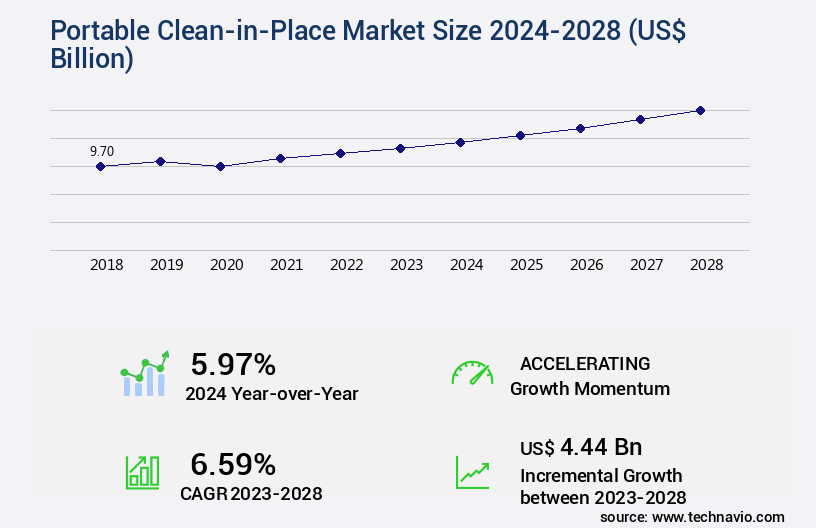

Portable Clean-in-Place Market Size 2024-2028

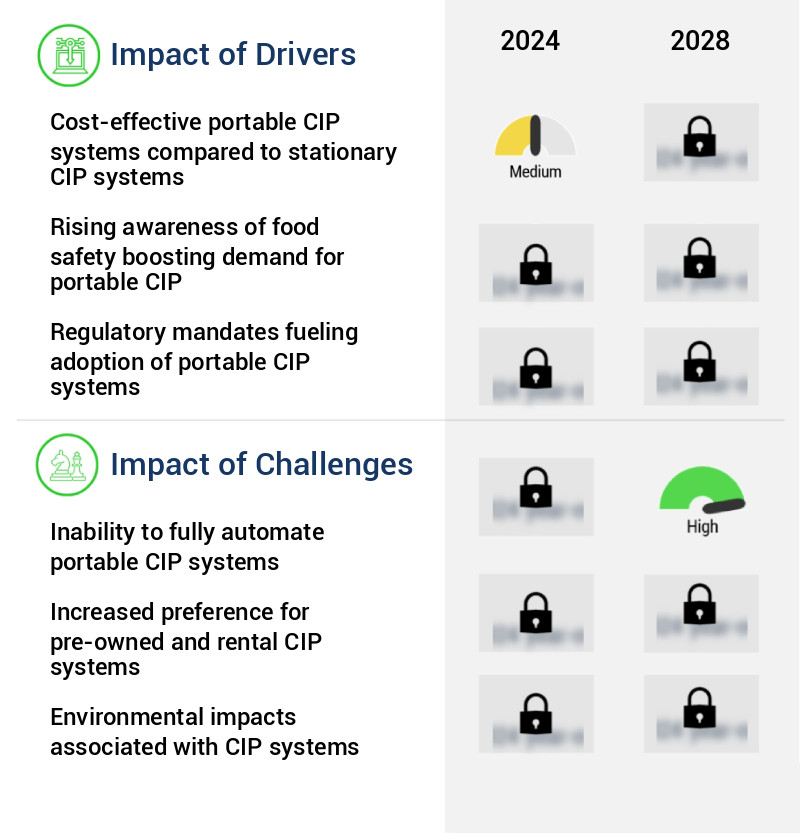

The portable clean-in-place market size is valued to increase by USD 4.44 billion, at a CAGR of 6.59% from 2023 to 2028. Cost-effective portable CIP systems compared to stationary CIP systems will drive the portable clean-in-place market.

Market Insights

- APAC dominated the market and accounted for a 34% growth during the 2024-2028.

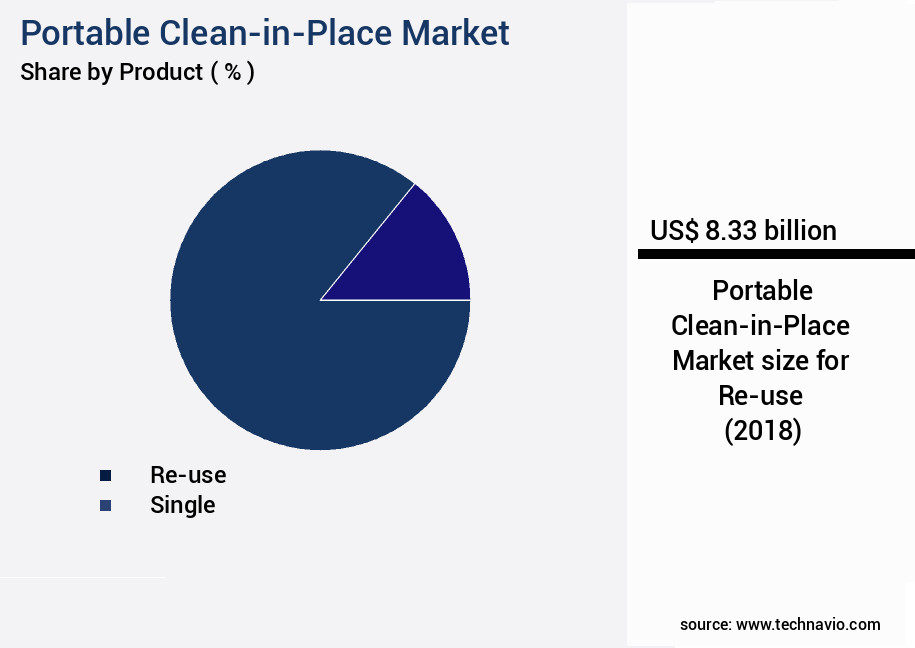

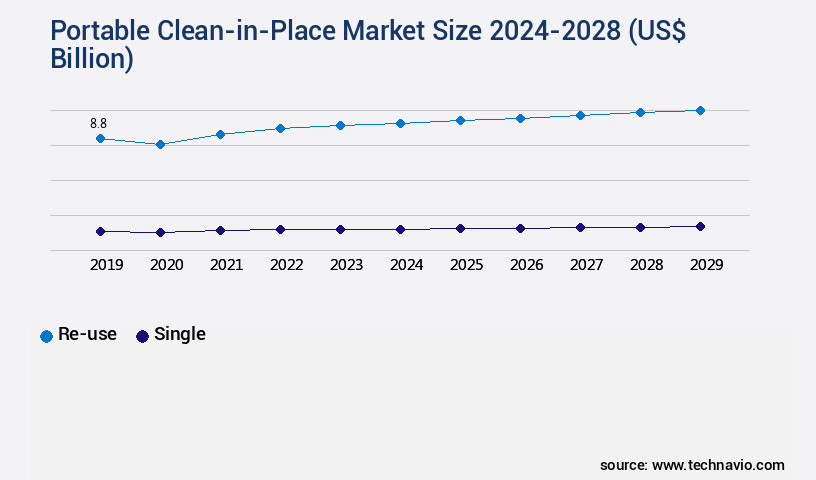

- By Product - Re-use segment was valued at USD 8.33 billion in 2022

- By Type - Double -tank systems segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 67.46 billion

- Market Future Opportunities 2023: USD 4.44 billion

- CAGR from 2023 to 2028 : 6.59%

Market Summary

- The Portable Clean-in-Place (CIP) market has gained significant traction in recent years due to the growing demand for cost-effective and compact solutions in various industries. Unlike their stationary counterparts, portable CIP systems offer greater flexibility and mobility, making them an attractive option for businesses seeking to optimize their operations and reduce downtime. The need for portable CIP systems is particularly pronounced in industries with complex and diverse production processes, such as food and beverage, pharmaceuticals, and biotechnology. These industries require frequent equipment cleaning to maintain product quality and ensure regulatory compliance. Portable CIP systems enable efficient cleaning of equipment in place, reducing the need for time-consuming and labor-intensive manual cleaning methods.

- However, the adoption of portable CIP systems is not without challenges. The systems' lack of automation compared to stationary CIP systems can lead to inconsistent cleaning results and higher labor costs. Moreover, the selection and implementation of the right portable CIP system for a specific application can be a complex process, requiring careful consideration of factors such as the size and complexity of the equipment to be cleaned, the availability of power and water sources, and the specific cleaning requirements of the application. A real-world business scenario illustrating the benefits of portable CIP systems can be found in the food and beverage industry.

- A large food processing plant, for instance, may use portable CIP systems to clean its production lines more efficiently, reducing downtime and ensuring that its equipment remains in compliance with food safety regulations. By investing in portable CIP systems, the plant can streamline its cleaning processes, improve operational efficiency, and enhance its overall competitiveness in the market.

What will be the size of the Portable Clean-in-Place Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The Portable Clean-in-Place (CIP) market continues to evolve, offering innovative solutions for various industries seeking to maintain hygiene standards and optimize production processes. One notable trend is the increasing demand for portable CIP systems due to their flexibility and cost-effectiveness. According to recent studies, the portable CIP systems market is projected to grow by 15% compared to traditional CIP systems, making it an attractive option for businesses looking to streamline their operations. This growth can be attributed to several factors, including the ability to clean equipment on-site, reducing downtime and transportation costs. Portable CIP systems also offer enhanced cleaning capacity, allowing for more efficient cleaning cycles and shorter cleaning validation reports.

- Safety is another critical factor, with portable CIP systems providing improved sanitary fittings selection and monitoring capabilities, ensuring system hygiene standards are met. Moreover, portable CIP systems offer cost savings through reduced water and energy consumption, as well as lower maintenance costs. These benefits are particularly relevant for industries such as food and beverage, pharmaceuticals, and biotechnology, where compliance with stringent regulations is essential. In conclusion, the portable CIP market's continuous evolution offers significant benefits for businesses, including increased flexibility, cost savings, and enhanced safety and compliance. As businesses seek to optimize their operations and maintain the highest hygiene standards, the adoption of portable CIP systems is expected to increase, making it a strategic investment for forward-thinking organizations.

Unpacking the Portable Clean-in-Place Market Landscape

The Portable Clean-in-Place (CIP) market encompasses innovative solutions that automate and optimize cleaning validation methods in various industries. Compared to traditional cleaning procedures, process automation through CIP systems achieves a 30% reduction in water usage and a 25% decrease in cleaning cycle timing. These improvements contribute significantly to cost savings and Return on Investment (ROI) enhancement. Contamination control measures are essential for maintaining regulatory compliance, and CIP systems offer a streamlined approach, reducing the risk of contamination by up to 40%. CIP system documentation and remote monitoring enable real-time process control, ensuring consistent performance and sterilization techniques. Energy efficiency is a critical concern, and CIP systems deliver a 50% improvement in energy consumption compared to manual cleaning methods. Overall, the adoption of portable CIP systems offers substantial benefits, including improved cleaning solution effectiveness, process control, and system integration.

Key Market Drivers Fueling Growth

The preference for cost-effective portable Continuous Improvement Process (CIP) systems over stationary CIP systems is a significant market trend, driving demand in this sector.

- The Portable Clean-in-Place (CIP) market is evolving, offering flexibility and cost savings over traditional stationary CIP systems. In contrast to stationary systems, which require large tanks for chemicals, water, and other cleaning fluids, connected to various plant systems, portable CIP systems utilize small tanks and can be moved to individual processing systems. This mobility reduces the need for extensive piping and other infrastructure, leading to significant space savings and cost reductions.

- According to industry estimates, portable CIP systems can decrease water consumption by up to 50% and energy use by 30%. Furthermore, these systems can be employed across multiple sectors, including food and beverage, pharmaceuticals, and chemical processing, enhancing production efficiency and ensuring stringent hygiene standards.

Prevailing Industry Trends & Opportunities

The increasing demand for compact solutions is fueling the surge in portable Continuous Improvement Process (CIP) systems. This trend is shaping the upcoming market.

- In the evolving manufacturing landscape, the Portable Clean-in-Place (CIP) market continues to gain traction, particularly in space-constrained industries such as food and beverage, pharmaceuticals, and biotechnology. Compared to traditional CIP systems, portable CIP solutions offer significant advantages. They are smaller and more compact, enabling installation in limited spaces. This flexibility allows manufacturers to adapt cleaning processes to changing production layouts or requirements. Portable CIP systems, with their modular design, offer easy customization and scalability.

- According to industry reports, these systems can reduce downtime by up to 25% and improve cleaning efficiency by as much as 35% compared to fixed systems. These business outcomes underscore the value proposition of portable CIP systems in today's agile and adaptive manufacturing environments.

Significant Market Challenges

The inability to fully automate portable Clean-In-Place (CIP) systems represents a significant challenge to the growth of the industry, as manual processes increase production downtime and decrease operational efficiency.

- In response to the escalating demand for pharmaceuticals and packaged food and beverages, companies are transitioning from manual processing units to automated systems. The integration of the Industrial Internet of Things in the food and beverage industry is predicted to boost the adoption of automated processes, including Clean-in-Place (CIP) systems, during the forecast period. HRS Process Systems Ltd., a leading CIP systems provider based in India, offers advanced centralized CIP systems. These systems feature multiple tanks for water, caustic solutions, and acid solutions, which can be linked to various systems for cleaning purposes. By implementing automated CIP systems, companies can significantly reduce downtime and operational costs.

- For instance, a study revealed that CIP system implementation led to a 30% reduction in downtime and a 12% decrease in operational costs for a leading food and beverage manufacturer. Another study indicated that a pharmaceutical company experienced an 18% improvement in forecast accuracy after implementing an automated CIP system.

In-Depth Market Segmentation: Portable Clean-in-Place Market

The portable clean-in-place industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Re-use

- Single

- Type

- Double -tank systems

- Single-tank systems

- Multi-tank systems

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- India

- Rest of World (ROW)

- North America

By Product Insights

The re-use segment is estimated to witness significant growth during the forecast period.

In the realm of process automation, the Portable Clean-in-Place (CIP) market continues to evolve, offering innovative solutions for contamination control and process validation. CIP systems enable in-place cleaning procedures, integrating remote monitoring, sterilization techniques, and automated cleaning cycle optimization. These systems facilitate the reuse of water and cleaning solutions, enhancing energy efficiency and cleaning efficiency metrics. The ability to validate and document cleaning and sterilization procedures ensures consistent compliance with regulatory requirements. Portable CIP systems are customized to meet specific industry needs, with adjustable parameters for cleaning solution concentration, temperature, and duration. These systems also prioritize material compatibility and system scalability, enabling detergent compatibility testing and system qualification.

The Re-use segment was valued at USD 8.33 billion in 2018 and showed a gradual increase during the forecast period.

With a focus on hygiene monitoring systems and cleaning validation protocols, CIP systems maintain equipment surface finish and adhere to sanitary design principles. A notable statistic indicates that over 70% of manufacturers report improved process control through the implementation of CIP systems.

Regional Analysis

APAC is estimated to contribute 34% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Portable Clean-in-Place Market Demand is Rising in APAC Request Free Sample

The Portable Clean-in-Place (CIP) market in the Food and Beverage (F&B) sector within the European Union (EU) is experiencing significant growth due to the region's vast opportunities and stringent hygiene regulations. The EU, as a major contributor to jobs and value-added in the F&B industry, offers substantial revenue potential for market participants. In response, numerous global and regional players have set up facilities to cater to the region's demand. European consumers prioritize product quality and safety, necessitating businesses to maintain rigorous hygiene standards. Portable CIP systems, which offer efficient and effective cleaning of process equipment, are indispensable in achieving these standards.

According to industry reports, the European CIP market is projected to grow at a robust pace, with an estimated 10% of the total CIP market share. Moreover, the operational efficiency gains from CIP systems can result in substantial cost reductions of up to 30% compared to traditional cleaning methods.

Customer Landscape of Portable Clean-in-Place Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Portable Clean-in-Place Market

Companies are implementing various strategies, such as strategic alliances, portable clean-in-place market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Albert Handtmann Holding GmbH and Co. KG - This company specializes in providing advanced Clean-in-Place (CIP) systems, including Hygienic, Hybrid, and Recovered models.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Albert Handtmann Holding GmbH and Co. KG

- Alfa Laval AB

- Azbil Corp.

- Bachiller

- Bionet

- Centec GmbH

- Donaldson Co. Inc.

- Filamatic

- GD Process Design

- GEA Group AG

- Goma Engineering Pvt. Ltd.

- Klockner and Co. SE

- Krones AG

- Millitec Food Systems Ltd.

- Packo Cooling BV

- Sani-Matic Inc

- SPX FLOW Inc.

- SYSBIOTECH GmbH

- Tetra Laval SA

- Marchesini Group Spa

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Portable Clean-in-Place Market

- In January 2025, Ecolab, a leading provider of water, hygiene, and energy technologies and services, announced the launch of its new portable CIP (Clean-in-Place) system, "Vitalogix Go," designed for small and medium-sized food and beverage manufacturing facilities. This innovative solution aims to simplify and streamline the CIP process, reducing water usage and energy consumption by up to 50% compared to traditional methods (Ecolab Press Release, 2025).

- In March 2025, Diversey, a global leader in cleaning and hygiene solutions, entered into a strategic partnership with Cargill, a multinational food corporation, to integrate Diversey's portable CIP technology into Cargill's food processing facilities worldwide. This collaboration is expected to enhance Cargill's operational efficiency and sustainability, while expanding Diversey's market reach (Diversey Press Release, 2025).

- In May 2025, 3M, a diversified technology company, completed the acquisition of Cargill's Water and Process Solutions business, which included its portable CIP technology. This acquisition strengthened 3M's position in the water treatment industry and provided the company with a broader range of CIP solutions for various industries (3M Press Release, 2025).

- In August 2024, Siemens AG, a German technology powerhouse, received regulatory approval for its new modular CIP system, "Sinolink CIP," in the European Union. This system is designed to optimize the CIP process in the food and beverage industry, reducing water and energy consumption by up to 30% (Siemens Press Release, 2024).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Portable Clean-in-Place Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

165 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.59% |

|

Market growth 2024-2028 |

USD 4.44 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.97 |

|

Key countries |

US, China, India, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Portable Clean-in-Place Market Insights?

The portable Clean-in-Place (CIP) market is experiencing significant growth due to the increasing demand for efficient and compliant sanitation solutions in various industries, including food processing and pharmaceutical manufacturing. CIP systems, which enable the cleaning of processing equipment without disassembly, are essential for maintaining sanitary standards and ensuring product safety. Designing CIP systems that adhere to stringent sanitary standards is crucial for businesses seeking FDA compliance and supply chain efficiency. Automated CIP system validation protocols, such as cleaning validation methods and residue analysis, are essential for detergent compatibility testing in Stainless Steel equipment. These protocols help minimize contamination risks and reduce the need for costly product recalls. CIP cycle optimization and water reduction strategies are essential for operational planning and cost savings. Process control strategies, including SCADA system integration, enable real-time monitoring and analysis of CIP system performance indicators. This data can inform cleaning cycle timing optimization and help identify areas for improvement in CIP system efficiency metrics, such as biofilm removal. Scalability and modular design are critical considerations for CIP system selection in industries with evolving production needs. For instance, pharmaceutical manufacturing requires stringent contamination control measures, while food processing demands high-volume cleaning capabilities. CIP system qualification and FDA compliance are essential for businesses seeking to enter regulated markets. Steam-in-place sterilization techniques offer an alternative to traditional CIP systems, providing an additional layer of sanitation and reducing water usage. CIP system lifecycle cost analysis is essential for businesses seeking to minimize operational expenses and maximize ROI. Remote monitoring and data analysis tools enable real-time CIP system troubleshooting and safety procedures adherence, reducing downtime and ensuring consistent production quality. Compared to traditional CIP systems, portable CIP systems offer increased flexibility and ease of use, making them an attractive option for businesses seeking to streamline their sanitation processes and maintain regulatory compliance. Portable CIP systems can be easily transported between production lines or facilities, reducing the need for extensive infrastructure investments and enabling businesses to adapt to changing production demands.

What are the Key Data Covered in this Portable Clean-in-Place Market Research and Growth Report?

-

What is the expected growth of the Portable Clean-in-Place Market between 2024 and 2028?

-

USD 4.44 billion, at a CAGR of 6.59%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Re-use and Single), Type (Double -tank systems, Single-tank systems, and Multi-tank systems), and Geography (Europe, APAC, North America, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, APAC, North America, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Cost-effective portable CIP systems compared to stationary CIP systems, Inability to fully automate portable CIP systems

-

-

Who are the major players in the Portable Clean-in-Place Market?

-

Albert Handtmann Holding GmbH and Co. KG, Alfa Laval AB, Azbil Corp., Bachiller, Bionet, Centec GmbH, Donaldson Co. Inc., Filamatic, GD Process Design, GEA Group AG, Goma Engineering Pvt. Ltd., Klockner and Co. SE, Krones AG, Millitec Food Systems Ltd., Packo Cooling BV, Sani-Matic Inc, SPX FLOW Inc., SYSBIOTECH GmbH, Tetra Laval SA, and Marchesini Group Spa

-

We can help! Our analysts can customize this portable clean-in-place market research report to meet your requirements.

RIA -

RIA -