US Tire Retreading Market Size 2025-2029

The US tire retreading market size is valued to increase USD 926.8 million, at a CAGR of 4.2% from 2024 to 2029. Lower cost of tire retreading will drive the US tire retreading market.

Major Market Trends & Insights

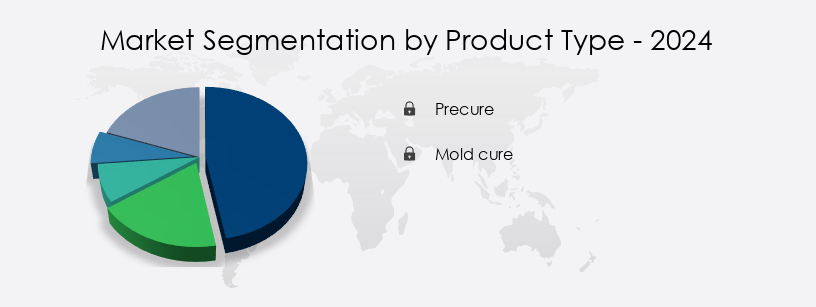

- By Product Type - Precure segment was valued at USD 3428.10 million in 2022

- By Consumption Pattern - Domestic consumption segment accounted for the largest market revenue share in 2022

- CAGR from 2024 to 2029 : 4.2%

Market Summary

- The Tire Retreading Market in the US is a dynamic and evolving industry, driven by the increasing focus on sustainability and cost savings. Core technologies, such as regenerated tread rubber and retreading processes, continue to advance, enabling higher quality retreaded tires. However, the availability of low-cost new tires poses a significant challenge to the market, accounting for over 30% of tire sales in the US. Despite this, opportunities abound, with growing demand from the commercial fleet sector and increasing regulatory support for retreading.

- For instance, the US Environmental Protection Agency (EPA) estimates that retreading one million scrap tires saves enough energy to power 11,000 homes for a year. This ongoing interplay of drivers, challenges, and opportunities underscores the importance of staying informed about the latest trends and developments in the Tire Retreading Market in the US.

What will be the Size of the US Tire Retreading Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Tire Retreading in US Market Segmented ?

The tire retreading in US industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product Type

- Precure

- Mold cure

- Consumption Pattern

- Domestic consumption

- Export

- Vehicle Type

- Commercial vehicle

- Passenger vehicle

- Performance Features

- Wet Traction

- Snow Performance

- Geography

- North America

- US

- North America

By Product Type Insights

The precure segment is estimated to witness significant growth during the forecast period.

The Tire Retreading Market in the US continues to evolve, with ongoing advancements in technology and industry standards. Precure retreading, which involves the separate vulcanization of retread rubber followed by its binding to the tire through the cushion gum, emerged in the 1960s with the widespread adoption of radial tires in commercial vehicles. Compared to mold cure retreading, precure retreading requires lower investment and follow-up costs. Retreading offers significant material cost reduction, with retread tire lifespan often exceeding that of new tires by up to 50%. Safety regulations mandate rigorous retread tire inspection, including tread depth measurement, bead seating methods, and repair techniques.

Retread tire performance is ensured through tire pressure monitoring, tread wear indicators, and retread quality control. Retreading processes have become more automated, with retread tire inspection, curing cycle optimization, and rubber compound mixing now largely mechanized. The environmental impact of retreading is minimized through waste tire recycling and the use of energy-efficient buffing machines. The retread process includes casing inspection protocols for bias ply and radial tires, as well as repair techniques for underinflation detection. Retread tire durability is enhanced through the use of advanced materials and techniques, such as cement application and tread pattern design. Retread technician training ensures consistent application of these methods, contributing to the economic viability of retreading.

The retread industry continues to innovate, with advancements in mold curing systems, tire tread patterns, and retread warranty programs.

The Precure segment was valued at USD 3428.10 million in 2019 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The tire retreading market in the US is witnessing significant growth due to the adoption of optimal curing parameters and advanced retreading technologies. Retread tires offer extended longevity, making them an economically viable alternative to new tires, especially for fleets operating under various loads. Casing preparation techniques and rubber compound formulations play a crucial role in ensuring effective quality control during retread production. The impact of tire retread methods on performance is a critical consideration, with precure and mold cure retreading methods offering distinct advantages. Precure retreading allows for faster production lines and improved efficiency, while mold cure retreading ensures better tire pressure maintenance, leading to enhanced performance and safety.

Advanced materials, such as silica and nanotechnology, are increasingly being used in retread tire production to improve durability and performance. Measuring tread depth and implementing monitoring systems are essential for maintaining consistent quality and regulatory compliance. The retreading industry is making strides in reducing waste by implementing cost-saving strategies, such as recycling unused rubber and optimizing production processes. Retread tire safety and environmental sustainability are key focus areas, with regulatory bodies setting stringent standards. Innovations in retread technology, including the use of advanced materials and automation, are transforming the industry, making it more competitive and efficient.

According to market intelligence, adoption rates for these advanced technologies are significantly higher in the commercial vehicle segment compared to the passenger car segment. This trend is expected to continue, with more than 60% of new retreading technologies focusing on the commercial vehicle market.

What are the key market drivers leading to the rise in the adoption of Tire Retreading in US Industry?

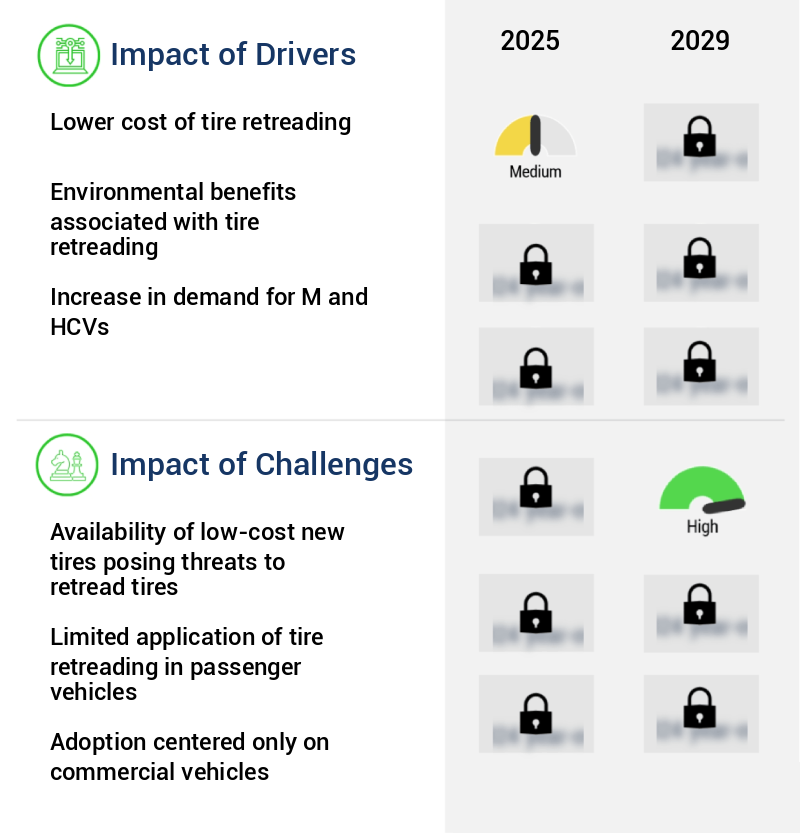

- The significant cost savings associated with tire retreading is the primary factor driving market growth in this industry.

- Tires represent a substantial portion of fleet operators' annual expenses, accounting for approximately one-third of their total costs. To optimize financial resources, fleet operators employ cost-saving strategies in the tire category. Retreads, which have seen advancements since the mid-19th century, have gained significant traction in the commercial vehicle sector. Retreaders have made strides in enhancing tread quality, expanding selection, raising manufacturing standards, improving plant safety, and refining evaluation procedures through the adoption of advanced technologies like shearography. These advancements have narrowed the gap between retreads and new tires in terms of quality and safety.

- Retreads offer a cost advantage of approximately 40% compared to new tires, making them an attractive option for fleet operators seeking operational efficiency. By embracing retreads, fleet operators can effectively reduce their tire-related expenses while maintaining the performance and reliability of their vehicles.

What are the market trends shaping the Tire Retreading in US Industry?

- The trend in the market involves significant technological advances in the field of tire retreading. Technological innovations are driving the development of tire retreading processes.

- The tire retreading market in the US is witnessing significant advancements, driven by technological innovations such as the development of Low Rolling Resistance (LRR) retreads and the integration of smart technology in vehicles. These developments are aimed at reducing fuel consumption and enhancing tire durability, making them increasingly popular among commercial vehicle operators. Furthermore, regulatory initiatives like the US Environmental Protection Agency's (EPA) SmartWay program, which encourages businesses to improve the sustainability of their supply chains by promoting fuel-efficient freight transportation, are fueling the market's expansion.

- The tire industry is responding by focusing on producing tires that meet these sustainability requirements and contribute to reduced greenhouse gas emissions. This data-driven narrative underscores the continuous evolution of the tire retreading market and its growing significance across various sectors.

What challenges does the Tire Retreading in US Industry face during its growth?

- The affordability of new, low-cost tires presents a significant challenge to the expansion of the retread tire industry, as consumers and businesses may opt for the former despite the environmental and cost benefits associated with retread tires.

- In the last decade, the tire market experienced a notable increase in demand, leading to a tire shortage and a subsequent growth surge for the retreading tire industry. However, the economic recession caused a decrease in tire demand, while new tire factories increased supply. This shift resulted in an oversupply of new tires, causing historically low prices. Furthermore, imports from China intensified the price competition, bridging the price gap between new and retreaded tires.

- Looking forward, this price disparity is predicted to decrease further, putting pressure on retread players to optimize operations and manufacturing costs to remain competitive. The tire industry's landscape continues to evolve, presenting both challenges and opportunities for market participants.

Exclusive Technavio Analysis on Customer Landscape

The US tire retreading market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the US tire retreading market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Tire Retreading in US Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, US tire retreading market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Michelin (France) - The company specializes in tire retreading services, meticulously examining tire carcasses for internal defects that may impact their suitability for retreading.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Michelin (France)

- Bridgestone Corporation (Japan)

- Goodyear Tire & Rubber Company (United States)

- Continental AG (Germany)

- Pirelli & C. S.p.A. (Italy)

- Hankook Tire Co., Ltd. (South Korea)

- Yokohama Rubber Company (Japan)

- Sumitomo Rubber Industries (Japan)

- Toyo Tire Corporation (Japan)

- Kumho Tire Co., Inc. (South Korea)

- Cooper Tire & Rubber Company (United States)

- Nokian Tyres plc (Finland)

- Apollo Tyres Ltd. (India)

- Giti Tire (Singapore)

- Maxxis International (Taiwan)

- Falken Tire (Japan)

- MRF Limited (India)

- Cheng Shin Rubber Ind. Co. Ltd. (Taiwan)

- Nexen Tire Corporation (South Korea)

- Trelleborg AB (Sweden)

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Tire Retreading Market In US

- In January 2024, Bridgestone Americas, a leading tire manufacturer, announced the launch of its new retreaded truck tire, Bandag B910+, engineered with advanced tread designs and materials for improved fuel efficiency and extended tread life (Bridgestone Americas press release).

- In March 2024, Goodyear and Michelin, two major tire companies, formed a strategic partnership to collaborate on research and development of retreading technologies, aiming to enhance sustainability and reduce the environmental impact of the tire industry (Goodyear press release).

- In May 2024, Tireco, a significant tire retreader, completed the acquisition of Retread Tire Company, expanding its production capacity and market presence in the Eastern United States (Tire Business).

- In April 2025, the Environmental Protection Agency (EPA) introduced new regulations encouraging the use of retreaded tires in the public sector, aiming to reduce waste and greenhouse gas emissions from the transportation sector (EPA press release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled US Tire Retreading Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

162 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.2% |

|

Market growth 2025-2029 |

USD 926.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

3.8 |

|

Key countries |

US |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The tire retreading industry continues to evolve, with a focus on material cost reduction and enhanced durability driving market activities. Off-the-road retreading, a segment that caters to heavy-duty vehicles, has gained significant traction due to the high operating costs of replacement tires. Bead seating methods have advanced, ensuring improved retread tire quality and safety. Retread warranty programs have become increasingly important, offering assurance to customers regarding tire performance and longevity. Buffing machine operation and safety regulations have been refined to ensure consistent results and minimize risks. Tread depth measurement and retread process automation have streamlined inspections, ensuring uniformity and accuracy.

- Retread tire inspection techniques have evolved, with a focus on identifying repairable damages and ensuring tire safety. Retread tire durability has been enhanced through advancements in rubber compound mixing, mold curing systems, and curing cycle optimization. The environmental impact of tire retreading is a growing concern, with waste tire recycling and precure retreading systems gaining popularity. Truck tire retreading and radial tire retreading have become standard practices, with casing inspection protocols ensuring the optimal use of casings. Bias ply retreading, while still in use, is gradually being phased out due to its lower performance and durability compared to radial retreading.

- Retread technician training programs have been established to ensure a skilled workforce, maintaining the economic viability of the retreading industry. Tire pressure monitoring and tread wear indicators have become essential tools for retreaders, enhancing tire performance and safety. Retread tire lifespan has been extended through advancements in retreading materials and processes, making retreading a cost-effective alternative to new tire purchases. Underinflation detection and the vulcanization process have been optimized, ensuring consistent tire performance and longevity. Repair techniques have evolved, with a focus on minimizing the need for retreading and ensuring optimal tire performance. Tire tread patterns have been developed to cater to various applications, enhancing tire performance and safety.

What are the Key Data Covered in this US Tire Retreading Market Research and Growth Report?

-

What is the expected growth of the US Tire Retreading Market between 2025 and 2029?

-

USD 926.8 million, at a CAGR of 4.2%

-

-

What segmentation does the market report cover?

-

The report segmented by Product Type (Precure and Mold cure), Consumption Pattern (Domestic consumption and Export), Vehicle Type (Commercial vehicle and Passenger vehicle), Geography (North America), and Performance Features (Wet Traction and Snow Performance)

-

-

Which regions are analyzed in the report?

-

US

-

-

What are the key growth drivers and market challenges?

-

Lower cost of tire retreading, Availability of low-cost new tires posing threats to retread tires

-

-

Who are the major players in the Tire Retreading Market in US?

-

Key Companies Michelin (France), Bridgestone Corporation (Japan), Goodyear Tire & Rubber Company (United States), Continental AG (Germany), Pirelli & C. S.p.A. (Italy), Hankook Tire Co., Ltd. (South Korea), Yokohama Rubber Company (Japan), Sumitomo Rubber Industries (Japan), Toyo Tire Corporation (Japan), Kumho Tire Co., Inc. (South Korea), Cooper Tire & Rubber Company (United States), Nokian Tyres plc (Finland), Apollo Tyres Ltd. (India), Giti Tire (Singapore), Maxxis International (Taiwan), Falken Tire (Japan), MRF Limited (India), Cheng Shin Rubber Ind. Co. Ltd. (Taiwan), Nexen Tire Corporation (South Korea), and Trelleborg AB (Sweden)

-

Market Research Insights

- The tire retreading market in the US continues to evolve, driven by the need for cost savings, improved fuel efficiency, and regulatory compliance. According to industry estimates, retreaded tires account for approximately 3% of the total tire market in the US, with over 11 million retreaded tires produced annually. This represents a significant increase from the 8 million retreaded tires produced in 2010. Material selection, casing preparation, and retread process control are critical factors in ensuring the quality and durability of retreaded tires. The retread process involves several stages, including cure time temperature monitoring, bonding strength assessment, and retread production capacity optimization.

- Equipment maintenance and operator skill are also essential for maximizing retread efficiency and process optimization. Retread technology continues to advance, with innovations in tread rubber compounds, mold design, and retread tire design enhancing performance and extending tire life. Environmental regulations play a key role in the market, with a focus on waste management and life cycle assessment. The use of adhesive properties and pressure control technologies helps to ensure regulatory compliance and improve retread tire durability. The ongoing investment in retread technology and process optimization is expected to drive continued growth in the US tire retreading market.

We can help! Our analysts can customize this US tire retreading market research report to meet your requirements.

RIA -

RIA -