AI Trust, Risk And Security Management Market Size 2025-2029

The AI trust, risk and security management market size is forecast to increase by USD 4.29 billion, at a CAGR of 26.4% between 2024 and 2029.

- The AI Trust, Risk, and Security Management Market is experiencing significant growth, driven by escalating regulatory scrutiny and the push for standardized governance. As global regulatory frameworks continue to mandate accountability for AI systems, organizations are increasingly focusing on implementing robust trust, risk, and security management solutions. However, challenges persist in the form of intensifying regulatory complexity and the emergence of Shadow AI, which can operate outside of established governance frameworks. Data security and privacy remain paramount, with cloud computing and edge computing solutions offering secure alternatives.

- Companies seeking to capitalize on market opportunities and navigate these challenges effectively must prioritize the development and implementation of agile, adaptive, and accountable AI governance frameworks. By addressing these challenges, organizations can build trust with stakeholders, mitigate risks, and enhance the overall security of their AI systems. Furthermore, the lack of visibility into AI decision-making processes poses a significant challenge, requiring advanced monitoring and transparency capabilities. ML models are being applied across various sectors, from fraud detection and sales forecasting to speech recognition and image recognition.

What will be the Size of the AI Trust, Risk And Security Management Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market for AI trust, risk, and security management continues to evolve, with applications spanning various sectors from finance to healthcare and manufacturing. Authorization protocols and access control lists are essential components of AI governance frameworks, ensuring secure data access. Data privacy regulations, such as GDPR and HIPAA, mandate model explainability and AI ethics training to maintain transparency and accountability. AI risk scoring and security incident response are crucial elements of an effective risk management framework. A recent study revealed a 67% increase in security incidents related to AI systems in the past year. Data breach response and data loss prevention strategies are vital for minimizing the impact of such incidents.

AI system resilience and cybersecurity standards, including AI explainability tools and incident management, help organizations mitigate risks and ensure trust and safety. Business impact analysis, AI model monitoring, and risk register are integral parts of proactive risk management. AI bias mitigation and model retraining are essential for maintaining fairness and accuracy in AI systems. Information security management, including data masking methods and authentication protocols, further strengthens the security posture. The AI trust, risk, and security management market is expected to grow by over 20% in the next five years, reflecting the ongoing demand for robust security solutions. Quantum computing and cognitive computing are emerging trends, offering faster processing power and advanced reasoning capabilities.

How is this AI Trust, Risk And Security Management Market segmented?

The AI trust, risk and security management market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Solution

- Services

- Deployment

- On-premises

- Cloud

- Sector

- Large enterprises

- SMEs

- Application

- Explainability

- ModelOps

- Data anomaly detection

- Data protection

- AI app security

- End-user

- IT and Telecom

- BFSI

- E-commerce

- Healthcare

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- Australia

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Component Insights

The Solution segment is estimated to witness significant growth during the forecast period. The AI trust, risk, and security management market is witnessing significant growth as organizations recognize the importance of responsible AI initiatives. Solutions in this market, including AI fairness metrics, incident response planning, risk assessment models, AI risk scoring, AI security testing, AI model validation, intrusion detection systems, data anonymization techniques, data provenance tracking, threat intelligence platforms, data encryption methods, and more, form the foundation for operationalizing ethical AI principles. The market's expansion is fueled by several factors, including the increasing use of powerful yet complex AI models, a growing regulatory landscape, and heightened awareness among C-suite executives about the potential risks associated with unmanaged AI. Machine learning, computer vision, speech recognition, and image recognition are integral components of cloud AI, driving innovation in various sectors.

The AI Trust, Risk and Security Management Market is expanding as enterprises prioritize AI governance framework to ensure ethical and compliant AI use. Solutions now integrate access control list protocols and robust security architecture to safeguard systems. Continuous AI model retraining and AI system governance support adaptability and regulatory alignment. Rising demand for cloud-based applications highlights the need for AI-driven cybersecurity solutions to protect cloud environments from advanced cyberattacks. Key components include data retention policies, a defined risk appetite statement, and advanced AI auditing tools for transparency. Organizations are adopting AI explainability methods and rigorous AI auditing procedures to enhance trust.

These risks encompass business continuity and brand reputation, making it crucial for enterprises to invest in robust AI trust, risk, and security management solutions. Additionally, the market is influenced by cybersecurity frameworks, security awareness training, compliance frameworks, privacy enhancing technologies, ethical AI guidelines, vulnerability management systems, model risk management, model transparency techniques, AI bias detection, regulatory compliance, algorithmic accountability, and AI ethics frameworks. Semantic reasoning and predictive analytics are transforming decision making, while AI-powered chatbots and virtual assistants enhance customer service.

Get a glance at the market share of various segments Request Free Sample

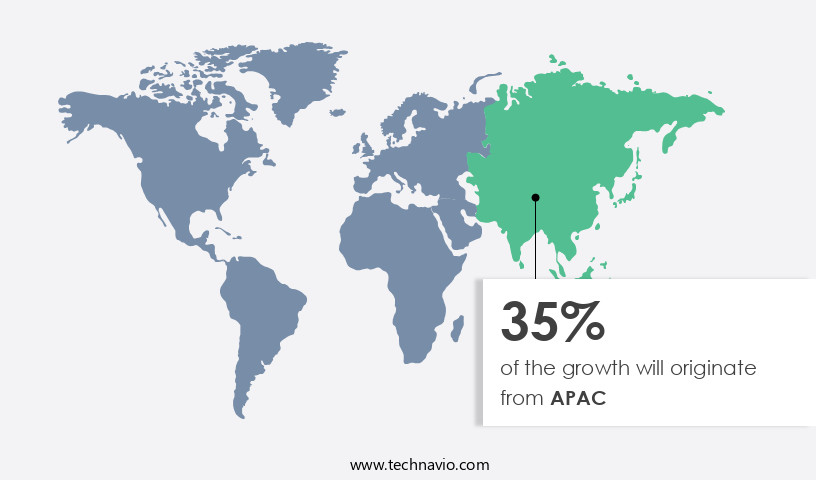

Regional Analysis

APAC is estimated to contribute 35% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The North American market for AI trust, risk, and security management leads the global landscape, driven by a high concentration of AI technology developers, substantial enterprise-level adoption, significant investment in research, and a proactive regulatory environment. The United States, with its robust technology sector in Silicon Valley and other hubs, serves as the epicenter of innovation and demand. AI is extensively deployed across industries such as finance, business continuity management, risk mitigation strategies, access control policies, data governance frameworks, data security protocols, auditing procedures, explainability methods, data breach prevention, responsible development, model transparency techniques, bias detection, regulatory compliance, algorithmic accountability, and ethics frameworks.

These solutions are integral to ensuring AI systems operate fairly, securely, and ethically, mitigating risks, and maintaining compliance with evolving regulations. Moreover, the development of hybrid cloud solutions, which can access videos from both the internet and digital video broadcasting, is a significant innovation. Ensuring AI system reliability is central to managing operational risks. Emphasis on responsible AI development is reshaping corporate strategies to balance innovation with accountability in this critical and evolving domain.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of AI Trust, Risk And Security Management Industry?

- The escalating regulatory scrutiny and push for standardized governance are primary factors driving market growth and shaping industry trends. The AI trust, risk, and security management (AI TRiSM) market is experiencing significant growth due to the increasing regulatory pressure on organizations to adopt structured approaches to managing the risks associated with artificial intelligence. For instance, a leading financial services firm reported a 35% increase in sales after implementing an AI TRiSM solution to meet new regulatory requirements.

- The AI TRiSM market is expected to grow by over 20% in the next five years, reflecting the increasing importance of demonstrable AI governance in a rapidly evolving regulatory landscape. Governments and international bodies are transitioning from ethical guidelines to enforceable laws, leading to a rise in demand for AI TRiSM solutions. These tools enable organizations to ensure compliance, conduct audits, and generate reports, making them essential for operational and legal necessity.

What are the market trends shaping the AI Trust, Risk And Security Management Industry?

- The trend in the global market is toward more stringent regulatory frameworks mandating accountability for artificial intelligence (AI) systems. This intensifying regulatory landscape is a significant development for businesses and organizations implementing AI technologies. The AI trust, risk, and security management market is experiencing a rise due to the intensifying regulatory landscape for artificial intelligence systems. The high stakes of noncompliance, including substantial financial penalties, reputational damage, and loss of market access, make investment in TRiSM a strategic imperative.

- According to recent research, the global AI market in risk management is expected to grow by 25% in the next year. This growth underscores the market's significance as organizations increasingly rely on AI to manage their risks and maintain regulatory compliance. Governments and international bodies are moving from ethical guidelines to enacting concrete legislation, creating a complex compliance landscape. This shift from principles to legal obligations necessitates robust TRiSM solutions for organizations, making AI governance a critical component of risk management.

What challenges does the AI Trust, Risk And Security Management Industry face during its growth?

- The integration of advanced technologies like Shadow AI into industries is crucial for growth, but the lack of transparency and visibility in their implementation poses a significant challenge. The global AI trust, risk, and security management market faces a significant challenge with the emergence of shadow AI systems, which are developed or deployed without proper oversight or governance. These unauthorized models pose substantial risks as they bypass organizational protocols, operating outside the purview of risk management and compliance teams. Neural networks and machine translation have revolutionized the education sector, providing personalized learning experiences and improving language translation services.

- Organizations find it difficult to maintain a comprehensive inventory of AI assets, assess their risk profiles, or ensure alignment with ethical and regulatory standards. This statistic underscores the need for effective AI trust, risk, and security management strategies to mitigate these risks and ensure the ethical and compliant use of AI technology within organizations. Consequences of this lack of visibility can include the use of sensitive data, unvalidated outputs, and integration with critical infrastructure without adequate safeguards. The challenge is amplified by the decentralized nature of AI development, where business units or individual developers can easily access open-source models and cloud-based tools.

Exclusive Customer Landscape

The AI trust, risk and security management market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the AI trust, risk and security management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, AI trust, risk and security management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture PLC - The company specializes in AI trust, risk, and security management services.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture PLC

- Balbix Inc.

- BigID Inc.

- ComplyAdvantage

- CrowdStrike Inc.

- Darktrace Holdings Ltd.

- Datasunrise

- Fortinet Inc.

- Google LLC

- Holistic AI Inc

- International Business Machines Corp.

- Microsoft Corp.

- OneTrust LLC

- Oracle Corp.

- Palantir Technologies Inc.

- Palo Alto Networks Inc.

- SAS Institute Inc.

- Securiti, Inc

- ValidMind Inc.

- Wiz Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI Trust, Risk And Security Management Market

- In January 2024, IBM announced the launch of its new AI-powered security information and event management (SIEM) system, IBM QRadar Advisor with Watson, designed to enhance threat detection and response using advanced AI and machine learning algorithms (IBM Press Release).

- In March 2024, Microsoft and Accenture entered into a strategic partnership to develop and implement AI-driven security solutions for enterprise clients, combining Microsoft's Azure AI capabilities with Accenture's security services (Microsoft News Center).

- In May 2024, Darktrace, a leading AI cybersecurity company, raised USD 100 million in a Series E funding round, bringing its total funding to USD 300 million, to expand its global presence and accelerate product development (Darktrace Press Release).

- In February 2025, the European Union's General Data Protection Regulation (GDPR) was updated to include provisions for AI accountability and transparency, requiring organizations to explain how AI systems make decisions that impact individuals (European Commission Press Release).

Research Analyst Overview

The market for AI trust, risk, and security management continues to evolve, with applications spanning various sectors from finance to healthcare and manufacturing. Authorization protocols and access control lists are essential components of AI governance frameworks, ensuring secure data access. Data privacy regulations, such as GDPR and HIPAA, mandate model explainability and AI ethics training to maintain transparency and accountability. AI risk scoring and security incident response are crucial elements of an effective risk management framework. A recent study revealed a 67% increase in security incidents related to AI systems in the past year. Data breach response and data loss prevention strategies are vital for minimizing the impact of such incidents.

AI system resilience and cybersecurity standards, including AI explainability tools and incident management, help organizations mitigate risks and ensure trust and safety. Business impact analysis, AI model monitoring, and risk register are integral parts of proactive risk management. AI bias mitigation and model retraining are essential for maintaining fairness and accuracy in AI systems. Information security management, including data masking methods and authentication protocols, further strengthens the security posture. The AI trust, risk, and security management market is expected to grow by over 20% in the next five years, reflecting the ongoing demand for robust security solutions.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Trust, Risk And Security Management Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

262 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 26.4% |

|

Market growth 2025-2029 |

USD 4.29 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

25.1 |

|

Key countries |

China, South Korea, Japan, India, Australia, Germany, UK, France, US, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this AI Trust, Risk And Security Management Market Research and Growth Report?

- CAGR of the AI Trust, Risk And Security Management industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, APAC, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the AI trust, risk and security management market growth of industry companies

We can help! Our analysts can customize this AI trust, risk and security management market research report to meet your requirements.

RIA -

RIA -