptic seizures along with sleep disorder symptoms also qualify for this diagnostic testing.

What are the market trends shaping the Polysomnography Devices Industry?

- Polysomnography technology is continually advancing, representing a significant market trend. Innovations in polysomnography devices are driving progress in the diagnosis and treatment of sleep disorders.

- Polysomnography devices have witnessed significant advancements in technology, revolutionizing the diagnosis and management of sleep disorders. One notable trend is the emergence of wearable or portable polysomnography devices, which offer increased patient engagement and mobility. Cleveland Medical Devices' Sapphire PSG system is an example, featuring 22 channels, advanced wireless hardware, and Crystal PSG software for managing patient data, acquiring, scoring, and reporting data. This wireless system supports attended, remotely attended, and unattended sleep diagnoses, enhancing patient comfort. Another innovation is SOMNOtouch RESP from SOMNOmedics, which bridges the gap between a polysomnograph and a polygraph. This device offers remote patient monitoring, data security, and patient education, enabling lifestyle modifications and bipap therapy for sleep-wake disorders, respiratory airflow issues, and restless legs syndrome.

- Furthermore, cloud computing technology facilitates data storage and access, allowing healthcare professionals to analyze patient data from anywhere. These technological advancements contribute to improved patient care and outcomes.

What challenges does the Polysomnography Devices Industry face during its growth?

- The exploration for viable alternatives to polysomnography devices poses a significant challenge to the industry's expansion. Polysomnography, a diagnostic technique for sleep disorders, relies heavily on specialized equipment for accurate assessment. The need for continuous innovation and improvement in this field is crucial to meet the growing demand for effective sleep disorder solutions while maintaining cost-effectiveness and accessibility.

- Polysomnography devices have seen significant competition from Home Sleep Apnea Tests (HSAT) and remote monitoring solutions in the diagnostic testing of sleep disorders, particularly Obstructive Sleep Apnea (OSA). HSAT has gained popularity due to its convenience, allowing patients to undergo testing in the comfort of their own homes. This alternative method is as effective as traditional polysomnography for OSA detection, with comparable results in terms of titration pressures, CPAP adherence, functional outcomes, and treatment time. HSAT's major advantage lies in its convenience and flexibility, eliminating the need for patients to stay overnight in a lab for testing.

- Digital health technologies, such as data analysis and wearable technology, have further enhanced the capabilities of HSAT, enabling remote monitoring and real-time data transmission for further evaluation by healthcare professionals. As the market for sleep disorders continues to grow, the integration of advanced technologies in diagnostic testing and remote monitoring is expected to drive clinical outcomes and improve patient care. The future of polysomnography devices lies in their ability to provide accurate, convenient, and cost-effective solutions for diagnosing and managing sleep disorders.

Exclusive Customer Landscape

The polysomnography devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the polysomnography devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, polysomnography devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advin Health Care - The company specializes in providing advanced polysomnography solutions, including the 09G01 polysomnography machine. This device is integral to diagnosing and treating sleep disorders through continuous recording and analysis of various physiological parameters during sleep. By utilizing state-of-the-art technology, our offerings enhance the accuracy and efficiency of sleep studies, ultimately improving patient care. Our commitment to innovation and excellence sets us apart in the field of sleep diagnostics.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advin Health Care

- BMC MEDICAL CO. LTD.

- Cadwell Industries Inc.

- Cleveland Medical Devices Inc.

- Compumedics Ltd.

- Contec Medical Systems Co. Ltd.

- Genotronics

- Koninklijke Philips N.V.

- Lowenstein Medical Technology GmbH and Co. KG

- MEDATEC Medical Data Technology SPRL BVBA

- Medicom MTD Ltd

- Natus Medical Inc.

- Neurosoft

- Neurovirtual USA

- Nihon Kohden Corp.

- Nox Medical

- Recorders and Medicare Systems Pvt Ltd

- ResMed Inc.

- SOMNOmedics GmbH

- Vyaire Medical Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Polysomnography Devices Market

- In February 2024, Philips Healthcare introduced the new Respironics Series EveraLink PSG and Portable Sleep & Diagnostic Solutions, expanding its polysomnography product portfolio. These advanced devices offer improved patient comfort and streamlined workflows, making sleep diagnosis more accessible (Philips Healthcare Press Release).

- In May 2025, ResMed and Nestle Health Science announced a strategic collaboration to integrate ResMed's sleep apnea devices with Nestle Health Science's nutritional solutions, aiming to improve patient outcomes by addressing both sleep disorders and associated health conditions (ResMed Press Release).

- In September 2024, Medtronic completed the acquisition of Inovonics, a leading provider of wireless sensors and monitoring solutions for sleep and respiratory care. This acquisition strengthened Medtronic's portfolio and enabled the company to offer more comprehensive solutions for sleep disorders (Medtronic Press Release).

- In March 2025, the Food and Drug Administration (FDA) granted clearance for the use of non-contact infrared temperature sensors for sleep studies, enabling more accurate and contactless temperature monitoring during polysomnography. This approval marked a significant technological advancement in the field, improving patient safety and comfort (FDA Press Release).

Research Analyst Overview

The market is witnessing significant advancements, driven by the increasing focus on improving sleep efficiency and addressing various sleep disorders. REM and NREM sleep stages are crucial indicators of sleep quality, with sleep fragmentation, sleep debt, oxygen desaturation, and apnea-hypopnea index being key metrics. Personalized and precision medicine are transforming the landscape, enabling virtual care and remote diagnostics through polygraphic recording.

Cardiovascular health, neurological disorders, cognitive function, mental health, and respiratory disturbance index are interconnected aspects of sleep health that polysomnography devices address. The integration of health informatics, data visualization, predictive analytics, digital therapeutics, patient portals, and sleep-wake regulation technologies is revolutionizing the industry, providing insights into circadian rhythm and sleep-wake cycle disruptions due to sleep deprivation.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Polysomnography Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

168 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.79% |

|

Market growth 2024-2028 |

USD 189.9 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.24 |

|

Key countries |

US, Germany, UK, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Polysomnography Devices Market Research and Growth Report?

- CAGR of the Polysomnography Devices industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the polysomnography devices market growth of industry companies

We can help! Our analysts can customize this polysomnography devices market research report to meet your requirements.

RIA -

RIA -