Premenstrual Syndrome Market Size 2024-2028

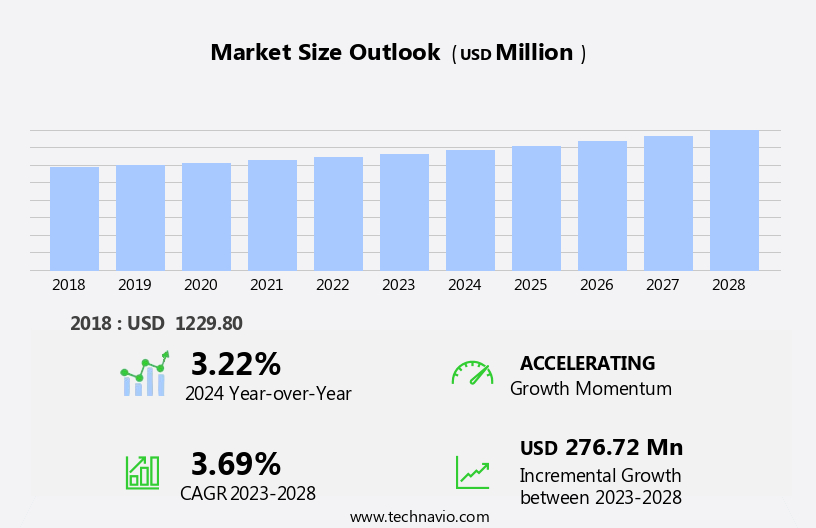

The premenstrual syndrome market size is forecast to increase by USD 276.72 million, at a CAGR of 3.69% between 2023 and 2028.

- The Premenstrual Syndrome (PMS) market is driven by increasing awareness and reporting about this condition, leading to a growing demand for effective treatments and management strategies. A significant trend shaping the market is the robust adoption of telemedicine, enabling remote diagnosis and consultation for women experiencing PMS symptoms. However, the diagnostic complexity surrounding PMS poses a notable challenge. With various symptoms and different severity levels, accurately diagnosing PMS remains a complex process, requiring extensive knowledge and expertise. This diagnostic challenge necessitates continuous research and development efforts to create more precise diagnostic tools and effective treatment options.

- Companies aiming to capitalize on market opportunities must focus on addressing this challenge through innovative solutions and collaborations with healthcare professionals. By doing so, they can effectively meet the needs of women seeking relief from PMS symptoms while ensuring accurate diagnoses and optimal treatment outcomes.

What will be the Size of the Premenstrual Syndrome Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The premenstrual syndrome (PMS) market continues to evolve, with various sectors integrating innovative solutions to address the diverse needs of individuals experiencing menstrual cycle-related symptoms. Birth control methods, treatment protocols, and hormonal therapies are among the traditional approaches, while mood swings and menstrual cycle tracking have gained traction through digital health solutions such as mobile health apps and period tracking apps. Support groups and patient education initiatives provide essential resources for individuals seeking understanding and coping strategies. Clinical trials and herbal supplements offer alternative treatment options, with a growing emphasis on natural remedies and lifestyle modifications.

Healthcare providers and machine learning algorithms are collaborating to enhance patient care and personalized medicine through predictive modeling and data analytics. Hormonal imbalances and stress management are critical areas of focus, with prescription medications, over-the-counter medications, and lifestyle changes being employed to alleviate symptoms. Environmental factors, breast tenderness, and pain management are also addressed through various interventions. Fertility awareness, ovulation prediction, and genetic testing are emerging trends, with a goal to improve health literacy and awareness campaigns. Digital health, wearable technology, and dietary changes are shaping the future of PMS management, as healthcare providers and patients explore the potential of precision medicine and diagnostic tools.

The continuous dynamism of the PMS market is driven by ongoing research, technological advancements, and evolving societal needs. The integration of artificial intelligence (AI) and machine learning in healthcare is expected to further revolutionize the landscape, offering personalized and data-driven solutions to individuals seeking relief from PMS symptoms.

How is this Premenstrual Syndrome Industry segmented?

The premenstrual syndrome industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Drug Class

- Analgesics

- Oral contraceptives & ovarian suppression agents

- Antidepressants

- Others

- Distribution Channel

- Retail pharmacies

- Hospital pharmacies

- Online pharmacies

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

.

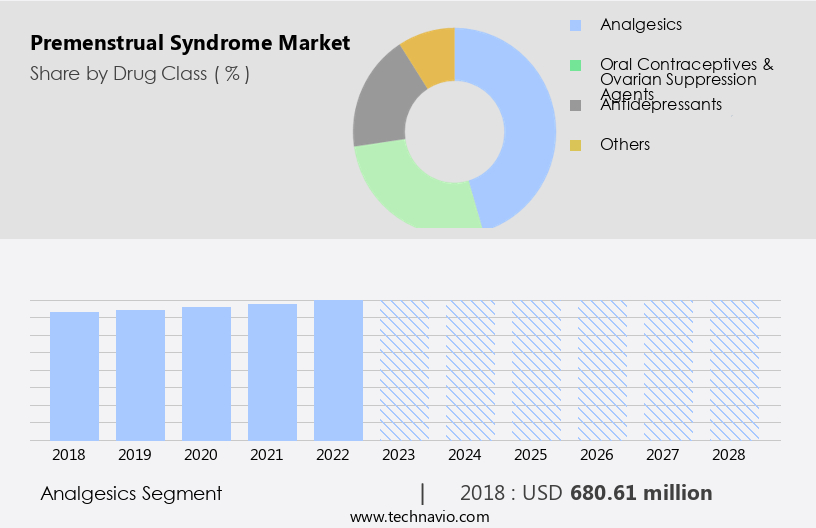

By Drug Class Insights

The analgesics segment is estimated to witness significant growth during the forecast period.

The market for menstrual health solutions encompasses various interventions, including birth control, treatment protocols, and pain management options. Birth control methods, such as hormonal contraceptives, help regulate menstrual cycles and alleviate premenstrual symptoms, including mood swings and menstrual cramps. Treatment protocols extend beyond pharmaceutical interventions, encompassing lifestyle modifications, herbal supplements, and natural remedies. Menstrual cycle tracking apps and wearable technology enable women to monitor their menstrual cycles, predict ovulation, and identify patterns in their symptoms. Support groups and patient education initiatives provide essential resources for managing menstrual health and addressing the stigma surrounding menstruation. Healthcare providers play a crucial role in diagnosing and treating hormonal imbalances and other underlying conditions contributing to menstrual symptoms.

Clinical trials and research advancements in areas like artificial intelligence, machine learning, and genetic testing contribute to a better understanding of menstrual health and the development of personalized treatment plans. Prescription medications, such as NSAIDs and acetaminophen, offer pain relief for menstrual cramps and other symptoms. Over-the-counter medications and dietary changes can also help manage symptoms. Stress management techniques, hormone therapy, and fertility awareness methods are additional approaches to managing menstrual health. The digital health landscape includes period tracking apps, symptom monitoring tools, and telehealth services, all contributing to increased health literacy and awareness. Health disparities and access to care remain significant challenges in the menstrual health market.

In summary, the menstrual health market is characterized by a diverse range of solutions, from pharmaceutical interventions to lifestyle modifications, digital health tools, and patient education initiatives. Continued research and innovation are essential to addressing the unique needs of women and improving access to effective, personalized care.

The Analgesics segment was valued at USD 680.61 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

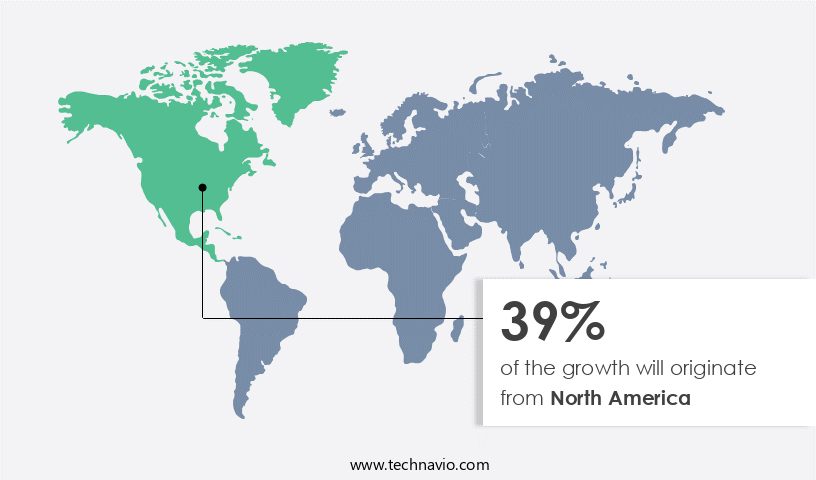

North America is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The Premenstrual Syndrome (PMS) market in North America has witnessed consistent growth due to several factors. The aging population, increasing prevalence of chronic diseases, and technological advancements are driving market expansion. The US, with its robust healthcare system, extensive medical device manufacturing capabilities, and large patient population, holds the largest share of the North American market. Health awareness is a significant cultural norm in North America, leading individuals to actively seek solutions for health-related issues. PMS, once perceived as a natural part of the menstrual cycle, is increasingly recognized as a medical condition. This shift in perception has resulted in increased attention and resources being directed towards researching and developing treatments.

Technological innovations, such as artificial intelligence (AI) and machine learning, are revolutionizing PMS management. Mobile health apps and period tracking apps enable users to monitor their menstrual cycles and identify patterns in their symptoms. These tools facilitate personalized treatment protocols and improve symptom management. Hormonal imbalances, a common cause of PMS, are being addressed through hormone therapy, herbal supplements, and natural remedies. Stress management techniques, including lifestyle modifications and dietary changes, are also gaining popularity. Healthcare providers are increasingly offering support groups and clinical trials to provide patients with comprehensive care. Prescription medications and over-the-counter medications are used to alleviate symptoms, while diagnostic tools and genetic testing help identify underlying causes.

Environmental factors and lifestyle choices contribute to PMS. Wearable technology and digital health solutions are being used to monitor and manage these factors. Precision medicine and data analytics are enabling personalized treatment plans, while predictive modeling and awareness campaigns improve health literacy. Health disparities are being addressed through targeted interventions and patient education. In conclusion, the PMS market in North America is experiencing steady growth, driven by increasing awareness, technological advancements, and a strong culture of health. The market encompasses a range of treatments, from hormone therapy and prescription medications to herbal supplements and lifestyle modifications. The integration of AI, machine learning, and digital health solutions is revolutionizing PMS management and improving patient outcomes.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Premenstrual Syndrome Industry?

- The heightened awareness and prevalent reporting on Premenstrual Syndrome (PMS) significantly contribute to the market's growth.

- The global market for Premenstrual Syndrome (PMS) solutions is experiencing significant growth due to increased awareness and education about the condition. More individuals are recognizing and reporting their symptoms to healthcare providers, leading to a greater understanding of PMS and its impact on women's health. Healthcare professionals, advocacy groups, and educational campaigns are actively disseminating accurate information about PMS symptoms, causes, and management strategies. As a result, there is a growing emphasis on personalized approaches to PMS management, including precision medicine, data analytics, and diagnostic tools. Over-the-counter medications for pain management and symptom monitoring are in high demand.

- The focus on improving menstrual health and reducing health disparities associated with PMS is driving innovation in the development of new treatments and interventions. In conclusion, the growing awareness and acceptance of PMS as a legitimate health concern are fueling the growth of the global PMS market. The emphasis on personalized medicine, data analytics, and diagnostic tools is expected to continue driving innovation in the development of effective PMS solutions during the forecast period.

What are the market trends shaping the Premenstrual Syndrome Industry?

- Telemedicine, characterized by its robust adoption, is currently a significant market trend. This progressive shift towards virtual healthcare services signifies a transformative approach in delivering efficient and accessible medical care.

- Premenstrual Syndrome (PMS) affects millions of women, characterized by mood swings, menstrual cycle irregularities, and hormonal imbalances. Treatment protocols for PMS include birth control, hormone therapy, stress management, and menstrual cycle tracking. With the advancement of technology, mobile health apps and period tracking apps have emerged as effective tools for managing PMS symptoms. These digital solutions offer convenience, enabling women to monitor their menstrual cycles and identify patterns in their symptoms. Telemedicine plays a pivotal role in expanding the reach of PMS treatment. By removing geographical barriers, telemedicine allows individuals in remote or underserved areas to access healthcare professionals specializing in PMS treatment.

- Virtual consultations via telemedicine platforms offer privacy and comfort, making it easier for individuals to discuss sensitive topics related to menstrual health and PMS symptoms. Furthermore, telemedicine offers flexibility, enabling women to seek advice and treatment without the need for in-person visits, which is particularly beneficial for those facing time constraints or mobility issues. Support groups provide a platform for women to connect with each other, share experiences, and offer emotional support. These communities offer a safe space for women to discuss their symptoms and learn coping strategies from others who have gone through similar experiences.

- By fostering a sense of community, support groups help reduce the stigma surrounding PMS and encourage women to seek appropriate treatment. In conclusion, the PMS market is driven by the increasing awareness of menstrual health and the availability of innovative treatment options. Telemedicine, mobile health apps, and period tracking apps are transforming the way women manage their symptoms, while support groups offer emotional support and a sense of community. As research continues to uncover new insights into the causes and treatments of PMS, we can expect to see further advancements in this field.

What challenges does the Premenstrual Syndrome Industry face during its growth?

- The diagnostic complexity associated with Product Management Systems (PMS) poses a significant challenge to the industry's growth. This intricacy, which is a fundamental aspect of implementing and utilizing PMS, necessitates a high level of expertise and resources to effectively address it. Consequently, overcoming this challenge is essential for companies aiming to maximize the potential benefits of these systems and foster industry expansion.

- Premenstrual Syndrome (PMS) is a complex condition characterized by a wide range of physical, emotional, and behavioral symptoms that can impact women's daily lives. The variability and subjective nature of these symptoms make diagnosing PMS a challenge for healthcare providers. No definitive laboratory tests or specific diagnostic criteria exist for PMS, and diagnosis relies on assessing a woman's reported symptoms, their timing in relation to her menstrual cycle, and their impact on her functioning. Several factors, including lifestyle and environmental, are believed to contribute to the development of PMS. Lifestyle factors such as stress, lack of sleep, and poor nutrition can exacerbate symptoms.

- Environmental factors, including pollution and toxins, may also play a role. Patients often seek relief through various treatments, including prescription medications, herbal supplements, and natural remedies. Clinical trials and research continue to explore the effectiveness of these treatments. In recent years, there has been growing interest in the use of artificial intelligence (AI) and machine learning to help diagnose and manage PMS. These technologies have the potential to improve patient education and personalize treatment plans based on individual symptoms and responses. Healthcare providers play a crucial role in helping women understand PMS, its causes, and available treatment options.

- By staying informed about the latest research and advancements in PMS management, providers can better support their patients and help them manage their symptoms effectively.

Exclusive Customer Landscape

The premenstrual syndrome market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the premenstrual syndrome market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, premenstrual syndrome market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - The company specializes in providing pharmaceutical solutions for premenopausal women experiencing heavy menstrual bleeding due to fibroids.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Aspen Pharmacare Holdings Ltd

- Bayer AG

- Bristol Myers Squibb Co.

- Eli Lilly and Co.

- GlaxoSmithKline Plc

- Herbalife International of America Inc.

- Hikma Pharmaceuticals Plc

- Johnson and Johnson

- Lupin Ltd.

- Merck KGaA

- Novartis AG

- Octavius Pharma Pvt. Ltd.

- Otsuka Pharmaceutical Co. Ltd.

- Pfizer Inc.

- Recordati S.p.A

- Sanofi SA

- Sun Pharmaceutical Industries Ltd.

- Teva Pharmaceutical Industries Ltd.

- Viatris Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Premenstrual Syndrome Market

- In March 2024, Pfizer Inc. Announced the launch of their novel oral therapy, Loryna, designed specifically for the treatment of premenstrual dysphoric disorder (PMDD), a severe form of premenstrual syndrome (PMS). This approval by the U.S. Food and Drug Administration (FDA) marked a significant milestone in addressing the unmet medical needs of women suffering from PMDD (FDA, 2024).

- In July 2024, Merck KGaA, Darmstadt, Germany, and FibriDiag GmbH entered into a strategic partnership to develop and commercialize a non-invasive diagnostic test for PMS. This collaboration aimed to improve the diagnosis and treatment of PMS, which often goes undiagnosed or misdiagnosed due to the lack of objective diagnostic tools (Merck KGaA, 2024).

- In October 2025, Myovant Sciences, a biopharmaceutical company, completed a successful Series C financing round, raising USD200 million. The proceeds from this financing would be used to fund the development and commercialization of its investigational oral therapy, relugolix, for the treatment of heavy menstrual bleeding associated with PMS (Myovant Sciences, 2025).

- In December 2025, the European Commission granted marketing authorization to Novo Nordisk for its new hormonal contraceptive, Sayana Press, for the prevention and treatment of PMS symptoms. This approval marked the first subcutaneous injection hormonal contraceptive available in Europe for the management of PMS symptoms (Novo Nordisk, 2025).

Research Analyst Overview

- The premenstrual syndrome (PMS) market encompasses various interventions aimed at managing symptoms associated with hormonal fluctuations during the menstrual cycle phases. Stress reduction techniques and holistic approaches, such as yoga and meditation, have gained popularity as effective methods for alleviating PMS symptoms. Hormonal contraceptives and surgical sterilization are common contraceptive methods used to regulate menstrual cycles and reduce PMS symptoms. Public health initiatives and health policy prioritize the development of contraceptive methods, ovulation tracking methods, and symptom management strategies. Estrogen and progesterone levels play a significant role in PMS symptoms. Hormonal fluctuations during the menstrual cycle can lead to mood swings, bloating, and pain.

- Lifestyle interventions, including nutrition counseling and symptom tracking logs, can help manage these symptoms. Alternative therapies, such as acupuncture and herbal remedies, are also gaining traction in the market. Symptom tracking logs, pain relief methods, and anti-anxiety medications are commonly used to manage PMS symptoms. Cervical mucus monitoring and barrier methods are effective contraceptive options for those seeking to avoid hormonal methods. Patient advocacy groups and support networks offer valuable resources for individuals dealing with PMS, providing education and community connections. The market for PMS management is diverse and dynamic, with ongoing research and innovation in hormonal fluctuations, contraceptive methods, and symptom management strategies.

- The integration of technology, such as period calendars and mobile apps, has further expanded the range of options available to consumers. Overall, the market prioritizes individualized approaches to PMS management, recognizing the unique experiences and needs of each woman.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Premenstrual Syndrome Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

158 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.69% |

|

Market growth 2024-2028 |

USD 276.72 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.22 |

|

Key countries |

US, Germany, UK, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Premenstrual Syndrome Market Research and Growth Report?

- CAGR of the Premenstrual Syndrome industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, Asia, and Rest of World (ROW)

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the premenstrual syndrome market growth of industry companies

We can help! Our analysts can customize this premenstrual syndrome market research report to meet your requirements.

RIA -

RIA -