Wireless Chargers Market Size 2024-2028

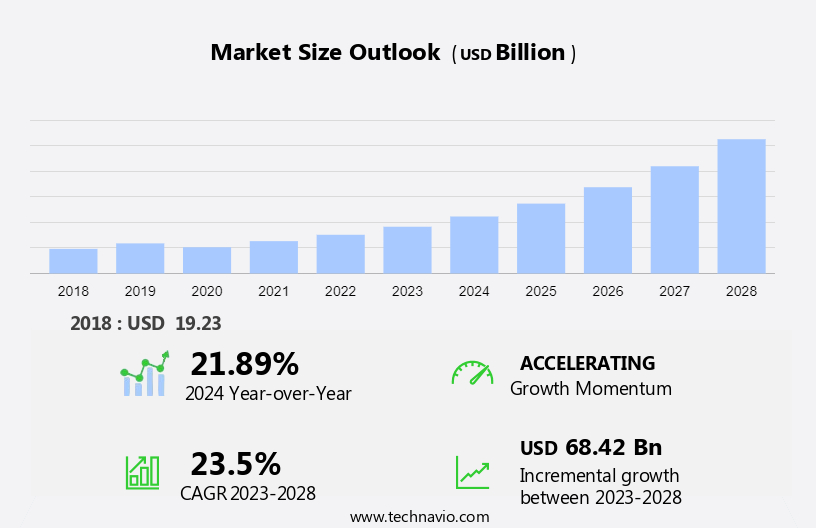

The wireless chargers market size is forecast to increase by USD 68.42 bn at a CAGR of 23.5% between 2023 and 2028.

What will be the Size of the Wireless Chargers Market during the Forecast Period?

How is this Wireless Chargers Industry segmented and which is the largest segment?

The wireless chargers industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Consumer electronics

- Healthcare

- Automotive

- Industrial

- Defense

- Technology

- Inductive

- Magnetic resonance

- Radio frequency

- Microwave

- Optical beam

- Geography

- APAC

- China

- Japan

- South Korea

- Europe

- Germany

- North America

- US

- South America

- Middle East and Africa

- APAC

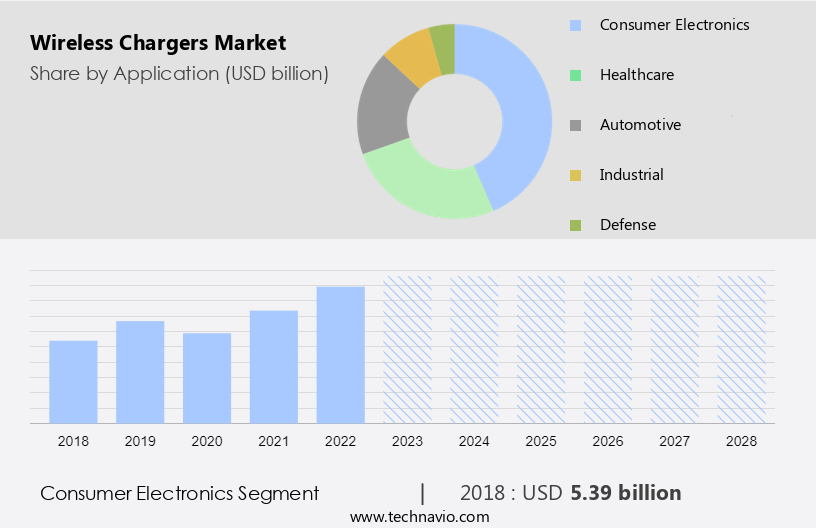

By Application Insights

The consumer electronics segment is estimated to witness significant growth during the forecast period. The market experiences substantial growth, primarily driven by the consumer electronics sector. Devices such as smartphones, tablets, smartwatches, and earbuds are major contributors to this trend, as wireless charging offers a convenient and cable-free charging experience. Notably, smartphones represent a significant portion of the consumer electronics segment embracing wireless charging. Leading manufacturers, including Apple Inc., integrate wireless charging capabilities into their premium models, fueling market expansion. For instance, Apple's MagSafe charging infrastructure on iPhones enables wireless charging without the use of cables. Furthermore, the automotive industry is another key application area for wireless charging technology, with electric vehicles (EVs) and logistics electric vehicles adopting this technology for charging infrastructure.

Technologies such as inductive, resonant, and radio frequency are employed in wireless charging systems. The consumer electronics and automotive industries are the primary industry verticals, with healthcare, aerospace & defense, and industrial robots also showing potential for growth. Wireless charging technology offers numerous benefits, including eliminating the need for physical wires and reducing carbon emissions, making it a preferred choice for both consumers and industries.

Get a glance at the market report of various segments Request Free Sample

The Consumer electronics segment was valued at USD 5.39 bn in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

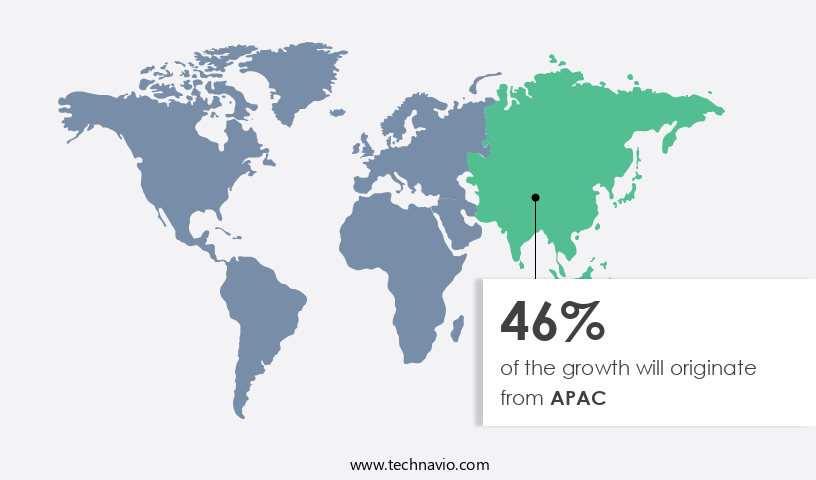

APAC is estimated to contribute 46% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The global wireless charging market is experiencing significant growth, driven by the increasing adoption of consumer electronic devices such as smartphones and computer laptops. The automotive industry is also embracing wireless charging technology for electric vehicles (EVs) and logistics electric vehicles. Two primary technologies, inductive and resonant, dominate the market. Inductive technology is widely used for charging small devices like smartphones and hearing aids, while resonant technology is preferred for long-range charging of heavy vehicles and industrial robots. Key market players include SLB Batteries, Halo receiver, and various consumer electronics and automotive companies. The integration of wireless charging with smart home automations and digital platforms like the SmartThings Hub and Qi-based charging stations is further fueling market growth.

Despite advancements, challenges such as physical wire replacement, cost per unit, and potential technical errors, including short circuits and overheating, must be addressed through thermal management systems and industry standards. The market is expected to expand across various industry verticals, including automotive, healthcare, aerospace & defense, and consumer electronics.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of market?

Increasing adoption of Qi standard is the key driver of the market.The wireless charging market is experiencing significant growth due to the increasing popularity of Qi-based charging technology. This standard, adopted by numerous firms globally, enables compatibility between devices and chargers from different manufacturers. The Qi specification is the only requirement for devices and chargers to work together, making it a preferred choice for various consumer electronic devices, including smartphones, computer laptops, electric vehicles (EVs), smartwatches, hearing aids, and more. Key players, such as Apple and Samsung, have integrated Qi technology into their products, expanding its reach and usage. This interoperability advantage is driving the market, allowing for digital connectivity and remote charging solutions in various industry verticals, including consumer electronics, automotive, healthcare, aerospace & defense, and logistics electric vehicles.

However, it is essential to ensure safety measures, such as thermal management systems and short circuit prevention, to prevent accidents and technical errors. The market consists of two main segments: inductive and radio frequency technology. While inductive technology is widely used for charging small batteries, resonant technology is gaining traction for long-range wireless charging applications in heavy vehicles, industrial robots, and electric cars. The cost per unit for wireless charging technology is expected to decrease as sales of resonant units increase, making it an attractive option for businesses and consumers alike.

What are the market trends shaping the Wireless Chargers market?

Increase in adoption of over-the-air wireless charging is the upcoming market trend.Wireless charging technology is evolving beyond traditional inductive methods, with companies exploring long-range options for charging various devices, including Electric Vehicles (EVs) and consumer electronic devices like smartphones, computer laptops, smartwatches, and hearing aids. Over-the-air wireless charging, which converts wireless signals into electricity, is gaining traction as it enables charging without the need for physical contact between the device and the charger. This technology, which can charge devices from a distance, is being developed by firms such as Energous. Their WattUp technology utilizes Radio Frequency (RF) to power multiple devices in order of priority. In the automotive industry, this technology could revolutionize EV infrastructure by eliminating the need for physical electric charging stations and reducing carbon emissions.

In addition, bi-directional wireless charging is being explored for smart home automations, allowing energy to flow between devices and the grid, enhancing digital connectivity and remote work capabilities. Other technologies, such as resonant and inductive, are also being employed in various industry verticals, including healthcare, aerospace & defense, and automotive, to power devices and heavy vehicles like industrial robots. While these advancements offer numerous benefits, potential challenges include technical errors, overheating, and thermal management systems to prevent short circuits and accidents. Cost per unit and home charging unit sales are crucial factors In the technology analysis of these wireless charging segments.

What challenges does the market face during its growth?

Compatibility issues of smartphones with wireless charger standards is a key challenge affecting the industry growth.The wireless charging market encompasses a diverse range of consumer electronic devices, including smartphones, computer laptops, electric vehicles (EVs), smartwatches, hearing aids, and industrial robots. While inductive technology dominates the market, resonant and radio frequency technology are gaining traction due to their long-range charging capabilities. However, the lack of standardization poses a significant challenge. For instance, not all smartphones and tablets, such as Samsung Galaxy S6 and S7, are compatible with Qi-based wireless charging, and iPhones still lack compatibility with most wireless charging standards. This issue hinders the mass adoption of wireless charging In the consumer electronics industry. Moreover, the automotive industry's shift towards electric vehicles (EVs) and the integration of smart home automations with the Internet of Things (IoT) and artificial intelligence (AI) necessitate the development of long-range wireless charging solutions.

The automotive segment, including logistics electric vehicles, is expected to witness significant growth In the wireless charging market. However, technical errors such as short circuits and overheating, which can lead to accidents, necessitate the implementation of thermal management systems in wireless charging units. The cost per unit for wireless charging units varies depending on the technology and industry vertical, with the inductive segment accounting for the largest market share and the radio frequency segment experiencing significant growth. The market analysis indicates that resonant unit sales are expected to increase as the technology becomes more cost-effective and efficient. The wireless charging market is poised for growth, driven by the increasing demand for digital connectivity, remote work, and the integration of wireless charging technology into various industry verticals, including consumer electronics, automotive, healthcare, aerospace & defense, and industrial applications.

Exclusive Customer Landscape

The wireless chargers market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the wireless chargers market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, wireless chargers market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

Aircharge - The company provides a range of wireless charging solutions, including the Anker MagGo wireless charging station and Anker MagGo wireless charger, as well as the Anker 3 in 1 cube with MagSafe technology. These offerings cater to diverse charging needs, ensuring compatibility with various devices and delivering efficient power transfer. The wireless chargers leverage advanced technologies to provide a convenient and clutter-free charging experience.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aircharge

- AirFuel Alliance

- Anker Technology UK Ltd.

- Apple Inc.

- Belkin International Inc.

- BEZALEL Inc.

- Delta Electronics Inc.

- Energizer Holdings Inc.

- iOttie Inc.

- Koninklijke Philips N.V.

- Mojo Mobility Inc.

- Murata Manufacturing Co. Ltd.

- Naztech Technologies

- Ossia Inc.

- Powercast Corp.

- Powermat Technologies Ltd.

- Qualcomm Inc.

- Renesas Electronics Corp.

- Samsung Electronics Co. Ltd.

- Sony Group Corp.

- Texas Instruments Inc.

- WiTricity Corp.

- ZENS Consumer BV

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The wireless charging market encompasses a range of technologies and applications, with inductive, resonant, and radio frequency being the primary methods utilized. Inductive charging, which uses magnetic fields to transfer energy between two objects, has gained significant traction In the consumer electronics industry. This technology is commonly used for charging smartphones, computer laptops, and other small devices. Resonant charging, on the other hand, operates at a higher frequency and can enable longer-range charging. This technology is increasingly being explored for use in electric vehicles (EVs) and industrial applications, such as charging heavy vehicles and powering giant robots. Another emerging trend In the wireless charging market is bi-directional charging, which allows energy to flow both ways between the charger and the device.

This technology can be particularly beneficial for EVs, as it enables the vehicle to feed excess energy back into the grid during periods of low demand. The infrastructure required for wireless charging varies depending on the technology and application. Inductive charging typically requires a physical pad or mat, while resonant charging may require specialized equipment and antennas. In the automotive industry, wireless charging is being integrated into smart things hubs and SLB batteries to facilitate seamless charging of electric cars and logistics vehicles. The wireless charging market is also being driven by advancements In the Internet of Things (IoT) and digital platforms.

With the increasing prevalence of smart home automations and wearable devices, the demand for wireless charging solutions is expected to grow. However, there are challenges associated with wireless charging, including the potential for short circuits and accidents. Physical wire-based charging remains a viable alternative, particularly for heavy-duty applications and electric charging stations. Despite these challenges, the wireless charging market is expected to grow significantly In the coming years. The automotive segment is expected to dominate the market, driven by the increasing adoption of electric vehicles. The consumer electronics industry is also expected to contribute significantly to the growth of the market, as the demand for wireless charging solutions for smartphones, laptops, and other devices continues to rise.

The cost per unit of wireless charging technology is expected to decrease as the technology becomes more widespread and competition increases. This will make wireless charging more accessible to consumers and businesses, further driving market growth. In conclusion, the wireless charging market is a dynamic and growing industry, driven by advancements in technology and the increasing demand for wireless charging solutions in various industries. Inductive, resonant, and radio frequency technologies are the primary methods used, with inductive charging being the most prevalent In the consumer electronics industry and resonant charging being explored for longer-range applications. The automotive segment is expected to dominate the market, driven by the increasing adoption of electric vehicles.

The challenges associated with wireless charging, such as the potential for short circuits and accidents, are being addressed through advancements in technology and the development of safety features. The cost per unit is expected to decrease, making wireless charging more accessible to consumers and businesses.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

185 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 23.5% |

|

Market growth 2024-2028 |

USD 68.42 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

21.89 |

|

Key countries |

US, China, Japan, South Korea, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Wireless Chargers Market Research and Growth Report?

- CAGR of the Wireless Chargers industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the wireless chargers market growth of industry companies

We can help! Our analysts can customize this wireless chargers market research report to meet your requirements.

RIA -

RIA -