Rotary Air Compressor Market Size 2024-2028

The rotary air compressor market size is forecast to increase by USD 2.61 billion at a CAGR of 3.27% between 2023 and 2028. The market is experiencing significant growth due to the increasing demand for consistent and oil-free compressed air in various industries, including process industries such as oil & gas, waste management, and chemicals. This trend is driven by the need for cost-effective and efficient compressed air solutions, which are essential for the smooth operation of various applications. One of the key market trends is the rising number of mergers and acquisitions, as companies look to expand their product offerings and strengthen their market positions. Additionally, fluctuations in raw material prices can impact the market, as the cost of manufacturing compressors can vary depending on the availability and price of materials.

What will be the Size of the Market During the Forecast Period?

Rotary air compressors are essential components in various industries, providing compressed air for powering pneumatic tools and systems. This market explores the current trends and applications in diverse sectors such as oil & gas, waste management, chemicals, power generation, mining, consumer goods, semiconductor & electronics, pharmaceuticals, food & beverage, energy & mining, and more. In the oil & gas industry, rotary air compressors are utilized for powering drilling operations, gas processing, and oil refining. These compressors ensure the efficient transfer of gases and fluids, contributing to increased productivity and cost savings.

Moreover, waste management and environmental services rely on these for powering various equipment, including waste compactors and conveyor systems. The compressed air generated by these compressors enables the efficient handling and transportation of waste materials. Chemicals and pharmaceuticals industries utilize them for powering production processes, such as mixing, filling, and packaging. The consistent and reliable air supply provided by these compressors ensures the production of high-quality products and reduces downtime. Power generation and mining sectors use them for various applications, including generating compressed air for powering pneumatic tools and systems, as well as for powering auxiliary equipment, such as generators and compressors.

Furthermore, consumer goods manufacturing industries, including food & beverage and semiconductor & electronics, rely on these compressors for powering various production processes, such as packaging, assembly, and testing. These compressors ensure consistent air quality and pressure, contributing to increased efficiency and product quality. They are also widely used in the energy & mining sector for powering drilling operations, as well as for compressing natural gas for transportation and storage. These compressors play a crucial role in maximizing productivity and reducing operational costs.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Manufacturing industry

- Mining and metallurgy industry

- Others

- Geography

- APAC

- China

- Japan

- Europe

- Germany

- UK

- North America

- US

- Middle East and Africa

- South America

- APAC

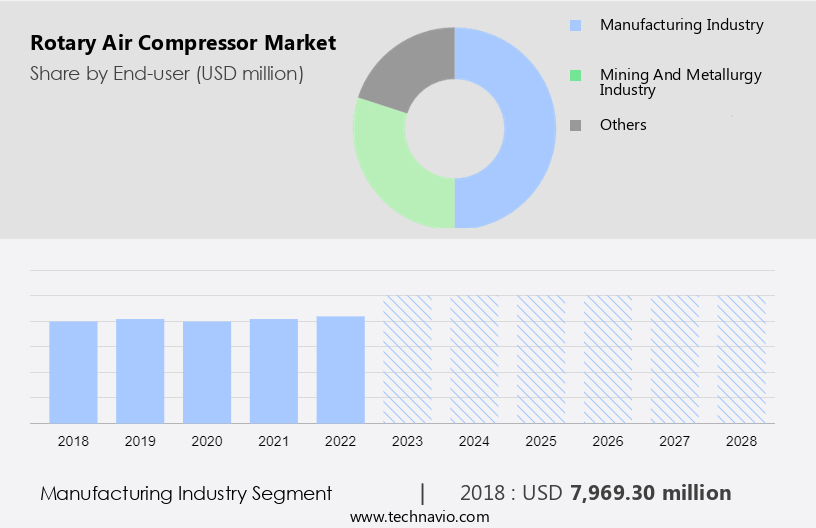

By End-user Insights

The manufacturing industry segment is estimated to witness significant growth during the forecast period. They play a significant role in numerous manufacturing sectors, including automotive, chemicals, oil & gas, waste management, and process industries. The automotive industry is a major contributor to the market's growth, as rotary compressors are indispensable in automobile production. In this industry, they provide consistent compressed air for tire inflation and maintenance, vehicle bodybuilding, and painting facilities. The increasing global automobile sales, particularly in Europe and APAC, have led to significant investments in the automotive sector, thereby boosting the demand for these compressors. ABAC Air Compressors, along with other key players, offer cost-effective rotary air compressor solutions to cater to the growing demand.

Get a glance at the market share of various segments Request Free Sample

The Manufacturing industry segment accounted for USD 7.96 billion in 2018 and showed a gradual increase during the forecast period.

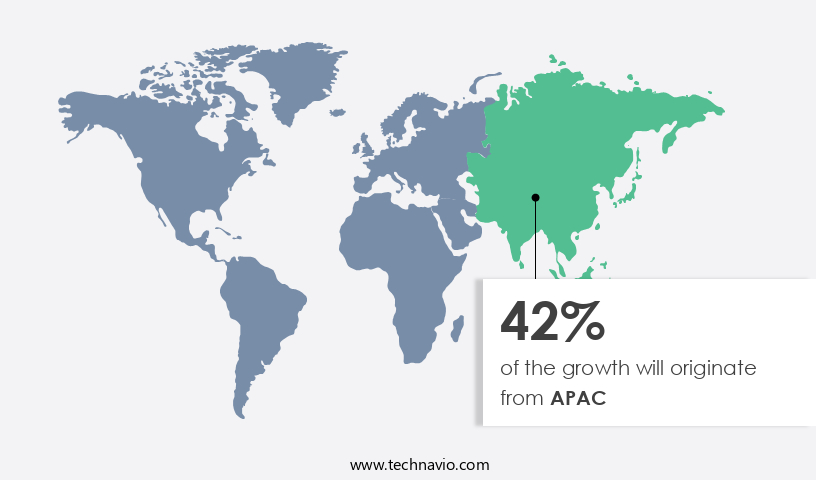

Regional Insights

APAC is estimated to contribute 42% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

Rotary air compressors play a vital role in various industries, including automotive, chemical and materials, medical devices, consumer goods, semiconductor and electronics, pharmaceutical, food and beverage, energy and mining, and more. In the automotive sector, rotary air compressors are utilized for applications such as tire inflation, air-operated robots, product finishing, plasma cutting and welding, and painting. The Asia Pacific (APAC) region, home to six of the world's largest two-wheeler markets, is expected to lead the global two-wheeler market's growth. APAC's strong expansion in automotive production and sales is driving the demand for rotary air compressors in this industry. The region's economic growth, increasing disposable incomes, and traffic congestion are significant factors contributing to the rising adoption of two-wheelers, thereby increasing the demand for rotary air compressors. This trend is expected to continue, making it a promising market for manufacturers and investors.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Rising number of HVAC installations is the key driver of the market. Rotary air compressors are essential components in heating, ventilation, and air conditioning (HVAC) systems, responsible for compressing refrigerant and preparing it for cooling. These compressors utilize a rotary-type positive-displacement mechanism. The escalating demand for HVAC systems in commercial and residential buildings is primarily driven by substantial investments in infrastructure development. This trend is propelling the demand for rotary air compressors, as they are indispensable elements in HVAC systems. The construction sector is witnessing a rise in projects, fueled by population growth and government support. Consequently, the need for advanced HVAC systems to ensure energy efficiency and optimal performance is increasingly recognized.

Rotary air compressors, with their high-efficiency rotary screw and rotary vane designs, are well-positioned to meet the evolving demands of the HVAC industry. Furthermore, rotary air compressors find extensive applications in various sectors, including aerospace, automation, robotics, and medicine, underlining their significance in diverse industries.

Market Trends

Mergers and acquisitions is the upcoming trend in the market. The market is experiencing significant competition among companies, who are focusing on price, product quality, efficiency, supply chain, and product diversification to maintain and expand their market positions. Various rotary air compressor manufacturers operate at both the global and regional levels, employing mergers and acquisitions (M&A) as a strategic business move. By merging, these companies can lower production costs and improve performance. A company that pursues a merger for diversification benefits from the acquisition of a business in a seemingly unrelated sector, thereby mitigating the impact of that sector's performance on its profitability.

The rotary air compressor industry caters to various sectors, including the oil & gas and energy industries, where pneumatic solutions are essential. IoT integration in rotary air compressors enhances their functionality and efficiency, making them an attractive choice for industrial settings. companies are also focusing on lubrication and cooling systems to ensure optimal performance and longevity. In summary, the market is a dynamic and competitive landscape, with companies leveraging various strategies to meet the evolving demands of their customers.

Market Challenge

Fluctuations in raw material prices is a key challenge affecting the market growth. Rotary air compressors are essential equipment in various industries, including healthcare, wind energy, solar energy, e-commerce, and logistics operations.

The production cost of these compressors is influenced by several factors, including the availability and cost of raw materials, competition among companies, and labor costs. Aluminum, steel, and castings are the primary components used in the manufacturing process. Fluctuations in the prices of these raw materials can significantly impact the final cost of rotary air compressors.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Atlas Copco AB - The company offers rotary air compressors such as G series, GA screw compressors series and GR two stage.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Atlas Copco AB

- Berkshire Hathaway Inc.

- Curtis Toledo Inc.

- Deere and Co.

- Doosan Corp.

- Dover Corp.

- Elgi Equipments Ltd

- Frank Technologies Pvt Ltd

- G and E Industrial Supplies Inc

- Hitachi Ltd.

- Ingersoll Rand Inc.

- KAESER KOMPRESSOREN SE

- Kirloskar Pneumatic Co. Ltd.

- Kobe Steel Ltd.

- Mitsubishi Heavy Industries Ltd.

- Siemens AG

- Sulzer Ltd.

- VMAC Global Technology Inc

- Volkswagen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Rotary air compressors are essential components in various industries, providing consistent compressed air for pneumatic solutions in industrial settings. These compressors, which include rotary screw and rotary vane types, are widely used in sectors such as oil & gas, energy, process industries, and mining. In the oil & gas industry, rotary air compressors are crucial for powering drilling operations and oil production. In the energy industry, they are employed in power generation, particularly in gas-fired power plants. Rotary air compressors offer several advantages over reciprocating air compressors, including energy efficiency, cost-effectiveness, and oil-free compressed air. The lubrication and cooling systems in these compressors ensure optimal performance and longevity.

Furthermore, the IoT revolution has brought about significant advancements in rotary air compressor technology, enabling remote monitoring and predictive maintenance, thereby reducing downtime and electricity bills. Rotary air compressors find applications in diverse industries, including waste management, chemicals, power generation, and consumer goods, among others. The construction sector, aerospace, automation, robotics, medicine, healthcare, wind energy, solar energy, e-commerce, and logistics operations are some sectors that heavily rely on rotary air compressors for their operations.

Moreover, the rotary air compressor market is growing rapidly, driven by the demand across various industries. Portable rotary air compressors are ideal for on-the-go applications, while stationary rotary air compressors dominate in industrial facilities. These compressors come in oil-filled and oil-free variants, offering flexibility depending on the application. Oil-filled rotary air compressors are cost-effective, while oil-free rotary air compressors cater to sectors requiring clean air, such as the medical device and chemical & materials industries. The stationary segment leads in heavy-duty operations, such as those in the oil and gas industry. Key performance metrics include cubic feet per minute (CFM) and pounds per square inch (PSI). These compressors are powered by electric motors or internal combustion engines, with varying lubrication methods to meet specific operational needs.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

153 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.27% |

|

Market growth 2024-2028 |

USD 2.61 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.13 |

|

Regional analysis |

APAC, Europe, North America, Middle East and Africa, and South America |

|

Performing market contribution |

APAC at 42% |

|

Key countries |

China, US, Germany, Japan, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Atlas Copco AB, Berkshire Hathaway Inc., Curtis Toledo Inc., Deere and Co., Doosan Corp., Dover Corp., Elgi Equipments Ltd, Frank Technologies Pvt Ltd, G and E Industrial Supplies Inc, Hitachi Ltd., Ingersoll Rand Inc., KAESER KOMPRESSOREN SE, Kirloskar Pneumatic Co. Ltd., Kobe Steel Ltd., Mitsubishi Heavy Industries Ltd., Siemens AG, Sulzer Ltd., VMAC Global Technology Inc, and Volkswagen AG |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -