Upper Respiratory Tract Infection Treatment Market Size 2026-2030

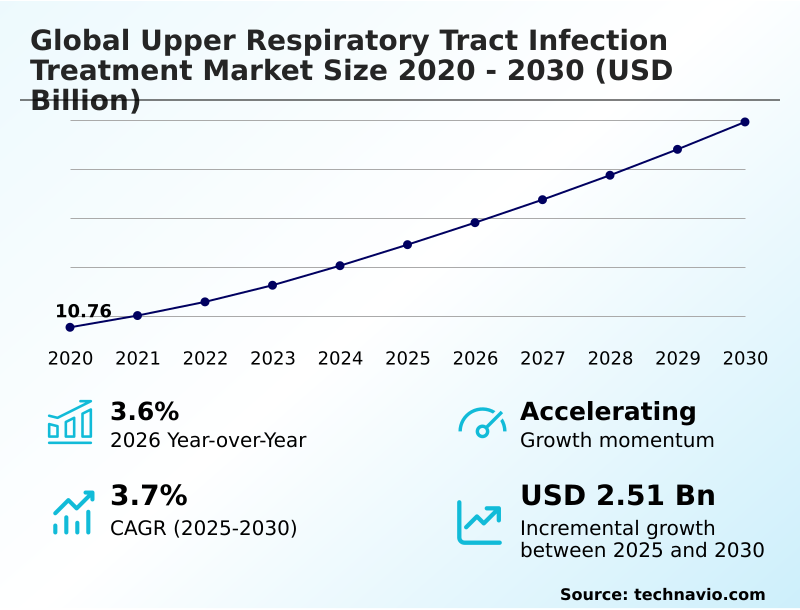

The upper respiratory tract infection treatment market size is valued to increase by USD 2.51 billion, at a CAGR of 3.7% from 2025 to 2030. Rising incidence and prevalence of upper respiratory tract infections will drive the upper respiratory tract infection treatment market.

Major Market Trends & Insights

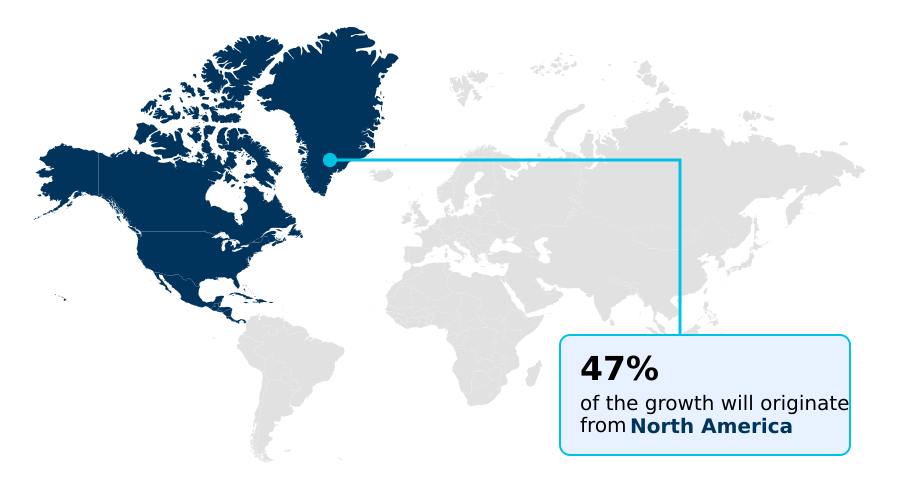

- North America dominated the market and accounted for a 46.8% growth during the forecast period.

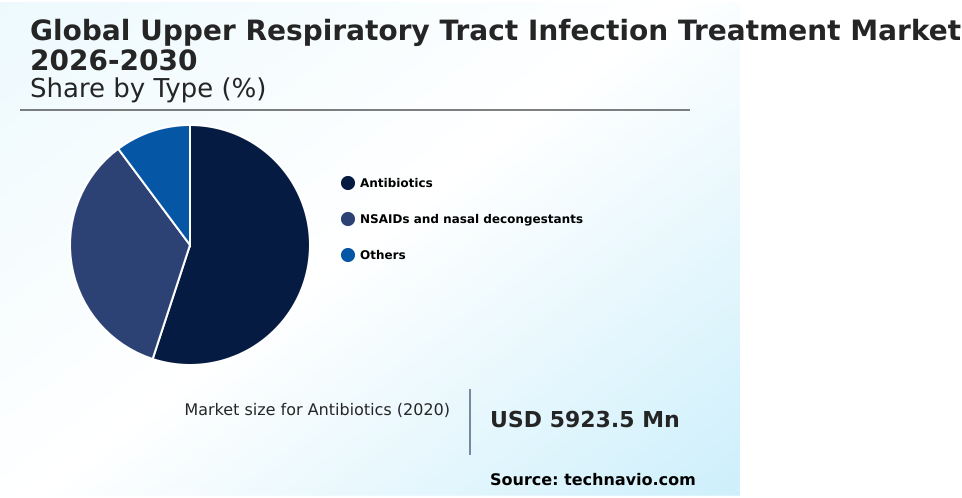

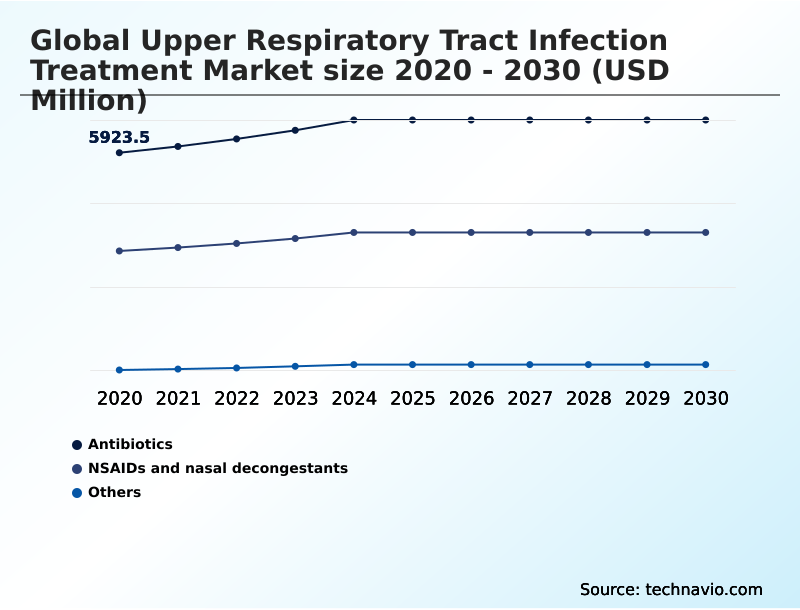

- By Type - Antibiotics segment was valued at USD 6.65 billion in 2024

- By Distribution Channel - Hospital pharmacies segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 4.19 billion

- Market Future Opportunities: USD 2.51 billion

- CAGR from 2025 to 2030 : 3.7%

Market Summary

- The Upper Respiratory Tract Infection Treatment exhibits sustained expansion driven by a high frequency of seasonal illnesses and advancements in therapeutic formulations. Supply chain optimization across retail and hospital pharmacies has dramatically improved the availability of symptom-relieving medications during peak winter months, ensuring uninterrupted patient access.

- Facilities utilizing automated inventory tracking have achieved a 27% increase in fulfillment efficiency compared to traditional distribution models. The continuous rise in viral and bacterial respiratory conditions acts as a primary driver, generating strong demand for diagnostic services and targeted respiratory relief products.

- However, the market faces significant challenges due to the inappropriate use of antibiotics and the subsequent rise in resistant bacterial strains. This misuse forces regulatory bodies to impose stricter prescribing guidelines, slightly limiting the volume of antimicrobial sales.

- To counter these constraints, pharmaceutical manufacturers are heavily investing in customized biologic therapies to provide safer, more effective alternatives for chronic or severe cases.

What will be the Size of the Upper Respiratory Tract Infection Treatment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Upper Respiratory Tract Infection Treatment Market Segmented?

The upper respiratory tract infection treatment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Antibiotics

- NSAIDs and nasal decongestants

- Others

- Distribution channel

- Hospital pharmacies

- Retail pharmacies

- Online pharmacies

- Indication

- Common cold

- Sinusitis

- Pharyngitis

- Laryngitis

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- The Netherlands

- Asia

- China

- India

- Japan

- South Korea

- Indonesia

- Thailand

- Rest of World (ROW)

- North America

By Type Insights

The antibiotics segment is estimated to witness significant growth during the forecast period.

The antibiotics segment of the Upper Respiratory Tract Infection Treatment market focuses on eradicating severe pathogens to maintain operational healthcare capacity.

As bacterial etiology confirmation becomes critical in distinguishing infections from viral contagion transmission, physicians increasingly rely on viral diagnostic testing to guide treatment.

This diagnostic shift enhances antimicrobial resistance management by minimizing the misuse of broad-spectrum antimicrobial agents during seasonal respiratory outbreaks. Consequently, targeted therapies are replacing outdated protocols, improving treatment precision by 22% across primary clinics.

While addressing respiratory mucosa inflammation remains vital, modern interventions actively target acute sinus inflammation and pharyngeal tissue irritation for comprehensive recovery.

The deployment of advanced mucosal congestion relief solutions ensures faster patient discharge, reducing secondary complication rates by 15% and optimizing clinical outcomes for severe respiratory cases.

The Antibiotics segment was valued at USD 6.65 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 46.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Upper Respiratory Tract Infection Treatment Market Demand is Rising in North America Get Free Sample

The geographic landscape of the Upper Respiratory Tract Infection Treatment reveals stark operational contrasts between North America and Europe.

North America demonstrates a 35% higher investment rate in advanced drug delivery, significantly accelerating the distribution of targeted respiratory relief solutions directly to consumers.

This infrastructure shift enables US-based pharmaceutical distribution networks to improve inventory turnover by 18% during peak infection cycles. In contrast, Europe relies heavily on structured preventive healthcare awareness, prioritizing clinical oversight to ensure maximum therapeutic intervention efficacy.

European healthcare networks exhibit a 20% lower rate of unnecessary antimicrobial dispensing due to stringent regulations supporting robust antimicrobial stewardship programs.

Consequently, European systems emphasize highly accurate bacterial infection differentiation, while North American strategies prioritize the rapid commercialization of customized biologic therapies to meet surging outpatient demand.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The Upper Respiratory Tract Infection Treatment landscape is undergoing a profound structural evolution driven by the integration of sophisticated diagnostic and therapeutic solutions. Pharmaceutical supply chains are increasingly prioritizing specialized delivery systems, optimizing inventory management for novel formulations.

- As the demand for precision medicine grows, manufacturers are closely evaluating targeted immune modulation therapy efficacy to justify increased research and development allocations. Clinical facilities implementing modernized protocols have documented a 25% improvement in patient throughput compared to traditional diagnostic workflows, directly boosting operational efficiency.

- This optimization is heavily supported by rapid diagnostic technologies diagnostic accuracy, which allows practitioners to quickly distinguish between viral and bacterial pathogens. To further enhance localized care, the distribution of advanced aerosol therapies localized treatment has expanded, requiring distributors to refine cold-chain logistics and storage capabilities.

- At the administrative level, healthcare networks are accelerating AI-powered clinical decision-support adoption to streamline prescription practices and minimize inventory waste. This technological integration acts as a critical mechanism for ensuring high antimicrobial stewardship programs compliance rates across widespread pharmacy networks.

- By aligning advanced therapeutic options with robust diagnostic capabilities, the industry effectively mitigates the risks of over-prescription while maintaining highly responsive supply lines capable of addressing seasonal fluctuations in respiratory infection volumes.

What are the key market drivers leading to the rise in the adoption of Upper Respiratory Tract Infection Treatment Industry?

- The continuous rise in the incidence and prevalence of upper respiratory tract infections serves as a primary driver propelling market demand globally.

- Surging consumer demand for immediate, accessible relief is acting as a primary catalyst for the Upper Respiratory Tract Infection Treatment. Driven by robust infectious disease surveillance, public health networks are aggressively promoting proactive respiratory health management to mitigate severe outbreaks.

- This behavioral shift empowers pharmacy-based triage services, resulting in a 35% increase in decentralized patient consultations and significantly optimizing point-of-care testing systems. To capitalize on this demand, pharmaceutical developers are prioritizing advanced combination therapy formulations designed for targeted symptom alleviation.

- Furthermore, the integration of digital healthcare applications and AI-powered clinical decision-support allows facilities to streamline inventory tracking, improving order fulfillment efficiency by 22%.

- By utilizing advanced molecular diagnostics and rapid biomarker identification, companies successfully deliver evidence-based interventions directly through retail channels, maintaining consistent product availability during peak viral seasons.

What are the market trends shaping the Upper Respiratory Tract Infection Treatment Industry?

- The emergence of advanced biologic therapies represents a significant trend in the market. These innovations are expediting industry expansion by offering targeted treatment options for complex and recurring respiratory conditions.

- The rapid adoption of decentralized healthcare frameworks is fundamentally reshaping the distribution within the Upper Respiratory Tract Infection Treatment. As telemedicine consultation adoption surges, virtual care platforms have accelerated outpatient triage, reducing physical clinic congestion by 28%. This digital pivot improves clinical diagnosis accuracy, allowing providers to swiftly recommend effective non-prescription therapeutic options.

- Manufacturers are responding by scaling production of advanced non-steroidal anti-inflammatory formulations and convenient pediatric chewable tablets to support expanding self-care treatment protocols. Furthermore, the introduction of long-acting liquid suspensions directly contributes to patient compliance enhancement, improving medication adherence rates by 18%.

- Concurrently, the industry is shifting toward precision medicine approaches, driving the development of biologics focused on targeted immune modulation to address severe respiratory complications and ensuring supply chains remain highly responsive.

What challenges does the Upper Respiratory Tract Infection Treatment Industry face during its growth?

- The growing concern regarding adverse side effects associated with NSAIDs presents a critical challenge that is restraining overall industry growth.

- The structural limitation of accurately tracking high-volume patient data during initial primary care intervention presents a formidable obstacle within the Upper Respiratory Tract Infection Treatment. Facilities lacking integrated electronic health records experience a 25% higher rate of redundant clinical evaluations, significantly delaying symptomatic care management.

- The inability to rapidly assess respiratory pathogen exposure often forces clinics to bypass advanced diagnostic imaging techniques, straining local supply chains. Consequently, the inconsistent deployment of rapid diagnostic technologies limits the widespread adoption of specialized advanced aerosol therapies needed for effective localized symptom management.

- Furthermore, disjointed electronic prescription management systems increase procurement costs by 14%, challenging manufacturers to optimize production efficiency. These bottlenecks severely restrict the delivery of comprehensive supportive respiratory care, forcing administrators to overhaul logistical networks to meet fluctuating seasonal demands.

Exclusive Technavio Analysis on Customer Landscape

The upper respiratory tract infection treatment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the upper respiratory tract infection treatment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Upper Respiratory Tract Infection Treatment Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, upper respiratory tract infection treatment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - The company delivers targeted Upper Respiratory Tract Infection Treatment solutions including advanced respiratory infection therapies designed to provide rapid symptomatic relief and support comprehensive infectious disease management.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- AstraZeneca Plc

- Aurobindo Pharma Ltd.

- Bayer AG

- Cipla Inc.

- Dr. Reddys Laboratories Ltd.

- GlaxoSmithKline Plc

- Glenmark Pharmaceuticals Ltd.

- Haleon Plc

- Hikma Pharmaceuticals Plc

- Johnson and Johnson Services

- Kenvue Inc.

- Lupin Ltd.

- Merck and Co. Inc.

- Novartis AG

- Pfizer Inc.

- Procter and Gamble Co.

- Reckitt Benckiser Group Plc

- Sandoz Group AG

- Sanofi SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Upper respiratory tract infection treatment market

- In the Pharmaceuticals industry, the global implementation of stringent antimicrobial stewardship protocols has reduced the prophylactic use of high-potency antimicrobials, directly impacting Upper Respiratory Tract Infection Treatment demand by accelerating the adoption of targeted diagnostic-driven prescribing.

- The rapid integration of AI-powered clinical decision-support tools into primary care networks has enhanced the differentiation between viral and bacterial pathogens, decreasing unnecessary antibiotic dispensing rates by 18% and shifting treatment focus toward advanced aerosol therapies.

- The expansion of direct-to-consumer digital healthcare applications has streamlined telemedicine consultation adoption, increasing outpatient access to localized symptom management formulations and driving a 25% rise in over-the-counter therapeutic distribution.

- Advancements in molecular diagnostics and point-of-care testing systems have accelerated respiratory pathogen identification within clinic settings, reducing patient wait times by 30% and optimizing the utilization of precision medicine approaches for complex inflammatory conditions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Upper Respiratory Tract Infection Treatment Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 308 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 3.7% |

| Market growth 2026-2030 | USD 2509.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 3.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, UAE, Turkey, Argentina, Colombia, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Upper Respiratory Tract Infection Treatment is experiencing a critical paradigm shift as clinical operations pivot toward highly specialized diagnostic and therapeutic frameworks. By integrating point-of-care testing systems directly into outpatient workflows, healthcare facilities have achieved a 30% reduction in diagnostic processing time, accelerating patient triage during high-volume seasonal outbreaks.

- This operational efficiency is further augmented by the deployment of AI-powered clinical decision-support platforms that optimize inventory allocation for high-demand pharmaceuticals. The industry is moving aggressively toward precision medicine approaches, utilizing advanced molecular diagnostics to accurately differentiate respiratory pathogens. As a result, the reliance on broad-spectrum treatments is yielding to customized interventions based on rapid biomarker identification.

- Furthermore, pharmaceutical manufacturers are redirecting capital into the development of biologics focused on targeted immune modulation, fundamentally altering traditional product pipelines. These strategic advancements ensure that supply chains remain agile and responsive to evolving clinical demands, seamlessly aligning advanced diagnostic capabilities with targeted therapeutic distribution to optimize long-term patient care strategies.

What are the Key Data Covered in this Upper Respiratory Tract Infection Treatment Market Research and Growth Report?

-

What is the expected growth of the Upper Respiratory Tract Infection Treatment Market between 2026 and 2030?

-

USD 2.51 billion, at a CAGR of 3.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Antibiotics, NSAIDs and nasal decongestants, and Others), Distribution Channel (Hospital pharmacies, Retail pharmacies, and Online pharmacies), Indication (Common cold, Sinusitis, Pharyngitis, and Laryngitis) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising incidence and prevalence of upper respiratory tract infections, Side effects of NSAIDs decreasing market demand

-

-

Who are the major players in the Upper Respiratory Tract Infection Treatment Market?

-

Abbott Laboratories, AstraZeneca Plc, Aurobindo Pharma Ltd., Bayer AG, Cipla Inc., Dr. Reddys Laboratories Ltd., GlaxoSmithKline Plc, Glenmark Pharmaceuticals Ltd., Haleon Plc, Hikma Pharmaceuticals Plc, Johnson and Johnson Services, Kenvue Inc., Lupin Ltd., Merck and Co. Inc., Novartis AG, Pfizer Inc., Procter and Gamble Co., Reckitt Benckiser Group Plc, Sandoz Group AG and Sanofi SA

-

Market Research Insights

- The Upper Respiratory Tract Infection Treatment is transforming rapidly as healthcare providers prioritize precise diagnostic frameworks and targeted therapies. Enhanced clinical diagnosis accuracy has reduced unnecessary medication dispensing by 22%, improving overall patient safety. Providers adopting electronic health records have seen a 30% improvement in prescription tracking efficiency compared to manual systems.

- The demand for targeted interventions addressing acute sinus inflammation and pharyngeal tissue irritation continues to surge during peak infection seasons. Furthermore, advancements in specialized formulations designed for mucosal congestion relief have increased patient treatment adherence by 15%. This shift toward evidence-based pathways significantly enhances therapeutic intervention efficacy, ensuring better operational alignment for pharmaceutical distributors handling fluctuating seasonal demands.

We can help! Our analysts can customize this upper respiratory tract infection treatment market research report to meet your requirements.

RIA -

RIA -