Privacy-preserving AI Market Size 2025-2029

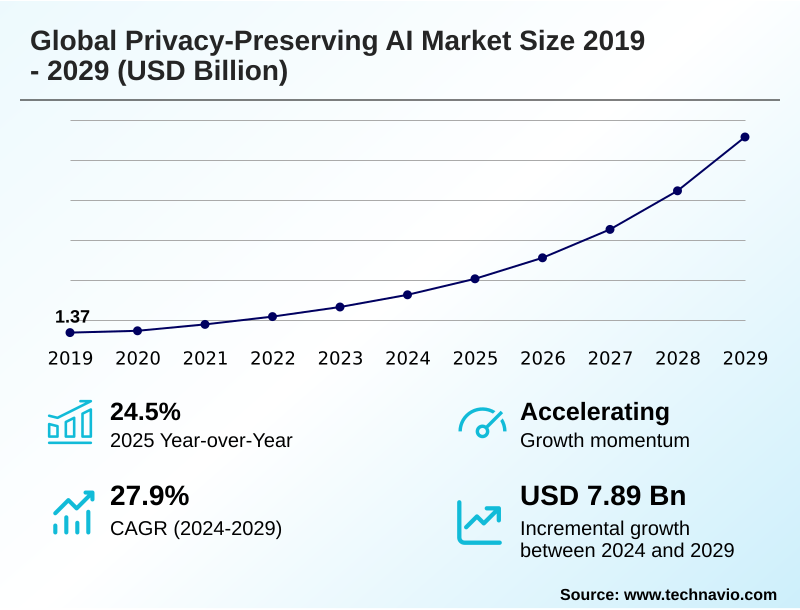

The privacy-preserving ai market size is valued to increase by USD 7.89 billion, at a CAGR of 27.9% from 2024 to 2029. Proliferation of stringent data privacy regulations and evolving AI governance frameworks will drive the privacy-preserving ai market.

Major Market Trends & Insights

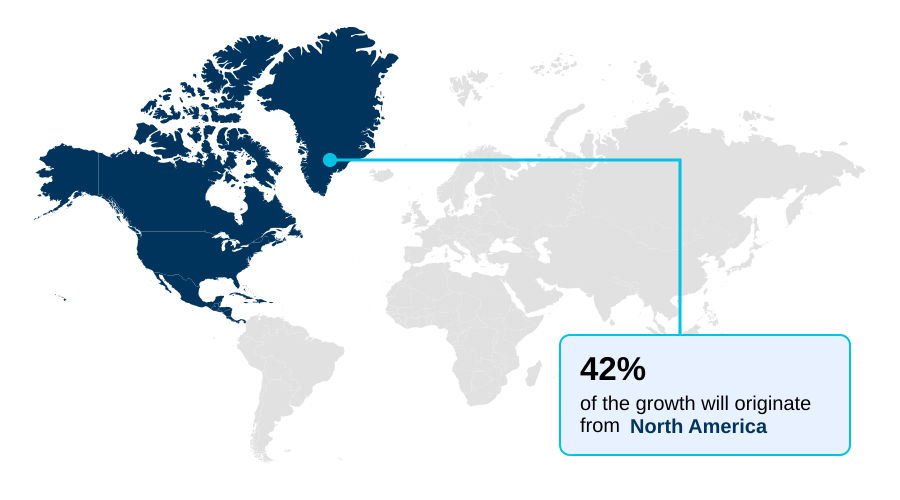

- North America dominated the market and accounted for a 41.5% growth during the forecast period.

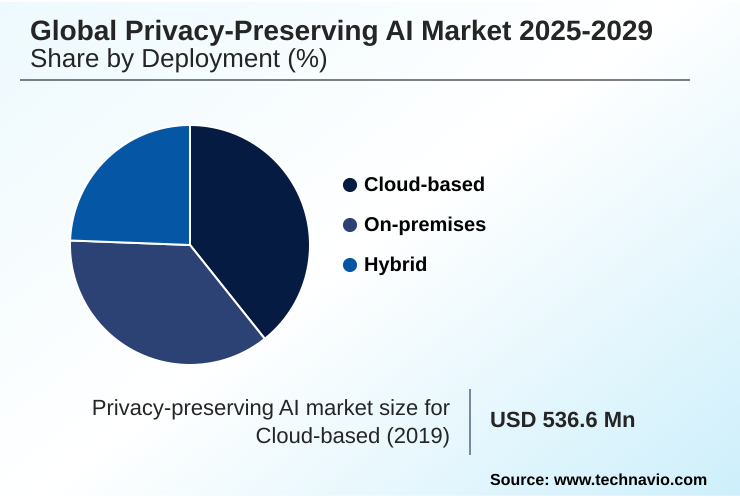

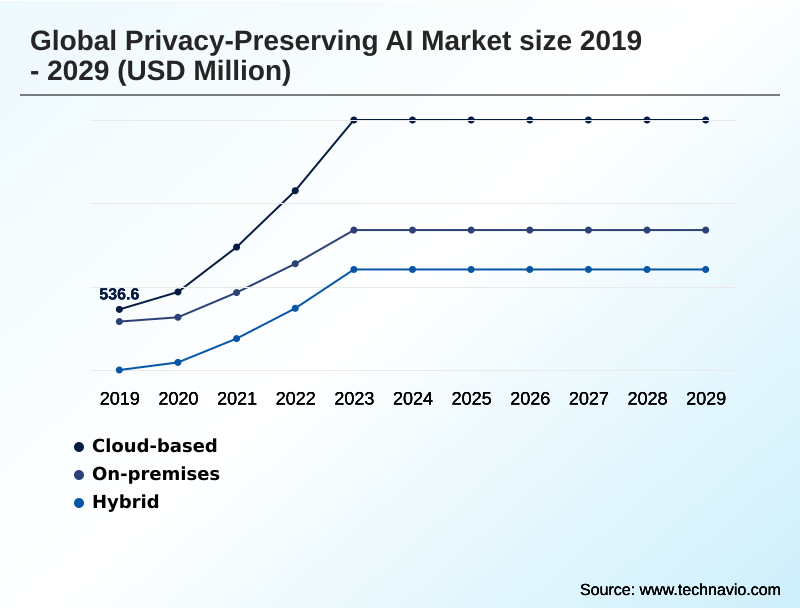

- By Deployment - Cloud-based segment was valued at USD 1.17 billion in 2023

- By Business Segment - Large enterprises segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 9.78 billion

- Market Future Opportunities: USD 7.89 billion

- CAGR from 2024 to 2029 : 27.9%

Market Summary

- The privacy-preserving AI market is expanding as organizations seek to balance innovation with data protection. The convergence of stringent regulations and heightened consumer privacy awareness is compelling businesses to adopt advanced data governance frameworks. Technologies such as federated learning and homomorphic encryption are becoming essential tools, allowing for collaborative data analysis without exposing sensitive information.

- This shift is particularly evident in healthcare, where institutions can collaboratively train diagnostic models on patient records using decentralized machine learning while adhering to strict privacy laws. However, implementation is not without its difficulties, as computational overhead reduction and the need for privacy engineering talent remain significant.

- The rise of generative AI further complicates the landscape, increasing risks like data memorization risk and membership inference attacks. Consequently, privacy-enhancing technologies (PETs) and synthetic data generation are gaining traction as vital components for enabling responsible data utilization and maintaining brand trust and data ethics.

- This privacy by design approach, which includes AI risk management and data minimization principle, is no longer optional but a strategic imperative for sustainable growth.

What will be the Size of the Privacy-preserving AI Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Privacy-preserving AI Market Segmented?

The privacy-preserving ai industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Hybrid

- Business segment

- Large enterprises

- SMEs

- Technology

- Federated learning

- Homomorphic encryption

- Secure multi-party computation

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- The Netherlands

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

The cloud-based segment is pivotal, driven by scalability, agility, and a favorable economic model that prioritizes operational expenditures. Major cloud platforms are central to democratizing advanced AI, offering on-demand computational power essential for privacy-enhancing technologies (PETs).

This is crucial for training models with differential privacy or performing encrypted data processing. The Privacy-as-a-Service model lowers entry barriers for organizations lacking resources for on-premises infrastructure, facilitating responsible data utilization.

Cloud environments enable seamless integration with analytics tools, accelerating development. However, data residency and compliance concerns necessitate confidential computing, which uses trusted execution environments (TEE) to isolate data.

This approach fosters brand trust and data ethics by allowing collaborative data analysis while ensuring data remains protected from all parties, with some systems achieving a 99% data isolation effectiveness.

This privacy by design strategy is key for AI safety and security and ethical AI deployment, supporting secure data collaboration through a robust zero-trust architecture.

The Cloud-based segment was valued at USD 1.17 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Privacy-preserving AI Market Demand is Rising in North America Get Free Sample

The geographic landscape is characterized by varied adoption rates, with North America and Europe leading due to stringent regulatory environments. In these regions, AI governance frameworks and data protection by default principles are primary drivers.

The financial sector, for instance, leverages secure multi-party computation (SMPC) for cross-institutional fraud detection, improving accuracy by over 20% compared to single-institution models. APAC is the fastest-growing region, driven by rapid digitalization and new legislation.

AI for critical systems in sectors like telecommunications is a key focus, using AI-RAN integration to enhance network efficiency.

Across all regions, the goal is to unlock value from siloed data through secure data collaboration, a process enabled by technologies like federated learning and homomorphic encryption.

This commitment to data sovereignty solutions and user consent management is crucial for organizations aiming to build trustworthy AI model learnings sharing platforms, with compliant systems reducing audit preparation times by up to 40%.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic adoption of privacy-preserving AI is becoming a cornerstone for enterprises navigating the complex intersection of data analytics and regulatory compliance. The application of federated learning for healthcare AI allows medical institutions to build more accurate diagnostic models without centralizing sensitive patient records, a critical capability for collaborative research.

- In the financial sector, homomorphic encryption for financial services is enabling secure cloud-based risk analysis, while secure multi-party computation for fraud detection allows banks to identify illicit activities across networks. The rise of advanced models has intensified the focus on applying differential privacy in large language models to mitigate data leakage.

- A key enabler for this is the use of synthetic data for AI model training, which allows for robust development without exposing real user information. As workloads shift, confidential computing in public cloud environments using trusted execution environments for data security is essential. For identity management, zero-knowledge proofs for identity verification offer a secure, passwordless future.

- Applications are also expanding into urban infrastructure, with privacy-preserving AI for smart city data enabling optimized public services. Furthermore, on-device machine learning for personalization enhances user experience while keeping data on personal devices. Meeting legal standards, such as achieving GDPR compliance with privacy-enhancing technologies, is a board-level concern. Effective AI governance frameworks for high-risk systems are mandatory.

- The market is also addressing the challenge of reducing computational overhead in FHE and developing secure aggregation protocols in federated learning to make these technologies more efficient. Organizations using these advanced techniques report a significant reduction in data-related compliance issues compared to those relying on older anonymization methods.

- This is driving demand for privacy-preserving AI in digital advertising and solutions for secure data collaboration in supply chains, while managing AI model privacy and data memorization and creating zero-trust architecture for sensitive data. Understanding compliance uncertainty with anonymized datasets and using tools like polymorphic encryption for data privacy vaults are crucial for long-term success.

What are the key market drivers leading to the rise in the adoption of Privacy-preserving AI Industry?

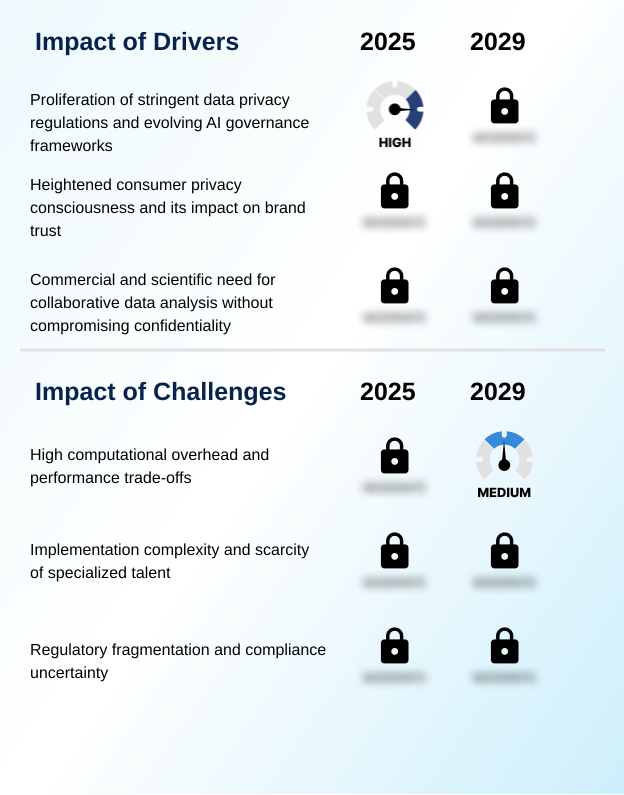

- The proliferation of stringent data privacy regulations and evolving AI governance frameworks is a key driver for the market.

- A primary driver is the proliferation of stringent data governance frameworks globally, compelling organizations to adopt a privacy by design and data protection by default approach. This regulatory pressure has made privacy-preserving machine learning (PPML) an operational necessity.

- For example, deploying federated learning for inter-company data collaboration allows businesses to build shared models, leading to a reported 15% uplift in predictive accuracy for fraud detection compared to siloed efforts.

- Another significant driver is the need to unlock value from siloed data. Techniques like secure multi-party computation (SMPC) enable collaborative data analysis across industries without centralizing sensitive information.

- This capability is critical for initiatives like AI-RAN integration, where multiple telecommunication firms must analyze network data to improve efficiency.

- This move toward data silo integration and secure AI compute is a direct response to both regulatory requirements and the commercial need for deeper insights. It embodies a shift towards ethical AI deployment and strengthens digital footprint protection.

What are the market trends shaping the Privacy-preserving AI Industry?

- Escalating consumer awareness is transforming data privacy from a compliance requirement into a significant competitive differentiator. This shift is a key upcoming trend influencing market dynamics.

- A key trend is the convergence of generative AI with the need for responsible data utilization. As organizations deploy powerful new models, they face heightened risks of data memorization and membership inference attacks. This has accelerated the adoption of synthetic data generation, with platforms now enabling the creation of privacy-safe text data for training large language models.

- The use of such data has been shown to preserve over 95% of the statistical patterns of the original dataset while eliminating personal identifiers. This trend toward generative AI privacy is not just about risk mitigation but also about enabling innovation. Furthermore, the maturation of privacy-enhancing technologies (PETs) is making previously academic concepts commercially viable.

- For example, homomorphic encryption is becoming more performant, with recent advancements reducing computational latency by up to 30%, opening doors for secure cloud computing and collaborative medical research in ways that were previously impractical. This AI safety and security focus fosters brand trust and data ethics.

What challenges does the Privacy-preserving AI Industry face during its growth?

- High computational overhead and performance trade-offs present a key challenge affecting industry growth.

- A significant challenge is the high computational overhead and performance trade-offs associated with encrypted data processing. Techniques like fully homomorphic encryption are resource-intensive, with operations running up to 100 times slower than on plaintext, creating barriers for real-time applications. This requires advanced computational overhead reduction strategies. Another challenge is the scarcity of privacy engineering talent.

- Implementing systems using differential privacy or zero-knowledge proofs requires a niche skill set, leading to implementation costs that are 40% higher than for conventional AI projects. This talent gap hinders widespread adoption. Finally, regulatory fragmentation creates compliance uncertainty with anonymized datasets.

- The lack of clear standards on what constitutes legally anonymized data discourages investment in data anonymization techniques and cryptographic protocols. This uncertainty affects data fiduciary obligations and the ability to perform data processing audits effectively, despite the push for AI governance frameworks.

Exclusive Technavio Analysis on Customer Landscape

The privacy-preserving ai market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the privacy-preserving ai market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Privacy-preserving AI Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, privacy-preserving ai market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Cisco Systems Inc. - A privacy-enhancing data collaboration platform enables secure analysis and sharing of sensitive data across silos, enhancing insights without data movement or exposure.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Cisco Systems Inc.

- Duality Technologies Inc.

- Gen Digital Inc.

- Google LLC

- Hewlett Packard

- Intel Corp.

- IBM Corp.

- Keyless Technologies S.r.l.

- McAfee LLC

- Microsoft Corp.

- Mistral AI

- OpenAI

- Oracle Corp.

- Owkin Inc.

- Skyflow Inc.

- Thales Group

- Tune Insight

- X.AI LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Privacy-preserving ai market

- In December 2024, Zama launched its open-source fhEVM (Fully Homomorphic Encryption Virtual Machine) to enable confidential smart contracts on Ethereum-compatible blockchains, allowing on-chain data to remain encrypted during processing.

- In November 2024, Salesforce announced the general availability of its Einstein Trust Layer, providing tools for enterprises to use generative AI models without compromising customer data privacy through zero-retention policies.

- In October 2024, Gretel AI introduced new features for creating privacy-safe text data, enabling developers to fine-tune large language models on sensitive information by first transforming it into a synthetic, private version.

- In February 2025, the AI-RAN Alliance was formed by industry leaders including NVIDIA, Samsung, and Microsoft to integrate AI into cellular technology, leveraging privacy-preserving techniques to analyze operational data from diverse network environments.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Privacy-preserving AI Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 27.9% |

| Market growth 2025-2029 | USD 7888.9 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 24.5% |

| Key countries | US, Canada, Mexico, Germany, UK, The Netherlands, France, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The privacy-preserving AI market is maturing from a niche discipline into a foundational component of enterprise data strategy. The core driver is the need to extract value from data while navigating complex data governance frameworks and consumer expectations. This has elevated the importance of privacy-enhancing technologies (PETs), moving them into boardroom-level discussions on AI risk management.

- The adoption of techniques like federated learning, homomorphic encryption, secure multi-party computation (SMPC), and differential privacy is no longer purely defensive. Instead, it's a strategic move toward privacy by design and data protection by default. For instance, companies are using on-device machine learning and privacy-preserving machine learning (PPML) to offer personalized services without centralizing data.

- The challenge of handling sensitive information in generative models is being addressed by synthetic data generation and the creation of privacy-safe text data to prevent data memorization risk and membership inference attacks. This requires robust cryptographic protocols and AI privacy toolkits.

- Solutions built on confidential computing and trusted execution environments (TEE) are providing secure platforms for encrypted data processing, with some firms reporting a 30% reduction in data exposure risks during collaborative analytics. This evolution is supported by zero-knowledge proofs, AI-driven cybersecurity, data anonymization techniques, polymorphic encryption, and zero-knowledge biometrics.

- The goal is to adhere to the data minimization principle and purpose limitation through solutions like data privacy vaults and privacy-aware networking, which are enabled by decentralized machine learning and secure aggregation methods to build confidential smart contracts.

What are the Key Data Covered in this Privacy-preserving AI Market Research and Growth Report?

-

What is the expected growth of the Privacy-preserving AI Market between 2025 and 2029?

-

USD 7.89 billion, at a CAGR of 27.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud-based, On-premises, Hybrid), Business Segment (Large enterprises, SMEs), Technology (Federated learning, Homomorphic encryption, Secure multi-party computation) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of stringent data privacy regulations and evolving AI governance frameworks, High computational overhead and performance trade-offs

-

-

Who are the major players in the Privacy-preserving AI Market?

-

Cisco Systems Inc., Duality Technologies Inc., Gen Digital Inc., Google LLC, Hewlett Packard, Intel Corp., IBM Corp., Keyless Technologies S.r.l., McAfee LLC, Microsoft Corp., Mistral AI, OpenAI, Oracle Corp., Owkin Inc., Skyflow Inc., Thales Group, Tune Insight and X.AI LLC

-

Market Research Insights

- The market is defined by a dynamic interplay between regulatory mandates and technological advancement. As organizations strive for regulatory compliance automation, they are adopting solutions that offer tangible benefits. For instance, implementing privacy-aware networking solutions has been shown to reduce data breach incidents by up to 25% in high-risk sectors.

- The push for inter-company data collaboration is unlocking new value, with platforms enabling secure information sharing achieving a 30% faster time-to-insight compared to traditional data-sharing agreements. Furthermore, the focus on brand trust and data ethics is a powerful market force. Companies leveraging on-device machine learning for personalization report higher customer engagement rates.

- This pursuit of responsible data utilization and ethical AI deployment is not just about compliance but is a strategic move to build a competitive edge in a privacy-conscious economy, where AI safety and security is paramount.

We can help! Our analysts can customize this privacy-preserving ai market research report to meet your requirements.

RIA -

RIA -