US Beer Market Size 2025-2029

The US beer market size is valued to increase USD 25.6 billion, at a CAGR of 4.1% from 2024 to 2029. Increasing demand for premium beers will drive the US beer market.

Major Market Trends & Insights

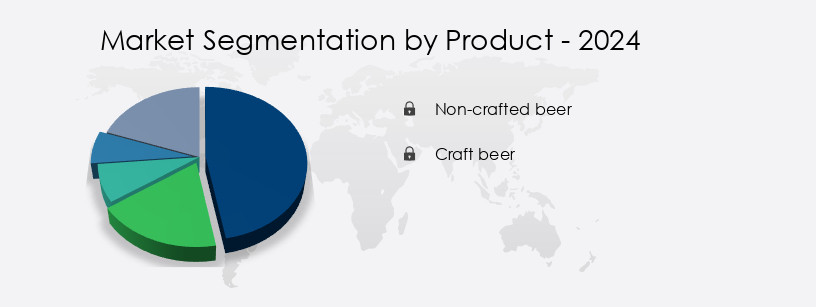

- By Product - Non-crafted beer segment was valued at USD 76.50 billion in 2022

- By Distribution Channel - On-trade segment accounted for the largest market revenue share in 2022

- CAGR from 2024 to 2029 : 4.1%

Market Summary

- The market is a dynamic and ever-evolving industry, characterized by the continuous introduction of new trends and innovations. One of the most notable developments is the increasing demand for premium beers, which currently account for over 20% of the total beer sales in the country. This shift in consumer preferences is driven by the growing awareness of craft beers and the desire for unique and authentic flavors. Another significant factor influencing the market is the introduction of new beer flavors, with fruit-infused and sour beers gaining popularity among consumers.

- Furthermore, the increasing growth of legal recreational cannabis in some states is expected to create new opportunities for the beer industry, as cannabis-infused beers gain traction among consumers. Despite these opportunities, the market faces challenges such as increasing competition and changing consumer preferences, which require brewers to stay agile and adapt to the evolving market landscape.

What will be the Size of the US Beer Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the US Beer Market Segmented?

The US beer industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Non-crafted beer

- Craft beer

- Distribution Channel

- On-trade

- Off-trade

- Packaging

- Bottles

- Cans

- Kegs

- Geography

- North America

- US

- North America

By Product Insights

The non-crafted beer segment is estimated to witness significant growth during the forecast period.

The market is in a state of continuous evolution, with ongoing activities and emerging patterns shaping the industry. Commercial beer production, spearheaded by macro-breweries like Molson Coors, Diageo, and Anheuser-Busch, focuses on large-scale production of diverse branded beers. However, these beers often lack the complex flavor profiles and unique character of craft beers. A significant shift in consumer preferences is driving change in the market. According to recent studies, approximately 53% of the US population in their 20s who consume alcohol do not favor beer. Instead, they lean towards wine and spirits. This trend, prevalent among younger generations like Generation Z, is reshaping the industry landscape.

Breweries must adapt to these evolving preferences, focusing on flavor innovation, ingredient sourcing, and process optimization. Key aspects of beer production, such as hop varieties, barley types, carbonation levels, and lagering processes, are being re-evaluated to meet the demands of discerning consumers. Quality assurance, from mashing schedules to water chemistry and aroma compounds, is a critical focus to ensure consistency and prevent microbial contamination. Brewing techniques, pasteurization methods, beer aging, and sensory evaluation are all undergoing refinement to enhance production efficiency and alcohol content while maintaining the desired flavor profiles. Packaging materials, such as SRM color scale and keg filling, are also being optimized for improved shelf life and consumer experience.

Ultimately, the beer market's future success hinges on the ability to adapt to these shifts while maintaining the highest standards of quality and innovation.

The Non-crafted beer segment was valued at USD 76.50 billion in 2019 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is a dynamic and intricately woven industry that encompasses various aspects of brewing science and technology. One of the critical factors influencing beer production in this market is the impact of hop isomerization during brewing. The wort boiling temperature significantly affects the isomerization process, which in turn influences the beer's bitterness and flavor profile. Another crucial element is yeast viability and fermentation performance. Malt modification, with its diastatic power, plays a pivotal role in determining the beer's color and sensory attributes. Beer color measurement methods are essential for ensuring consistency and quality in various beer styles.

Water hardness also influences beer flavor, with optimal fermentation temperature control being essential for maintaining beer stability. Packaging material oxygen barrier properties are vital for preserving beer's freshness and preventing spoilage bacteria. Beer aging flavor compounds are impacted by temperature and carbonation pressure, which in turn affect foam quality and filtration membrane efficiency. Yeast selection significantly influences the beer profile, and malt quality impacts the brewing process's overall efficiency. Measuring beer bitterness through IBU (International Bittering Units) is a standard practice in the industry, and controlling fermentation parameters is crucial for maintaining beer stability. Advanced beer stability prediction models help brewers optimize their processes and improve efficiency.

Compared to traditional methods, modern brewing processes prioritize temperature control and automation to enhance efficiency and consistency. For instance, more than 70% of new breweries in the US invest in advanced temperature control systems, significantly outpacing the adoption rate in older, traditional breweries. This shift towards technology-driven brewing is transforming the market landscape.

What are the key market drivers leading to the rise in the adoption of US Beer Industry?

- The surge in consumer preference for high-end beers serves as the primary catalyst for market growth in this sector.

- The premium beer segment is experiencing significant growth in the US market, fueled by consumers' preference for authentic taste and brand identity. Companies such as Heineken are capitalizing on this trend by offering a diverse range of premium beer brands, including Birra Moretti, Tiger, Tecate, Krusovice, and Red Stripe. The increasing per capita income in the US is a key factor driving the demand for premium beers, with consumers willing to pay a premium for superior quality and unique flavors.

- The beer market in the US is expected to witness continuous expansion, as the trend towards premium and craft beers gains momentum across various demographics. This shift in consumer preferences is a notable development in the beverage industry, underscoring the importance of catering to evolving tastes and preferences.

What are the market trends shaping the US Beer Industry?

- The introduction of new beer flavors is currently a significant market trend. This trend reflects the evolving preferences of consumers and the continuous innovation within the beer industry.

- The market is experiencing a significant shift towards flavored beer, driven by an expanding consumer base and innovative offerings from craft brewers. Flavored beers differentiate themselves from traditional brews, attracting a broader audience and fueling market growth. In response, companies have been introducing new flavors to their product lines. For example, Yuengling, a leading beer brand, launched Bongo Fizz in November 2024, a premium beer infused with natural mango flavor, adding to the diverse range of options available in the market.

- This trend signifies the dynamic nature of the US beer industry, where continuous innovation and consumer preferences shape market developments.

What challenges does the US Beer Industry face during its growth?

- The expansion of legal recreational cannabis use poses a significant challenge to the industry, as the increasing demand and regulatory complexities may impact growth trajectories.

- The legalization of recreational cannabis in certain US states has significantly impacted the beer market. This trend was already underway due to the increasing demand for alternative beverage options like wine, spirits, and malt beverages. States with high densities of craft breweries and extensive beer availability, such as Oregon, Colorado, and Washington, have seen a noticeable decline in beer sales following the legalization of recreational cannabis. This shift is a response to consumers seeking new experiences and preferences, which cannabis offers in contrast to traditional beer. The beer market's challenges are not limited to these substitutes; it also faces regulatory hurdles and evolving consumer preferences.

- As a professional, it's essential to acknowledge these trends and their implications for the industry.

Exclusive Technavio Analysis on Customer Landscape

The US beer market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the US beer market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of US Beer Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, US beer market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Anheuser Busch InBev SA NV - This company specializes in producing innovative beverage options beyond traditional beer.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anheuser Busch InBev SA NV

- Asahi Group Holdings Ltd.

- Bells Brewery Inc.

- Carlsberg Breweries AS

- Constellation Brands Inc.

- D.G. Yuengling and Son Inc.

- Deschutes Brewery

- Diageo PLC

- Duvel Moortgat NV

- FIFCO USA

- Heineken NV

- Molson Coors Beverage Co.

- New Belgium Brewing Co. Inc.

- Pabst Brewing

- SALT LAKE BREWING CO

- Sierra Nevada Brewing Co.

- Stone Brewing Co. LLC

- Suntory Holdings Ltd.

- The Boston Beer Co. Inc.

- The Mark Anthony Group of Companies

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in US Beer Market

- In January 2024, Anheuser-Busch InBev, the world's largest brewer, announced the launch of its new hard seltzer brand, 'Bud Light Seltzer,' in the US market (Anheuser-Busch InBev press release, 2024). This move aimed to capitalize on the growing popularity of hard seltzers, with market research indicating a 76.2% increase in sales volume in 2023 (IBISWorld, 2024).

- In March 2024, MillerCoors, the second-largest US beer producer, entered into a strategic partnership with Molson Coors Beverage Company to form a new joint venture, Tenth and Blake Beer Company, focusing on craft breweries and import brands (MillerCoors press release, 2024). This collaboration was expected to strengthen their positions in the competitive craft beer segment.

- In May 2024, Constellation Brands, a leading wine, beer, and spirits company, completed the acquisition of Fieldhouse Brewing Company, a fast-growing craft brewer based in Ohio, for an undisclosed amount (Constellation Brands press release, 2024). This acquisition expanded Constellation's craft beer portfolio and increased its presence in the Midwest region.

- In April 2025, the US Alcohol and Tobacco Tax and Trade Bureau (TTB) approved the label for Boston Beer Company's new hard kombucha product, Truly Hard Kombucha, marking the first major US beer company to enter the hard kombucha market (Boston Beer Company press release, 2025). This approval signaled a potential new trend in the US beer industry, as hard kombucha combines the popularity of hard seltzers and craft beers.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Beer Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

164 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.1% |

|

Market growth 2025-2029 |

USD 25.6 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

3.9 |

|

Key countries |

US |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The dynamic and evolving market showcases a rich tapestry of styles, ingredients, and processes that continue to captivate consumers and industry professionals alike. This intriguing landscape is shaped by various factors, including hop and barley varieties, carbonation levels, and the lagering process. Hops and barley are essential components of beer production, with numerous varieties influencing flavor profiles. Hop varieties, such as Cascade, Centennial, and Citra, contribute unique aromas and bitterness levels, while barley varieties like Maris Otter and Munich malt add depth and complexity to the final product. Carbonation levels and the lagering process significantly impact the beer drinking experience.

- Carbonation provides the effervescence that enhances the taste sensation, while lagering refines the beer's flavors and clarifies it, resulting in a smoother, more refined beverage. Brewing techniques, such as mashing schedules and water chemistry, play a crucial role in determining beer's taste and quality. For instance, mashing schedules influence the degree of sugar conversion, while water chemistry affects the beer's pH balance and mineral content. Aroma compounds, microbial contamination, and ingredient sourcing are essential aspects of beer quality. Aroma compounds contribute to the beer's unique scent, while microbial contamination can negatively impact the taste and shelf life.

- Ingredient sourcing ensures the consistency and authenticity of the beer's flavor profile. Quality assurance measures, such as gravity readings, sensory evaluation, and quality control metrics, ensure that the final product meets the desired specifications. Packaging materials, pasteurization techniques, and beer aging further impact the beer's shelf life and overall quality. The market is a complex and fascinating ecosystem, with ongoing research and innovation shaping its dynamics. Brewing techniques, ingredient sourcing, and process optimization continue to evolve, ensuring that consumers enjoy a diverse and ever-improving range of beer styles.

What are the Key Data Covered in this US Beer Market Research and Growth Report?

-

What is the expected growth of the US Beer Market between 2025 and 2029?

-

USD 25.6 billion, at a CAGR of 4.1%

-

-

What segmentation does the market report cover?

-

The report segmented by Product (Non-crafted beer and Craft beer), Distribution Channel (On-trade and Off-trade), Packaging (Bottles, Cans, and Kegs), and Geography (North America)

-

-

Which regions are analyzed in the report?

-

US

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for premium beers, Increasing growth of legal recreational cannabis

-

-

Who are the major players in the US Beer Market?

-

Key Companies Anheuser Busch InBev SA NV, Asahi Group Holdings Ltd., Bells Brewery Inc., Carlsberg Breweries AS, Constellation Brands Inc., D.G. Yuengling and Son Inc., Deschutes Brewery, Diageo PLC, Duvel Moortgat NV, FIFCO USA, Heineken NV, Molson Coors Beverage Co., New Belgium Brewing Co. Inc., Pabst Brewing, SALT LAKE BREWING CO, Sierra Nevada Brewing Co., Stone Brewing Co. LLC, Suntory Holdings Ltd., The Boston Beer Co. Inc., and The Mark Anthony Group of Companies

-

Market Research Insights

- The market is a dynamic and complex industry, characterized by ongoing innovation and adaptation to consumer preferences and regulatory requirements. Sales data reveals a steady growth in the market, with an estimated production capacity of over 160 million barrels in 2021, up from 155 million barrels in 2019. Quality testing plays a crucial role in ensuring beer stability and consumer satisfaction, with sensory panels conducting rigorous analysis to assess flavor chemistry and beer preservation. Tax regulations and regulatory compliance also impact brewing efficiency and production costs, with breweries implementing process automation and data analytics to optimize yield and reduce energy consumption.

- Distribution channels continue to evolve, with a focus on sustainability practices and packaging technology to enhance shelf life and labeling requirements. Ingredient quality and waste management are key concerns for breweries, with wort production and inventory control essential for maintaining production capacity and cost reduction. Despite these challenges, the market remains a vibrant and competitive industry, with breweries continually investing in process control systems and innovation to meet evolving consumer demands.

We can help! Our analysts can customize this US beer market research report to meet your requirements.