Sensors In Oil And Gas Market Size 2025-2029

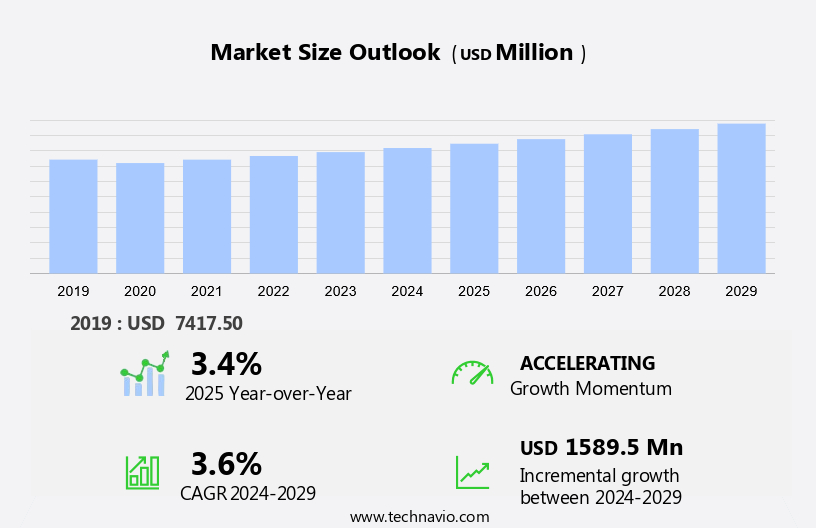

The sensors in oil and gas market size is forecast to increase by USD 1.59 billion, at a CAGR of 3.6% between 2024 and 2029.

- The market is experiencing significant growth, driven by the increasing adoption of Internet of Things (IoT) products in the industry. The integration of IoT sensors enables real-time monitoring and predictive maintenance, enhancing operational efficiency and safety. However, this market faces challenges, primarily price volatility in the oil and gas industry. This instability impacts the investment decisions of companies, making it essential to maintain a flexible business strategy. Another challenge is the increasing adoption of sensors in LNG trade, intensifying competition and necessitating continuous innovation to stay competitive.

- Companies in this market must navigate these challenges by focusing on cost optimization, technological innovation, and strategic partnerships to capitalize on the growth opportunities presented by the increasing use of IoT in the oil and gas sector.

What will be the Size of the Sensors In Oil And Gas Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2019-2023 and forecasts 2025-2029 - in the full report.

Request Free Sample

In the dynamic and evolving oil and gas market, sensors play a crucial role in production optimization and asset management. Data acquisition systems integrate various sensors, including pressure sensors, flow meters, temperature sensors, and gas detection sensors, to collect valuable data in real-time. This data is then subjected to rigorous sensor calibration, testing, and validation to ensure accuracy and reliability. Sensor interoperability and standardization are essential for seamless integration into SCADA systems and other data analytics platforms. Machine learning and deep learning algorithms enable advanced data analysis, providing insights for process control and safety and security measures. Cloud computing facilitates remote monitoring and real-time data access, enabling efficient asset management and predictive maintenance.

Vibration sensors, acoustic emission sensors, and wireless sensor networks contribute to corrosion monitoring, leak detection, and well integrity assessments. The oil and gas industry's ongoing commitment to safety and environmental stewardship drives the adoption of advanced sensor technologies for pipeline monitoring, reservoir management, and downhole sensors. Sensor certification and standardization ensure compliance with industry regulations and best practices. Sensor lifespan, sensor installation, and maintenance are critical factors in optimizing the overall performance and cost-effectiveness of these systems. Continuous innovation in sensor technology and applications across drilling operations, completion operations, and production operations ensures the industry remains at the forefront of technological advancements.

How is this Sensors In Oil And Gas Industry segmented?

The sensors in oil and gas industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Wired

- Wireless

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Spain

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

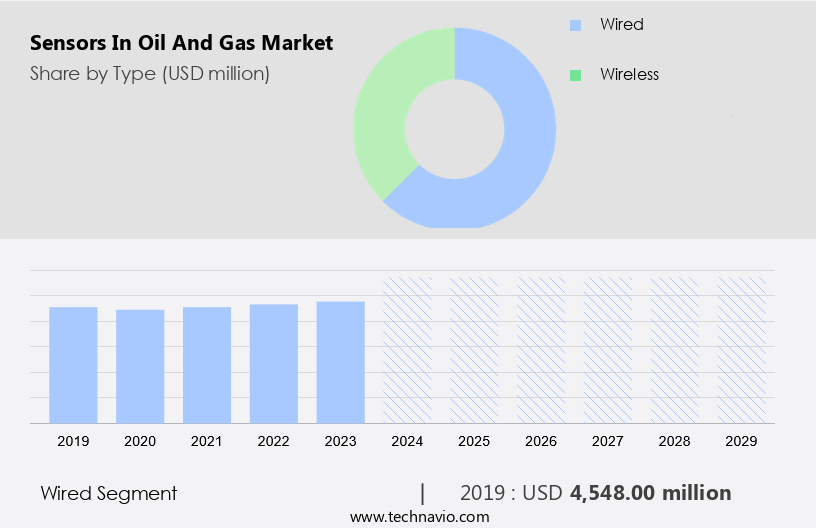

By Type Insights

The wired segment is estimated to witness significant growth during the forecast period.

The sensors market in the oil and gas industry is witnessing significant growth due to the increasing focus on production optimization and asset management. Data acquisition systems are integral to this market, with sensors playing a crucial role in collecting accurate data for analysis. Leak detection and corrosion monitoring are key applications, ensuring safety and security, while process control relies on sensor reliability and interoperability. Pressure sensors and flow meters are essential for monitoring and controlling fluid flow, with sensor accuracy a critical factor. Gas detection sensors are vital for detecting leaks and maintaining wellhead pressure.

Real-time monitoring and sensor integration are important for drilling operations, sensor validation, and completion operations. Big data and machine learning are transforming the industry, with cloud computing enabling remote monitoring and data analytics. Sensor maintenance and calibration are essential for ensuring sensor lifespan and performance. Wireless sensor networks offer flexibility, but wired sensors remain preferred in certain applications due to their high reliability and accuracy. Sensor standardization and certification are essential for ensuring compatibility and interoperability. Downhole sensors provide valuable insights into reservoir management and well integrity. Temperature sensors and vibration sensors are crucial for monitoring equipment performance and detecting anomalies.

Corrosion monitoring is essential for maintaining pipeline integrity and preventing costly downtime. Safety and security are paramount, with sensors playing a vital role in detecting potential hazards and ensuring compliance. SCADA systems and production operations rely on sensors for real-time data, enabling proactive maintenance and optimization. In conclusion, the sensors market in the oil and gas industry is evolving, driven by the need for accurate data and efficient operations. From drilling to refining, sensors are essential for monitoring and controlling various processes, ensuring safety, efficiency, and profitability.

The Wired segment was valued at USD 4.55 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

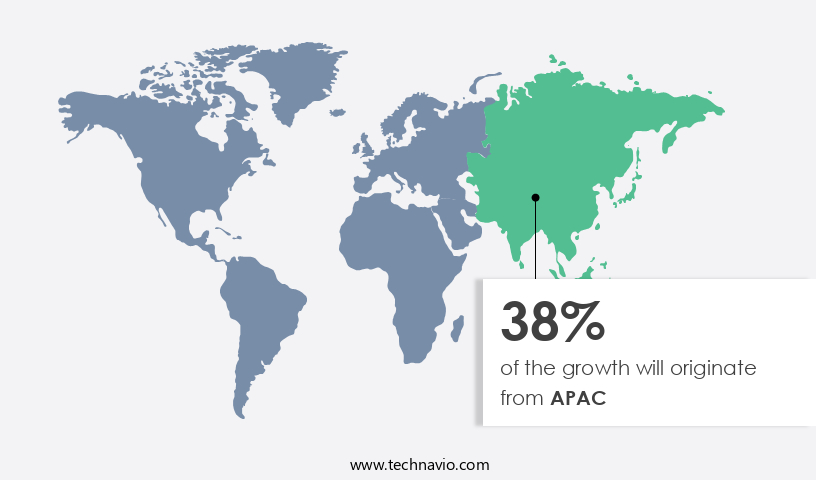

APAC is estimated to contribute 38% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

In the oil and gas industry, sensors play a crucial role in optimizing production and managing assets. The market for sensors in this sector is witnessing significant growth, particularly in the Asia-Pacific (APAC) region. Driven by the increasing adoption of industrial automation in countries like India and China, APAC is leading the global market. The demand for consumer goods and transportation fuel in the region has resulted in increased investments in refineries. Countries such as China, India, Vietnam, Indonesia, and Malaysia are planning or constructing refinery projects. Data acquisition systems, including pressure sensors, flow meters, temperature sensors, and gas detection sensors, are integral to production optimization and process control.

Leak detection and corrosion monitoring sensors ensure safety and security. Sensor calibration, testing, and integration are essential for maintaining accuracy and reliability. Real-time monitoring, machine learning, and artificial intelligence are revolutionizing data analytics. Sensor interoperability, standardization, and certification are critical for seamless integration into SCADA systems and wireless sensor networks. Downhole sensors and wellhead sensors provide valuable data for reservoir management and completion operations. Vibration sensors and acoustic emission sensors are essential for monitoring pipeline integrity and drilling operations. Cloud computing and big data are transforming the industry by enabling remote monitoring, environmental monitoring, and sensor maintenance. Data security is a growing concern, with machine learning and deep learning algorithms used for sensor validation and anomaly detection.

Sensor lifespan and sensor installation are essential considerations for cost-effective and efficient operations.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Sensors In Oil And Gas Industry?

- The LNG (Liquified Natural Gas) trade sector is experiencing significant growth and serves as the primary catalyst for market expansion.

- The Sensors market in the Oil and Gas industry is witnessing significant growth due to the increasing demand for real-time monitoring during completion operations and production processes. The integration of advanced technologies like Artificial Intelligence (AI) and SCADA systems is driving the market's growth. Temperature sensors and acoustic emission sensors are widely used for monitoring the operational parameters of oil and gas wells. Sensor certification is crucial to ensure accuracy and reliability, especially in harsh environmental conditions. Moreover, remote monitoring and environmental monitoring are essential for reservoir management and efficient production. The market's dynamics are influenced by several factors, including the need for sensor maintenance and the increasing focus on automation.

- The Oil and Gas industry's shift towards digitalization and the integration of advanced technologies are expected to create new opportunities for sensor manufacturers. In conclusion, the Oil and Gas Sensors market's growth is driven by the need for real-time monitoring, increasing demand for clean energy, and the integration of advanced technologies. The market's dynamics are influenced by factors like sensor maintenance, environmental monitoring, and automation. Proper certification and calibration of sensors are crucial to ensure their accuracy and reliability. The market's future looks promising, with several opportunities for growth in the coming years.

What are the market trends shaping the Sensors In Oil And Gas Industry?

- The IoT market is experiencing significant growth as more businesses and consumers adopt Internet of Things products. This trend is expected to continue, making the IoT sector an increasingly important and dynamic industry.

- In the oil and gas sector, IoT-enabled sensors play a crucial role in ensuring operational efficiency and safety. These sensors, which primarily measure pressure, level, flow, and temperature, are essential for applications such as remote monitoring, condition monitoring, and analysis and simulation. With the growing adoption of unconventional drilling techniques, the demand for liquid-level sensors is particularly high in the upstream industry. According to the US Bureau of Labor Statistics, accidents during drilling and exploration activities accounted for approximately 40% of all work-related fatalities in the country. Consequently, the demand for reliable and accurate sensors to prevent such incidents is increasing.

- Furthermore, advancements in technologies such as cloud computing, machine learning (ML), and deep learning enable real-time data analysis and predictive maintenance, enhancing the overall performance of the sensors. Corrosion sensors and wellhead sensors are other types of sensors gaining popularity due to their ability to monitor pipeline conditions and prevent leaks. Data security is a significant concern in the oil and gas industry, and the integration of sensors with ML and deep learning algorithms can help ensure data privacy and integrity.

What challenges does the Sensors In Oil And Gas Industry face during its growth?

- The oil and gas industry faces significant growth challenges due to the volatile pricing trend, which is a prominent issue in this sector.

- The oil and gas industry's price volatility poses a significant challenge to the global sensors market. Fluctuating oil prices can disrupt investment plans, leading to delays or cancellations of sensor deployment projects. For instance, when oil prices decrease, oil companies may reduce exploration and production activities, subsequently decreasing the demand for sensors used in these operations. Conversely, when prices surge, there is a rush to ramp up production, which can strain the sensor supply chain and technology availability. This volatility also impacts the financial stability of oil and gas companies, making it challenging for them to commit to long-term investments in advanced sensor technologies.

- Production optimization and asset management are crucial applications of sensors in the oil and gas industry. Data acquisition systems, including pressure sensors, flow meters, and gas detection sensors, play a vital role in these applications. Sensor calibration, testing, and integration are essential to ensure sensor accuracy and reliability. Data analytics enables oil and gas companies to make informed decisions based on real-time data from these sensors. Despite the challenges, the market for sensors in the oil and gas industry is expected to grow due to the increasing demand for improved operational efficiency and safety.

Exclusive Customer Landscape

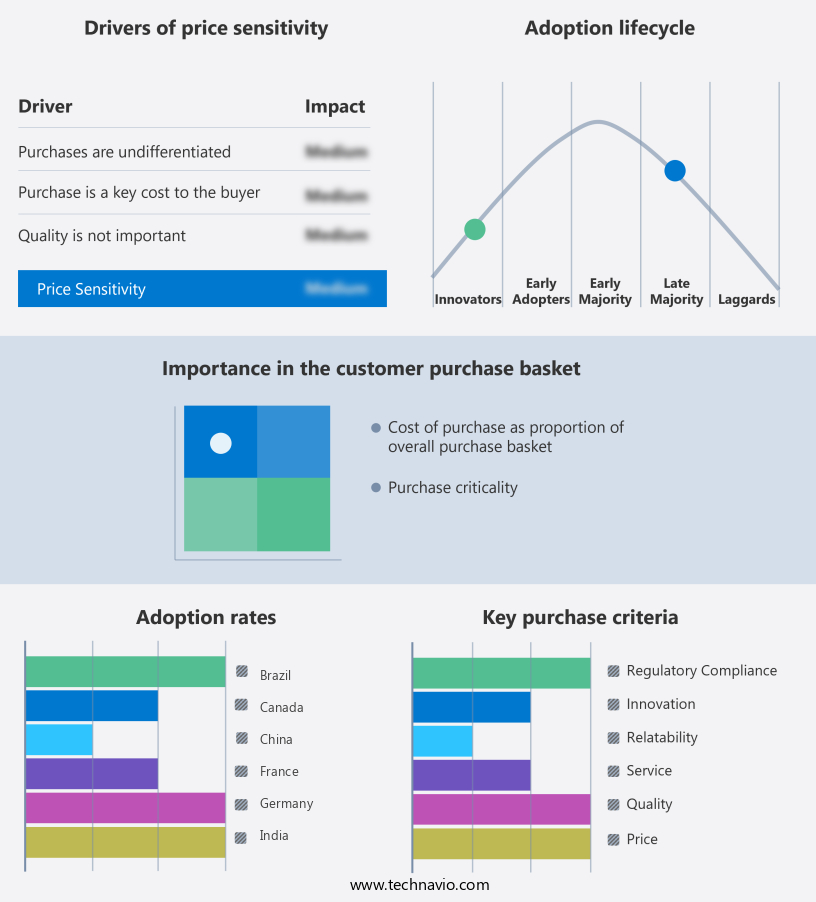

The sensors in oil and gas market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the sensors in oil and gas market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, sensors in oil and gas market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB - The company specializes in providing advanced sensor solutions, encompassing products like the LMS 7100, MS10, and MS 50. These sensors are designed to enhance operational efficiency and accuracy across various industries. With cutting-edge technology and rigorous quality standards, our offerings ensure reliable performance and data collection. By integrating these sensors into systems, businesses can optimize processes, minimize downtime, and make informed decisions based on real-time data. Our commitment to innovation and excellence sets us apart in the sensor market.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB

- Amphenol Corp.

- Automation Products Inc.

- BD SENSORS GmbH.

- Carlo Gavazzi

- Edinburgh Instruments Ltd.

- Emerson Electric Co.

- Endress Hauser Group Services AG

- Figaro Engineering Inc.

- Fortive Corp.

- Gas Sensing Solutions Ltd.

- General Electric Co.

- Honeywell International Inc.

- LORD Corp.

- Robert Bosch GmbH

- Rockwell Automation Inc.

- RS Technics BV

- Siemens AG

- TE Connectivity Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Sensors In Oil And Gas Market

- In February 2023, Honeywell announced the launch of its new Ultra-Low Power Gas Sensor, designed to enhance the detection capabilities of methane leaks in oil and gas operations. This innovative sensor is expected to reduce false positives and improve overall efficiency by up to 50% (Honeywell press release).

- In May 2024, Schneider Electric and ABB entered into a strategic partnership to jointly develop and market advanced sensing technologies for the oil and gas industry. This collaboration aims to combine Schneider Electric's EcoStruxure platform with ABB's Ability⢠Oil and Gas solution, providing integrated and efficient process control systems (Schneider Electric press release).

- In October 2024, Emerson acquired Aventics, a leading provider of pneumatic components and automation technologies. This acquisition is expected to strengthen Emerson's position in the oil and gas market by expanding its portfolio of pressure control solutions and enhancing its digital transformation capabilities (Emerson press release).

- In January 2025, the US Department of Energy announced a USD100 million investment in the development of advanced sensors for oil and gas operations. This initiative aims to improve operational efficiency, reduce emissions, and ensure safety in the industry (US Department of Energy press release).

Research Analyst Overview

- In the oil and gas industry, inductive sensors play a crucial role in environmental compliance by monitoring fluid levels and detecting leaks. ISO standards and industry regulations mandate the use of these sensors to ensure operational efficiency and adherence to regulations. Cellular networks and satellite communication enable real-time alerts and notifications for fault detection and risk assessment. Nanotechnology sensors, including MEMS, optical, electrochemical, piezoelectric, and capacitive sensors, offer enhanced accuracy and cost optimization. Furthermore, fieldbus protocols such as Foundation Fieldbus, Profibus, and Modbus, as well as Ethernet/IP and HART protocols, facilitate seamless data exchange and analysis.

- Historical data analysis and trend analysis are essential for cost optimization and root cause identification. Wireless communication protocols enable remote monitoring and control, while IEC standards ensure interoperability and safety. ISO and IEC standards continue to evolve, driving innovation in sensor technology and integration with advanced data visualization tools. Root cause analysis and risk assessment are critical components of proactive maintenance strategies, reducing downtime and improving overall operational efficiency.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Sensors In Oil And Gas Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

166 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.6% |

|

Market growth 2025-2029 |

USD 1589.5 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

3.4 |

|

Key countries |

US, China, Japan, Germany, UK, India, Canada, France, Brazil, and Spain |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Sensors In Oil And Gas Market Research and Growth Report?

- CAGR of the Sensors In Oil And Gas industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the sensors in oil and gas market growth of industry companies

We can help! Our analysts can customize this sensors in oil and gas market research report to meet your requirements.

RIA -

RIA -