Smart Stadium Market Size 2026-2030

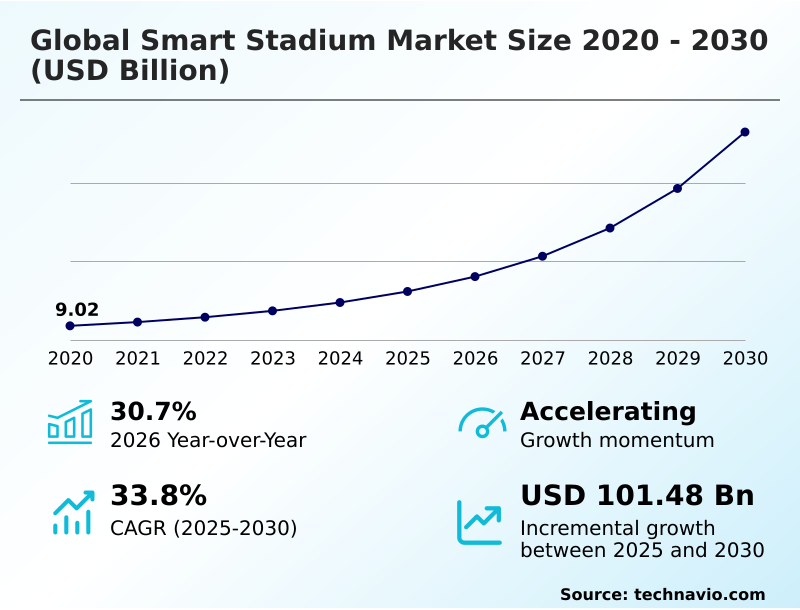

The smart stadium market size is valued to increase by USD 101.48 billion, at a CAGR of 33.8% from 2025 to 2030. Improved operational efficiency will drive the smart stadium market.

Major Market Trends & Insights

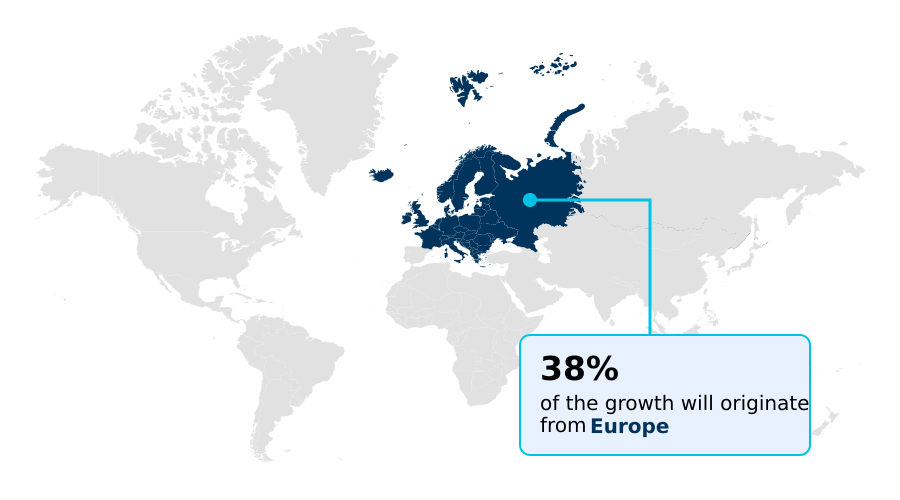

- Europe dominated the market and accounted for a 37.6% growth during the forecast period.

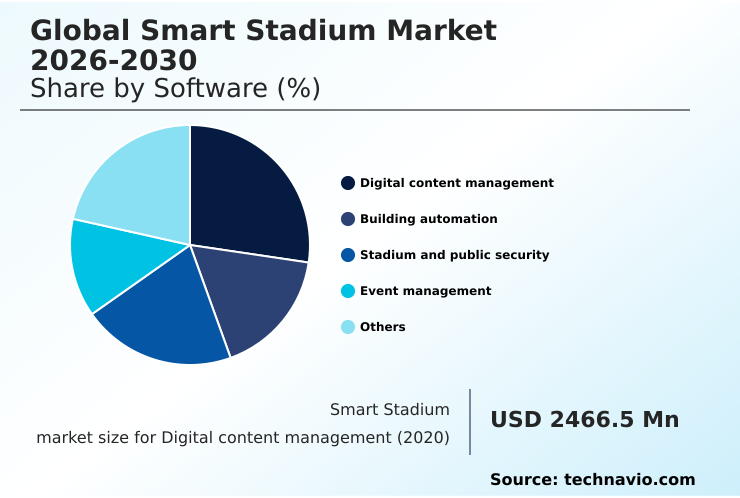

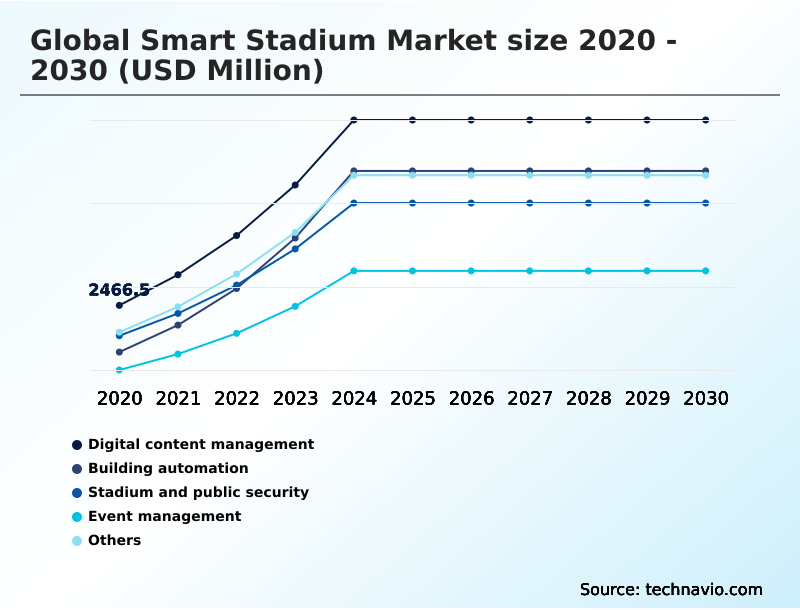

- By Software - Digital content management segment was valued at USD 6.11 billion in 2024

- By Deployment - On-premises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 123.33 billion

- Market Future Opportunities: USD 101.48 billion

- CAGR from 2025 to 2030 : 33.8%

Market Summary

- The smart stadium market is undergoing a significant transformation, driven by the need for enhanced spectator experiences and operational efficiency. The integration of advanced technologies such as high-density Wi-Fi, 5G small cells, and IoT sensors is becoming standard. These technologies facilitate a range of services from augmented reality overlays to real-time data analytics, creating a deeply engaging environment for fans.

- For instance, a venue can use its integrated building management platform not only for climate control systems but also to analyze foot traffic, redirecting fans to less crowded concession stands and improving sales flow. However, the market is not without its challenges.

- The high initial capital required for deploying a digital twin management system or comprehensive AI-based security can be prohibitive. Furthermore, the increasing reliance on connected systems introduces significant cybersecurity risks, as cashless payments and biometric identification systems become prime targets for data breaches.

- Balancing innovation with robust security and managing the substantial upfront costs are critical considerations for stakeholders navigating this dynamic landscape.

What will be the Size of the Smart Stadium Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Smart Stadium Market Segmented?

The smart stadium industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Software

- Digital content management

- Building automation

- Stadium and public security

- Event management

- Others

- Deployment

- On-premises

- Cloud based

- Type

- New installation

- Retrofit

- Geography

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- Europe

By Software Insights

The digital content management segment is estimated to witness significant growth during the forecast period.

The digital content management segment is pivotal for the global smart stadium market 2026-2030, transforming how information is delivered during live events.

This involves software controlling large-scale LED scoreboards, digital signage, and displays, leveraging high-performance networks to push real-time analytics and player data. The integration of augmented reality overlays enhances fan engagement, bridging the gap between at-home viewing and the live atmosphere.

Robust software architectures are required to manage high-resolution video without network instability, a key aspect of smart energy management.

Effective systems utilize big data analytics to deliver personalized advertising, with some venues reporting up to a 15% increase in ancillary revenue.

This data-driven approach, supported by high-density wi-fi and advanced audio-visual imaging, is essential for creating an immersive and profitable fan journey.

The Digital content management segment was valued at USD 6.11 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 37.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Smart Stadium Market Demand is Rising in Europe Get Free Sample

The geographic landscape of the global smart stadium market 2026-2030 is characterized by varied growth rates and technological priorities across regions.

Europe leads in market share, contributing over 37% of the incremental growth, driven by stringent sustainability regulations and the modernization of historic venues with technologies like connected LED lighting systems.

North America follows, with a strong focus on enhancing the fan experience through high-density Wi-Fi and 5G advanced networks. The region's growth is steady, though slightly behind Europe's.

Notably, APAC is projected to be the fastest-growing region, with a CAGR of 35.3%, significantly higher than North America's 33.3%.

This expansion is fueled by new constructions in countries like China and Japan, which integrate advanced audio-visual imaging and AI-based security from the ground up, leveraging technologies like the NVIDIA metropolis platform and robust real-time analytics to create futuristic entertainment hubs.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic investment in the global smart stadium market 2026-2030 is increasingly focused on specialized applications that deliver tangible returns on investment and enhance venue functionality. For instance, AI in stadium crowd control management is becoming critical for ensuring safety and optimizing foot traffic, which directly correlates with higher concession sales.

- Similarly, the use of a digital twin for predictive maintenance in stadiums is gaining traction, as it allows operators to preemptively address equipment failures, reducing downtime and costly emergency repairs. While the market for AR applications for live sports events continues to grow, its adoption is closely tied to the rollout of robust 5G connectivity for an enhanced spectator experience.

- The implementation of IoT sensor networks for venue management provides the foundational data for these advanced systems, enabling everything from smart energy management to dynamic pricing. However, cybersecurity challenges in smart stadiums remain a significant concern, with the cost of mitigating a single data breach often surpassing the initial investment in security infrastructure.

- The market for smart stadium operational efficiency improvements is expanding more than twice as fast as the market for basic connectivity upgrades, highlighting a shift from foundational infrastructure to value-added analytics and automation. Organizations that successfully navigate these complexities by integrating comprehensive security with fan-centric technologies will be best positioned for success.

What are the key market drivers leading to the rise in the adoption of Smart Stadium Industry?

- Improved operational efficiency through automation and real-time data is a key driver for the market, enabling significant cost savings and streamlined venue management.

- The primary drivers of the global smart stadium market 2026-2030 are improved operational efficiency and the rising demand for an enhanced spectator experience.

- Venues are implementing integrated building management platforms to streamline operations, with some achieving a 25% reduction in energy costs through AI-driven smart lighting and climate control systems. This efficiency extends to staffing and maintenance, where predictive maintenance sensors minimize downtime.

- Concurrently, the deployment of 5G advanced networks is enabling unparalleled fan engagement through services like in-seat ordering and real-time player statistics.

- This push for a hyper-connected environment, supported by cloud-based data analytics, not only increases fan satisfaction but also creates new revenue streams, making technology investment a critical competitive differentiator.

What are the market trends shaping the Smart Stadium Industry?

- The emergence of augmented reality in stadiums is a significant market trend, transforming the spectator experience by overlaying digital information onto the physical environment.

- Key trends in the global smart stadium market 2026-2030 are centered on data-driven experiences and operational intelligence. The growing adoption of big data analytics allows venues to move beyond simple crowd counting to predictive modeling, with some facilities leveraging an Oracle sports analytics cloud to boost secondary spending by 15%.

- This is complemented by the emergence of augmented reality (AR) in stadiums, where stadium-integrated landmarkers are used by over 60% of fans for interactive experiences. These innovations are powered by high-density Wi-Fi and advanced audio-visual imaging, enabling real-time analytics and personalized content delivery.

- Furthermore, the increasing use of artificial intelligence is transforming back-end systems like smart energy management and front-end services, creating a more responsive and efficient venue.

What challenges does the Smart Stadium Industry face during its growth?

- The high initial investment required for a comprehensive overhaul of physical and digital infrastructure remains a key challenge affecting industry growth.

- Significant challenges constrain the global smart stadium market 2026-2030, led by high initial investment and complex data security issues. The capital required for a comprehensive digital twin management system, including thousands of IoT sensors and 5G small cells, can be prohibitive.

- Beyond hardware, integrating disparate systems and ensuring robust cybersecurity for features like cashless payments and biometric identification adds considerable expense. Data privacy is a major hurdle, as the collection of personal information makes venues high-value targets for cyberattacks.

- A single security breach can lead to significant financial loss and reputational damage, with targeted ransomware attacks causing operational downtime to increase by over 18% in affected facilities, complicating the path to digital transformation.

Exclusive Technavio Analysis on Customer Landscape

The smart stadium market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the smart stadium market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Smart Stadium Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, smart stadium market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Cisco Systems Inc. - Cisco Systems Inc. delivers smart stadium solutions, offering high-density Wi-Fi connectivity, secure networking, and real-time analytics to support enhanced digital fan services.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Cisco Systems Inc.

- Daktronics Inc.

- GP Smart Stadium

- Honeywell International Inc.

- Johnson Controls International

- NEC Corp.

- Nippon Telegraph and Corp.

- Nokia Corp.

- Oracle Corp.

- PARTTEAM and OEMKIOSKS

- Samsung Electronics Co. Ltd.

- SAP SE

- Schneider Electric SE

- Siemens AG

- Signify NV

- SKIDATA AG

- Sony Group Corp.

- Sunrise Communications AG

- Tech Mahindra Ltd.

- Telefonaktiebolaget Ericsson

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Smart stadium market

- In March, 2025, Schneider Electric reported that a major European football arena using its integrated building management platform achieved a 25% reduction in energy costs by leveraging AI-driven sensors to manage electricity loads.

- In August, 2025, T-Mobile USA highlighted the impact of its 5G Advanced network, detailing how new in-seat augmented reality features allowed fans to see player stats in real-time, increasing fan engagement scores.

- In April, 2025, Oracle published a report on how the Golden State Warriors utilized its Sports Analytics Cloud to analyze fan movement, leading to optimized merchandise placement and a 15% increase in secondary spending.

- In May, 2025, Fortinet released an analysis on the cybersecurity threat landscape for large public venues, identifying a significant rise in ransomware attempts targeting the integrated networks of major sports facilities.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Smart Stadium Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 305 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 33.8% |

| Market growth 2026-2030 | USD 101476.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 30.7% |

| Key countries | Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The global smart stadium market 2026-2030 is defined by the deep integration of digital infrastructure to create intelligent, responsive environments. Core technologies such as high-density Wi-Fi, 5G small cells, and ubiquitous IoT sensors are no longer optional but foundational, enabling advanced functionalities like biometric identification and real-time data analytics.

- The deployment of AI-based security and facial recognition is becoming standard for access control and threat detection. Venues are leveraging edge computing to process vast amounts of data locally, which is crucial for applications like augmented reality overlays and cashless payments that require minimal latency. For boardroom consideration, the adoption of these technologies directly impacts revenue and risk management.

- For example, the successful implementation of interactive AR features has been shown to increase fan engagement, with some venues reporting that over 60% of attendees use such features during an event.

- This highlights a clear path to monetization, though it must be balanced with investment in a digital twin management system for operational oversight, predictive maintenance sensors to ensure uptime, and robust cybersecurity to protect the entire ecosystem, from building automation and smart lighting to sensitive fan data.

What are the Key Data Covered in this Smart Stadium Market Research and Growth Report?

-

What is the expected growth of the Smart Stadium Market between 2026 and 2030?

-

USD 101.48 billion, at a CAGR of 33.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Software (Digital content management, Building automation, Stadium and public security, Event management, and Others), Deployment (On-premises, and Cloud based), Type (New installation, and Retrofit) and Geography (Europe, North America, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Improved operational efficiency, High initial investment

-

-

Who are the major players in the Smart Stadium Market?

-

Cisco Systems Inc., Daktronics Inc., GP Smart Stadium, Honeywell International Inc., Johnson Controls International, NEC Corp., Nippon Telegraph and Corp., Nokia Corp., Oracle Corp., PARTTEAM and OEMKIOSKS, Samsung Electronics Co. Ltd., SAP SE, Schneider Electric SE, Siemens AG, Signify NV, SKIDATA AG, Sony Group Corp., Sunrise Communications AG, Tech Mahindra Ltd. and Telefonaktiebolaget Ericsson

-

Market Research Insights

- The smart stadium market is evolving through the strategic deployment of technologies that yield measurable business outcomes. The integration of a high-capacity IP networking infrastructure is now standard, enabling functionalities that directly impact profitability and operational excellence.

- For example, venues deploying an Oracle sports analytics cloud have seen secondary spending increase by as much as 15% by optimizing retail placement based on real-time crowd movement. Similarly, the adoption of smart energy management systems, often part of an integrated building management platform, has allowed some facilities to reduce energy costs by 25%.

- These advancements, supported by cloud-based data analytics and NVIDIA metropolis platform for security, demonstrate a clear shift toward data-driven decision-making, where every aspect of the fan journey and venue operation is monitored and optimized for efficiency and engagement.

We can help! Our analysts can customize this smart stadium market research report to meet your requirements.

RIA -

RIA -