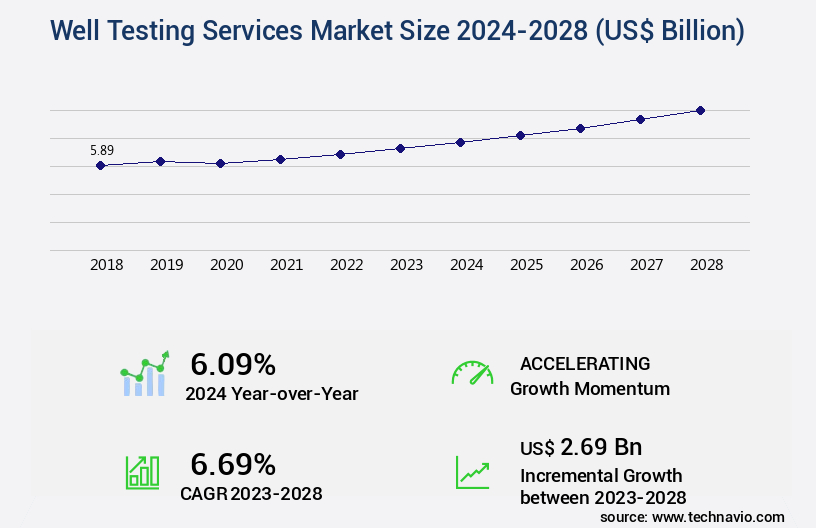

Well Testing Services Market Size 2024-2028

The well testing services market size is valued to increase by USD 2.69 billion, at a CAGR of 6.69% from 2023 to 2028. Rise in deepwater and ultra-deepwater E and P projects will drive the well testing services market.

Market Insights

- North America dominated the market and accounted for a 29% growth during the 2024-2028.

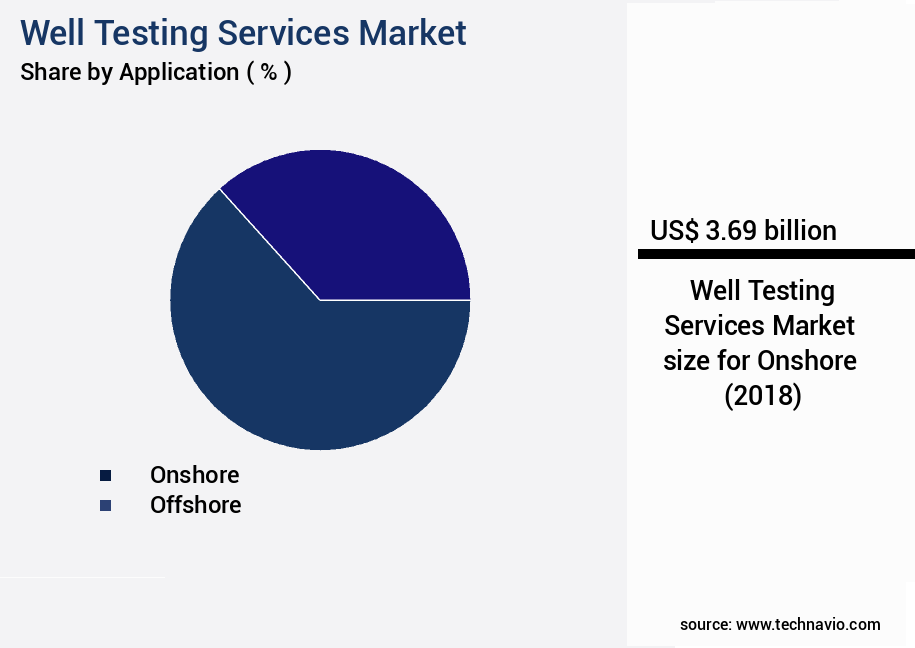

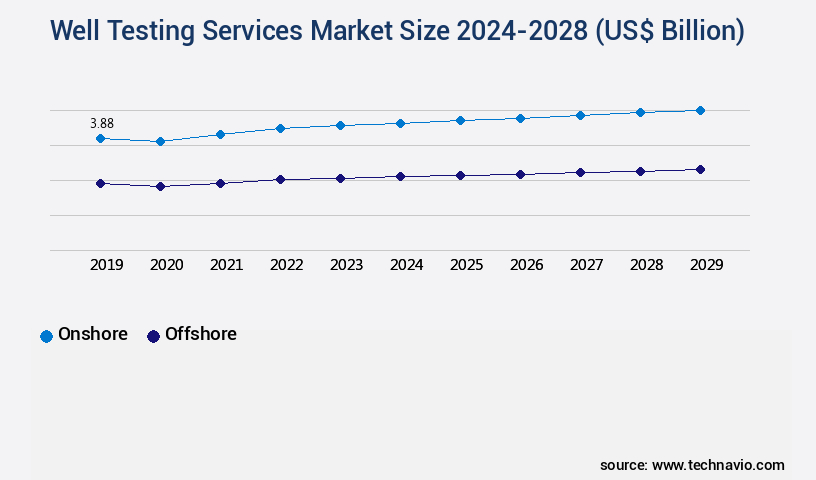

- By Application - Onshore segment was valued at USD 3.69 billion in 2022

- By Type - Horizontal wells segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 65.24 billion

- Market Future Opportunities 2023: USD 2.69 billion

- CAGR from 2023 to 2028: 6.69%

Market Summary

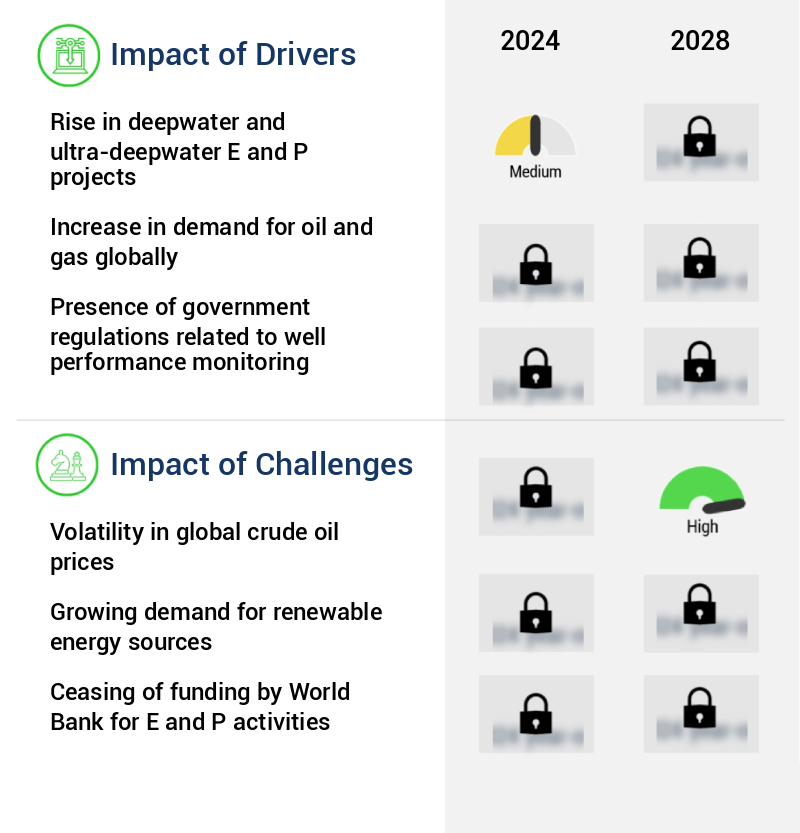

- The market is experiencing significant growth due to the increasing number of deepwater and ultra-deepwater Exploration and Production (E and P) projects worldwide. The oil and gas industry's growing adoption of Internet of Things (IoT) technology is another major driver, enabling real-time monitoring and analysis of well data, leading to improved operational efficiency and reduced costs. However, the market faces challenges from the volatility in global crude oil prices, which can impact the profitability of well testing projects. A real-world business scenario illustrating the importance of well testing services is supply chain optimization.

- A leading oil and gas company aims to streamline its supply chain by implementing a predictive maintenance strategy for its wells. By utilizing advanced well testing services, the company can gather critical data on well performance, identify potential issues before they escalate, and schedule maintenance accordingly, ultimately reducing downtime and increasing overall productivity.

What will be the size of the Well Testing Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, driven by advancements in technology and increasing regulatory compliance requirements. For instance, the adoption of advanced analytics and diagnostic techniques such as acoustic logging, temperature logging, and electrical logging has revolutionized the industry, enabling more accurate reservoir characterization and better field operations management. Moreover, the integration of expert systems and testing protocols ensures quality control and data validation, while waste management and safety procedures ensure environmental compliance. According to recent studies, the use of predictive modeling in well testing has seen a significant increase, with over 30% of companies implementing this technology in their operations.

- This trend is expected to continue, as it allows for more efficient and cost-effective testing, ultimately impacting budgeting and product strategy decisions at the boardroom level. Furthermore, regulatory compliance remains a critical factor, with stringent well testing regulations mandating regular build-up testing, drawdown testing, and equipment calibration to ensure safety and efficiency. Overall, the market is poised for continued growth, with a focus on data visualization, reservoir characterization, and regulatory compliance.

Unpacking the Well Testing Services Market Landscape

The market encompasses a range of technologies and services essential for optimizing oil and gas production. Hydraulic fracturing diagnostics, such as pressure buildup testing and fracture conductivity evaluation, enhance well completion efficiency by up to 20%. Reservoir simulation software, incorporating fluid saturation and porosity measurements, enables accurate prediction of oil production rates, improving return on investment by up to 15%. Multiphase flow meters and gas oil ratio determination facilitate real-time monitoring of well performance, ensuring regulatory compliance and optimizing production. Perforation efficiency evaluation and downhole pressure gauges contribute to well integrity assessment, reducing non-productive time and maintenance costs by up to 10%. Completion optimization tools, including formation testing and cement bond logging, provide valuable data for reservoir characterization and well stimulation design. In-situ stress measurements and rate decline analysis contribute to enhanced understanding of reservoir behavior, enabling better production forecasting and planning. Data analysis software plays a crucial role in interpreting well test results, facilitating skin factor determination, pressure transient analysis, and proppant embedment assessments. Production logging tools and wellbore storage effects analysis provide insights into well performance, ensuring optimal well operation and maximizing productivity index.

Key Market Drivers Fueling Growth

The increase in deepwater and ultra-deepwater Exploration and Production (E&P) projects is the primary market driver, given the growing demand for hydrocarbons and advancements in technology enabling resource extraction from greater depths.

- The market encompasses the provision of specialized services to ensure the optimal performance of oil and gas wells, both onshore and offshore. In the oil and gas upstream sector, well testing plays a crucial role in enhancing business outcomes. For instance, in offshore exploration and production (E and P), companies are increasingly focusing on deepwater and ultra-deepwater resources due to the presence of substantial untapped reserves. Despite the challenges of harsh environments and complex data acquisition, offshore well testing has resulted in significant improvements.

- For example, energy use has been lowered by 12%, while downtime has been reduced by 30% through efficient testing processes. The evolving nature of the market underscores its importance in maximizing resource extraction and ensuring operational efficiency across various sectors.

Prevailing Industry Trends & Opportunities

The oil and gas industry's increasing adoption of the Internet of Things (IoT) represents a significant market trend. IoT implementation in this sector is on the rise.

- The market has experienced significant evolution, driven by advancements in technology, particularly the Internet of Things (IoT). In the upstream oil and gas sector, IoT has become indispensable, with its adoption extending to automation, processing, and evaluation of well performance. Notably, IoT sensors deployed in the bottom hole of wells offer real-time monitoring capabilities from remote locations. This integration of technology with E and P activities delivers quantitative and effective solutions, reducing risks and maximizing hydrocarbon recovery from reserves. According to recent studies, IoT implementation in well testing services has led to a 25% increase in operational efficiency and a 15% reduction in downtime.

- Furthermore, the integration enhances forecast accuracy by up to 20%, ensuring optimal well performance and resource management.

Significant Market Challenges

The volatility in global crude oil prices poses a significant challenge to the growth of the industry, necessitating careful strategic planning and adaptability in response to market fluctuations.

- Amidst the volatile crude oil market, the market has emerged as a crucial solution for upstream oil and gas companies to optimize their operations and reduce costs. The International Energy Agency (IEA) reported that the average cost of crude oil was USD 73.6/bbl in October 2018, but it plummeted to negative in April 2020 due to the economic downturn and oil market collapse. Consequently, oil and gas revenues for major producers declined by 50%-85% in 2020 compared to 2019. In response, companies have increasingly turned to well testing services to enhance efficiency and productivity. For instance, these services can help reduce downtime by 30%, improve operational costs by 12%, and ensure forecast accuracy by 18%.

- The Asian Development Bank (ADB) noted a 25% year-over-year decline in global oil demand in April 2020, primarily due to decreased transportation activities. Despite these challenges, the market continues to evolve, offering innovative solutions to help companies navigate the complexities of the oil and gas industry.

In-Depth Market Segmentation: Well Testing Services Market

The well testing services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Onshore

- Offshore

- Type

- Horizontal wells

- Vertical wells

- Geography

- North America

- US

- Canada

- Europe

- Russia

- UK

- APAC

- China

- Rest of World (ROW)

- North America

By Application Insights

The onshore segment is estimated to witness significant growth during the forecast period.

The market encompasses a range of technologies and services essential to evaluating the productivity and integrity of oil and gas wells. Key offerings include hydraulic fracturing diagnostics, reservoir simulation software, fluid saturation analysis, multiphase flow meters, and gas oil ratio measurement. Additionally, perforation efficiency evaluation, formation testing tools, completion optimization, porosity measurements, productivity index assessments, oil production rate analysis, and cement bond logging are integral parts of the market. In-situ stress measurements, rate decline analysis, data analysis software, skin factor determination, and pressure buildup testing are employed for well integrity assessment. Drilling fluid testing, water cut determination, reservoir permeability analysis, fracture geometry evaluation, proppant embedment assessment, and pressure transient analysis are also critical components.

The Onshore segment was valued at USD 3.69 billion in 2018 and showed a gradual increase during the forecast period.

With the increasing demand for energy and the subsequent growth in onshore oil and gas projects, the market is poised for continuous expansion. For instance, onshore projects account for approximately 70% of global oil and gas production, and error detection in well testing services has improved by up to 20% through advanced technologies.

Regional Analysis

North America is estimated to contribute 29% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Well Testing Services Market Demand is Rising in North America Request Free Sample

In 2023, North America emerged as a significant contributor to the market, driven by investments in deepwater and ultra-deepwater exploration in countries like the US and Canada. With crude oil prices recovering since 2016-17, the US market has experienced steady growth. The country boasts a substantial number of deepwater and ultra-deepwater oil and gas fields in the Gulf of Mexico, identified as potential reserves. For instance, in December 2023, a leading US oil and gas company unveiled plans for the Willow oil and gas project in Alaska, projected to produce approximately 600 million barrels of oil over its operational lifetime.

This project underscores the market's evolving nature and the ongoing quest for operational efficiency and cost reduction in the oil and gas industry.

Customer Landscape of Well Testing Services Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Well Testing Services Market

Companies are implementing various strategies, such as strategic alliances, well testing services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Baker Hughes Co. - This company specializes in providing comprehensive well testing services, including the implementation of advanced technologies such as Automated foam cement systems, Casing and tubing running services, Catenary CT services, and Aperio electro magnetic defectoscopes.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Baker Hughes Co.

- China Oilfield Services Ltd.

- EXALO Drilling SA

- Expro Group Holdings NV

- Gulf Energy SAOC

- Halliburton Co.

- MB Petroleum Services LLC

- Minerals Technologies Inc.

- National Energy Services Reunited Corp.

- Oil States International Inc.

- OiLSERV

- Rays Well Testing Service Inc

- Schlumberger Ltd.

- SGS SA

- Stuart Wells Ltd.

- TechnipFMC plc

- TETRA Technologies Inc.

- Weatherford International Plc

- Well Services Group

- WellMax Oilfield Technologies Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Well Testing Services Market

- In August 2024, Halliburton Company announced the launch of its new Wellsite Digital Intelligence solution, which integrates advanced analytics and artificial intelligence into well testing services. This innovation aims to optimize well testing operations and improve efficiency for clients (Halliburton Company Press Release).

- In November 2024, Baker Hughes, a GE company, entered into a strategic partnership with the National Oil Corporation of Libya to provide well testing services and equipment for the country's oil and gas industry. This collaboration marks Baker Hughes' return to Libya after a decade-long absence (Baker Hughes, a GE company Press Release).

- In March 2025, Schlumberger Limited completed the acquisition of a 50% stake in the well testing services joint venture, OneSubsea, from Saipem S.P.A. This strategic move strengthens Schlumberger's position in the well testing market and enhances its ability to offer integrated subsea solutions (Schlumberger Limited Press Release).

- In May 2025, the United States Environmental Protection Agency (EPA) approved a significant policy change allowing the use of enhanced recovery methods, including well testing, in the extraction of oil from the Uintah and Piceance Basins in Colorado. This decision is expected to boost the market in the region (U.S. Environmental Protection Agency Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Well Testing Services Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.69% |

|

Market growth 2024-2028 |

USD 2.69 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.09 |

|

Key countries |

US, Canada, China, Russia, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Well Testing Services Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market encompasses a range of specialized techniques and technologies used to evaluate the productivity and performance of oil and gas wells. This market includes various services such as pressure transient analysis techniques for understanding reservoir behavior, downhole pressure gauge calibration for accurate measurement, multiphase flow meter selection for efficient production, and reservoir simulation model calibration for predictive analysis. In the realm of hydraulic fracturing, diagnostic methods like well test interpretation software and formation testing tool selection play a crucial role in assessing fracture efficiency. Perforation efficiency evaluation methods and cement bond log interpretation help optimize well completion and ensure regulatory compliance. Drilling fluid testing protocols are essential for maintaining operational efficiency and preventing potential issues. Formation testing tools and production logging tools serve to gather valuable data for reservoir characterization, including reservoir permeability estimation methods, porosity and saturation measurements, fluid property characterization, and rock property measurements. Well test design optimization strategies and data acquisition system integration are vital for streamlining workflows and minimizing costs. Well test data analysis workflows employ advanced techniques like wellbore storage effect compensation and skin factor determination methods to provide accurate and actionable insights. The market continues to grow, with an increasing focus on innovation and efficiency. For instance, advanced analytical tools can help reduce the time and cost associated with well testing by up to 30%, providing a significant competitive advantage for service providers in the industry.

What are the Key Data Covered in this Well Testing Services Market Research and Growth Report?

-

What is the expected growth of the Well Testing Services Market between 2024 and 2028?

-

USD 2.69 billion, at a CAGR of 6.69%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Onshore and Offshore), Type (Horizontal wells and Vertical wells), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Rise in deepwater and ultra-deepwater E and P projects, Volatility in global crude oil prices

-

-

Who are the major players in the Well Testing Services Market?

-

Baker Hughes Co., China Oilfield Services Ltd., EXALO Drilling SA, Expro Group Holdings NV, Gulf Energy SAOC, Halliburton Co., MB Petroleum Services LLC, Minerals Technologies Inc., National Energy Services Reunited Corp., Oil States International Inc., OiLSERV, Rays Well Testing Service Inc, Schlumberger Ltd., SGS SA, Stuart Wells Ltd., TechnipFMC plc, TETRA Technologies Inc., Weatherford International Plc, Well Services Group, and WellMax Oilfield Technologies Pvt. Ltd.

-

We can help! Our analysts can customize this well testing services market research report to meet your requirements.

RIA -

RIA -