Remote Weapon Systems Market Size 2025-2029

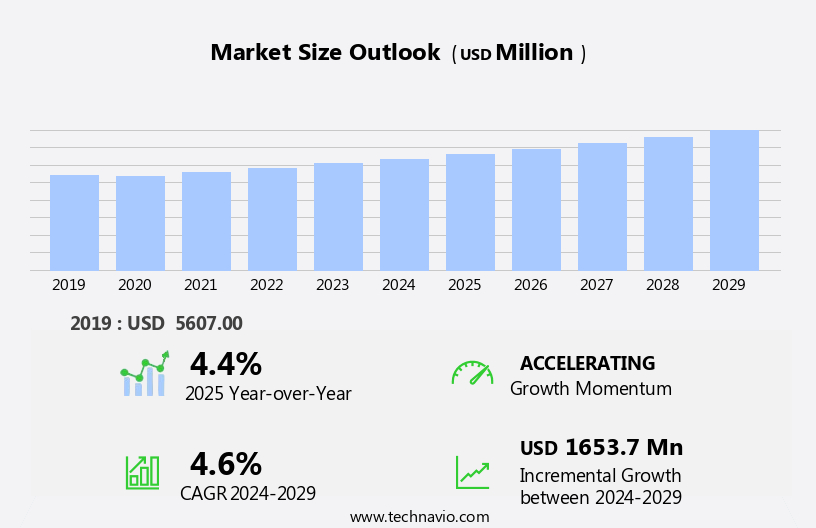

The remote weapon systems market size is forecast to increase by USD 1.65 billion, at a CAGR of 4.6% between 2024 and 2029.

- The market is experiencing significant growth, driven by escalating defense spending and the increasing deployment of these systems on unmanned platforms. This trend reflects the strategic importance of remote weapon systems in enhancing military capabilities and reducing risks to personnel. However, the market also faces challenges, most notably the complexities of supply chain management. As the production and integration of these advanced systems involve multiple components and companies, ensuring seamless supply and timely delivery can be a daunting task. Companies operating in this market must navigate these challenges effectively to capitalize on the opportunities presented by the growing demand for remote weapon systems.

- In doing so, they will need to establish robust supply chain management systems, build strong relationships with key suppliers, and continuously innovate to meet the evolving needs of defense forces. By addressing these challenges, market participants can position themselves for long-term success in the dynamic and rapidly evolving remote weapon systems landscape.

What will be the Size of the Remote Weapon Systems Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

The market continues to evolve, driven by the dynamic nature of modern military conflicts and the need for advanced capabilities in various sectors. Combat effectiveness is a key focus, with thermal imaging and stabilization systems enhancing the performance of naval vessels and infantry fighting vehicles. Rate of fire and remote control enable tactical deployment, while weapon systems integration and software defined radio facilitate battlefield management. Military doctrine emphasizes situational awareness, with infrared cameras and day/night vision providing critical information. Training simulation and modular design enable efficient preparation and adaptation to changing situations. Precision guided munitions and fire control systems ensure accuracy, while over-the-horizon targeting expands reach.

Electronic countermeasures and data link enhance force protection and communication, with machine learning and sensor fusion improving target tracking and object recognition. Weapon payload integration and open architecture enable network centric warfare, while laser rangefinders and frequency hopping provide additional advantages. The market unfolds with ongoing activities, from live fire exercises to weapon effectiveness evaluations. Anti-armor munitions and gunnery control are essential components, with electronic warfare and counter-terrorism operations requiring advanced capabilities. The continuous evolution of technology and military strategy shapes the market, with ongoing developments in computer vision, image intensifiers, and artificial intelligence shaping future applications.

How is this Remote Weapon Systems Industry segmented?

The remote weapon systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Sensor modules

- Weapons

- Human machine interface

- Technology

- Remote controlled gun systems

- Close in weapon systems

- Type

- Non-lethal weapons

- Lethal weapons

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

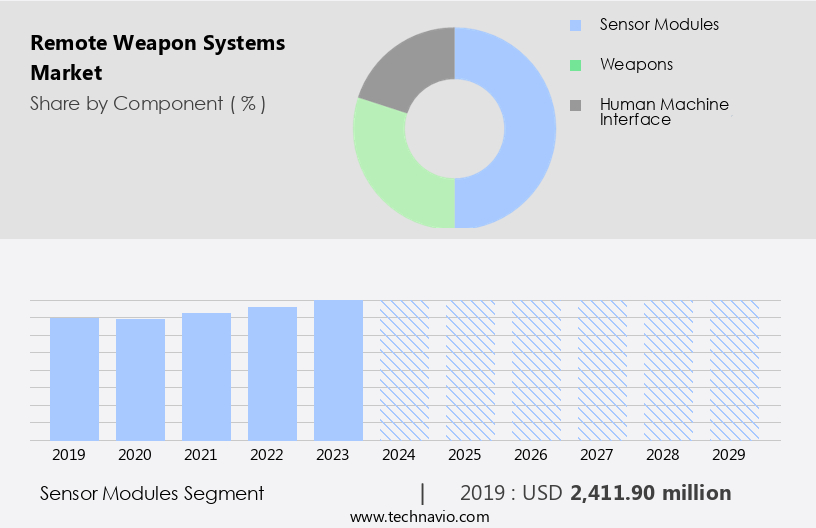

By Component Insights

The sensor modules segment is estimated to witness significant growth during the forecast period.

Remote weapon systems have become increasingly crucial in modern warfare due to their ability to enhance combat effectiveness through advanced sensors and remote control capabilities. These systems integrate various technologies such as thermal imaging, stabilization systems, and data links to provide situational awareness and improve hit probability. Naval vessels and infantry fighting vehicles are common platforms for remote weapon stations, which offer a high rate of fire and rapid tactical deployment. Sensor modules, including electro-optical systems, laser rangefinders, and infrared cameras, are essential components of remote weapon systems. Thermal imaging sensors enable target detection and identification in various lighting conditions, while laser rangefinders measure the distance to a target for accurate ballistic calculations.

Fire control systems integrate data from multiple sensors to provide target tracking and missile guidance, enabling precision-guided munitions to be employed effectively. Military doctrine emphasizes the importance of network centric warfare, sensor fusion, and open architecture, allowing for real-time data sharing and collaboration between forces. Machine learning and artificial intelligence are also being integrated into remote weapon systems to improve hit probability and autonomous operation. Electronic countermeasures and electronic warfare systems are critical for force protection and electronic signature management. Weapon systems integration and software-defined radio technology enable seamless communication and coordination between various platforms and forces. Training simulation and modular design allow for efficient and effective maintenance and upgrades.

Precision-guided munitions, such as airburst munitions, offer increased weapon effectiveness and reduced collateral damage. Remote weapon systems are also used in border security applications, providing situational awareness and deterrence against potential threats. Target tracking and day/night vision capabilities enable effective surveillance and response. In summary, remote weapon systems are essential components of modern military capabilities, providing enhanced situational awareness, precision, and effectiveness in various applications. The integration of advanced technologies and sensors continues to drive innovation and improve combat readiness.

The Sensor modules segment was valued at USD 2.41 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

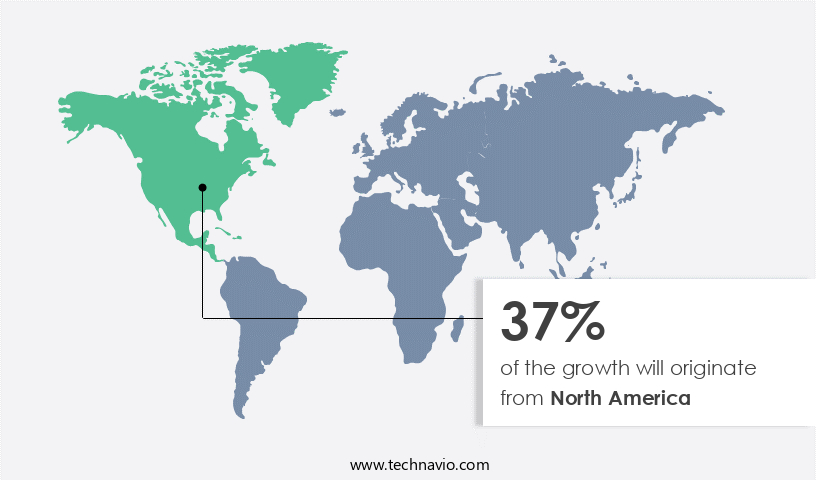

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in North America is significant due to the region's status as the largest military spender globally. The US Department of Defense (DoD) is a major buyer of remote weapon systems, with a substantial portion of its budget allocated through the National Defense Authorization Act (NDAA). The Defense Logistics Agency (DLA) manages all arms deals for the US military, encompassing raw materials, spare parts, fuel, sustenance, military equipment re-utilization, infrastructure, and inventory tracking and supplier management. Naval vessels in North America are extensively utilizing remote weapon stations for enhanced combat effectiveness and situational awareness. These systems integrate stabilization systems, thermal imaging, infrared cameras, and day/night vision for improved target identification and engagement.

Rate of fire and hit probability are crucial factors in the selection of remote weapon systems for naval applications. Military doctrine emphasizes the importance of battlefield management, and remote weapon systems play a pivotal role in this context. Real-time data link communication and sensor fusion enable effective target tracking and missile guidance. Live fire exercises are essential for testing weapon systems integration, software defined radio, and electronic countermeasures. Modular design, precision guided munitions, and weapon payload integration are essential features for remote weapon systems in various military applications, including border security, infantry fighting vehicles, armored vehicles, and military aircraft.

Machine learning, computer vision, and object recognition contribute to autonomous operation and counter-terrorism operations. Network centric warfare, open architecture, and sensor fusion are essential trends in the market, enhancing situational awareness and enabling effective force protection and electronic warfare capabilities. Over-the-horizon targeting and gunnery control systems are crucial for engaging targets at extended ranges. The supply chain for remote weapon systems involves various stakeholders, including manufacturers, integrators, and suppliers. Efficient management of this complex ecosystem is essential for maintaining readiness and ensuring the availability of critical components and systems.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Remote Weapon Systems Industry?

- The defense sector's escalating budget allocations serve as the primary catalyst for market growth.

- Remote weapon systems have gained significant attention in military defense due to increasing security threats and the need for combat effectiveness. These systems, which include thermal imaging, stabilization systems, and high explosive rounds, are integrated into naval vessels and ground platforms for tactical deployment. The integration of electronic countermeasures, data links, and machine learning enhances battlefield management and remote control capabilities. Military spending on defense has surged in developed and developing economies, such as the US, Germany, France, Canada, India, and China. NATO allies, including the US, Canada, and several European countries, have been directed to spend a minimum of 2% of their GDP on defense, with 23 of 32 NATO members achieving this goal as of 2024.

- This increased spending is driven by the need for advanced technology and capabilities to maintain combat readiness. Remote weapon stations offer numerous benefits, including increased rate of fire, improved accuracy, and reduced crew requirements. Thermal imaging technology enables weapons to be fired in low-light conditions, while stabilization systems ensure precision during movement. Data links facilitate communication between platforms, allowing for real-time tactical deployment and coordination. The integration of electronic countermeasures and machine learning enhances situational awareness and improves overall combat effectiveness. In conclusion, the demand for remote weapon systems is expected to continue growing due to the increasing need for advanced technology and capabilities in the defense sector.

- The integration of thermal imaging, stabilization systems, electronic countermeasures, data links, and machine learning enhances combat effectiveness and reduces crew requirements. Military spending on defense is projected to increase in developed and developing economies, making remote weapon systems a crucial investment for maintaining combat readiness.

What are the market trends shaping the Remote Weapon Systems Industry?

- Unmanned platforms are increasingly being equipped with remote weapon systems, representing a significant market trend in the defense industry. This deployment enables enhanced capabilities and flexibility for military operations.

- Remote weapon systems have gained significant importance in modern defense mechanisms due to the increasing adoption and deployment of unmanned platforms such as UAVs, UGVs, and UMVs. These systems are equipped with advanced cameras and sensors for reconnaissance operations and surveillance capabilities. Moreover, they have been armed with precision guided munitions for lethal purposes. Over the past decade, countries have invested substantially in the development and procurement of these next-generation unmanned platforms to enhance their security and surveillance capabilities. The focus on maritime warfare due to territorial disputes has further necessitated the acquisition and deployment of advanced remote weapon systems, including portable ground remote weapon stations and associated payloads and subsystems.

- These systems integrate advanced technologies such as hit probability calculations, missile guidance systems, software-defined radio, and infrared cameras to improve situational awareness and weapon effectiveness. Live fire exercises are conducted to test the performance and accuracy of these systems. Weapon systems integration and over-the-horizon targeting capabilities are essential features of these advanced systems. The use of modular designs enables easy upgrades and customization of these systems to meet evolving military doctrine requirements. Training simulation plays a crucial role in ensuring the effectiveness of these systems. The software-defined radio technology enables real-time communication and data exchange between various components of the remote weapon system.

- Infrared cameras provide thermal imaging capabilities, enhancing the system's ability to detect and engage targets in various weather conditions. Fire control systems ensure accurate and efficient weapon deployment, while precision-guided munitions increase the probability of a successful strike. Overall, the advanced features and capabilities of remote weapon systems make them an essential component of modern defense mechanisms.

What challenges does the Remote Weapon Systems Industry face during its growth?

- The complexities in the supply chain for remote weapon systems pose a significant challenge to industry growth, as threats resulting from these intricate networks can hinder progress and development in this sector.

- The defense logistics supply chain for remote weapon systems faces complexities and security threats, requiring strategic measures for mitigation. Regulatory requirements and export controls are stringent due to the military-grade technology involved. The unscheduled movement of defense forces during emergencies can disrupt maintenance and transportation of these systems. Integration of various technologies and the increasing number of terrorist activities pose security risks in the supply chain. Countries implement strategies to secure their defense logistics, ensuring the integrity and availability of remote weapon systems. These systems incorporate advanced technologies such as laser rangefinders, target tracking, day/night vision, and targeting systems.

- Military communications, including frequency hopping and electronic warfare, are essential for effective operation. Armored vehicles and infantry fighting vehicles are integral components of remote weapon systems, offering force protection. Electro-optical systems provide enhanced situational awareness, enabling accurate target engagement. Airburst munitions offer a decisive advantage in various combat scenarios. In conclusion, the defense logistics supply chain for remote weapon systems requires robust security measures and efficient management practices to address the complexities and threats. The integration of advanced technologies and a well-structured command and control system are crucial for maintaining operational readiness.

Exclusive Customer Landscape

The remote weapon systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the remote weapon systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, remote weapon systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ASELSAN AS - The company specializes in advanced remote weapon systems, including the AWG-35(V) Defense Weapon System. This system integrates a Weapon Control Computer, Motor Control Unit, Power Distribution Unit, Transformer Rectifier Unit, Sensor, Sensor Deploy Module, Gunner Control Station, and Weapon Turret. These components work in unison to provide precision and effectiveness in various applications. The Weapon Control Computer processes data from sensors to enable accurate targeting, while the Motor Control Unit manages weapon movement. The Power Distribution Unit ensures consistent power supply, and the Transformer Rectifier Unit converts AC to DC power. The Sensor and Sensor Deploy Module detect threats, and the Gunner Control Station allows for operator control. The Weapon Turret, a key component, houses the weapon and facilitates its deployment and aiming. The company's commitment to innovation and technology drives the development of these advanced systems.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ASELSAN AS

- BAE Systems Plc

- Elbit Systems Ltd.

- Electro Optic Systems Pty Ltd.

- FN Herstal SA

- General Dynamics Corp.

- Hanwha Corp.

- Israel Aerospace Industries Ltd.

- KNDS N.V.

- Kongsberg Gruppen ASA

- Leonardo Spa

- Moog Inc.

- NORINCOGROUP.com Inc.

- Rafael Advanced Defense Systems Ltd.

- Rheinmetall AG

- Rostec

- RTX Corp.

- Saab AB

- Singapore Technologies Engineering Ltd.

- Thales Group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Remote Weapon Systems Market

- In March 2024, Lockheed Martin unveiled its new Remote Gun System (RGS) for the M1 Abrams tank, marking a significant technological advancement in the market (Lockheed Martin Press Release, 2024). This system, which integrates a 30mm gun with advanced targeting sensors and a remote control interface, aims to enhance combat capabilities and reduce crew exposure to danger.

- In June 2024, Elbit Systems and Rafael Advanced Defense Systems announced a strategic partnership to jointly develop and market a new family of remote weapon stations (Elbit Systems Press Release, 2024). This collaboration combines Elbit's expertise in unmanned turret systems and Rafael's advanced weapon systems, creating a strong synergy that is expected to broaden their market reach and strengthen their competitive position.

- In October 2025, General Dynamics Land Systems secured a USD250 million contract from the U.S. Army to produce and deliver 345 Remote Weapon Stations for the Stryker Infantry Carrier Vehicle (General Dynamics Press Release, 2025). This contract underscores the growing demand for remote weapon systems in military applications and highlights the company's ability to meet this demand with its advanced offerings.

- In November 2025, Thales announced the successful deployment of its new remote weapon station, Turret 360, on the French Navy's new generation of patrol boats (Thales Press Release, 2025). This system, which offers 360-degree situational awareness and advanced targeting capabilities, is expected to significantly enhance the defensive capabilities of these vessels and further solidify Thales' position in the market.

Research Analyst Overview

- The market is experiencing significant advancements, driven by the integration of emerging technologies such as augmented reality, simulation software, and virtual reality. Field trials for trajectory prediction and threat detection systems are underway, enhancing weapon system accuracy and effectiveness. Hypersonic weapons and secure communications are prioritized for military modernization, while cyber warfare and obsolescence management remain critical concerns. Weapon system upgrades incorporate advanced materials, automatic target recognition, and human-machine interface to improve operational deployment. Ballistic missile defense relies on multi-spectral sensors and biometric authentication for enhanced security.

- Non-line-of-sight engagement and laser designator technologies expand engagement capabilities. Quantum computing and directed energy weapons are future game-changers, while anti-drone systems ensure airspace security. Life cycle cost reduction and cooperative engagement are essential for sustainable military modernization.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Remote Weapon Systems Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

204 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.6% |

|

Market growth 2025-2029 |

USD 1653.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.4 |

|

Key countries |

US, China, France, Canada, Germany, UK, Japan, India, South Korea, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Remote Weapon Systems Market Research and Growth Report?

- CAGR of the Remote Weapon Systems industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the remote weapon systems market growth of industry companies

We can help! Our analysts can customize this remote weapon systems market research report to meet your requirements.

RIA -

RIA -