Suppository Packaging Market Size 2026-2030

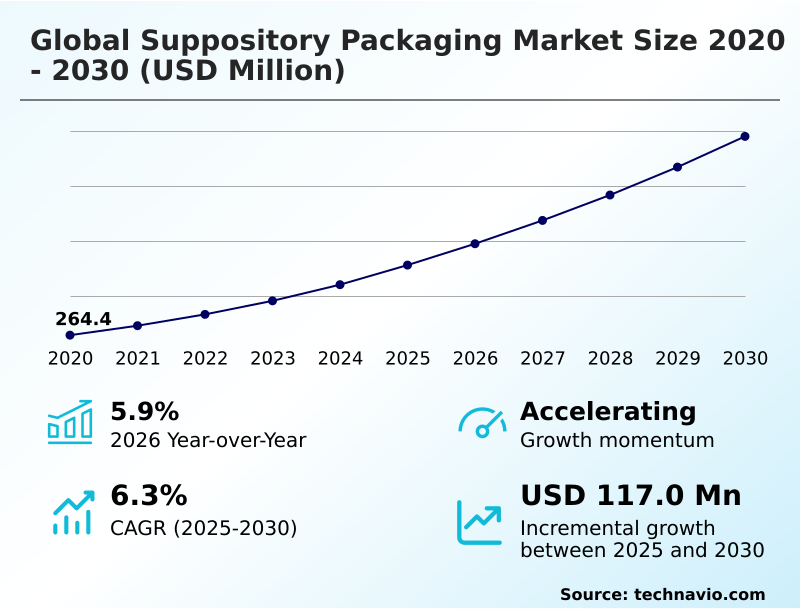

The suppository packaging market size is valued to increase by USD 117 million, at a CAGR of 6.3% from 2025 to 2030. Rising prevalence of dysphagia and geriatric healthcare requirements will drive the suppository packaging market.

Major Market Trends & Insights

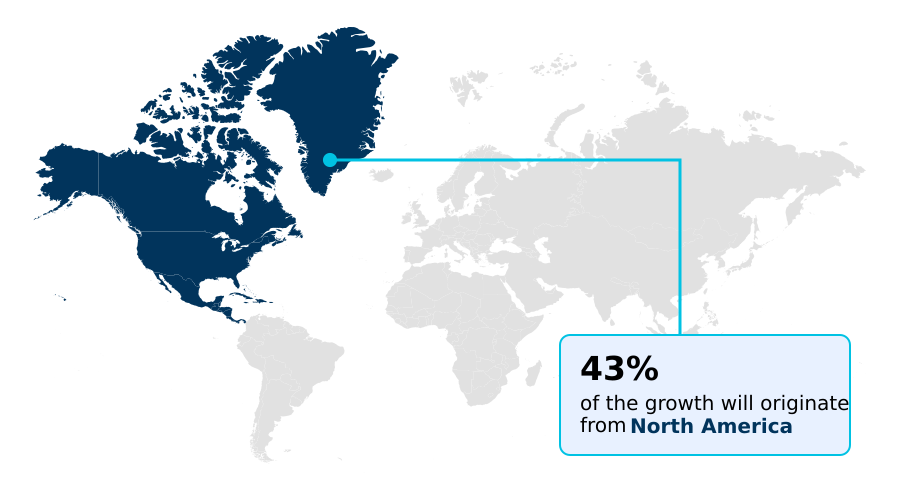

- North America dominated the market and accounted for a 43.2% growth during the forecast period.

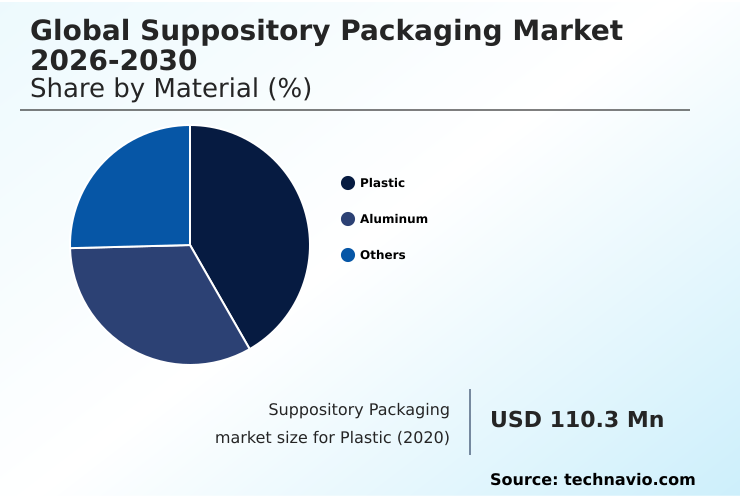

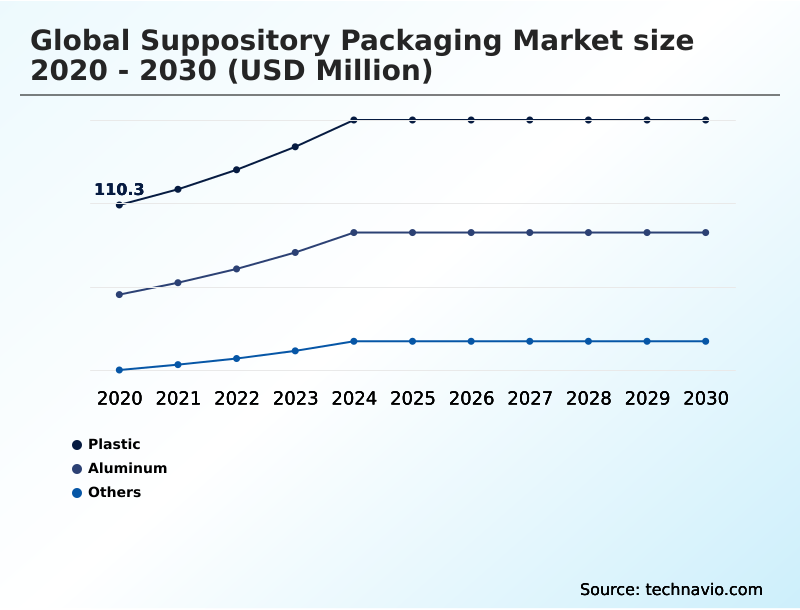

- By Material - Plastic segment was valued at USD 132.5 million in 2024

- By Application - Single dose unit segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 180.7 million

- Market Future Opportunities: USD 117 million

- CAGR from 2025 to 2030 : 6.3%

Market Summary

- The suppository packaging market is defined by the need for high-performance containment solutions that ensure the stability of heat-sensitive formulations. Growth is fueled by an expanding geriatric population and the broadening therapeutic use of suppositories for conditions requiring localized delivery or bypassing first-pass metabolism.

- Key trends include the shift toward sustainable materials, such as mono-material structures and recyclable aluminum solutions, and the integration of anti-counterfeiting technologies to enhance drug supply chain security. A central business scenario involves a contract development and manufacturing organization (CDMO) upgrading its automated packaging lines.

- The objective is to accommodate both traditional PVC/PE laminates and advanced PVC-free blister systems, allowing the firm to serve a diverse client base ranging from large pharmaceutical companies with strict sustainability mandates to smaller generic drug makers requiring cost-effective solutions.

- This strategic investment in flexible, high-speed machinery with integrated vision inspection systems is crucial for maintaining good manufacturing practices (GMP) compliance and optimizing overall equipment effectiveness (OEE). Challenges remain, including the high capital cost of advanced machinery, navigating stringent regulatory compliance for extractables and leachables, and managing the complexities of cold chain distribution.

What will be the Size of the Suppository Packaging Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Suppository Packaging Market Segmented?

The suppository packaging industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Material

- Plastic

- Aluminum

- Others

- Application

- Single dose unit

- Multi-dose unit

- Type of packaging

- Strip packs

- Blister packs

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- Middle East and Africa

- South Africa

- Israel

- Turkey

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Material Insights

The plastic segment is estimated to witness significant growth during the forecast period.

Plastic materials, including PVC/PE laminates and emerging PVC-free blister systems, are central to the suppository packaging market. These thermoformable films are favored for their cost-effectiveness and versatility in creating custom cavities for semi-solid dosage form packaging.

The industry is undergoing a significant transition toward sustainable pharmaceutical packaging, with a focus on mono-material structures that align with circular economy in pharma packaging principles.

Innovations aim to enhance moisture barrier performance in recyclable polymers without compromising the integrity required by pharmacopeia standards.

This shift is critical, as adopting polypropylene-based films can achieve a 30% reduction in carbon footprint compared to traditional materials, influencing choices in geriatric healthcare packaging and rectal drug delivery systems.

The Plastic segment was valued at USD 132.5 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 43.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Suppository Packaging Market Demand is Rising in North America Get Free Sample

The geographic landscape of the suppository packaging market is diverse, with North America leading in incremental growth, accounting for over 43% of the market expansion.

This region demands high-barrier packaging and advanced tamper-evident features to comply with stringent drug supply chain security regulations.

In contrast, APAC is the fastest-growing region, driven by large-scale manufacturing in China and India, where the focus is on volume and cost-efficiency for both domestic and export markets.

Europe represents a mature market with a strong emphasis on sustainability and regulatory compliance with EU directives, pushing for the adoption of recyclable aluminum solutions and advancements in biodegradable packaging films.

This regional divergence requires suppliers of suppository filling machines and primary pharmaceutical packaging to offer flexible solutions catering to varied market needs, from high-end specialty packaging materials in developed economies to cost-effective options in emerging ones.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the suppository packaging market are increasingly shaped by a complex interplay of sustainability, regulatory demands, and technological advancements. The push for sustainable materials for suppository packaging is driving significant R&D in high barrier films for temperature-sensitive suppositories, with a notable trend toward advances in mono-material blister packs for pharma.

- These materials must provide robust protection while also contributing to the goal of reducing carbon footprint of pharmaceutical packaging. A key operational consideration is the impact of serialization on suppository packaging lines, which necessitates investment in sophisticated printing and inspection technology, directly influencing the total cost of ownership.

- The role of packaging in preventing drug counterfeiting is another critical factor, compelling the adoption of secure solutions. On the operational side, automation solutions for suppository filling and sealing are essential for optimizing OEE in pharmaceutical packaging lines, with a focus on improving patient compliance with smart suppository packaging.

- The cost analysis of cold-form vs thermoform blisters remains a pivotal decision point for manufacturers, weighing material costs against barrier properties. Furthermore, the industry grapples with regulatory challenges for extractables and leachables and the complexities of cold chain logistics for semi-solid pharmaceuticals, which require diligent material validation for primary pharmaceutical contact and secure supply chain management.

What are the key market drivers leading to the rise in the adoption of Suppository Packaging Industry?

- The rising prevalence of dysphagia and the specific healthcare needs of the geriatric population are key drivers for market growth.

- Market growth is fundamentally driven by demographic shifts and therapeutic expansion, necessitating advancements in material science. The increasing global geriatric population requires patient-centric packaging design that is easy to handle, driving demand for innovative peel-apart mechanics in unit-dose blister packs.

- Simultaneously, the broadening use of suppositories in gynecology and proctology creates a need for specialized vaginal ovule packaging and rectal drug delivery systems with superior barrier properties.

- A major catalyst is the industry's focus on sustainability; the adoption of new polypropylene-based films has enabled a 30% reduction in carbon footprint over traditional PVC/aluminum blisters.

- This push toward a circular economy is compelling providers of pharmaceutical packaging machinery and materials to innovate, ensuring both pharmaceutical packaging stability and environmental responsibility without compromising on light-sensitive drug protection.

What are the market trends shaping the Suppository Packaging Industry?

- A key market trend is the integration of smart packaging solutions and advanced anti-counterfeiting technologies. This enhances patient safety and improves supply chain visibility.

- Key trends are reshaping the market, led by the adoption of automation and smart packaging. The integration of tamper-evident pharmaceutical labels with RFID and NFC technologies enhances supply chain visibility and provides a crucial layer of anti-counterfeiting technologies. This digitalization allows for adherence monitoring technology, with some systems improving patient compliance tracking.

- On the manufacturing floor, the deployment of high-speed packaging automation and robotics on packaging lines has led to a 40% increase in throughput efficiency for some contract development and manufacturing (CDMO) firms.

- This trend toward automated vision inspection systems also minimizes defects in cold forming aluminum blisters and other primary pharmaceutical packaging, ensuring higher quality output and supporting the rigorous demands of pharmaceutical packaging regulations for pediatric dosage forms and other sensitive applications.

What challenges does the Suppository Packaging Industry face during its growth?

- Stringent regulatory compliance requirements and evolving material safety standards present a significant challenge to industry growth.

- Navigating the complex suppository packaging market involves overcoming significant regulatory, financial, and logistical hurdles. The stringent enforcement of standards for extractables and leachables requires extensive pharmaceutical stability testing and packaging material validation, a costly and time-consuming process.

- The high capital investment needed for advanced suppository filling machines, with prices increasing by 15% year-over-year, presents a major barrier, especially for smaller manufacturers. Furthermore, the thermal sensitivity of these products necessitates robust cold chain distribution and thermal insulation packaging to prevent spoilage, particularly in warmer climates.

- A single failure in the supply chain can result in the loss of entire batches, leading to significant financial repercussions. These challenges demand rigorous adherence to good manufacturing practices (GMP) and innovative solutions for oxygen barrier packaging to ensure drug packaging integrity from production to patient.

Exclusive Technavio Analysis on Customer Landscape

The suppository packaging market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the suppository packaging market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Suppository Packaging Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, suppository packaging market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ACG - Provides integrated solutions including barrier packaging films and blister packing machinery tailored for hygroscopic suppository products, ensuring product stability and manufacturing efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ACG

- Aenova Holding GmbH

- Alutech Packaging Pvt. Ltd

- Amcor Plc

- Berry Global Inc.

- Bilcare Ltd.

- Catalent Inc.

- Constantia Flexibles GmbH

- Gerresheimer AG

- Huhtamaki Oyj

- KP Holding GmbH and Co. KG

- Liveo Research

- Marchesini Group Spa

- MULTIVAC SE and Co. KG

- Romaco Holding GmbH

- Sonoco Products Co.

- Tekni Plex Inc.

- WestRock Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Suppository packaging market

- In August 2024, Amcor Plc unveiled a new line of pharmaceutical-grade, ready-to-recycle blister lidding engineered for heat-sensitive applications.

- In October 2024, Tekni-Plex Healthcare announced the commercial availability of a new polypropylene-based blister film series designed to replace PVC/PVDC in semi-solid dose packaging.

- In January 2025, Bayer AG announced the expansion of its women's health portfolio with a new localized hormonal therapy delivered via vaginal ovules, requiring specialized high-barrier packaging.

- In February 2025, Avery Dennison launched a specialized range of tamper-evident pharmaceutical labels equipped with RFID technology capable of functioning effectively on aluminum foil surfaces.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Suppository Packaging Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 294 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.3% |

| Market growth 2026-2030 | USD 117.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.9% |

| Key countries | US, Canada, Mexico, China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, South Africa, Israel, Turkey, Saudi Arabia, UAE, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The suppository packaging market is navigating a period of significant transformation, driven by demands for both enhanced product protection and environmental responsibility. The core of this evolution lies in material science, with a definitive move away from traditional PVC/PE laminates toward advanced mono-material structures and PVC-free blister systems.

- This transition to high-barrier polymer films and recyclable aluminum solutions addresses the stringent pharmacopeia standards for heat-sensitive formulations. Boardroom decisions increasingly center on balancing the high capital investment in new automated packaging lines with the long-term benefits of regulatory compliance and market differentiation.

- For instance, the average price of GMP-compliant suppository filling machines has risen by 15% year-over-year, presenting a significant financial hurdle. Key to success is the adoption of technologies like vision inspection systems and serialization and traceability to ensure good manufacturing practices (GMP) and drug supply chain security.

- Packaging design must also incorporate child-resistant features and senior-friendly opening mechanisms to improve patient safety and adherence, particularly as applications for hormonal replacement therapies expand.

What are the Key Data Covered in this Suppository Packaging Market Research and Growth Report?

-

What is the expected growth of the Suppository Packaging Market between 2026 and 2030?

-

USD 117 million, at a CAGR of 6.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Material (Plastic, Aluminum, and Others), Application (Single dose unit, and Multi-dose unit), Type of Packaging (Strip packs, Blister packs, and Others) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Rising prevalence of dysphagia and geriatric healthcare requirements, Stringent regulatory compliance and material safety standards

-

-

Who are the major players in the Suppository Packaging Market?

-

ACG, Aenova Holding GmbH, Alutech Packaging Pvt. Ltd, Amcor Plc, Berry Global Inc., Bilcare Ltd., Catalent Inc., Constantia Flexibles GmbH, Gerresheimer AG, Huhtamaki Oyj, KP Holding GmbH and Co. KG, Liveo Research, Marchesini Group Spa, MULTIVAC SE and Co. KG, Romaco Holding GmbH, Sonoco Products Co., Tekni Plex Inc. and WestRock Co.

-

Market Research Insights

- Market dynamics are shaped by a dual focus on enhancing therapeutic efficacy and operational efficiency. The demand for advanced semi-solid dosage form packaging is growing, driven by innovations in patient-centric packaging design and the need for robust hygroscopic drug protection. Adopting high-speed packaging automation allows manufacturers to increase throughput by over 40%, directly impacting profitability.

- Simultaneously, the move toward sustainable pharmaceutical packaging is compelling companies to re-evaluate material choices, with new recyclable films reducing carbon footprints by up to 30% compared to legacy plastics. This shift toward circular economy in pharma packaging principles is balanced against the need for rigorous packaging material validation to ensure drug packaging integrity.

- These factors create a competitive environment where pharmaceutical packaging innovation is key to meeting both regulatory and consumer demands.

We can help! Our analysts can customize this suppository packaging market research report to meet your requirements.

RIA -

RIA -