Semiconductor Micro Components Market Size 2024-2028

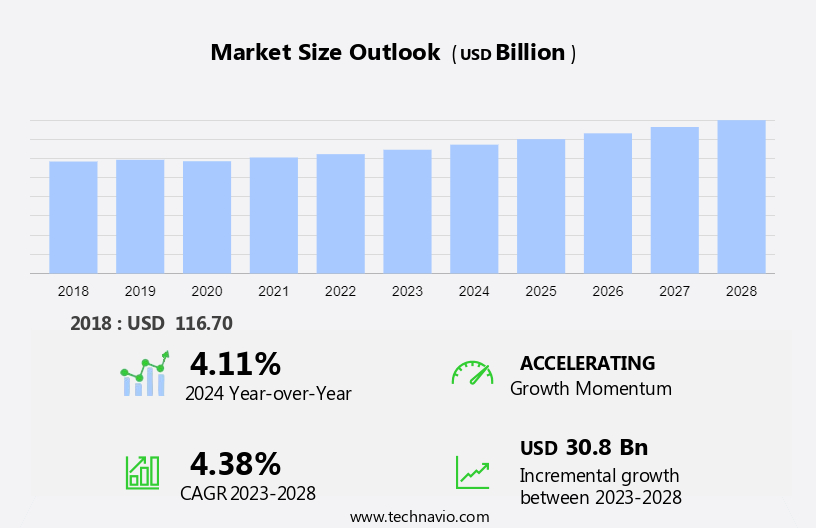

The semiconductor micro components market size is forecast to increase by USD 30.8 billion at a CAGR of 4.38% between 2023 and 2028.

- In the dynamic market, three primary growth factors are driving the industry's expansion. Firstly, the growth in new product development, fueled by continuous innovation and technological advancements, is significantly contributing to market growth. Secondly, the increased proliferation of the Internet of Things (IoT) is leading to an escalating demand for semiconductor micro components, as these devices rely on advanced micro components for efficient data processing and connectivity. The semiconductor components market is fuelled by the digital transformation in industries, including healthcare, where advanced medical devices and diagnostic equipment require high precision and efficiency. Semiconductor microcomponents are essential for smart manufacturing, control systems, and sensor integration, enabling the Internet of Things (IoT) to expand across various industries. Lastly, the demand for miniaturization in various industries, including consumer electronics and automotive, is propelling the market forward, as smaller, more efficient components are increasingly preferred. These trends, coupled with the challenges of maintaining cost competitiveness and ensuring product reliability, present both opportunities and obstacles for market participants.

What will be the Size of the Semiconductor Micro Components Market During the Forecast Period?

- The market encompasses intricate devices that play a crucial role in various sectors, including electronics, telecommunications, consumer electronics, wearable devices, and automotive electronics. Semiconductor components are essential for miniaturized, energy-efficient devices such as Smart phones, Laptops, Automated door locks, Coffee makers, GPS enabled pet trackers, and Mobile phones. The market is driven by the increasing demand for energy efficiency and the integration of Artificial Intelligence (AI) in various applications. Semiconductor Manufacturers face pricing pressures and profit margin challenges due to the intense competition In the market. Energy Efficiency is a significant factor In the market's growth, as consumers demand longer battery life and reduced power consumption.

- Semiconductor Security is another critical concern, with vulnerabilities in devices posing a threat to data privacy and security. Analog Devices are a vital segment of the market, providing solutions for signal processing, power management, and connectivity. Obstacles to market growth include the complex manufacturing process and the high cost of advanced semiconductor technology. Despite these challenges, the market is expected to continue its expansion due to the increasing demand for advanced technology in various industries.

How is this Semiconductor Micro Components Industry segmented and which is the largest segment?

The semiconductor micro components industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Microprocessors

- Microcontrollers

- Digital signal processors

- End-user

- Consumer electronics

- Defense

- Automotive

- Industrial

- Geography

- APAC

- China

- Japan

- South Korea

- North America

- US

- Europe

- South America

- Middle East and Africa

- APAC

By Product Insights

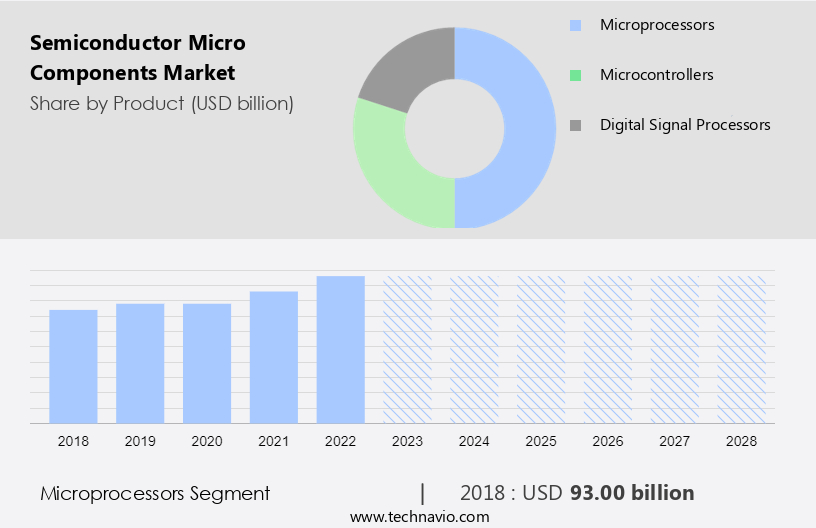

- The microprocessors segment is estimated to witness significant growth during the forecast period.

The semiconductor microcomponents market encompasses intricate semiconductor devices that play a pivotal role In the electronics industry. These components, including microprocessors made of Silicon, germanium, GaAs, and other microelectronic materials, contain millions of miniaturized transistors, diodes, and resistors. Semiconductor microcomponents are integral to various sectors, such as automotive, consumer electronics, and industrial applications. In the automotive industry, semiconductor microcomponents enable advanced driver-assistance systems (ADAS), electric vehicles (EVs), and in-car connectivity. In consumer electronics, these components power tablets, wearable devices, and communication devices, enhancing processing power, sensor integration, and communication capabilities. Real-time data processing is crucial in various sectors, such as telecommunications, where 5G technology and networks offer increased data speeds, low latency, and network capacity through communication modules and RF communication.

The growing popularity of communication devices, such as smartphones and tablets, and the increasing adoption of IoT are expected to drive market growth during the forecast period. However, the market may be affected by the declining sales of PCs and the shift towards mobile devices. Hence, the semiconductor microcomponents market is a dynamic and evolving industry that plays a vital role in powering various sectors, from automotive and consumer electronics to healthcare and telecommunications. The increasing demand for miniaturized, advanced semiconductor devices with high processing power, sensor integration, and communication capabilities will continue to drive market growth.

Get a glance at the market report of share of various segments Request Free Sample

The microprocessors segment was valued at USD 93.00 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

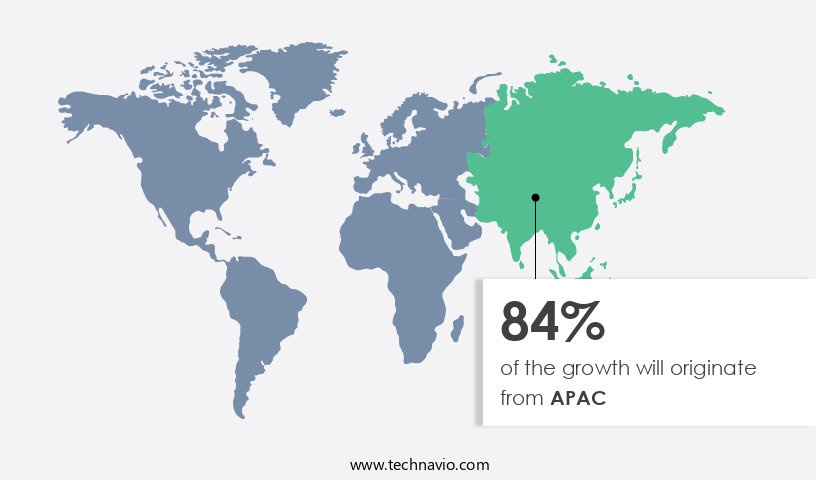

- APAC is estimated to contribute 84% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market encompasses a wide range of technologically advanced devices, including microprocessors and microcontrollers, that are integral to various electronic applications. Gallium nitride (GaN) semiconductors, in particular, have gained significant attention due to their high power density and switching speeds. These properties make GaN semiconductors ideal for use in Automotive Electronics, Artificial Intelligence (AI), and Energy Efficiency applications. Semiconductor Manufacturers face pricing pressures and profit margin constraints in this competitive landscape. The market is characterized by the development and integration of semiconductor security features to mitigate vulnerabilities. Key players in this market include Analog Devices, among others. Obstacles to market growth include power consumption concerns and the need for VLSI technology and technologically advanced DSPs.

The market spans various sectors, including Televisions, Air conditioners, Cellular standards, IoT components, and Defense. Semiconductor devices are essential components in Smart phones, Laptops, Automated door locks, Coffee makers, GPS-enabled pet trackers, Mobile phones, and numerous other electronic devices. The Average offering price for semiconductor micro components is a critical factor influencing market dynamics. As the demand for energy efficiency and technologically advanced features continues to grow, the market is expected to witness significant expansion. However, the increasing complexity of semiconductor devices and the need for continuous innovation pose challenges for market participants.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Semiconductor Micro Components Industry?

Increase in new product development is the key driver of the market.

- The semiconductor microcomponents market encompasses the production and sale of intricate semiconductor devices, including those used in electronics, automotive, and consumer electronics sectors. With the proliferation of technology, the demand for semiconductor microcomponents has grown, driven by the introduction of various electronic devices such as tablets, wearable devices, and advanced driver-assistance systems in automobiles. This trend is particularly notable In the automotive industry, where miniaturized semiconductor components are integral to electric vehicles (EVs), in-car connectivity, and processing power for advanced driver-assistance systems. Moreover, semiconductor components play a pivotal role In the digital transformation of industries, including healthcare, where precision and efficiency are paramount.

- Advanced medical devices and diagnostic equipment rely on semiconductor microcomponents for sensor integration, communication capabilities, real-time data processing, and control systems. In the telecommunications industry, semiconductor microcomponents, such as communication modules, RF components, and transistors, are essential for 5G technology and networks, enabling data speeds, low latency, and network capacity. Semiconductor microcomponents are manufactured using various materials, including Silicon, germanium, and GaAs, and encompass a wide range of microelectronic devices, including transistors and diodes. The continuous investment in research and development by semiconductor components manufacturers has led to the launch of several new products, further fueling the market's growth. The semiconductor microcomponents market is poised for significant expansion, as the demand for advanced sensor integration, communication capabilities, and real-time data processing continues to increase across various industries.

What are the market trends shaping the Semiconductor Micro Components Industry?

Increased proliferation of IoT is the upcoming market trend.

- The semiconductor microcomponents market encompasses the production and distribution of intricate semiconductor devices essential to various sectors, including electronics, automotive, and consumer electronics. These microcomponents are integral to the functioning of tablets, wearable devices, advanced driver-assistance systems in EVs, and in-car connectivity. With the increasing demand for miniaturized and advanced semiconductor components, the need for high processing power, sensor integration, and communication capabilities has become paramount. Semiconductor microcomponents play a pivotal role in enabling real-time data processing, digital transformation, and connectivity in industries such as healthcare, with applications in advanced medical devices and diagnostic equipment. In the automotive sector, semiconductor components are crucial for the development of electric vehicles, enabling efficient power management and communication between various vehicle systems.

- The telecommunications industry's digital transformation relies heavily on semiconductor microcomponents, with 5G technology and networks requiring high data speeds, low latency, and increased network capacity. Communication modules, such as RF communication devices, are essential components In the development of 5G networks, utilizing materials like Silicon, germanium, and GaAs In the production of microelectronic devices, including transistors and diodes. Semiconductor microcomponents are indispensable In the creation of microelectronic devices, enabling the miniaturization of components and the integration of sensors and control systems into communication devices. The semiconductor components market is expected to grow significantly due to the increasing demand for precision, efficiency, and connectivity in various industries.

What challenges does the Semiconductor Micro Components Industry face during its growth?

Increased demand for miniaturization is a key challenge affecting the industry growth.

- The semiconductor microcomponents market encompasses intricate devices that play a pivotal role in various sectors, including electronics, automotive, and consumer electronics. With the advent of compact gadgets, such as smartphones, tablets, and wearable devices like smartwatches, the demand for miniaturized semiconductor components has grown. Advanced driver-assistance systems (ADAS), electric vehicles (EVs), in-car connectivity, and precision control systems In these devices necessitate high processing power, sensor integration, and communication capabilities. In the automotive industry, semiconductor microcomponents are integral to the development of advanced safety features and electric powertrains. In consumer electronics, they enable real-time data processing, digital transformation, and enhanced connectivity.

- The telecommunications industry's transition to 5G technology and networks necessitates the production of communication modules, RF components, and microelectronic devices, such as transistors and diodes, made from materials like Silicon, germanium, and GaAs. The manufacturing of these semiconductor components requires significant investments in advanced equipment and increased budgets to produce intelligent systems. Rapid technological advances in areas like sensor integration, control systems, and communication devices necessitate constant updates to meet evolving consumer requirements. This investment in research and development can impact profitability but is essential for staying competitive In the market.

Exclusive Customer Landscape

The semiconductor micro components market forecasting report includes the adoption lifecycle of the market,market growth and forecasting, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the semiconductor micro components market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, semiconductor micro components market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- ADVACAM Oy

- Advanced Micro Devices Inc.

- Allegro MicroSystems Inc.

- Analog Devices Inc.

- Hendon Semiconductors

- Infineon Technologies AG

- Micro Hybrid Components

- Microchip Technology Inc.

- Micron Technology Inc.

- Nichia Corp.

- NXP Semiconductors NV

- Panasonic Holdings Corp.

- Renesas Electronics Corp.

- Samsung Electronics Co. Ltd.

- Seoul Semiconductor Co. Ltd.

- STMicroelectronics International N.V.

- Texas Instruments Inc.

- Toshiba Corp.

- Utmel Electronics

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is a significant sector In the electronics industry. These components play a crucial role in various applications, including consumer electronics, automotive, healthcare, and industrial automation. Semiconductor micro components are integral to the functioning of electronic devices, enabling features such as signal conditioning, power management, and data conversion. The market for semiconductor micro components is driven by the increasing demand for miniaturization and automation in various industries. The growing adoption of advanced technologies like IoT, AI, and machine learning is also fueling the market's growth. Additionally, the development of new materials and manufacturing processes is expected to provide opportunities for market expansion.

Semiconductor micro components are available in various types, including sensors, actuators, capacitors, and transistors. These components are used in various applications, such as temperature sensing, pressure sensing, and power management. The market for semiconductor micro components is competitive, with several players offering a wide range of products and solutions. Hence, the market is a dynamic and growing sector, driven by the increasing demand for advanced electronics in various industries. The market is expected to continue its growth trajectory, driven by technological advancements and the increasing adoption of electronics in various applications.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

190 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.38% |

|

Market growth 2024-2028 |

USD 30.8 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.11 |

|

Key countries |

China, Taiwan, US, South Korea, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Semiconductor Micro Components Market Research and Growth Report?

- CAGR of the Semiconductor Micro Components industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the semiconductor micro components market growth of industry companies

We can help! Our analysts can customize this semiconductor micro components market research report to meet your requirements.

RIA -

RIA -