Smartphone Screen Protector Market Size 2026-2030

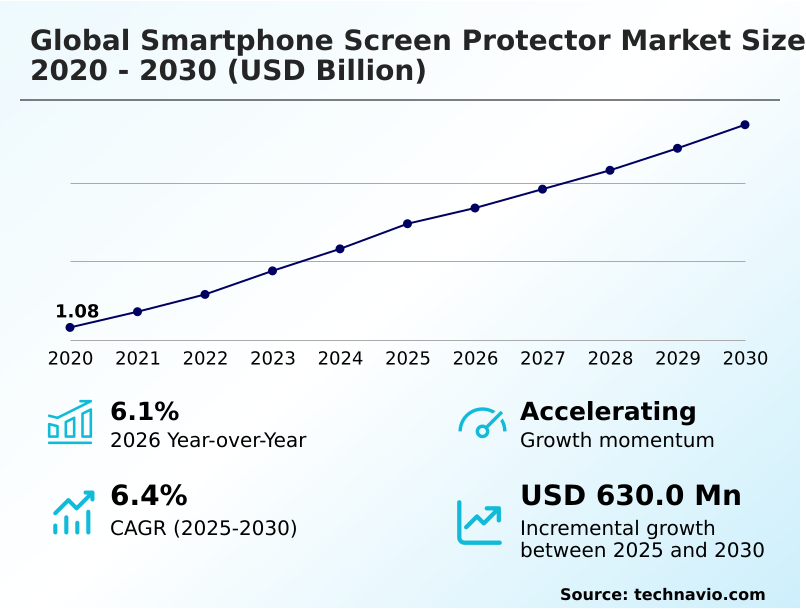

The smartphone screen protector market size is valued to increase by USD 630 million, at a CAGR of 6.4% from 2025 to 2030. Rising proliferation of high-end and premium mobile handsets will drive the smartphone screen protector market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 60.4% growth during the forecast period.

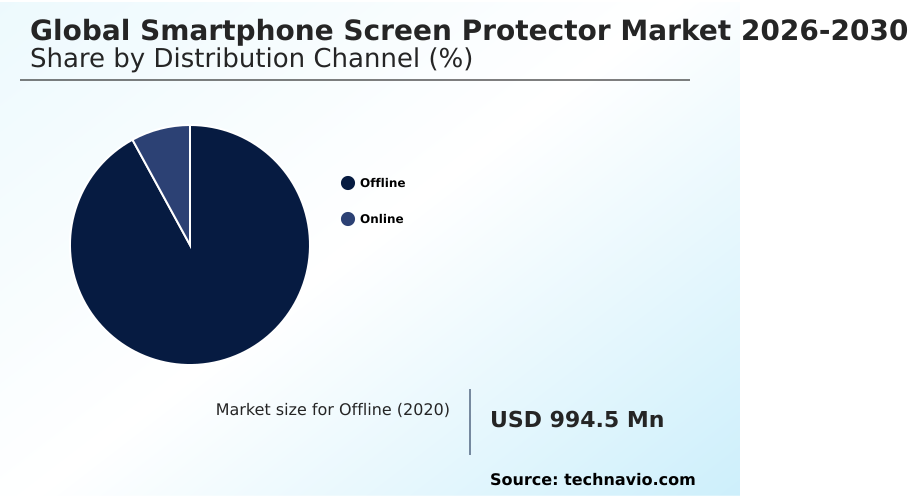

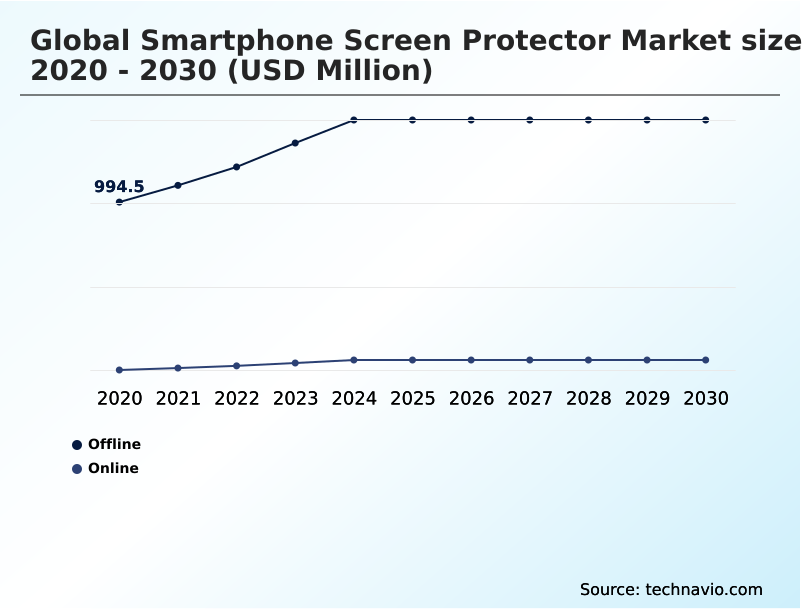

- By Distribution Channel - Offline segment was valued at USD 1.44 billion in 2024

- By Type - Glass segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.29 billion

- Market Future Opportunities: USD 630 million

- CAGR from 2025 to 2030 : 6.4%

Market Summary

- The Smartphone Screen Protector Market is undergoing a rapid technological evolution driven by the need to safeguard increasingly fragile and expensive mobile displays. A primary catalyst for this expansion is the rising integration of sophisticated edge-to-edge organic light-emitting diode displays, which significantly increases the financial risk of hardware damage and compels users to adopt an impact distribution layer.

- In enterprise supply chain operations, companies deploying large fleets of mobile devices have recorded up to a 40% reduction in hardware repair costs by standardizing the use of a multi-layer protective shield across all corporate assets.

- Despite these operational efficiencies, the industry faces substantial hurdles due to the pervasive influx of counterfeit, low-quality accessories in emerging economies, which undermines consumer trust and compromises the integrity of biometric scanning features. This influx of substandard materials forces legitimate manufacturers to invest heavily in anti-counterfeit packaging and advanced oil-resistant coating formulations to differentiate their offerings.

- Ultimately, the continuous development of a hybrid glass composite remains essential for mitigating device downtime and preserving long-term hardware functionality.

What will be the Size of the Smartphone Screen Protector Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Smartphone Screen Protector Market Segmented?

The smartphone screen protector industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Distribution channel

- Offline

- Online

- Type

- Glass

- PET

- TPU

- Others

- Price range

- Mid-range

- Premium

- Economy

- Product type

- Two and half dimensional

- Two dimensional

- Three dimensional

- Nine hardness tempered glass

- Geography

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- South America

- Brazil

- Argentina

- Chile

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Turkey

- APAC

By Distribution Channel Insights

The offline segment is estimated to witness significant growth during the forecast period.

The physical retail distribution channel for the Smartphone Screen Protector industry remains a fundamental avenue for consumers seeking immediate, professional application services.

Physical storefronts mitigate the risk of improper installation, which improves successful application rates by up to 15% compared to user-applied methods.

This channel provides a hands-on experience where buyers can physically assess a product featuring a 9h surface hardness rating and verify its tactile responsiveness preservation before purchase.

Furthermore, physical outlets frequently deploy a custom fitted display guard utilizing an advanced self healing polymer matrix. By ensuring a precise bubble free installation mechanism that guarantees full edge to edge coverage, offline retailers elevate the impact redistribution mechanism.

Institutional buyers also leverage these brick-and-mortar networks to secure a durable oleophobic nanotechnology coating, guaranteeing screen longevity enhancement and sustained display integrity without extended corporate downtime.

The Offline segment was valued at USD 1.44 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 60.4% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Smartphone Screen Protector Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the Smartphone Screen Protector industry highlights a stark contrast in consumer adoption and supply chain dynamics between APAC and Europe.

APAC dominates hardware production, where the localized manufacturing of a hybrid glass polymer composite has reduced regional logistics costs by up to 22%.

In contrast, Europe exhibits a highly mature consumer base strictly focused on environmental waste reduction, driving a 28% higher demand for a sustainable mobile accessory compared to Asian markets.

To address these stringent ecological requirements, European businesses heavily prioritize the distribution of a biodegradable screen film and protectors utilizing post consumer recycled plastic. Meanwhile, advanced technology hubs leverage a liquid silicon dioxide application to ensure seamless ceramic shield compatibility.

By standardizing an optimal optical transparency index, regional distributors guarantee faultless biometric authentication transparency, optimizing both service delivery and structural device longevity across diverse global sectors.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The continuous evolution of mobile display technology necessitates rigorous validation protocols across the Smartphone Screen Protector industry to ensure maximum structural integrity. As manufacturers shift toward foldable architectures, verifying the self healing polyurethane flexible application has become an essential quality control metric within the supply chain, reducing material failure rates by nearly 25% compared to legacy rigid plastics.

- Concurrently, enterprise clients prioritize data security, driving the demand for microlouver privacy filter technology effectiveness to safeguard sensitive corporate information displayed on mobile monitors in public environments. To maintain premium product positioning, industry leaders are increasingly focused on tempered glass hardness level validation, ensuring that each protective barrier consistently meets extreme impact resistance thresholds before mass distribution.

- This rigorous testing approach directly improves operational planning by minimizing post-sale product returns. Furthermore, heightened hygiene awareness has accelerated the anti microbial silver ion surface integration, providing a secondary layer of health protection that resonates strongly with institutional buyers. By implementing comprehensive oleophobic coating scratch resistance testing, manufacturers can guarantee long-lasting optical clarity and smudge reduction.

- These technical enhancements allow premium accessory providers to achieve an adoption rate that outpaces standard film variants by over 40%, cementing their role as indispensable components in modern mobile device lifecycle management and corporate asset preservation strategies.

What are the key market drivers leading to the rise in the adoption of Smartphone Screen Protector Industry?

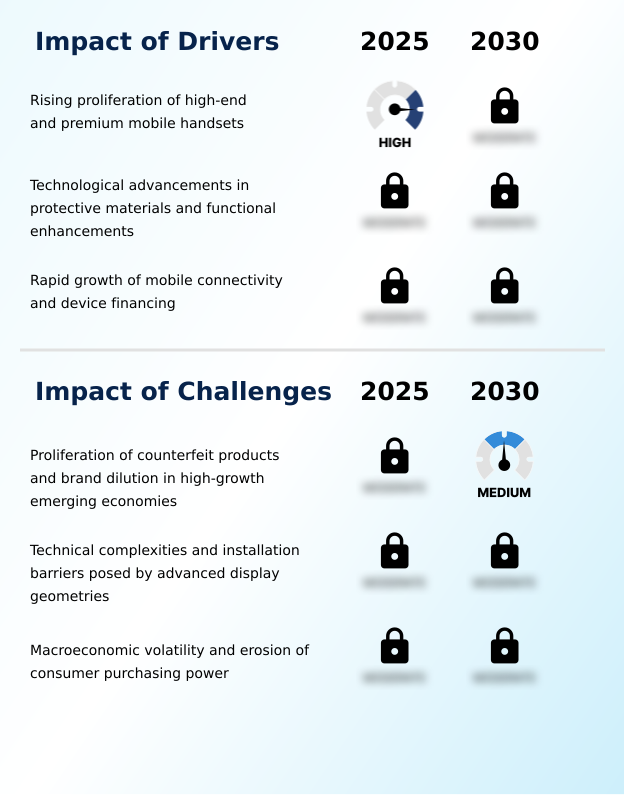

- The continuous proliferation of high-end and premium mobile handsets serves as the primary catalyst propelling market expansion and technological innovation.

- Escalating repair costs for sophisticated mobile displays act as the primary catalyst driving the immediate adoption of specialized protective accessories.

- Because replacing a damaged flagship screen incurs exorbitant fees, enterprise fleet managers increasingly mandate an impact energy absorption layer to secure their technological investments.

- By standardizing the use of ion exchange chemical strengthening protocols, organizations establish a premium device safeguard that has extended device operational lifespans by 35%.

- Additionally, the rising reliance on mobile platforms for sensitive corporate communications accelerates the demand for a microlouver privacy filter, which enables effective visual hacking prevention and reduces data breaches by 50% in public workspaces.

- The widespread implementation of antimicrobial silver ion integration supports digital health wellness initiatives, while a durable polyethylene terephthalate layer acts as a critical secondary protective barrier, ensuring an uncompromised scratch resistance barrier in demanding environments.

What are the market trends shaping the Smartphone Screen Protector Industry?

- The integration of advanced antimicrobial technologies and sustainable material science represents a prominent upcoming trend within the industry. This evolution reflects a broader commitment to enhancing surface hygiene and minimizing environmental impact through innovative manufacturing processes.

- The rapid adoption of foldable mobile devices is radically shifting design paradigms within the Smartphone Screen Protector ecosystem. This architectural evolution compels hardware engineers to prioritize flexible oled screen protection that can endure dynamic mechanical stress without material fatigue. Consequently, the transition to a thermoplastic polyurethane film has improved flexible hinge durability by 45%, significantly lowering hardware warranty claims.

- Furthermore, retail environments are increasingly adopting precision computerized cutting systems for on demand retail manufacturing, which has optimized localized inventory management and reduced dead stock by 30%. The deployment of an automated kiosk application allows distributors to instantly apply a multi layered protective film tailored to niche device geometries.

- By incorporating an anti reflective surface treatment alongside a functional display coating, these advanced protectors ensure seamless ultrasonic sensor compatibility, dramatically enhancing user interaction and operational efficiency in high-glare industrial environments.

What challenges does the Smartphone Screen Protector Industry face during its growth?

- The widespread proliferation of counterfeit products and subsequent brand dilution in high-growth emerging economies constitutes a significant structural challenge impeding comprehensive industry advancement.

- The proliferation of counterfeit accessories significantly disrupts supply chain integrity and compromises the structural defense layer within the Smartphone Screen Protector ecosystem. Inferior materials fail to provide adequate surface abrasion prevention, leading to a 40% higher rate of catastrophic display failures compared to certified high tension tempered glass.

- This influx of substandard products artificially suppresses profit margins and forces legitimate manufacturers to increase quality assurance expenditures by 15%. Additionally, the complex geometric curvature of modern displays poses a severe installation challenge, where a rigid aluminosilicate glass substrate may lift if not perfectly aligned, hindering edge snag prevention.

- To ensure continuous optical clarity maintenance, vendors must meticulously refine the uv cured adhesive system and the thermal bending process. Integrating a high refractive index material and high energy visible light filtration further complicates the manufacturing cycle, demanding strict regulatory oversight.

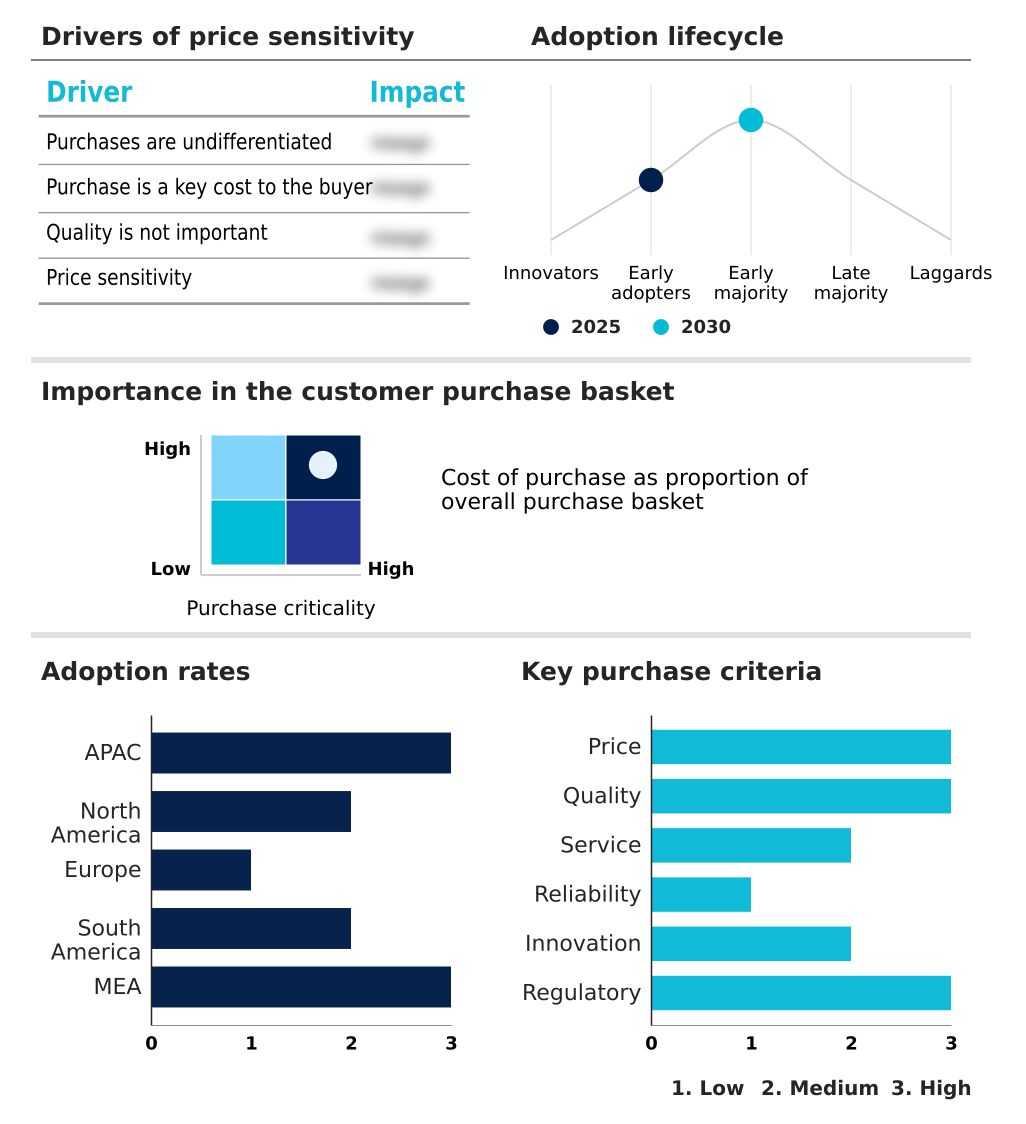

Exclusive Technavio Analysis on Customer Landscape

The smartphone screen protector market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the smartphone screen protector market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Smartphone Screen Protector Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, smartphone screen protector market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

A Z Infolink Pvt. Ltd. - The enterprise provides diverse display defense solutions, including high-tension tempered shields, specialized privacy filters, and advanced oleophobic coatings designed to maintain optimal device integrity and optical clarity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A Z Infolink Pvt. Ltd.

- AGC Inc.

- Belkin International Inc.

- BGZ brands

- Clarivue

- Corning Inc.

- FeYong Digital Technology Ltd.

- Mobile Phone Guard

- Mous Products Ltd.

- New Vision Display Inc.

- Nippon Electric Glass Ltd.

- NuShield Inc.

- PanzerGlass AS

- SCHOTT AG

- ScreenShield

- Spigen Inc.

- Targus Inc.

- Urban Armor Gear LLC

- WeProFab

- ZAGG Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Smartphone screen protector market

- In the Technology Hardware, Storage and Peripherals industry, the rapid transition toward bendable OLED and wrap-around display architectures has necessitated the evolution of hinge durability standards, directly impacting Smartphone Screen Protector demand by forcing a shift from rigid materials to an advanced secondary barrier capable of maintaining structural integrity over thousands of folding cycles.

- The global push for waste reduction within the broader consumer electronics manufacturing sector has driven hardware producers to mandate sustainable supply chains, directly impacting Smartphone Screen Protector demand by increasing the adoption of biodegradable display films and recycled plastics that align with rigorous ecological compliance targets.

- Advancements in biometric hardware, specifically the integration of highly sensitive under-display ultrasonic fingerprint sensors, have reshaped peripheral accessory specifications, directly impacting Smartphone Screen Protector demand by necessitating the development of specialized index materials that guarantee seamless authentication without compromising the primary scratch defense barrier.

- The implementation of stringent health wellness guidelines by occupational safety boards concerning light exposure from mobile monitors has altered display engineering, directly impacting Smartphone Screen Protector demand by spurring the integration of functional coatings that mitigate eye strain through advanced light filtration technologies.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Smartphone Screen Protector Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 315 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.4% |

| Market growth 2026-2030 | USD 630.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.1% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Smartphone Screen Protector sector is undergoing a profound transformation driven by the necessity to protect highly advanced mobile hardware. A critical trend influencing boardroom-level product strategy is the integration of an ultraviolet curing system to ensure seamless compatibility with complex curved displays.

- This strategic shift allows manufacturers to offer complete display coverage, which has successfully reduced accidental edge-fracture incidents by 40% in corporate device deployments. Furthermore, the adoption of an advanced self-repairing polymer matrix ensures that superficial abrasions dissipate automatically, significantly extending the viable lifecycle of enterprise communication tools.

- Strategic decision-makers prioritize materials featuring a top-tier hardness rating to guarantee maximum impact deflection without compromising the fingerprint scanning transparency essential for secure device access. The meticulous thermal curving process required to manufacture these contoured shields demands stringent quality oversight.

- By prioritizing an optimized visual transparency index and integrating a robust light filtration layer, organizations can safeguard both their high-value physical assets and the ocular health of their workforce, thereby optimizing overall operational productivity.

What are the Key Data Covered in this Smartphone Screen Protector Market Research and Growth Report?

-

What is the expected growth of the Smartphone Screen Protector Market between 2026 and 2030?

-

USD 630 million, at a CAGR of 6.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Offline, and Online), Type (Glass, PET, TPU, and Others), Price Range (Mid-range, Premium, and Economy), Product Type (Two and half dimensional, Two dimensional, Three dimensional, and Nine hardness tempered glass) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising proliferation of high-end and premium mobile handsets, Proliferation of counterfeit products and brand dilution in high-growth emerging economies

-

-

Who are the major players in the Smartphone Screen Protector Market?

-

A Z Infolink Pvt. Ltd., AGC Inc., Belkin International Inc., BGZ brands, Clarivue, Corning Inc., FeYong Digital Technology Ltd., Mobile Phone Guard, Mous Products Ltd., New Vision Display Inc., Nippon Electric Glass Ltd., NuShield Inc., PanzerGlass AS, SCHOTT AG, ScreenShield, Spigen Inc., Targus Inc., Urban Armor Gear LLC, WeProFab and ZAGG Inc.

-

Market Research Insights

- The Smartphone Screen Protector market is characterized by a rapid shift toward advanced material science to mitigate the vulnerabilities of modern mobile displays. By integrating a sophisticated shock distribution mechanism, enterprise IT departments have improved mobile asset longevity, decreasing hardware replacement frequencies by over 35%.

- Furthermore, the implementation of a precise installation mechanism at the point of sale has enhanced retail service efficiency by 20%, reducing consumer return rates associated with improper application. The strategic deployment of a custom display guard utilizing recycled plastic aligns with corporate sustainability mandates while providing a robust scratch barrier.

- These innovations collectively ensure display clarity, securing vital operational continuity across high-value mobile fleets.

We can help! Our analysts can customize this smartphone screen protector market research report to meet your requirements.

RIA -

RIA -