Water Recycle And Reuse Market Size 2024-2028

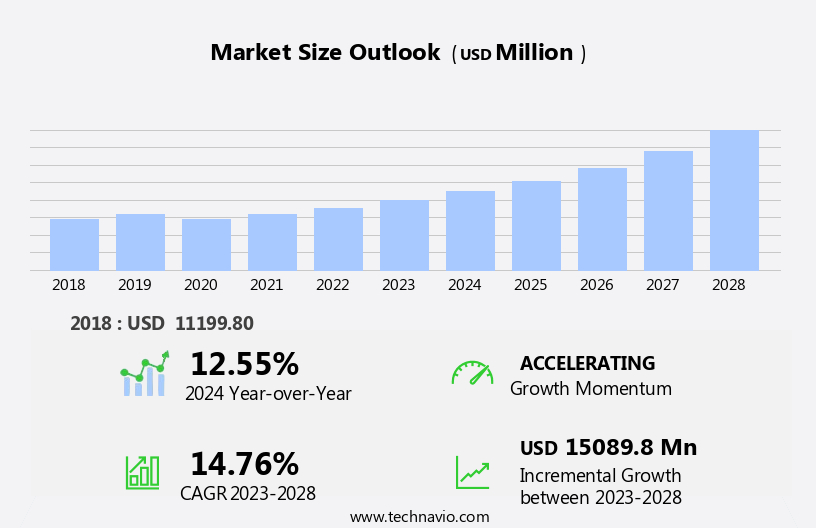

The water recycle and reuse market size is forecast to increase by USD 15.09 billion, at a CAGR of 14.76% between 2023 and 2028.

- The market is driven by the pressing need to address the scarcity of water resources and escalating environmental concerns. With increasing water scarcity and the growing awareness of the environmental impact of freshwater usage, the demand for water recycling and reuse solutions is surging. This trend is further fueled by advancements in water treatment technologies, enabling the conversion of wastewater into potable water, thereby reducing the reliance on freshwater sources. However, the market faces significant challenges. Infrastructure requirements for water treatment and distribution systems represent a substantial investment, posing financial hurdles for market entrants. Moreover, stringent regulations governing water quality and safety standards necessitate substantial investment in research and development to ensure compliance.

- These challenges call for strategic partnerships and collaborations among stakeholders to pool resources, expertise, and capabilities, enabling the development of cost-effective and sustainable water recycling and reuse solutions. Companies seeking to capitalize on the market opportunities must navigate these challenges effectively, focusing on innovation, collaboration, and regulatory compliance to secure their position in the market.

What will be the Size of the Water Recycle And Reuse Market during the forecast period?

Explore in-depth regional segment analysis with market size data - historical 2018-2022 and forecasts 2024-2028 - in the full report.

Request Free Sample

The market continues to evolve, driven by the increasing importance of sustainable water management and circular economy principles. Anaerobic digestion and biological treatment are key technologies used to transform wastewater into reusable resources, adhering to stringent water quality standards and regulations. Water pricing and infrastructure investments play a crucial role in encouraging water conservation and efficiency, while ultraviolet disinfection and ozone disinfection ensure the safety of reclaimed water. Water reuse facilities are gaining popularity across various sectors, including agriculture, industry, and municipalities, as drought management becomes a pressing concern. Water audits and metering help identify opportunities for water savings, while rainwater harvesting and stormwater management contribute to local water resource management.

Circular economy approaches to water treatment, such as membrane filtration and activated sludge systems, enable the recycling of greywater and blackwater for non-potable uses. Wastewater treatment plants employ a combination of chemical treatment, trickling filters, and reverse osmosis to produce high-quality reclaimed water. Water reuse regulations and policies continue to evolve, reflecting the ongoing dynamism of this market. Irrigation systems, agricultural water reuse, and industrial water reuse are just a few applications of reclaimed water, demonstrating the market's broad reach and potential. In the context of water scarcity, water security, and sustainable water management, the market is poised for continued growth and innovation.

How is this Water Recycle And Reuse Industry segmented?

The water recycle and reuse industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- Industrial

- Agricultural

- Domestic and commercial

- Technology

- Conventional treatment and recycling technologies

- Membrane filtration technologies

- Chemical treatment and disinfection technologies

- Geography

- North America

- US

- Europe

- Germany

- Spain

- APAC

- China

- India

- Rest of World (ROW)

- North America

.

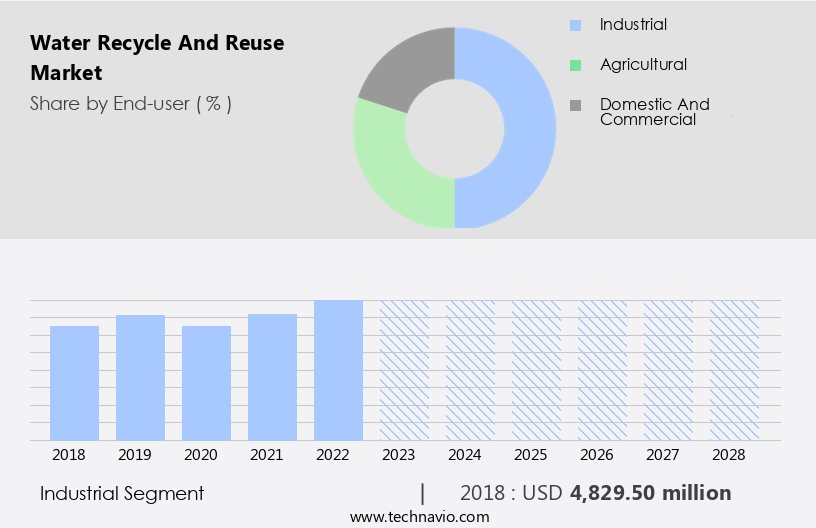

By End-user Insights

The industrial segment is estimated to witness significant growth during the forecast period.

In the energy and power sector, industries such as power generation, upstream oil and gas, and refining and petrochemical rely heavily on water. According to the International Energy Agency (IEA), the demand for freshwater in energy production is projected to double in the next quarter-century. Water is indispensable in power plants, serving as the working fluid, and is utilized for cooling, condensing, and oil extraction. Wastewater reuse and recycling play a crucial role in the energy sector. Applications include general wastewater recycling, boiler feedwater, condensate polishing, cooling tower makeup, and ion exchange rinse waters. Biological treatment, membrane filtration, and ultraviolet disinfection are essential techniques in water reclamation.

Water infrastructure, water resource management, and sustainable water management are key to addressing water scarcity and ensuring water security. Regulations and standards, such as water quality and water reuse, govern the industry. Water pricing and metering are essential for efficient water usage. Drought management and stormwater management are crucial in mitigating water shortages. Circular economy principles, like rainwater harvesting and greywater recycling, contribute to water conservation. The manufacturing, mining and quarrying, and construction industries also leverage water reuse and recycling. Biological treatment, activated sludge, and trickling filters are common methods for wastewater treatment. Reverse osmosis, ozone disinfection, and chemical treatment are other techniques used to ensure water quality.

Industrial water reuse and agricultural water reuse are vital for sustainable water management. Water footprint, an essential concept in water resource management, highlights the water usage impact of various industries. The integration of these practices into the energy and power sector, as well as other industries, is crucial for a circular economy and efficient water usage.

The Industrial segment was valued at USD 4.83 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

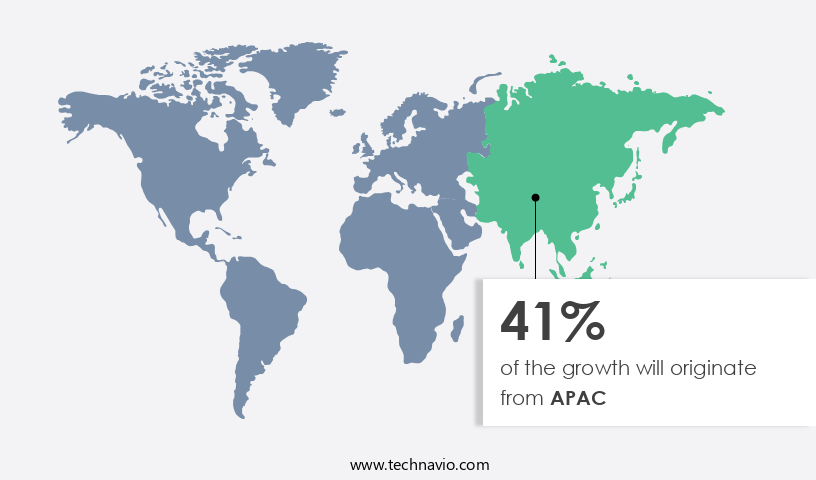

APAC is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

The market in Asia Pacific (APAC) is experiencing significant growth, with China and India leading the charge. Strict water quality standards and regulations are driving the need for water conservation and efficiency, leading to increased investment in water treatment technologies such as anaerobic digestion, biological treatment, and membrane filtration. Ultraviolet disinfection and ozone disinfection are also gaining popularity for their effectiveness in ensuring water safety. Water pricing is another key factor influencing market growth, as governments and industries seek to reduce their water footprint and secure water resources. Water reclamation and rainwater harvesting are becoming essential components of sustainable water management and resource management strategies.

Drought management and water metering are also crucial for efficient water usage. The circular economy is a significant trend in the water industry, with wastewater treatment plants and industrial facilities increasingly focusing on water reuse for irrigation systems, municipal water supply, and industrial processes. Agricultural water reuse is also gaining traction, particularly in regions with water scarcity. Governments and private entities are investing heavily in water infrastructure, including water treatment plants, stormwater management systems, and water reuse facilities. Technological advancements in chemical treatment, trickling filters, and reverse osmosis are enhancing the capabilities of these facilities and enabling more effective water reuse.

Overall, the market is expected to grow rapidly in APAC, driven by a combination of regulatory requirements, water scarcity, and the pursuit of sustainable water management practices.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Water Recycle And Reuse Industry?

- The scarcity of water and escalating environmental concerns serve as the primary drivers in shaping the market dynamics.

- The global water crisis is a pressing issue, with freshwater accounting for only a minimal percentage of the world's total water resources. The depletion of freshwater resources is primarily due to the excessive extraction of water from underground sources, which is outpacing the rate of replenishment. This situation is further exacerbated by population growth, increasing per capita water consumption, and urbanization. In response to this challenge, water recycling and reuse have emerged as crucial solutions. Approximately two-fifths of the global population currently faces water shortages, and regions such as the Middle East, North Africa, and Southeast Asia are projected to experience severe water scarcity in the coming decade due to poor water management and insufficient water recycling.

- Aerobic digestion, greywater recycling, industrial water reuse, municipal water reuse, irrigation systems, rainwater harvesting, and wastewater treatment are some of the essential techniques employed for water recycling and reuse. These methods help reduce the demand for freshwater and decrease the overall water footprint. The primary drivers for water recycling and reuse include population growth, increasing water consumption, and urbanization. By implementing these techniques, businesses and communities can conserve water resources and contribute to a more sustainable future.

What are the market trends shaping the Water Recycle And Reuse Industry?

- Water treatment technology innovation is gaining significant traction in the market. Two key trends in this field include the adoption of advanced filtration systems and the integration of automation and digital technologies for improved efficiency and precision.

- The market is experiencing significant growth due to the increasing focus on water conservation and water efficiency. Water reuse regulations and water quality standards are driving the demand for advanced water treatment technologies. Technologies such as anaerobic digestion, biological treatment, ultraviolet disinfection, and water reclamation are gaining popularity in the market. One innovative technology is the Aquaporin Inside technology, which uses biomimetic membranes for water treatment. This Danish company's technology mimics the structure of natural water channels in cell membranes, allowing water to pass through while filtering out impurities. Reverse osmosis technology is used in conjunction with this technology to filter out salts and larger solution components, providing clean water for industrial and household use.

- Water pricing also plays a crucial role in the market's growth as water scarcity increases and the cost of traditional water sources rises. The implementation of these advanced water treatment technologies is essential for preserving water infrastructure and ensuring a sustainable water supply.

What challenges does the Water Recycle And Reuse Industry face during its growth?

- The growth of the water treatment industry is significantly influenced by the infrastructure requirements, which pose a significant challenge in this sector.

- The market faces significant infrastructure challenges due to the complexity of water treatment processes. Municipal water treatment involves multiple stages, including flocculation, coagulation, sedimentation, filtration, and disinfection, which can make water reclamation and reuse a complex undertaking. The design and implementation of water reuse facilities require careful consideration of water quality objectives, operational and maintenance requirements, and flexibility of operations. These factors contribute to the intricacies of water treatment infrastructure, which can hinder market growth. Sustainable water management and circular economy principles are increasingly important in water resource management. Drought management and water security are critical concerns, making water metering and efficient water use essential.

- Water policy and regulations play a significant role in promoting water reuse and recycling. Water treatment plants are integral to these efforts, ensuring the quality and safety of reclaimed water for various uses, including agriculture, industry, and municipal applications. By addressing the infrastructure challenges and embracing advanced water treatment technologies, the market can contribute to more efficient and sustainable water management practices.

Exclusive Customer Landscape

The water recycle and reuse market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the water recycle and reuse market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, water recycle and reuse market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Alfa Laval AB - The company specializes in providing innovative water recycling and reuse solutions for both municipal and industrial sectors.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alfa Laval AB

- Aquatech International LLC

- aquatherm GmbH

- Aries Chemical Inc.

- DeLoach Industries Inc.

- Ecolab Inc.

- Element Solutions Inc.

- Evoqua Water Technologies LLC

- Fluence Corp. Ltd.

- General Electric Co.

- Grundfos Holding AS

- Komline Sanderson Corp.

- Lenntech BV

- Nitto Denko Corp.

- PHOENIX Process Equipment Co.

- Praj Industries Ltd.

- Samco Technologies Inc.

- Siemens AG

- Tata Sons Pvt. Ltd.

- Veolia Environnement SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Water Recycle And Reuse Market

- In March 2024, Suez Water Technologies & Solutions, a global water technology leader, announced the launch of its new Membrane Filtration System, named "Aquaflex MF," designed to enhance water reuse efficiency by up to 30% compared to traditional systems. This innovation addresses the growing demand for water recycling and reuse, especially in water-stressed regions (Suez Water Technologies & Solutions Press Release, 2024).

- In July 2025, Veolia Water Technologies, a global water solutions provider, entered into a strategic partnership with Microsoft to develop an IoT-based water management platform. This collaboration aims to optimize water treatment processes, reduce energy consumption, and improve operational efficiency in the water reuse industry (Microsoft News Center, 2025).

- In October 2024, Siemens Water Technologies Corporation, a leading water infrastructure provider, secured a USD100 million contract from the Saudi Arabian government to build a seawater reverse osmosis desalination plant in Jeddah. This project, expected to be completed by 2026, will significantly contribute to the country's water reuse efforts and its growing water infrastructure (Siemens AG Press Release, 2024).

- In January 2025, the European Union passed the revised Water Framework Directive, which includes stricter regulations on water reuse and recycling. This policy change is expected to drive investments in advanced water treatment technologies and encourage the adoption of circular water management practices across Europe (European Commission, 2025).

Research Analyst Overview

- The market encompasses various technologies and applications, including nutrient removal and phosphorus removal in industrial processes. Cooling towers benefit from membrane bioreactors and ion exchange for water reuse in applications such as landscape irrigation and toilet flushing. Multi-stage flash distillation and electrodialysis reversal are employed for water reuse in industries, addressing water reuse challenges and economics. Water reuse research continues to innovate, with sand filtration and sludge dewatering enhancing treatment processes. Nitrogen removal and sludge treatment are crucial components of water reuse, ensuring high-quality end products.

- Reverse osmosis desalination and water softening are additional water reuse technologies that offer benefits for businesses. Water reuse policy and filtration media are essential factors shaping the market landscape. Activated carbon plays a vital role in water treatment, contributing to the overall success of water reuse initiatives.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Water Recycle And Reuse Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

173 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.76% |

|

Market growth 2024-2028 |

USD 15089.8 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

12.55 |

|

Key countries |

China, US, Spain, India, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Water Recycle And Reuse Market Research and Growth Report?

- CAGR of the Water Recycle And Reuse industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the water recycle and reuse market growth of industry companies

We can help! Our analysts can customize this water recycle and reuse market research report to meet your requirements.

RIA -

RIA -