Veterinary Chemistry Analyzers Market Size 2025-2029

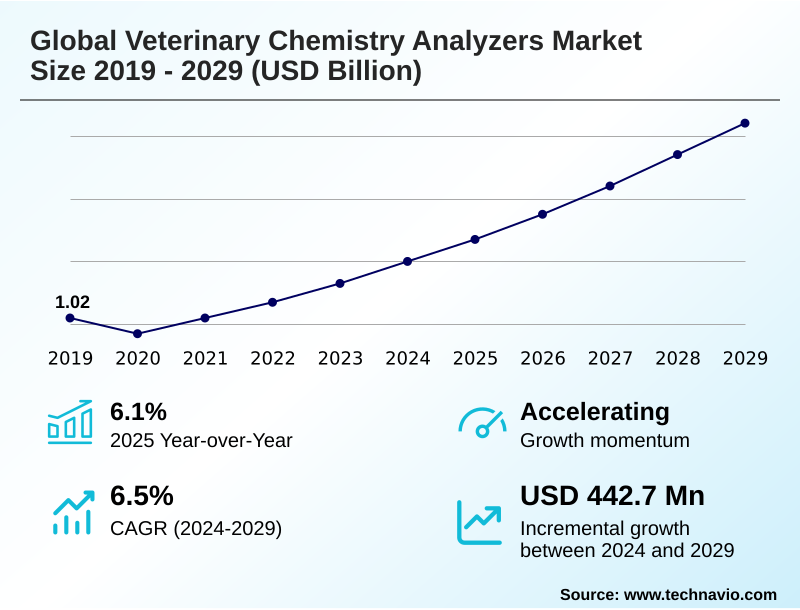

The veterinary chemistry analyzers market size is valued to increase by USD 442.7 million, at a CAGR of 6.5% from 2024 to 2029. Ascendancy of companion animal ownership and humanization trend will drive the veterinary chemistry analyzers market.

Major Market Trends & Insights

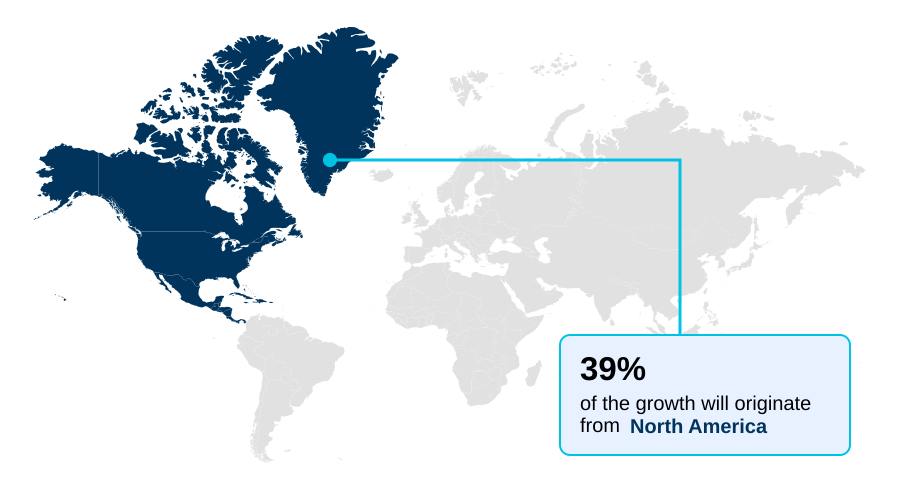

- North America dominated the market and accounted for a 39.1% growth during the forecast period.

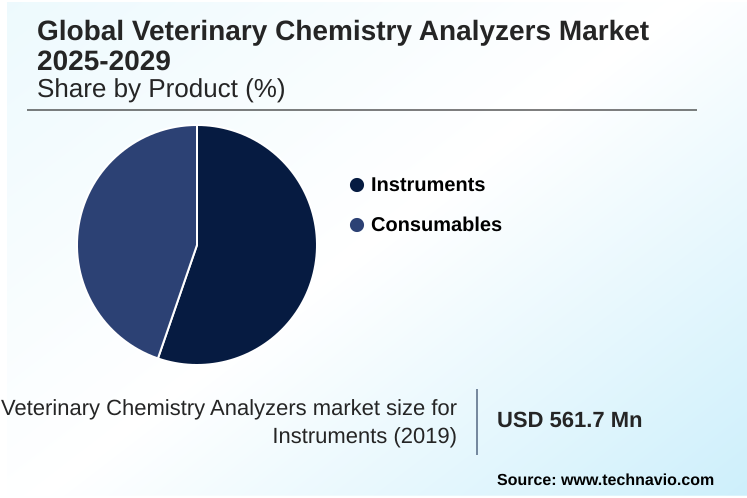

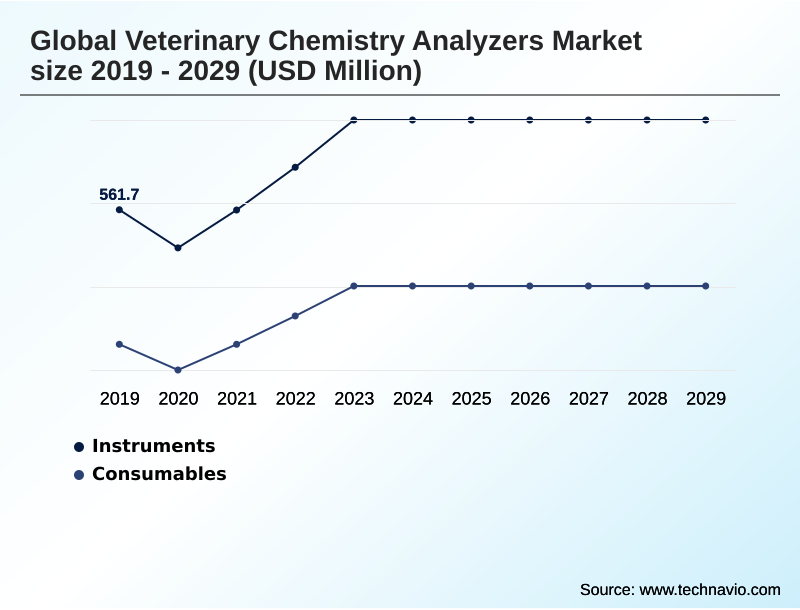

- By Product - Instruments segment was valued at USD 633.3 million in 2023

- By Type - Benchtop analyzers segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 627.8 million

- Market Future Opportunities: USD 442.7 million

- CAGR from 2024 to 2029 : 6.5%

Market Summary

- The veterinary chemistry analyzers market is defined by its role in advancing animal healthcare through sophisticated in-vitro diagnostic instruments. These systems perform automated biochemical analysis on samples, providing critical data for disease detection, management, and preventive care in both companion and production animals.

- Key drivers include the humanization of pets, which elevates owner expectations for care standards, and the economic necessity of herd health management in livestock industries. A primary trend is the dual development of compact point-of-care testing (POCT) devices for in-clinic use and high-throughput automation in central reference labs.

- For instance, a small animal clinic can leverage a benchtop chemistry analyzer to perform immediate pre-anesthetic screening, significantly improving patient safety and operational workflow efficiency without delaying surgical procedures. However, the high capital investment and recurring reagent costs associated with closed-system platforms present a persistent challenge, influencing purchasing decisions and market penetration, especially within smaller, independent practices.

- Technological innovation focuses on enhancing the diagnostic test menu, improving user-friendliness, and enabling better data integration with practice management software.

What will be the Size of the Veterinary Chemistry Analyzers Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Veterinary Chemistry Analyzers Market Segmented?

The veterinary chemistry analyzers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Instruments

- Consumables

- Type

- Benchtop analyzers

- Automated analyzers

- Portable analyzers

- Application

- Blood chemistry analysis

- Electrolyte and gas analysis

- Urinalysis

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Product Insights

The instruments segment is estimated to witness significant growth during the forecast period.

The instruments segment represents the market's foundational capital investment, with physical analyzers defining a clinic's diagnostic capacity and operational efficiency. Continuous innovation in photometry analysis, ion-selective potentiometry, and microfluidics technology fuels regular upgrade cycles.

These systems provide critical clinical pathology data and are essential for veterinary immunoassay applications and comprehensive test result validation. Advanced hardware using rotor-based analysis is designed for high efficiency, with integrated systems reducing administrative errors by up to 25%.

This core hardware supports a wide range of applications, from veterinary hematology integration and specialized endocrinology testing panels to exotic animal diagnostics, ensuring its indispensable role.

The use of precise calibrator solutions for large animal veterinary services further underpins their market value.

The Instruments segment was valued at USD 633.3 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

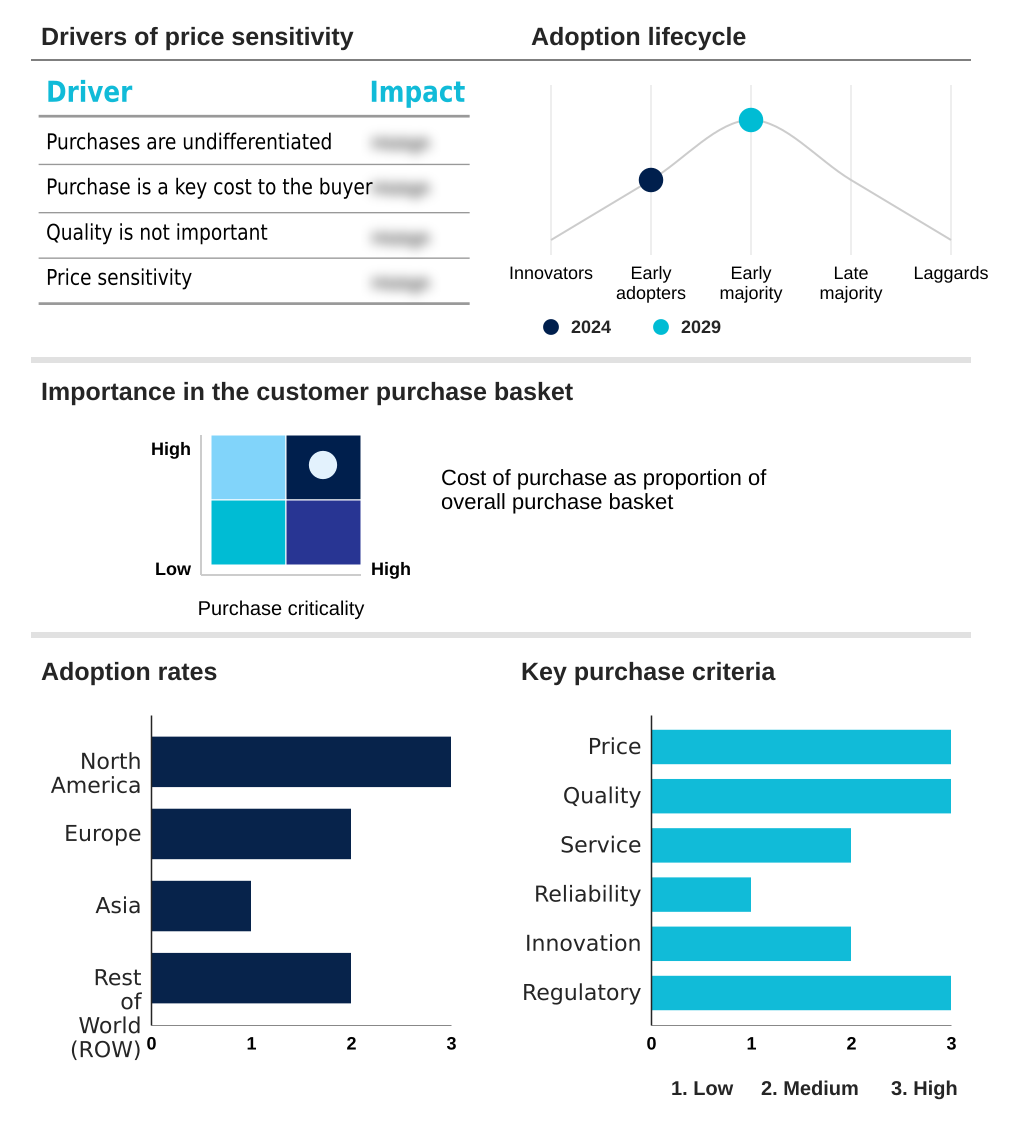

North America is estimated to contribute 39.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Veterinary Chemistry Analyzers Market Demand is Rising in North America Get Free Sample

The geographic landscape is led by North America, which has a mature in-house laboratory setup focused on automated clinical chemistry to ensure high veterinary diagnostic accuracy.

This region's reliance on in-vitro diagnostic instruments for routine biochemical analysis makes it the largest market segment. In contrast, Asia is the fastest-growing region, with expanding livestock disease surveillance and herd health management programs driving demand.

The adoption of instruments utilizing dry-slide technology, which have lower sample volume requirements for animal serum testing, plasma sample analysis, and urine sample analysis, is increasing in emerging markets.

Across all regions, adherence to validated quality control (QC) materials and species-specific veterinary reference intervals is becoming standard, with modern systems reducing test processing times by over 40%.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions within the veterinary chemistry analyzers market are increasingly complex, balancing technology, cost, and clinical utility. The debate over benchtop vs portable veterinary analyzers often centers on the specific needs of a practice, whether for in-clinic blood testing for dogs and cats or for mobile field diagnostics.

- The total cost of ownership calculation is paramount, as veterinary chemistry analyzer reagent costs for high-throughput systems for reference labs can be substantial. Clinics must evaluate the long-term expense of proprietary consumables against the efficiency gains from urinalysis automation in veterinary medicine and the accuracy of point-of-care chemistry analyzers.

- The integration of analyzers with veterinary software is now a critical purchasing criterion, as it is key to improving turnaround time with in-house diagnostics and streamlining workflows for managing chronic kidney disease in pets or performing routine liver function tests for companion animals. The choice between dry-slide vs wet chemistry analyzers also impacts operational costs and maintenance schedules.

- For specialized applications, such as biochemical profiling for equine health or electrolyte analysis for critical care, the availability of specific test panels on a platform is non-negotiable.

- Practices utilizing microfluidic analyzers for veterinary use often report higher client satisfaction due to faster results, with some showing client compliance rates for follow-up care that are 50% higher than clinics relying solely on external labs.

What are the key market drivers leading to the rise in the adoption of Veterinary Chemistry Analyzers Industry?

- The sustained growth in companion animal ownership, coupled with the increasing humanization of pets, serves as the primary driver for demand in advanced veterinary diagnostics.

- The primary market driver is the rise of companion animal diagnostics, fueled by an emphasis on preventive care screening and sophisticated chronic disease monitoring.

- This creates demand for instruments with a broad diagnostic test menu, including species-specific assays and panels for pre-anesthetic screening. This trend justifies the capital equipment investment in systems capable of precise enzyme measurement, metabolite measurement, and hormone measurement.

- For example, the availability of specific renal function markers and hepatic function tests improves clinical decision support, with practices using these panels reporting a 20% increase in early-stage disease detection.

- The ability to perform multi-parameter testing in a single run enhances efficiency, making advanced diagnostics a standard component of modern veterinary care.

What are the market trends shaping the Veterinary Chemistry Analyzers Industry?

- A defining market trend is the proliferation of point-of-care testing solutions for immediate in-clinic diagnostics, which coexists with the ongoing consolidation of high-volume, complex testing within large reference laboratories.

- Market trends are defined by a dual movement toward decentralized point-of-care testing (POCT) and centralized high-throughput automation. The proliferation of in-clinic diagnostic solutions, including compact portable chemistry analyzer and benchtop chemistry analyzer models, is shortening test result turnaround time to under 15 minutes in many cases.

- This shift optimizes the veterinary diagnostics workflow for small animal clinic diagnostics and large animal veterinary services alike, providing real-time test results through a user-friendly interface. Simultaneously, reference laboratory integration is becoming more seamless, with data flowing directly into practice management software (PIMS).

- This hybrid model allows clinics to balance immediate diagnostic needs with the comprehensive testing capabilities of large, automated labs, which report over 99% consistency in results.

What challenges does the Veterinary Chemistry Analyzers Industry face during its growth?

- High initial acquisition costs and ongoing operational expenses for diagnostic systems pose a significant financial challenge for many veterinary practices, limiting technology adoption.

- Financial considerations represent a significant challenge, with the total cost of ownership (TCO) of a closed-system platform being a primary barrier. High diagnostic reagent pricing and instrument maintenance contracts strain budgets. The capital equipment investment in a semi-automated analyzer using proprietary reagent disk technology or liquid reagent systems is substantial.

- To mitigate this, reagent rental models are emerging, improving clinic cash flow by over 30%. The need for quality control (QC) materials and calibrator solutions adds to expenses. Technology choices are complex, weighing the benefits of biosensor technology or reflectometer photometry against the costs of future molecular diagnostics integration or a full diagnostic workstation integration.

Exclusive Technavio Analysis on Customer Landscape

The veterinary chemistry analyzers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the veterinary chemistry analyzers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Veterinary Chemistry Analyzers Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, veterinary chemistry analyzers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Abbott Laboratories - Key offerings include advanced handheld systems providing rapid, quantitative in-clinic diagnostics to enable immediate point-of-care clinical decisions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Abbott Laboratories

- Antech Diagnostics, Inc.

- Arkray USA Inc.

- Chengdu Seamaty Technology

- DiaSys Diagnostic Systems

- Diconex SA

- ELITechGroup SAS

- Eurolyser Diagnostics GmbH

- HORIBA Ltd.

- IDEXX Laboratories Inc.

- Labomed Inc.

- Neogen Corp.

- NeoMedica

- Randox Laboratories Ltd.

- Scil Animal Care Co. GmbH

- Skyla Corp.

- Tianjin LOCMEDT Technologies

- Ushio Inc.

- Zoetis Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Veterinary chemistry analyzers market

- In September 2024, Zoetis Inc. launched Vetscan OptiCell, a new platform designed to transform veterinary diagnostics with an integrated suite of products and services.

- In November 2024, Abbott Laboratories announced a strategic partnership with a leading practice management software provider to embed its i-STAT handheld system data directly into veterinary clinic workflows.

- In January 2025, IDEXX Laboratories Inc. acquired a specialized European diagnostics company, expanding its portfolio with novel immunoassay technologies and strengthening its market presence in the region.

- In April 2025, Randox Laboratories Ltd. received regulatory clearance for a new biochip array focused on equine metabolic syndromes, offering a comprehensive diagnostic panel for horse-specific conditions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Veterinary Chemistry Analyzers Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 288 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.5% |

| Market growth 2025-2029 | USD 442.7 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 6.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, UAE, Turkey, Argentina, Colombia, South Africa and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market's evolution is driven by increasingly sophisticated in-vitro diagnostic instruments. Boardroom decisions now weigh capital investment in a benchtop chemistry analyzer with high-throughput automation against the flexibility of a portable chemistry analyzer for point-of-care testing (POCT). The core technology, from photometry analysis and ion-selective potentiometry to advanced biosensor technology and microfluidics technology, is advancing rapidly.

- A key differentiator is the breadth of the diagnostic test menu, which must include species-specific assays and robust veterinary immunoassay capabilities for pre-anesthetic screening. Systems using dry-slide technology compete with those using liquid reagent systems or reagent disk technology. The goal is to deliver real-time test results for everything from enzyme measurement, electrolyte measurement, and metabolite measurement to hormone measurement.

- This is achieved via rotor-based analysis and reflectometer photometry on both semi-automated analyzer and automated clinical chemistry platforms. The seamless diagnostic workstation integration of clinical pathology data from animal serum testing, plasma sample analysis, and urine sample analysis is critical.

- Leading systems offer multi-parameter testing and aim for molecular diagnostics integration within a user-friendly interface, moving beyond the constraints of a simple closed-system platform to provide comprehensive biochemical analysis.

What are the Key Data Covered in this Veterinary Chemistry Analyzers Market Research and Growth Report?

-

What is the expected growth of the Veterinary Chemistry Analyzers Market between 2025 and 2029?

-

USD 442.7 million, at a CAGR of 6.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Instruments, and Consumables), Type (Benchtop analyzers, Automated analyzers, and Portable analyzers), Application (Blood chemistry analysis, Electrolyte and gas analysis, and Urinalysis) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Ascendancy of companion animal ownership and humanization trend, High costs and budgetary constraints in veterinary practice

-

-

Who are the major players in the Veterinary Chemistry Analyzers Market?

-

Abbott Laboratories, Antech Diagnostics, Inc., Arkray USA Inc., Chengdu Seamaty Technology, DiaSys Diagnostic Systems, Diconex SA, ELITechGroup SAS, Eurolyser Diagnostics GmbH, HORIBA Ltd., IDEXX Laboratories Inc., Labomed Inc., Neogen Corp., NeoMedica, Randox Laboratories Ltd., Scil Animal Care Co. GmbH, Skyla Corp., Tianjin LOCMEDT Technologies, Ushio Inc. and Zoetis Inc.

-

Market Research Insights

- Market dynamics are shaped by the dual pursuit of immediate clinical decision support and comprehensive, cost-effective analytics. This has led to high adoption rates for in-clinic diagnostic solutions, with many practices reporting a 25% faster test result turnaround time compared to external labs.

- The emphasis on chronic disease monitoring and preventive care screening is driving investment in systems that enhance veterinary diagnostic accuracy. Strategic decisions are influenced by total cost of ownership (TCO) calculations, as recurring diagnostic reagent pricing can exceed initial capital equipment investment.

- Consequently, flexible reagent rental models are gaining traction, improving cash flow for small animal clinic diagnostics by up to 30%. The integration with practice management software (PIMS) remains a critical factor, directly impacting veterinary diagnostics workflow and data management.

We can help! Our analysts can customize this veterinary chemistry analyzers market research report to meet your requirements.

RIA -

RIA -