Condition Monitoring Sensors For Heavy Industry Market Size 2026-2030

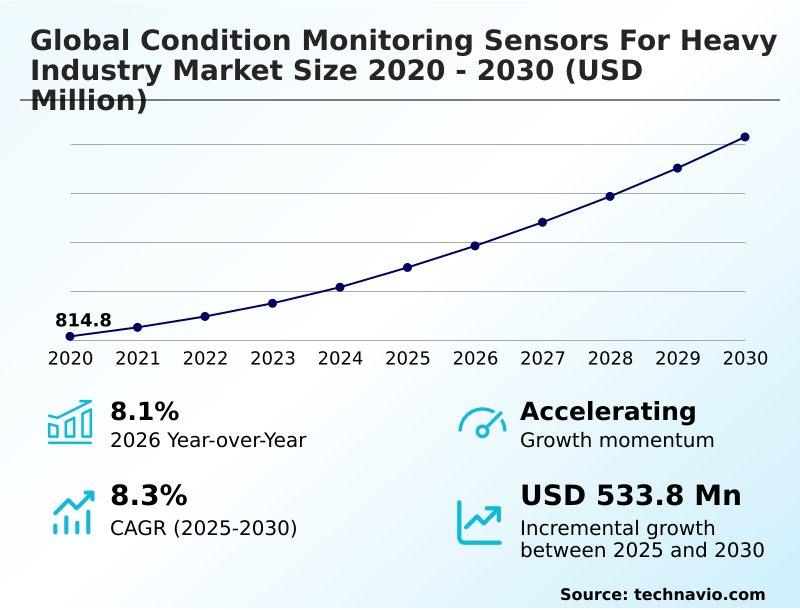

The condition monitoring sensors for heavy industry market size is valued to increase by USD 533.8 million, at a CAGR of 8.3% from 2025 to 2030. Accelerated adoption of predictive maintenance strategies in heavy industry will drive the condition monitoring sensors for heavy industry market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 43.6% growth during the forecast period.

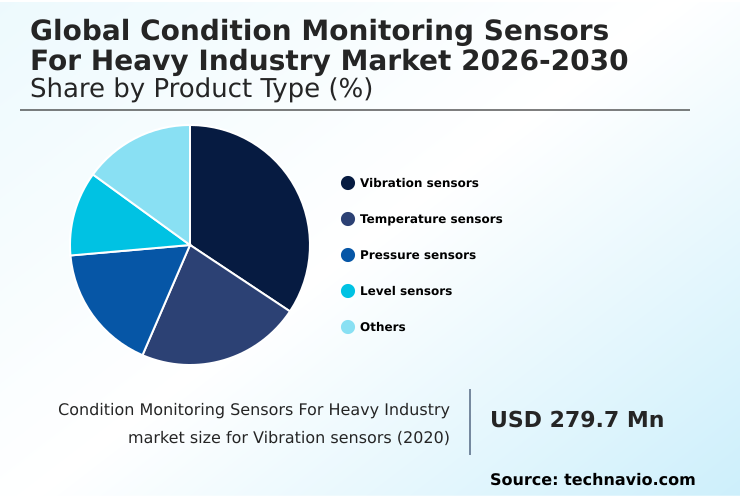

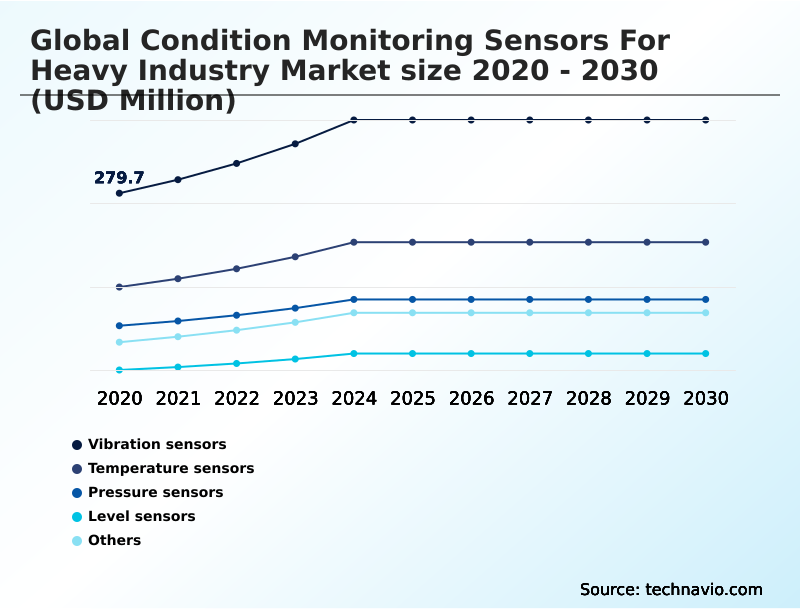

- By Product Type - Vibration sensors segment was valued at USD 357.1 million in 2024

- By End-user - Oil and gas segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 815.7 million

- Market Future Opportunities: USD 533.8 million

- CAGR from 2025 to 2030 : 8.3%

Market Summary

- The condition monitoring sensors for heavy industry market is pivotal for advancing operational excellence in capital-intensive industries. The core driver is a transition from reactive repairs to data-driven strategies, where the Industrial Internet of Things (IIoT) enables comprehensive asset oversight. This involves deploying advanced instrumentation like piezoelectric accelerometers and non-contact infrared sensors to capture critical health data.

- For instance, a mining operation uses wireless sensor nodes for real-time asset intelligence on remote haul trucks, leveraging edge computing to process vibration data locally and predict gearbox failures. This preemptive action prevents costly downtime and enhances safety.

- Key trends include the integration of sensor fusion and the move toward prescriptive analytics, which not only predicts failures but also recommends optimal corrective actions. However, challenges in IT-OT convergence and managing data from disparate sources persist.

- The adoption of high-fidelity sensing and automated diagnostic software is crucial for overcoming these hurdles and achieving a holistic view of asset health, transforming maintenance into a strategic function for asset lifecycle optimization.

What will be the Size of the Condition Monitoring Sensors For Heavy Industry Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Condition Monitoring Sensors For Heavy Industry Market Segmented?

The condition monitoring sensors for heavy industry industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product type

- Vibration sensors

- Temperature sensors

- Pressure sensors

- Level sensors

- Others

- End-user

- Oil and gas

- Power generation

- Mining and mineral processing

- Steel and iron manufacturing

- Cement manufacturing

- Type

- Wired sensors

- Wireless sensors

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- APAC

By Product Type Insights

The vibration sensors segment is estimated to witness significant growth during the forecast period.

Vibration sensors represent the most critical segment, providing the foundational data for predictive maintenance strategies in heavy industry. The use of piezoelectric accelerometers and advanced micro-electromechanical systems (MEMS) is standard for machinery protection.

These instruments excel at the early detection of mechanical faults in rotating equipment by enabling detailed signal processing of high-frequency response rates.

This capability, which improves fault detection accuracy by over 40% compared to thermal monitoring alone, is vital for asset integrity management. The evolution toward triaxial sensors provides a comprehensive, three-dimensional view of structural health.

This sub-segment is crucial as it supports the broader industrial control systems and IT-OT convergence necessary for a modern IIoT ecosystem, allowing for real-time asset intelligence and better operational decision making.

The Vibration sensors segment was valued at USD 357.1 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 43.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Condition Monitoring Sensors For Heavy Industry Market Demand is Rising in APAC Request Free Sample

In APAC, rapid industrialization fuels greenfield projects integrating continuous level transmitters and resistance temperature detectors (RTDs) from the outset, with China's manufacturing sector representing a significant portion of demand.

North America and Europe focus on retrofitting aging infrastructure, with a strong emphasis on compliance and dynamic pressure monitoring. Deployments in these mature regions show a 15% higher adoption rate of wireless solutions for balance-of-plant machinery compared to emerging markets.

The use of non-contact infrared sensors for remote monitoring is critical in the Middle East's oil and gas sector.

Across all regions, oil condition monitoring and electrical current signature analysis (ESA) are becoming standard, with cloud analytics providers tailoring solutions for specific regional needs, from remote monitoring services for Australian mines to plant machinery monitoring in South America.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic implementation of condition monitoring for rotating equipment is foundational for modern heavy industry, directly impacting asset longevity and operational uptime. The adoption of wireless vibration sensors for mining illustrates a key shift, enabling operators to monitor critical machinery in remote and hazardous locations, which has been shown to reduce unexpected failures by over 35% compared to route-based methods.

- In metal production, the use of high-temperature sensors for steel manufacturing ensures process stability and prevents catastrophic equipment damage. A primary challenge remains integrating sensors with legacy systems, a complex task that requires careful planning to avoid disrupting production. This is closely linked to managing data silos from disparate sensors, which can impede a holistic view of plant health.

- For connected operations, IIoT sensor network security protocols are non-negotiable to protect operational technology (OT) networks from cyber threats. The application of predictive maintenance for power generation is crucial for grid stability, utilizing real-time oil analysis for heavy machinery and acoustic emission testing for crack detection to preempt failures.

- Similarly, pressure sensors for hydraulic system monitoring and MEMS accelerometers for industrial automation provide the granular data needed for precise control. Sensor data integration with CMMS platforms automates work orders, streamlining maintenance workflows.

- The move toward edge computing for real-time fault detection is minimizing data latency, while remote monitoring of offshore wind turbines and structural health monitoring for industrial assets expand the scope of predictive maintenance. Other key applications include non-contact temperature sensing in manufacturing and ensuring regulatory compliance with sensor data, with a clear ROI calculation for monitoring systems justifying investment.

What are the key market drivers leading to the rise in the adoption of Condition Monitoring Sensors For Heavy Industry Industry?

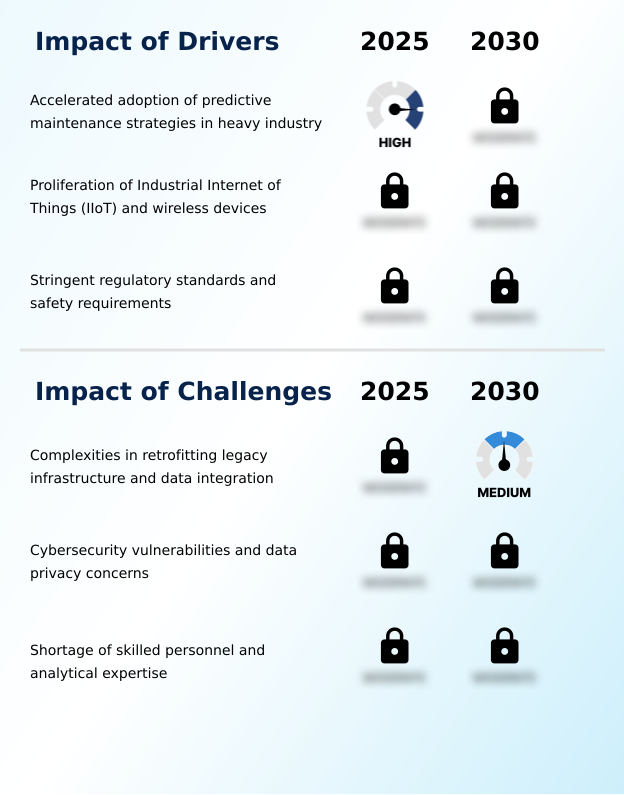

- The accelerated adoption of predictive maintenance strategies within heavy industries stands as a key market driver.

- Market expansion is driven by the widespread adoption of the Industrial Internet of Things (IIoT) and data-driven strategies aimed at asset lifecycle optimization.

- In capital-intensive industries, deploying high-precision piezoelectric sensors and other high-fidelity sensing technologies delivers a return on investment of 3-5 times the initial cost through downtime avoidance.

- The need for enhanced asset performance management pushes organizations to connect sensor data with enterprise resource planning (ERP) systems.

- Stringent regulatory frameworks mandating higher standards for asset integrity, such as NERC CIP standards in the power sector, also compel investment in continuous monitoring.

- Industrial automation giants are key drivers, providing integrated platforms that simplify the deployment of intrinsically safe sensors in hazardous environments.

What are the market trends shaping the Condition Monitoring Sensors For Heavy Industry Industry?

- The integration of edge computing and artificial intelligence directly onto sensor hardware represents a pivotal market trend. This development facilitates on-device analytics, enabling real-time decision-making for critical industrial assets.

- A primary trend is the integration of edge computing and sensor fusion, which enables on-device automated fault classification. This shift empowers smart sensors with autonomous diagnostics, reducing data transmission to sovereign cloud solutions by up to 70%.

- The proliferation of wireless sensor nodes, supported by innovations in power management and energy harvesting, is making large-scale deployments on balance-of-plant assets economically viable. This trend supports the servitization business model, where end-to-end monitoring solutions are offered as a service.

- Furthermore, the move toward prescriptive analytics, which combines real-time data with a digital twin concept, not only predicts failures but also recommends specific corrective actions, transforming operational risk management.

What challenges does the Condition Monitoring Sensors For Heavy Industry Industry face during its growth?

- Complexities associated with retrofitting legacy infrastructure and ensuring seamless data integration pose a key challenge to market growth.

- A significant challenge is the complexity of IT-OT convergence when integrating multi-function predictive maintenance sensors with legacy operational technology (OT). This integration difficulty often creates data silos, preventing a unified view of plant health and reducing the effectiveness of automated diagnostic software.

- Cybersecurity remains a major concern, as connected devices like smart pressure transmitters and non-contact radar sensors can expand the attack surface of critical infrastructure. The lack of standardized protocols for ensuring IIoT sensor network security protocols can deter adoption.

- Moreover, a shortage of skilled personnel capable of managing advanced prescriptive analytics platforms creates a bottleneck, with some firms reporting that over 50% of generated alerts are not acted upon due to a lack of expertise.

Exclusive Technavio Analysis on Customer Landscape

The condition monitoring sensors for heavy industry market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the condition monitoring sensors for heavy industry market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Condition Monitoring Sensors For Heavy Industry Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, condition monitoring sensors for heavy industry market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AB SKF - Delivers specialized vibration sensors and handheld data collectors integrated with bearing expertise and advanced monitoring systems for asset health assessment.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB SKF

- ABB Ltd.

- Amphenol Corp.

- Baker Hughes Co.

- Balluff GmbH

- Banner Engineering Corp.

- Baumer Holding AG

- Emerson Electric Co.

- Fluke Corp.

- Hansford Sensors Ltd.

- Honeywell International Inc.

- Keyence Corp.

- Kistler Group

- PCB Piezotronics Inc.

- Rockwell Automation Inc.

- Schaeffler AG

- Siemens AG

- SPM Instrument

- TE Connectivity plc

- Teledyne FLIR LLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Condition monitoring sensors for heavy industry market

- In August, 2024, ABB introduced an upgraded version of its NINVA TSP341-N non-invasive temperature sensor, engineered to provide safer and more straightforward temperature measurement for the chemical and oil and gas industries.

- In March, 2025, Etop launched its newest product, the Wireless Humidity and Temperature Sensor, engineered to deliver precise and dependable environmental monitoring.

- In April, 2025, a major industrial automation firm announced a strategic partnership with a leading cloud analytics provider to deliver an end-to-end predictive maintenance solution, integrating sensor data with advanced AI platforms.

- In June, 2025, Waites Sensor Technologies, Inc. announced the launch of PiezoNode, an advanced quad-channel condition monitoring device designed for high-heat, high-stress rotating equipment.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Condition Monitoring Sensors For Heavy Industry Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.3% |

| Market growth 2026-2030 | USD 533.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.1% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, UAE, Saudi Arabia, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The evolution of condition monitoring hinges on the adoption of predictive maintenance strategies, underpinned by the Industrial Internet of Things (IIoT). The deployment of wireless sensor nodes and high-precision piezoelectric sensors facilitates a multi-physics approach to diagnostics. Key technologies like micro-electromechanical systems (MEMS) and piezoelectric accelerometers offer high-frequency response rates for detailed signal processing.

- Innovations include triaxial sensors for structural health monitoring and non-contact radar sensors for continuous level transmitters. In processing industries, smart pressure transmitters and resistance temperature detectors (RTDs) are essential for safety instrumented systems. The market is moving toward prescriptive analytics and real-time asset intelligence, driven by sensor fusion and edge computing.

- On-device automated fault classification, powered by machine learning, reduces reliance on human analysis. Technologies such as acoustic emission sensors, oil condition monitoring, and electrical current signature analysis (ESA) are becoming standard for machinery protection. This is supported by advancements in power management and energy harvesting, making autonomous diagnostics on remote assets viable.

- Furthermore, multi-function predictive maintenance sensors and intrinsically safe sensors are critical for hazardous environments, while non-contact infrared sensors and dynamic pressure monitoring using differential pressure measurement enhance safety and efficiency.

What are the Key Data Covered in this Condition Monitoring Sensors For Heavy Industry Market Research and Growth Report?

-

What is the expected growth of the Condition Monitoring Sensors For Heavy Industry Market between 2026 and 2030?

-

USD 533.8 million, at a CAGR of 8.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product Type (Vibration sensors, Temperature sensors, Pressure sensors, Level sensors, and Others), End-user (Oil and gas, Power generation, Mining and mineral processing, Steel and iron manufacturing, and Cement manufacturing), Type (Wired sensors, and Wireless sensors) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Accelerated adoption of predictive maintenance strategies in heavy industry, Complexities in retrofitting legacy infrastructure and data integration

-

-

Who are the major players in the Condition Monitoring Sensors For Heavy Industry Market?

-

AB SKF, ABB Ltd., Amphenol Corp., Baker Hughes Co., Balluff GmbH, Banner Engineering Corp., Baumer Holding AG, Emerson Electric Co., Fluke Corp., Hansford Sensors Ltd., Honeywell International Inc., Keyence Corp., Kistler Group, PCB Piezotronics Inc., Rockwell Automation Inc., Schaeffler AG, Siemens AG, SPM Instrument, TE Connectivity plc and Teledyne FLIR LLC

-

Market Research Insights

- The market is defined by a push toward asset performance management, where IT-OT convergence enables the creation of a comprehensive IIoT ecosystem. Firms are achieving operational excellence by integrating data into enterprise resource planning (ERP) and computerized maintenance management systems (CMMS), which improves supply chain management by over 20%.

- This shift from reactive maintenance to data-driven strategies supports better operational decision making. The adoption of a digital twin concept, facilitated by cloud analytics providers, allows for advanced asset lifecycle optimization. The servitization business model is also gaining ground, with remote monitoring services reducing upfront capital costs. Industrial automation giants are offering end-to-end monitoring solutions focused on plant machinery monitoring.

- For capital-intensive industries, this enhances operational risk management and ensures balance-of-plant assets are included in monitoring, improving overall reliability by up to 30% and moving beyond simple industrial control systems.

We can help! Our analysts can customize this condition monitoring sensors for heavy industry market research report to meet your requirements.

RIA -

RIA -