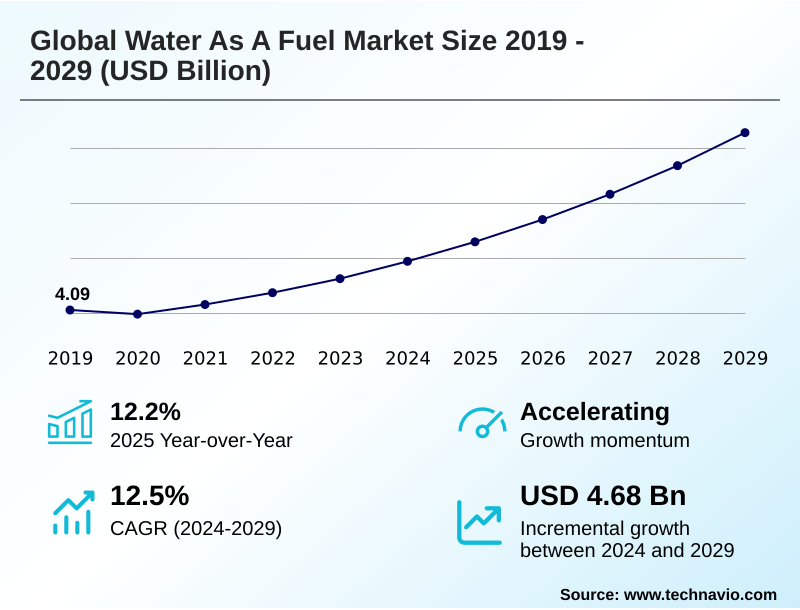

Water As A Fuel Market Size 2025-2029

The water as a fuel market size is valued to increase by USD 4.68 billion, at a CAGR of 12.5% from 2024 to 2029. Global decarbonization policies and net-zero commitments will drive the water as a fuel market.

Major Market Trends & Insights

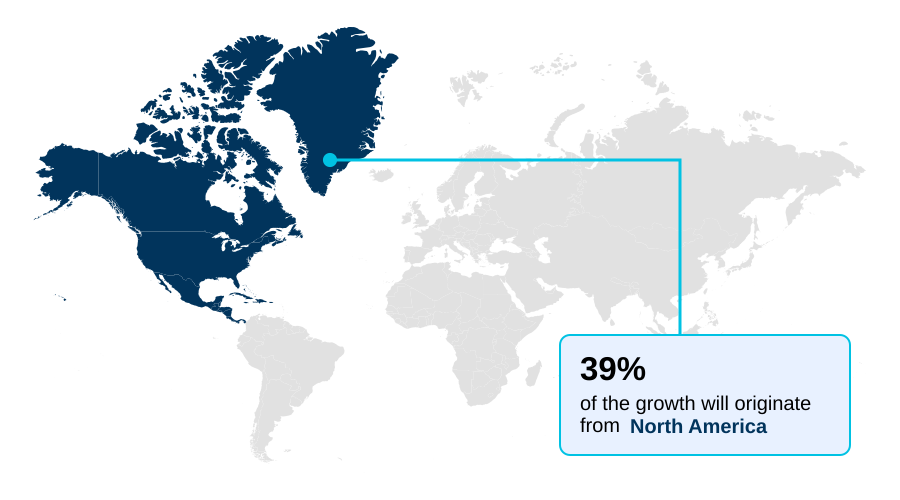

- North America dominated the market and accounted for a 39.3% growth during the forecast period.

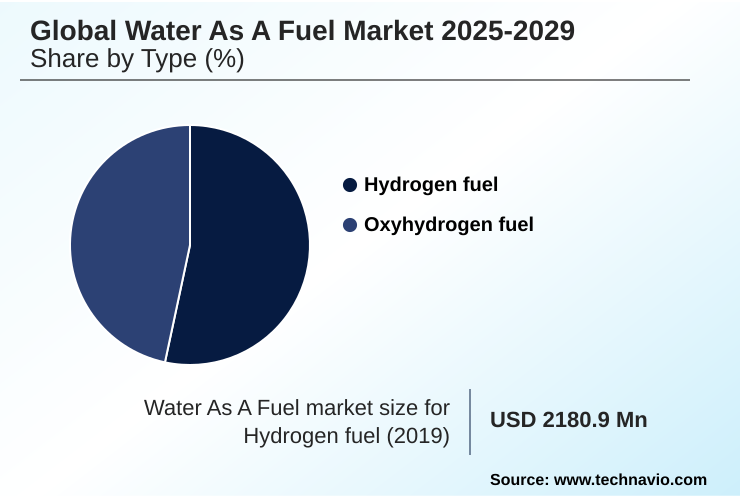

- By Type - Hydrogen fuel segment was valued at USD 2.85 billion in 2023

- By Technology - Natural gas reforming segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 6.45 billion

- Market Future Opportunities: USD 4.68 billion

- CAGR from 2024 to 2029 : 12.5%

Market Summary

- The water as a fuel market is foundational to the global energy transition, driven by the dual imperatives of achieving net-zero emissions and enhancing energy security. This market centers on producing hydrogen from water via electrolysis, a process that, when powered by renewables, yields a zero-emission energy carrier.

- A key trend is the strategic development of hydrogen hubs that co-locate production with industrial offtake, creating economies of scale. However, the sector faces significant hurdles, including the high production cost of green hydrogen compared to fossil-based alternatives and the lack of dedicated storage and transport infrastructure.

- For instance, a global logistics firm seeking to decarbonize its fleet must weigh the rapid refueling of hydrogen-powered trucks, which can restore full range in minutes, against the operational complexities and capital costs of establishing a private hydrogen refueling network, illustrating the practical trade-offs that define the current market landscape.

What will be the Size of the Water As A Fuel Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Water As A Fuel Market Segmented?

The water as a fuel industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

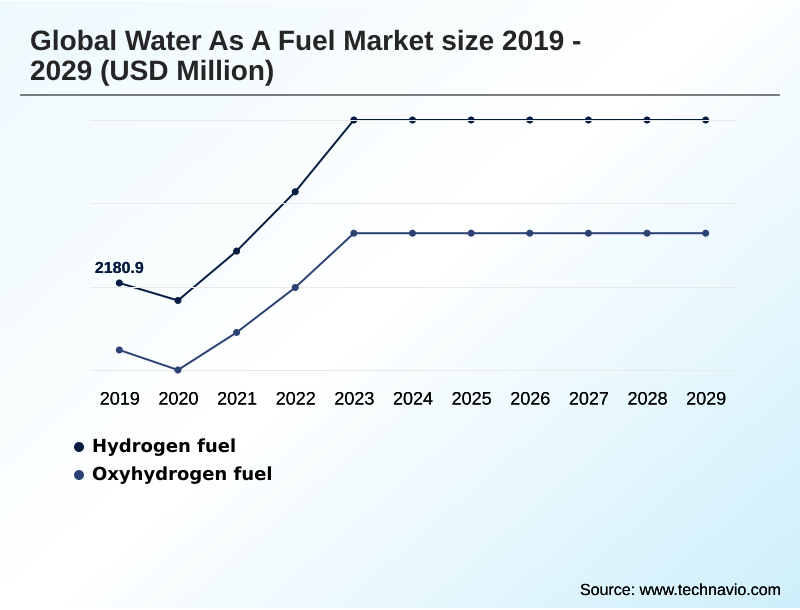

- Hydrogen fuel

- Oxyhydrogen fuel

- Technology

- Natural gas reforming

- Electrolysis

- End-user

- Transportation

- Power generation

- Material handling equipment

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- South Africa

- UAE

- Saudi Arabia

- Rest of World (ROW)

- North America

By Type Insights

The hydrogen fuel segment is estimated to witness significant growth during the forecast period.

The hydrogen fuel segment is pivotal, focusing on producing high-purity hydrogen for applications where battery power is insufficient.

In the push for zero-emission transportation solutions and clean mobility solutions, this segment powers hydrogen fuel cell systems and advanced fuel cell powertrain designs.

This is central to the national hydrogen strategy of many countries aiming for the decarbonization of heavy industry.

For heavy-duty hydrogen-powered mobility, refueling from compressed hydrogen storage takes minutes, a significant operational advantage that reduces downtime by over 95% compared to battery charging.

Development of integrated hydrogen hubs and hydrogen valley development projects supports the necessary hydrogen refueling stations infrastructure, targeting hard-to-abate sector decarbonization. This contrasts with niche applications like stoichiometric oxyhydrogen combustion.

The Hydrogen fuel segment was valued at USD 2.85 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Water As A Fuel Market Demand is Rising in North America Get Free Sample

The geographic landscape is defined by a division between production and consumption hubs, fostering a global hydrogen economy ecosystem.

Regions with favorable renewable energy integration, such as Australia and Chile, are developing giga-scale export projects focused on industrial hydrogen feedstock and derivatives.

In Europe, proton exchange membrane electrolysis is favored for its flexibility, while solid oxide electrolysis cell technology is explored for high-efficiency industrial process decarbonization.

In North America, the focus includes on-site hydrogen generation and retrofitting power plants with hydrogen-ready gas turbines. The US, accounting for almost 40% of incremental growth, is advancing the direct reduced iron process for green steel production.

Mature technologies like alkaline water electrolysis enable cost-effective green industrial feedstock production, enhancing grid stability and balancing.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The trajectory of the global water as a fuel market hinges on resolving several interconnected factors, beginning with the economic viability of green hydrogen versus blue hydrogen, where policy incentives play a critical role.

- A primary focus is the cost reduction in electrolysis technology for green hydrogen, which is being driven by scaling up electrolyzer manufacturing for cost parity with conventional methods. This effort is complemented by extensive water as a fuel research and development and advancements in proton exchange membrane fuel cells, alongside parallel work on solid oxide electrolysis for high-efficiency hydrogen.

- The integration of renewables for hydrogen production is fundamental, but the industry concurrently faces significant challenges in hydrogen storage and distribution infrastructure. Policy impact on clean hydrogen production investments is crucial for underwriting the supply chain for green hydrogen export and establishing technical standards for cross-border hydrogen trade.

- The role of hydrogen in long-duration grid energy storage and its use in hydrogen fuel cells for stationary power generation are key to grid stability.

- Ultimately, success lies in using green hydrogen for industrial process decarbonization, developing hydrogen hubs for industrial clusters, and decarbonizing heavy-duty transport with hydrogen fuel cells, all while exploring green ammonia as a carrier for hydrogen trade and the potential of hydrogen as a fuel in the aviation industry.

- The viability of steam methane reforming with carbon capture and the impact of geopolitics on hydrogen energy security remain important considerations.

What are the key market drivers leading to the rise in the adoption of Water As A Fuel Industry?

- Global decarbonization policies and net-zero commitments are the primary drivers for the market, compelling industries to adopt water-derived hydrogen to meet stringent emissions targets.

- The market is propelled by robust climate policy frameworks and binding net-zero emissions targets that mandate a shift toward cleaner energy.

- This top-down push from global decarbonization policies creates demand for green hydrogen production, which is supported by incentives like the hydrogen production tax credit.

- These policies stimulate investment in advanced electrolysis technology to lower electrolyzer capital expenditure, crucial for achieving a low-carbon hydrogen standard.

- The adoption of renewable fuels of non-biological origin is becoming a core tenet of strategic energy independence, helping companies with future-proofing industrial operations.

- By securing long-term renewable power purchase agreements, producers can ensure a viable zero-emission fuel cycle, reducing industrial carbon footprints by more than 70% in targeted applications.

What are the market trends shaping the Water As A Fuel Industry?

- A key market trend is the development of large-scale hydrogen hubs and valleys. This approach co-locates production and consumption to create economies of scale and de-risk investments.

- A significant trend is the focus on hydrogen derivatives as the primary medium for cross-border hydrogen trade and establishing a seaborne hydrogen commodity market. Green ammonia production and green methanol production offer a more practical alternative to liquefied hydrogen transport, as they are denser energy carriers and can leverage existing infrastructure, facilitating their role as a clean energy export commodity.

- This pragmatic approach simplifies the hydrogen supply chain, with cryogenic liquid hydrogen reserved for specific applications. These sustainable maritime fuels are essential for reducing energy import dependency reduction. The build-out of pan-european hydrogen infrastructure and giga-scale green hydrogen projects accelerates this trend, with project financing for export-oriented facilities increasing by 40% in the last year.

What challenges does the Water As A Fuel Industry face during its growth?

- The high production cost of green hydrogen and its overall economic viability compared to conventional fuels remain a key challenge affecting industry growth.

- Key challenges temper market expansion, centering on the hydrogen production cost and the need to scale electrolyzer manufacturing capacity to achieve economies of scale. While water electrolysis technology is central, competition from the incumbent steam methane reforming process and autothermal reforming technology—even with carbon capture and storage—remains significant.

- The push for grey hydrogen substitution is hampered by the lack of a pervasive hydrogen infrastructure backbone and decentralized energy networks. Creating resilient energy systems requires immense investment coordination.

- Energy transition pathways are further complicated by the need for sector coupling strategies to balance supply and demand, with infrastructure gaps representing an investment deficit at least 20 times larger than current annual spending. A circular carbon economy model is still aspirational for this sector.

Exclusive Technavio Analysis on Customer Landscape

The water as a fuel market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the water as a fuel market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Water As A Fuel Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, water as a fuel market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Air Liquide SA - Delivers integrated hydrogen solutions, from electrolysis-based production to advanced fuel cell applications for clean energy generation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Air Liquide SA

- Ballard Power Systems Inc.

- Bloom Energy Corp.

- Cummins Inc.

- Enel Spa

- ENGIE SA

- Exxon Mobil Corp.

- FuelCell Energy Inc.

- Iberdrola SA

- ITM Power PLC

- Linde Plc

- McPhy Energy SA

- Nel ASA

- Orsted AS

- Panasonic Holdings Corp.

- Plug Power Inc.

- Siemens Energy AG

- Sinopec Shanghai Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Water as a fuel market

- In September 2024, the governments of Germany and Australia solidified their bilateral Hydrogen Accord with a joint declaration to accelerate the development of a green hydrogen supply chain between the two nations.

- In November 2024, Cummins Inc. announced the commercial rollout of its new generation of PEM electrolyzers, designed to increase green hydrogen output efficiency by 15% while reducing the use of scarce platinum group metals.

- In January 2025, Air Liquide SA and the Port of Rotterdam jointly announced the final investment decision for a 200 MW electrolyzer plant, a key project for the port's ambition to become a major European hydrogen hub.

- In March 2025, NEOM Green Hydrogen Co. confirmed the start of commercial operations for the first phase of its mega-plant, initiating the first shipments of green ammonia to targeted European and Asian markets.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Water As A Fuel Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 12.5% |

| Market growth 2025-2029 | USD 4678.7 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 12.2% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Colombia, South Africa, UAE, Saudi Arabia, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is fundamentally reshaping the energy landscape, moving beyond niche applications toward becoming a cornerstone of industrial strategy. Boardroom decisions are now centered on the long-term capital allocation for grey hydrogen substitution, leveraging clean hydrogen production as a competitive differentiator.

- This involves assessing the entire hydrogen supply chain, from sourcing water for electrolysis technology to the logistics of liquefied hydrogen transport. A key deliberation is the investment in industrial hydrogen feedstock for processes like the direct reduced iron process, versus deploying hydrogen-powered mobility solutions.

- The viability of on-site hydrogen generation using advanced electrolysis technology, such as proton exchange membrane electrolysis or solid oxide electrolysis cell systems, is a critical variable. These systems, supported by incentives like the hydrogen production tax credit, can achieve a 20% lower operational cost in regions with low-cost renewables.

- The conversation also includes hydrogen-ready gas turbines and hydrogen combustion engines, which offer pathways for decarbonizing existing assets. Strategic planning must navigate the complexities of hydrogen embrittlement issues in existing infrastructure and the high cost of compressed hydrogen storage and hydrogen refueling stations.

- Firms are evaluating the transition from steam methane reforming process and autothermal reforming technology, with or without carbon capture and storage, to true zero-emission fuel cycle pathways using high-purity hydrogen.

What are the Key Data Covered in this Water As A Fuel Market Research and Growth Report?

-

What is the expected growth of the Water As A Fuel Market between 2025 and 2029?

-

USD 4.68 billion, at a CAGR of 12.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Hydrogen fuel, and Oxyhydrogen fuel), Technology (Natural gas reforming, and Electrolysis), End-user (Transportation, Power generation, Material handling equipment, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Global decarbonization policies and net-zero commitments, High production cost and economic viability

-

-

Who are the major players in the Water As A Fuel Market?

-

Air Liquide SA, Ballard Power Systems Inc., Bloom Energy Corp., Cummins Inc., Enel Spa, ENGIE SA, Exxon Mobil Corp., FuelCell Energy Inc., Iberdrola SA, ITM Power PLC, Linde Plc, McPhy Energy SA, Nel ASA, Orsted AS, Panasonic Holdings Corp., Plug Power Inc., Siemens Energy AG and Sinopec Shanghai Co. Ltd.

-

Market Research Insights

- The market's dynamics are shaped by a strategic push for energy import dependency reduction and the decarbonization of heavy industry. Supportive climate policy frameworks are accelerating the development of a hydrogen economy ecosystem, with a focus on sector coupling strategies to enhance grid stability and balancing.

- The pursuit of strategic energy independence is driving investment in resilient energy systems and giga-scale green hydrogen projects. This focus on zero-emission transportation solutions has resulted in a 30% increase in public funding for hydrogen refueling infrastructure in leading regions.

- Furthermore, the use of green hydrogen as a green industrial feedstock can reduce the carbon intensity of products like steel by over 90%, creating a powerful incentive for industrial process decarbonization and the future-proofing of industrial operations.

We can help! Our analysts can customize this water as a fuel market research report to meet your requirements.

RIA -

RIA -