US Primary Care Physicians Market Size 2024-2028

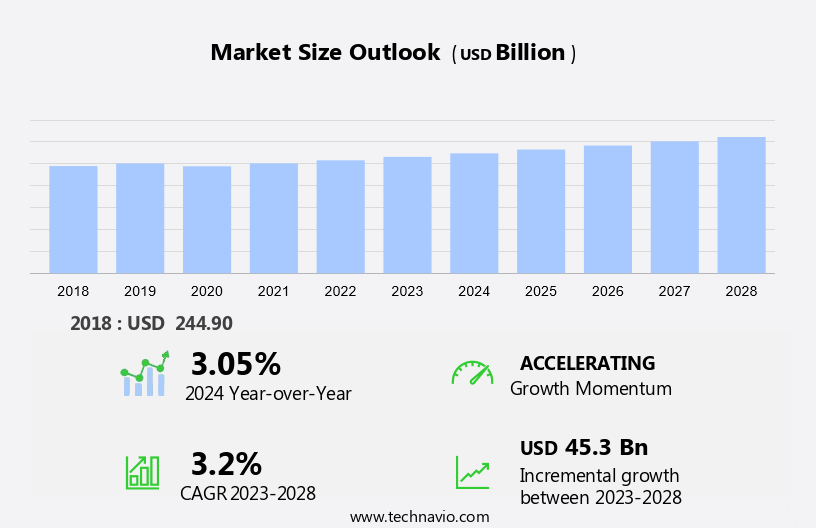

The US primary care physicians market size is forecast to increase by USD 45.3 billion at a CAGR of 3.2% between 2023 and 2028. The market is experiencing significant changes, driven by the shift towards value-based care and alternative payment models. Volume-based care, which reimburses providers based on the number of services rendered, is giving way to value-based payment models, which reward providers for delivering quality care and keeping patients healthy. This trend is impacting both independent healthcare settings and small physician practices, as well as large physician groups and hospitals. Non-physician-owned practices are also gaining ground, challenging the dominance of insurers and hospitals in the primary care landscape. Telehealth integration is another key trend, enabling remote consultations and improving access to care, particularly in rural areas.

However, challenges remain, including physician shortages in primary care and the need for technological infrastructure to support value-based care. Demographic shifts and an aging population are further fueling demand for primary care services. As the healthcare industry continues to evolve, primary care physicians will play a crucial role in delivering cost-effective, high-quality care to patients.

The market is a significant segment of the healthcare industry, encompassing various specialties including family medicine, internal medicine, pediatrics, and geriatrics. These primary care providers play a crucial role in managing chronic conditions, delivering preventive care, and coordinating patient care across various healthcare settings. A general pediatric physician plays a crucial role in patient counselling within point of care settings, ensuring that families receive timely advice and support during visits to the outpatient department. These primary care providers employ various models, such as direct primary care and concierge services, to enhance patient engagement and improve health outcomes.

Furthermore, primary care providers, including family physicians, internal medicine specialists, pediatricians, geriatricians, and others, are at the forefront of managing these chronic diseases. They work in various settings, such as medical clinics, hospitals, long-term care facilities, and outpatient departments, to ensure comprehensive care for their patients. Family medicine and internal medicine specialists focus on the overall health and well-being of their patients, while pediatricians specialize in the care of infants, children, and adolescents. Geriatricians, on the other hand, are dedicated to the healthcare needs of older adults.

Moreover, telehealth services have gained increasing popularity in recent years, allowing primary care providers to offer remote consultations and follow-up appointments. This is particularly beneficial for Medicare beneficiaries who may have mobility issues or live in rural areas with limited access to healthcare facilities. Primary care providers also play a significant role in health promotion and patient counseling. They work closely with their patients to help them make informed decisions about their health, including the use of drugs and lifestyle modifications. In addition, they collaborate with specialists and other healthcare professionals to ensure coordinated care for their patients. The primary care providers market in the US is diverse and complex, with various stakeholders, including employed physicians, medical clinics, hospitals, and long-term care facilities.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Age Group

- Infants

- Geriatrics

- Pediatrics

- Adults

- Type

- General practice family physician and geriatrics

- General internal medicine

- General pediatrics

- Service Type

- Physical

- Virtual

- Geography

- US

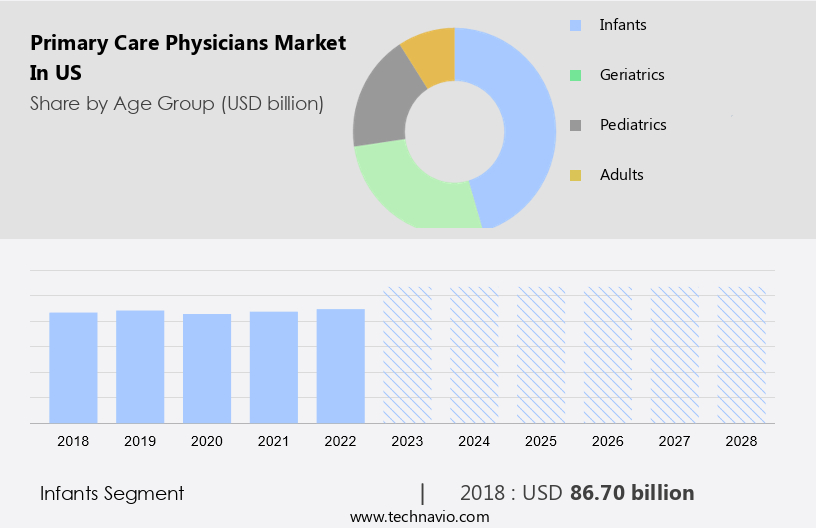

By Age Group Insights

The Infants segment is estimated to witness significant growth during the forecast period. In the United States primary care physicians market, primary care doctors, including pediatricians and family practitioners, play a significant role in delivering healthcare services to infants, children, and adolescents. Primary care visits are essential for newborns, kids, and teenagers, providing vital services such as well-baby and well-child exams, growth and developmental evaluations, vaccinations, and advice on infant nutrition and safety. These visits are crucial for monitoring a child's overall health and ensuring they reach developmental milestones. The first few years of a child's life involve numerous vaccinations, which must be administered by primary care providers according to recommended schedules. In addition, the increasing adoption of telehealth and virtual care services by health plans and corporate-owned practices is expanding the reach of primary care services, making healthcare more accessible to communities and medical centers across the US.

Get a glance at the market share of various segments Request Free Sample

The infants segment was valued at USD 86.70 billion in 2018 and showed a gradual increase during the forecast period.

Our market researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Demographic shifts and aging population is the key driver of the market. The aging population in the United States is driving the demand for primary care providers, including family medicine, internal medicine, and pediatric specialists. With an increasing number of Americans reaching retirement age and living longer due to advancements in healthcare, the need for primary care physicians to manage chronic conditions and provide preventive care is becoming more crucial.

Furthermore, the primary care market is expanding to accommodate this growing need, as older adults often require ongoing medical attention and support for conditions such as Type 2 diabetes, heart disease, and arthritis. Primary care models, such as direct primary care, are gaining popularity due to their focus on personalized care and cost savings. As the US population continues to age, the importance of primary care providers in managing chronic conditions and delivering preventive care will only become more significant.

Market Trends

Telehealth integration is the upcoming trend in the market. The market is experiencing a significant transformation through the integration of volume-based care and value-based payment models. In independent healthcare settings and small practices, as well as large physician groups and hospitals, this shift is taking place. Telehealth, a crucial aspect of this evolution, enables the delivery of healthcare services via electronic communication technology, including consultations, diagnostics, monitoring, and education.

Furthermore, this innovation expands access to primary care, particularly for patients in rural or underserved areas, reducing the need for travel and in-person visits. The convenience of telehealth leads to higher patient engagement and enhanced satisfaction. Insurers are increasingly supporting this trend, recognizing its potential to improve healthcare efficiency and effectiveness.

Market Challenge

Physician shortages in primary care is a key challenge affecting the market growth. The United States faces a persistent shortage of primary care physicians, leading to challenges in the healthcare system and limited access to essential medical services for some patients. This issue is particularly pronounced in underserved rural and urban areas, where physician shortages exacerbate healthcare disparities. Patients in these regions may endure longer wait times for appointments and travel significant distances to receive primary care services. Concerns over physician shortages have led to various solutions, including the adoption of concierge services by some primary care physicians. These services offer patients direct access to their doctors, often for a fee, and can help address the issue of limited availability.

Furthermore, both Medicare and private insurance providers are working to address the shortage through different means. Medicare, for example, has initiatives aimed at increasing the number of primary care physicians in underserved areas through salary-based compensation models and physician organizations. Private insurance providers, on the other hand, are increasingly employing primary care physicians under volume-based compensation models. Value-based care is another approach gaining traction in the primary care sector. This model incentivizes physicians to focus on preventative care and patient outcomes, rather than just the number of patients seen. By promoting a more holistic approach to care, value-based care has the potential to improve patient outcomes and reduce the overall burden on the healthcare system.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Amazon.com Inc. - The company offers care physicians services such as chronic conditions, everyday care, and wellness and prevention.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Apollo Asset Management Inc.

- Cedars Sinai Health System

- ChenMed LLC

- Colonial Healthcare

- Colorado Primary Health Care

- Crossover Health

- Duly Health and Care

- MDVIP

- New West Physicians

- Premier Medical Associates

- Privia Health Group Inc.

- Pure Family Medicine

- Rhode Island Primary Care Physicians Corp.

- The Cleveland Clinic Foundation

- The General Hospital Corp.

- The Nemours Foundation

- UCSF Health

- Trinity Health

- United Health Group Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Primary care providers play a crucial role in the US healthcare system, encompassing various specialties such as family medicine, internal medicine, pediatrics, and others. These specialists focus on providing comprehensive care for patients, managing chronic conditions, and delivering preventive care. Primary care models have evolved, with direct primary care and concierge services offering more personalized care. Medicare and private insurance providers reimburse primary care physicians differently, with employed physicians often receiving salary-based compensation, while independent practices may rely on volume-based compensation. Physician organizations, hospitals, and large groups also employ primary care providers. Value-based care is increasingly popular, with volume-based care and value-based payment models incentivizing quality patient care.

Furthermore, non-physician-owned practices, small healthcare settings, and large corporate-owned practices all offer primary care services. Community health centers, medical centers, and outpatient departments also provide essential primary care services. Telehealth and virtual care services have expanded access to primary care, enabling geriatrics, family physicians, pediatricians, and other specialists to consult with patients remotely. Teleconsultation, health promotion, disease prevention, patient counseling, and long-term care facilities are some areas where telehealth services have made a significant impact. Primary care providers address various chronic diseases, hospitalizations, and the need for drugs, offering crucial services for managing and preventing health issues. Obstetrics and gynecology, geriatrics, and other specialties are integral to primary care, ensuring comprehensive care for diverse patient populations.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

142 |

|

Base year |

2023 |

|

Historic period |

2017-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.2% |

|

Market growth 2024-2028 |

USD 45.3 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.05 |

|

Key companies profiled |

Amazon.com Inc., Apollo Asset Management Inc., Cedars Sinai Health System, ChenMed LLC, Colonial Healthcare, Colorado Primary Health Care, Crossover Health, Duly Health and Care, MDVIP, New West Physicians, Premier Medical Associates, Privia Health Group Inc., Pure Family Medicine, Rhode Island Primary Care Physicians Corp., The Cleveland Clinic Foundation, The General Hospital Corp., The Nemours Foundation, UCSF Health, Trinity Health, and United Health Group Inc. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -