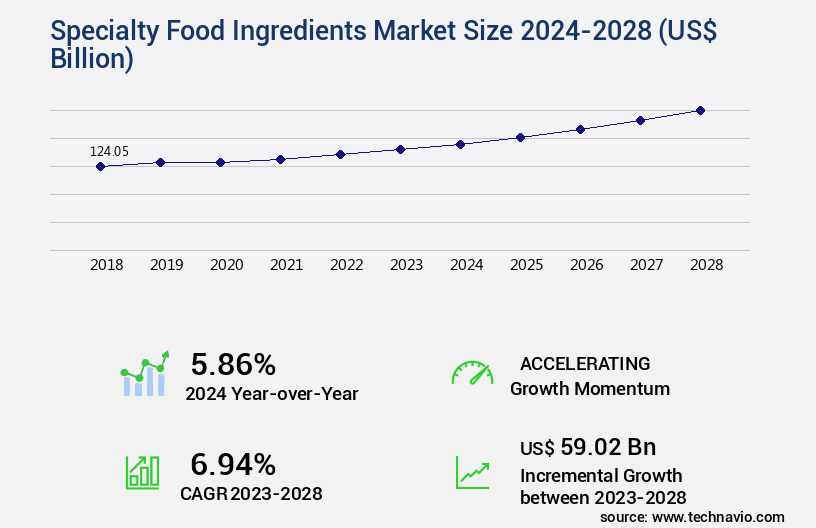

Specialty Food Ingredients Market Size 2024-2028

The specialty food ingredients market size is valued to increase by USD 59.02 billion, at a CAGR of 6.94% from 2023 to 2028. Growing demand for plant-based specialty food ingredients will drive the specialty food ingredients market.

Market Insights

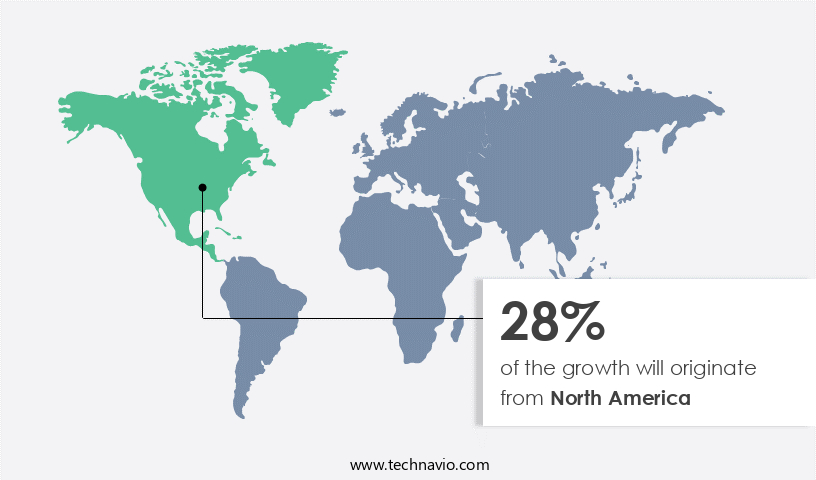

- North America dominated the market and accounted for a 28% growth during the 2024-2028.

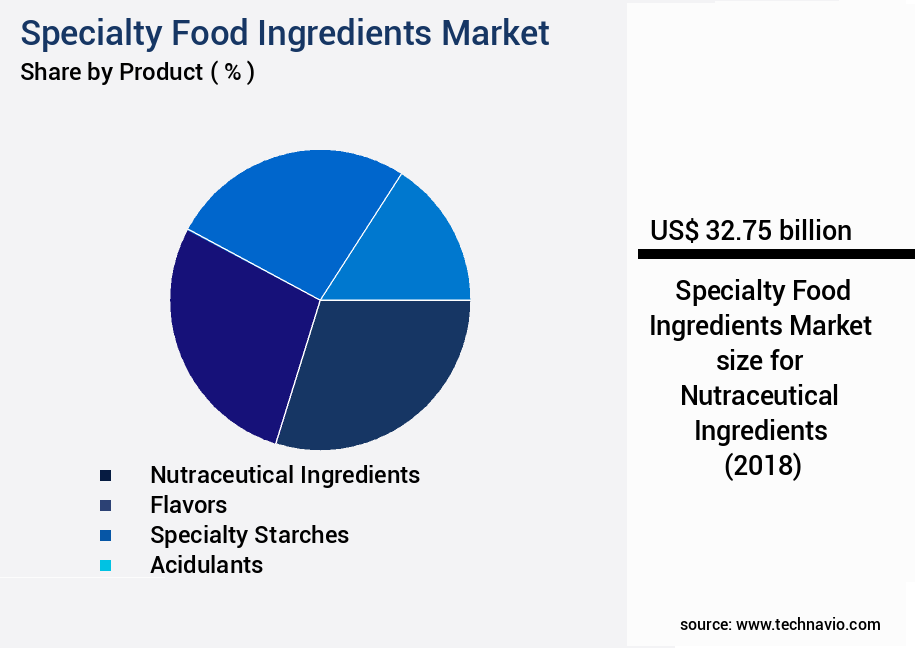

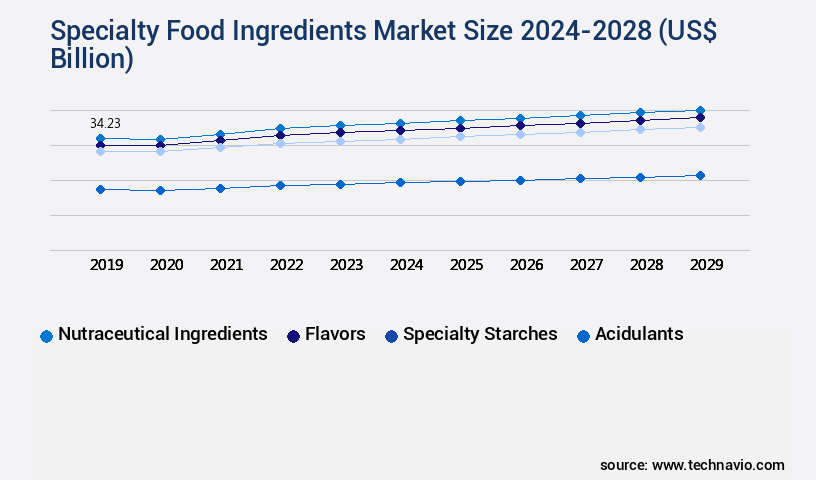

- By Product - Nutraceutical Ingredients segment was valued at USD 32.75 billion in 2022

- By Application - Bakery and confectionary segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 66.91 billion

- Market Future Opportunities 2023: USD 59.02 billion

- CAGR from 2023 to 2028 : 6.94%

Market Summary

- The market encompasses a diverse range of components, including plant-based proteins, natural colorants, and neutraceutical additives, that cater to evolving consumer preferences for healthier and more natural food options. Market growth is driven by several factors, including increasing health consciousness, a trend toward clean labeling, and the rising popularity of plant-based diets. Plant-based proteins, derived from sources such as soy, pea, and rice, are gaining significant traction due to their nutritional benefits and sustainability. Natural neutraceutical ingredients, such as omega-3 fatty acids, vitamins, and minerals, are also in high demand as consumers seek to enhance their overall health and wellness.

- However, the consumption of specialty food ingredients is not without challenges. Potential side effects, such as allergic reactions or gastrointestinal distress, can pose risks for some consumers. Furthermore, ensuring the safety and quality of these ingredients throughout the supply chain is essential to mitigate risks and maintain consumer trust. For instance, a food manufacturer may employ rigorous testing and traceability measures to ensure the authenticity and purity of their specialty food ingredients. By optimizing their supply chain and implementing robust quality control processes, they can minimize risks and maintain operational efficiency while meeting the evolving demands of consumers.

What will be the size of the Specialty Food Ingredients Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with companies implementing various strategies to optimize production processes and ensure regulatory compliance. For instance, waste reduction is a critical focus area, with many firms employing sophisticated food matrix interaction techniques to minimize ingredient usage without compromising product quality. Food additive regulations remain a significant concern for businesses, necessitating rigorous process validation techniques and ingredient sourcing strategies. Texture profile analysis and sensory attribute profiling are essential tools in this regard, helping to ensure that final products meet consumer preferences while adhering to regulatory guidelines. Packaging material selection is another crucial consideration, with ingredient bioavailability and microbial stability playing pivotal roles in product shelf life and safety.

- Quality control procedures, including ingredient safety assessment, sensory consumer testing, and cost reduction strategies, are also essential components of a robust quality assurance program. In the realm of production process parameters, ingredient storage conditions and ingredient transportation methods are vital factors in maintaining ingredient functionality and preserving product quality. Color stability analysis and flavor chemistry analysis are essential techniques for ensuring that final products meet desired sensory attributes, while yield optimization strategies help maximize production efficiency. Ingredient characterization techniques and nutrient fortification strategies are increasingly popular, enabling companies to differentiate their offerings and cater to diverse consumer needs.

- Overall, the market is a dynamic and complex landscape, requiring a deep understanding of various production, regulatory, and consumer trends.

Unpacking the Specialty Food Ingredients Market Landscape

The market encompasses a diverse range of products, from rheologically complex components that optimize texture and sensory attributes, to natural colorants produced through innovative methods. Quality control systems ensure compliance with food safety regulations, while allergenic ingredient detection techniques mitigate potential risks. Emulsion stabilization methods and protein hydrolysis processes improve ingredient formulation design and efficiency. Supply chain traceability and ingredient sourcing strategies ensure purity and standardization. Functional food ingredients, such as probiotics and antioxidants, necessitate preservation techniques and stability studies to maintain their efficacy. Ingredient interaction studies and flavor compound extraction methods enhance product development. Microbial contamination control and ingredient purity testing are essential for maintaining product safety and consumer trust. Ingredient cost optimization and clean label initiatives drive innovation in processing technology and labeling requirements. Carbohydrate modification methods cater to evolving consumer preferences, while sensory perception and nutritional content analysis provide valuable insights for product development and improvement.

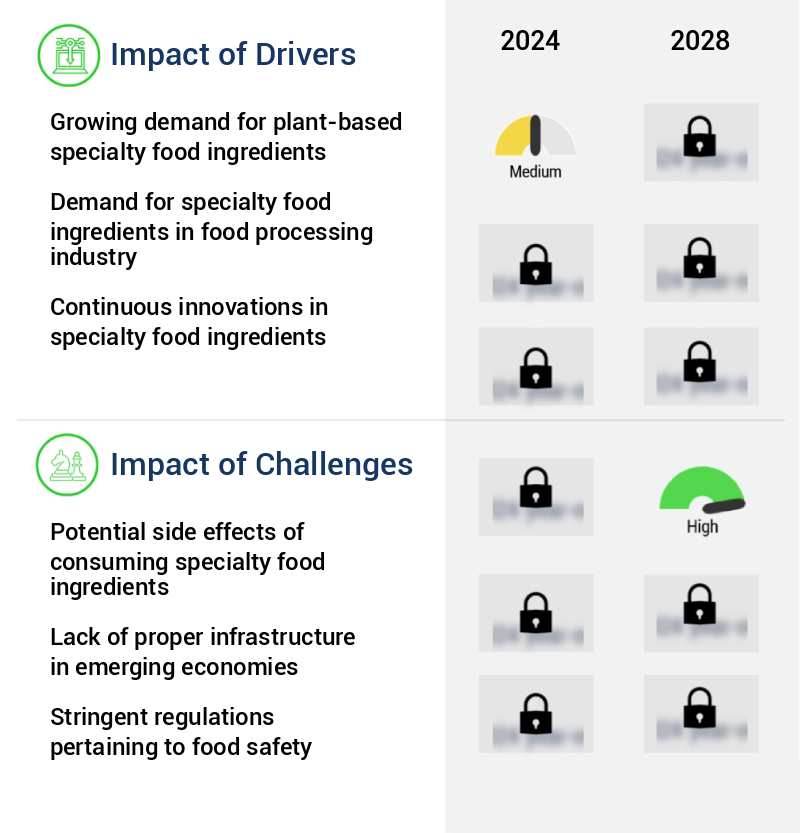

Key Market Drivers Fueling Growth

The surge in demand for plant-based specialty food ingredients serves as the primary catalyst for market growth.

- The market is experiencing dynamic evolution, driven by the increasing popularity of plant-based alternatives in various sectors. Consumers' shifting preferences towards healthier, sustainable, and ethically sourced food options have fueled the demand for plant-derived ingredients. According to recent studies, plant-based diets are on the rise, with over 50% of consumers incorporating plant-based foods into their daily meals. This trend is leading to significant growth in the demand for plant-based specialty food ingredients, such as proteins, fats, fibers, flavors, and colors. Manufacturers are innovating to meet this demand, developing a diverse range of plant-based ingredients sourced from grains, legumes, nuts, seeds, fruits, and vegetables.

- These ingredients offer functional properties and nutritional benefits comparable to their animal-derived counterparts, reducing the need for animal agriculture. For instance, plant-based proteins can provide up to 20g of protein per serving, while plant-based fats offer healthier alternatives to saturated animal fats. These advancements are transforming the market, offering sustainable and ethical solutions for consumers and businesses alike.

Prevailing Industry Trends & Opportunities

The growing demand for natural nutraceutical ingredients represents a significant market trend. Nutraceuticals, derived from natural sources, are increasingly preferred by consumers seeking health benefits beyond basic nutrition.

- The market is witnessing significant evolution, driven by the increasing health consciousness among consumers and the growing demand for food safety. According to recent research, over 50% of global consumers prefer foods made with natural ingredients, compared to just 35% in 2015. This trend is fueling the adoption of natural ingredients in a wide range of food and beverage products, including functional foods, sports drinks, nutritional supplements, and medically formulated foods. Companies in the food processing industry are responding to this demand by incorporating natural ingredients into their offerings. The use of natural ingredients provides numerous health benefits, such as vitamins, minerals, and antioxidants, and can help prevent chronic diseases through the inclusion of natural nutraceutical ingredients.

- These factors are contributing to the increasing popularity of specialty food ingredients in various sectors. For instance, the use of natural ingredients in the production of functional foods has resulted in a 45% increase in sales over the past five years. Similarly, the adoption of natural ingredients in sports drinks has led to a 30% market share growth in the same period.

Significant Market Challenges

The growth of the specialty food industry is significantly impacted by potential side effects associated with the consumption of specialized ingredients.

- The market continues to evolve, expanding its reach across various sectors, including bakery, beverages, confectionery, and savory food applications. Despite the market's growth, it faces challenges related to potential side effects of certain ingredients. Specialty food ingredients are essential for enhancing flavor, texture, and nutritional value, but they may also pose risks for consumers. For instance, common allergens such as nuts, gluten, and dairy are often used in specialty food ingredients, posing risks for individuals with allergies or intolerances. Furthermore, artificial additives, flavors, and preservatives may trigger adverse reactions or sensitivities in some consumers. According to a study, food allergies affect approximately 6 million children in the United States, and 1 in 13 children have a food allergy.

- Another study revealed that 32 million adults in the US have food intolerances. To address these concerns, manufacturers are increasingly focusing on producing allergen-free and clean-label specialty food ingredients. For example, the use of natural flavors and preservatives, as well as alternative sources of allergens, is gaining popularity. This shift towards natural and allergen-free ingredients is expected to drive market growth and meet the evolving demands of health-conscious consumers.

In-Depth Market Segmentation: Specialty Food Ingredients Market

The specialty food ingredients industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Nutraceutical Ingredients

- Flavors

- Specialty starches

- Acidulants

- Others

- Application

- Bakery and confectionary

- Beverages

- Sauces and condiments

- Others

- Source

- Natural

- Synthetic

- Form

- Dry

- Liquid

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The nutraceutical ingredients segment is estimated to witness significant growth during the forecast period.

In the dynamic market, texturizing agents and sensory enhancers continue to dominate, with a focus on improving rheological properties through texture modification techniques. Sensory evaluation methods are essential for quality control systems, ensuring consumer satisfaction and adherence to food safety regulations. Allergenic ingredient detection and natural colorants production are key areas of innovation, with emulsion stabilization methods and supply chain traceability ensuring product consistency and safety. Protein hydrolysis and fat modification techniques are utilized for ingredient formulation design, while food ingredient sourcing and standardization are crucial for cost optimization and preserving ingredient stability.

The Nutraceutical Ingredients segment was valued at USD 32.75 billion in 2018 and showed a gradual increase during the forecast period.

Flavor compound extraction and microbial contamination control are integral to maintaining ingredient purity, and probiotic viability assessment and carbohydrate modification methods cater to the growing demand for functional food ingredients. The market prioritizes clean label ingredients, with a focus on ingredient interaction studies, antioxidant capacity measurement, and process optimization for naturally derived solutions.

Regional Analysis

North America is estimated to contribute 28% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Specialty Food Ingredients Market Demand is Rising in North America Request Free Sample

The market is experiencing dynamic growth, with North America leading the charge due to the region's significant consumption of these ingredients. This trend is driven by the increasing demand for functional foods, fueled by health-conscious consumers seeking to prevent various health issues. The North American market for specialty food ingredients is projected to expand steadily, with the consumption of these ingredients increasing at a constant rate. According to industry reports, the North American market for specialty food ingredients accounted for over 35% of the global market share in 2020.

Moreover, the use of specialty food ingredients in the region's food industry contributes to operational efficiency gains and cost reductions by enhancing product quality and extending shelf life. These factors collectively underpin the market's robust growth trajectory.

Customer Landscape of Specialty Food Ingredients Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Specialty Food Ingredients Market

Companies are implementing various strategies, such as strategic alliances, specialty food ingredients market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Food Systems Inc. - This company specializes in providing innovative ingredient solutions for the food industry, focusing on meat and poultry products, frozen foods, sauces, and marinades.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Food Systems Inc.

- Archer Daniels Midland Co.

- Ashland Inc.

- Axiom Foods Inc.

- Barentz International BV

- Cargill Inc.

- Chr Hansen Holding AS

- DuPont de Nemours Inc.

- Fonterra Cooperative Group Ltd.

- Givaudan SA

- Ingredion Inc.

- Kerry Group Plc

- Koninklijke DSM NV

- Nagase and Co. Ltd.

- Roquette Freres SA

- Sensient Technologies Corp.

- SubNutra Food Ingredients Pvt. Ltd.

- Tate and Lyle PLC

- Woodland Foods Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Specialty Food Ingredients Market

- In January 2025, Archer Daniels Midland Company (ADM) announced the launch of its new line of plant-based proteins, Protera, specifically designed for the market (ADM press release, 2025). These proteins are derived from peas, lentils, and chickpeas, providing a sustainable alternative to traditional animal-derived ingredients.

- In March 2025, DuPont Nutrition & Biosciences and Ingredion Inc. entered into a strategic partnership to expand their joint venture, NutriScience Innovations, which focuses on developing and marketing specialty food ingredients (DuPont press release, 2025). This collaboration combines DuPont's expertise in fermentation and Ingredion's knowledge of texturizing technologies to create innovative solutions for the food industry.

- In May 2025, Kerry Group, a leading global taste and nutrition company, acquired Bio-Techne Corporation's food division, Quadrant Health Sciences, for approximately € 1.1 billion (Kerry Group press release, 2025). This acquisition significantly expanded Kerry's capabilities in the market, particularly in the areas of probiotics, enzymes, and functional proteins.

- In August 2024, Firmenich, a global leader in the creation of flavors and fragrances, received regulatory approval for its natural food coloring ingredient, Rubia Natural, in the European Union (Firmenich press release, 2024). This approval marked a significant milestone for Firmenich, as Rubia Natural is the first natural red food coloring derived from the rubia tinctorum plant to be approved for use in the EU.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Specialty Food Ingredients Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

188 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.94% |

|

Market growth 2024-2028 |

USD 59.02 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.86 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Specialty Food Ingredients Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market encompasses a diverse range of high-value components used to enhance the sensory experience, functionality, and nutritional value of food products. The effectiveness of these ingredients relies significantly on the processing methods employed, as their functionality can be influenced by various factors such as temperature, pressure, and time. Proper storage conditions are equally crucial to maintain ingredient stability, ensuring consistent product quality and minimizing potential degradation. Sensory evaluation methods play a pivotal role in assessing the impact of specialty food ingredients on food systems. Determining key functional properties through techniques like rheology testing and texture analysis is essential for optimizing ingredient processing parameters and understanding ingredient interactions. Measuring the bioavailability of food components using techniques such as in vitro digestion and chromatography is another critical aspect of specialty food ingredient development. Investigating flavor compound interactions and implementing strategies for enhancing ingredient shelf life, controlling microbial contamination, and optimizing sourcing are all vital components of a successful specialty food ingredient business. Developing clean label ingredient formulations and assessment of allergenic potential are essential for compliance with consumer preferences and regulatory requirements. Techniques for improving ingredient purity, such as chromatography and filtration, are essential for ensuring product consistency and quality. Approaches for optimizing ingredient sourcing, implementing food safety management systems, monitoring supply chain traceability, and evaluating food ingredient labeling are all crucial elements of operational planning and supply chain efficiency. Compared to traditional food ingredients, specialty food ingredients offer a significant competitive edge in terms of product differentiation and consumer appeal. By focusing on the optimization of ingredient processing parameters, analysis of ingredient interactions, assessment of ingredient stability under various conditions, and evaluation of different texture modification methods, businesses can create unique and innovative food products that cater to evolving consumer demands.

What are the Key Data Covered in this Specialty Food Ingredients Market Research and Growth Report?

-

What is the expected growth of the Specialty Food Ingredients Market between 2024 and 2028?

-

USD 59.02 billion, at a CAGR of 6.94%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Nutraceutical Ingredients, Flavors, Specialty starches, Acidulants, and Others), Application (Bakery and confectionary, Beverages, Sauces and condiments, and Others), Geography (North America, APAC, Europe, South America, and Middle East and Africa), Source (Natural and Synthetic), and Form (Dry and Liquid)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growing demand for plant-based specialty food ingredients, Potential side effects of consuming specialty food ingredients

-

-

Who are the major players in the Specialty Food Ingredients Market?

-

Advanced Food Systems Inc., Archer Daniels Midland Co., Ashland Inc., Axiom Foods Inc., Barentz International BV, Cargill Inc., Chr Hansen Holding AS, DuPont de Nemours Inc., Fonterra Cooperative Group Ltd., Givaudan SA, Ingredion Inc., Kerry Group Plc, Koninklijke DSM NV, Nagase and Co. Ltd., Roquette Freres SA, Sensient Technologies Corp., SubNutra Food Ingredients Pvt. Ltd., Tate and Lyle PLC, and Woodland Foods Ltd.

-

We can help! Our analysts can customize this specialty food ingredients market research report to meet your requirements.

RIA -

RIA -