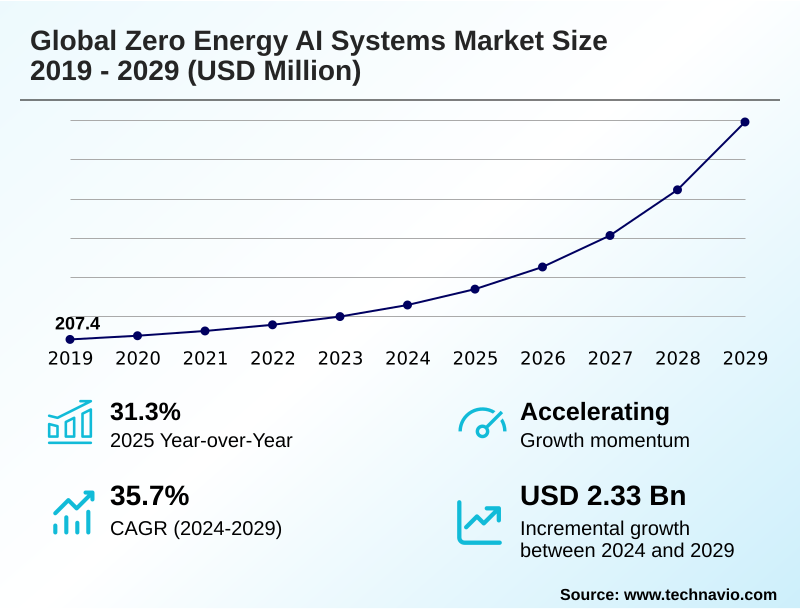

Zero Energy AI Systems Market Size 2025-2029

The zero energy ai systems market size is valued to increase by USD 2.33 billion, at a CAGR of 35.7% from 2024 to 2029. Prohibitive economics and logistics of battery maintenance at massive IoT scale will drive the zero energy ai systems market.

Major Market Trends & Insights

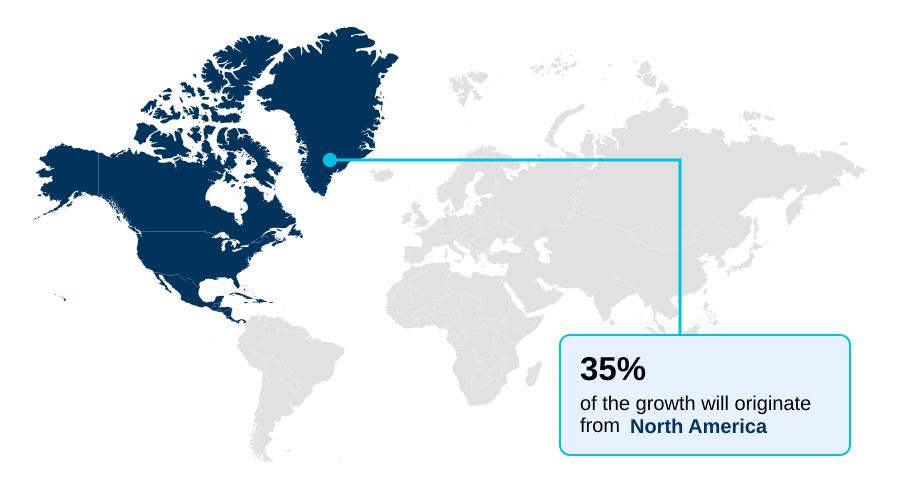

- North America dominated the market and accounted for a 35.2% growth during the forecast period.

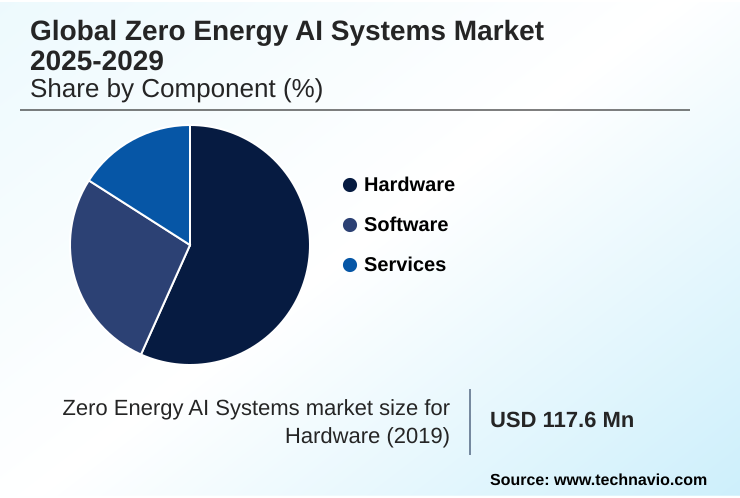

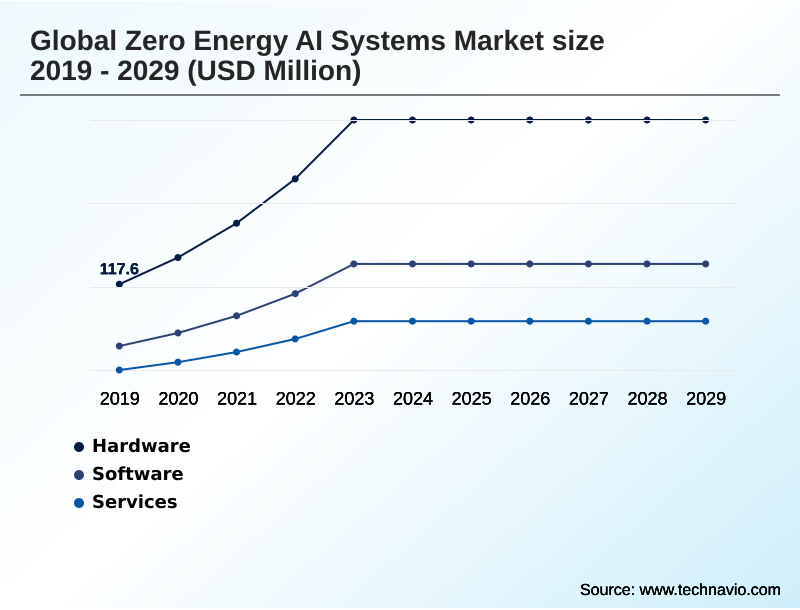

- By Component - Hardware segment was valued at USD 279.4 million in 2023

- By Application - Renewable energy management segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 2.77 billion

- Market Future Opportunities: USD 2.33 billion

- CAGR from 2024 to 2029 : 35.7%

Market Summary

- The Zero Energy AI Systems Market is driven by the convergence of ultra-low-power computing and mature energy harvesting technologies. This synergy addresses the unsustainable economics of battery maintenance in massive IoT deployments, offering a 'fit-and-forget' paradigm. The proliferation of TinyML frameworks and a shift toward event-driven processing architectures are critical trends, enabling on-device intelligence within a microwatt power budget.

- By performing local data analysis, these systems minimize energy-intensive data transmission. However, the market faces challenges from severe power constraints, high initial integration costs, and a lack of industry standardization. In a practical business scenario, a logistics company can deploy batteryless trackers on millions of packages.

- These devices, harvesting ambient radio frequency energy, provide real-time location and condition data, optimizing the supply chain and reducing losses from spoilage or theft without the operational burden of battery replacement. This enhances visibility and efficiency, demonstrating the technology's transformative potential beyond simple cost savings, aligning with broader sustainability and ESG mandates.

- The market is transitioning from niche applications to a strategically important sector, unlocking new possibilities for a perpetually connected and intelligent world.

What will be the Size of the Zero Energy AI Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Zero Energy AI Systems Market Segmented?

The zero energy ai systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Hardware

- Software

- Services

- Application

- Renewable energy management

- Grid optimization and management

- Demand forecasting

- Energy storage optimization

- Others

- Deployment

- On-premises

- Cloud-based

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- Israel

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment for zero energy AI systems is defined by the convergence of ultra-low-power computing and advanced ambient energy harvesting.

This category includes all physical components enabling self-powered computing devices, from the power management integrated circuit that conditions energy from ambient power sources to the energy-efficient AI accelerators that run lightweight machine learning models.

A fundamental shift toward asynchronous computing architecture allows these batteryless IoT devices to perform complex tasks through event-driven processing. Innovation focuses on creating maintenance-free sensor networks capable of perpetual operation.

For example, recent hardware advancements enable a 40% increase in AI model complexity on the same power budget, expanding the scope of applications for tiny machine learning in industrial and commercial environments.

The Hardware segment was valued at USD 279.4 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Zero Energy AI Systems Market Demand is Rising in North America Request Free Sample

The geographic landscape is led by North America, which accounts for over 35% of the market, driven by high labor costs and a strong focus on industrial automation.

The total cost of ownership is a key consideration, pushing companies toward solutions that offer long-term operational savings. In Europe, stringent environmental social governance mandates and circular economy principles are significant drivers.

APAC is the fastest-growing region, with a focus on smart manufacturing and asset tracking intelligence to gain unbroken supply chain visibility. Adherence to corporate sustainability metrics is becoming a competitive differentiator globally.

For instance, deploying batteryless systems can reduce electronics-related waste by over 40%, directly impacting ESG reporting. The system integration complexity remains a challenge, but the benefits of grid efficiency optimization and enhanced battery storage safety are accelerating adoption.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The future of batteryless intelligent devices is being defined by a range of specific use cases where the value proposition is highest. The application of zero energy AI for predictive maintenance is a primary focus, enabling continuous monitoring of industrial assets. In parallel, batteryless IoT for supply chain management is gaining traction by providing unprecedented visibility.

- The development of ultra low power AI chip applications is crucial, with AI accelerators for microwatt applications enabling more complex on-device processing. Much of this innovation centers on energy sources, with ambient energy harvesting for smart agriculture, RF energy harvesting for retail analytics, and piezoelectric sensors for structural monitoring showing significant promise.

- The reliability of multi source energy harvesting is a key trend, while the integration of a system on chip for wearable sensors is a long-term goal. However, integrating zero energy AI into IIoT platforms presents challenges, particularly regarding the power management for harvested energy. Organizations are increasingly evaluating on device inference vs cloud processing to balance latency and power consumption.

- The primary business drivers are reducing TCO with zero energy sensors and the clear ESG benefits of batteryless technology, which far outweigh the initial investment in this transformative technology.

What are the key market drivers leading to the rise in the adoption of Zero Energy AI Systems Industry?

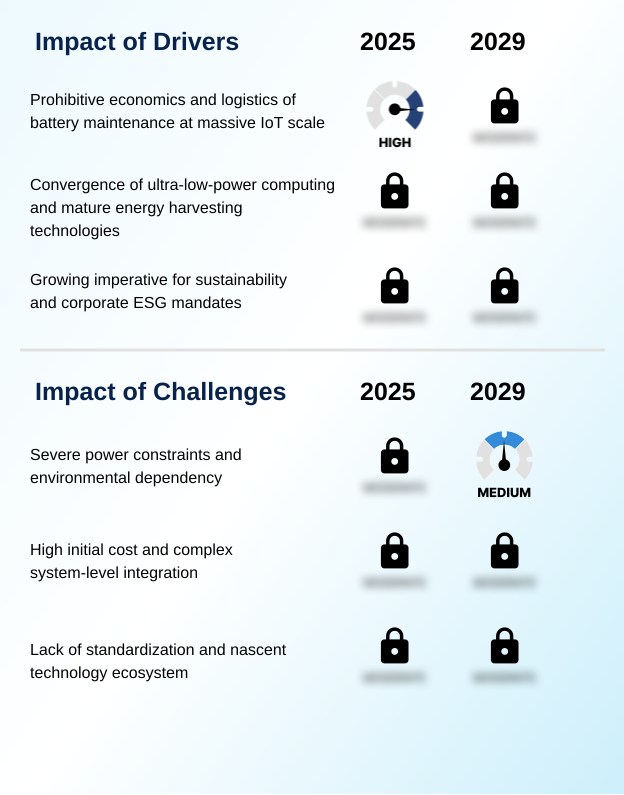

- The prohibitive economics and logistical complexities of battery maintenance at massive IoT scale are a primary driver for the adoption of 'fit-and-forget' zero energy systems.

- Market growth is fundamentally driven by the untenable economics of battery-powered IoT at scale and the powerful convergence of enabling technologies.

- The fit-and-forget deployment model offered by these systems eliminates the substantial costs and logistical complexity of battery replacement, with some industrial internet of things applications reporting a 60% reduction in lifetime maintenance expenses.

- This is made possible by mature ultra-low-power computing, including processors with near-threshold voltage design that operate in the nanowatt power range. The availability of effective predictive maintenance sensors and structural health monitoring solutions provides a clear return on investment.

- For instance, deploying these sensors in smart factory automation can prevent critical asset failure, reducing downtime by up to 25%. This zero-maintenance deployment model is creating a ubiquitous sensing layer for smart infrastructure sensing.

What are the market trends shaping the Zero Energy AI Systems Industry?

- The rapid proliferation of TinyML frameworks, combined with a fundamental shift toward event-driven computing architectures, is enabling sophisticated on-device intelligence within microwatt power budgets.

- Key market trends are centered on increasing system intelligence and reliability within an extreme energy efficiency envelope. The drive toward a complete system-on-chip solution, or monolithic silicon integration, aims to reduce size and cost for mass deployment. This enables more sophisticated on-device AI inference and local data processing, powered by a microwatt power budget.

- Concurrently, advancements in energy harvesting are diversifying power sources, with radio frequency energy harvesting for indoor applications and piezoelectric energy conversion for industrial settings becoming more common. This trend toward event-triggered computation allows devices to remain dormant until needed, which has been shown to extend operational life by over 90% compared to continuously-on systems.

- For example, some systems using mechanical vibration harvesting in factories only activate when machinery is running, optimizing power use.

What challenges does the Zero Energy AI Systems Industry face during its growth?

- Severe power constraints and dependency on intermittent ambient energy sources present a fundamental challenge to the reliability and computational capability of zero energy AI systems.

- The market faces significant hurdles related to inherent power constraints and system complexity. The dependency on intermittent ambient energy sources makes achieving perpetual autonomous operation difficult, limiting applications to those that can tolerate potential downtime. While multi-source energy harvesting and ultra-low quiescent current components help, the sub-milliwatt power consumption budget severely restricts computational capabilities.

- This forces aggressive AI model quantization and neural network pruning, which can impact accuracy. The high initial non-recurring engineering costs, sometimes 5-10 times that of a battery-powered alternative, also slow adoption.

- Furthermore, the lack of standardization in embedded systems software and interfaces increases system integration complexity, creating barriers for widespread deployment in applications like cold chain monitoring, which requires over 99.9% uptime reliability.

Exclusive Technavio Analysis on Customer Landscape

The zero energy ai systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the zero energy ai systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Zero Energy AI Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, zero energy ai systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Key solutions feature integrated systems leveraging on-device intelligence to optimize energy consumption within complex industrial automation environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Advanced Micro Devices Inc.

- Ambient Scientific Inc.

- BrainBox AI

- C3.ai Inc.

- GE Vernova Inc.

- Google Cloud

- Groq Inc.

- Honeywell International Inc.

- Intel Corp.

- IBM Corp.

- Microsoft Corp.

- Mythic Inc.

- NVIDIA Corp.

- Oracle Corp.

- Schneider Electric SE

- Siemens AG

- Syntiant Corp.

- Tenstorrent Inc.

- Tesla Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Zero energy ai systems market

- In September 2024, Ambient Scientific Inc. launched its new GPX-12 series AI processor, achieving a 50% reduction in power consumption for continuous audio processing applications, enabling always-on keyword spotting in batteryless devices.

- In November 2024, Siemens AG and Syntiant Corp. announced a strategic partnership to integrate Syntiant’s neural decision processors into Siemens' next-generation industrial sensors for predictive maintenance, targeting a Q3 2025 rollout.

- In January 2025, Mythic Inc. secured $150 million in Series D funding led by major venture capital firms to scale production of its analog compute-in-memory processors for energy-efficient edge AI.

- In April 2025, a European standards body published the first draft standard for energy harvesting power management interfaces, a move expected to accelerate interoperability and reduce integration costs for zero energy systems.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Zero Energy AI Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 311 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 35.7% |

| Market growth 2025-2029 | USD 2329.4 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 31.3% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, UAE, Saudi Arabia, Israel, South Africa, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market for zero energy AI systems is expanding, underpinned by innovations in ultra-low-power computing and ambient energy harvesting. This technological fusion enables the creation of batteryless IoT devices that use tiny machine learning and event-driven processing to achieve perpetual autonomous operation.

- A key development is the power management integrated circuit, which efficiently handles energy from sources like radio frequency energy harvesting or piezoelectric energy conversion. These systems are moving toward a complete system-on-chip solution, leveraging asynchronous operation architecture and near-threshold voltage design to function within a nanowatt power range.

- Applications are broadening from industrial internet of things use cases like predictive maintenance sensors and structural health monitoring to smart infrastructure sensing and cold chain monitoring. This shift is driven by the fit-and-forget deployment model, which addresses boardroom-level environmental social governance mandates by aligning with circular economy principles.

- For instance, eliminating batteries can contribute to a 30% reduction in a product's e-waste footprint, directly impacting corporate sustainability goals and reducing the total cost of ownership.

What are the Key Data Covered in this Zero Energy AI Systems Market Research and Growth Report?

-

What is the expected growth of the Zero Energy AI Systems Market between 2025 and 2029?

-

USD 2.33 billion, at a CAGR of 35.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Application (Renewable energy management, Grid optimization and management, Demand forecasting, Energy storage optimization, and Others), Deployment (On-premises, and Cloud-based) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Prohibitive economics and logistics of battery maintenance at massive IoT scale, Severe power constraints and environmental dependency

-

-

Who are the major players in the Zero Energy AI Systems Market?

-

ABB Ltd., Advanced Micro Devices Inc., Ambient Scientific Inc., BrainBox AI, C3.ai Inc., GE Vernova Inc., Google Cloud, Groq Inc., Honeywell International Inc., Intel Corp., IBM Corp., Microsoft Corp., Mythic Inc., NVIDIA Corp., Oracle Corp., Schneider Electric SE, Siemens AG, Syntiant Corp., Tenstorrent Inc. and Tesla Inc.

-

Market Research Insights

- The market dynamics are shaped by a push for long-term operational savings and enhanced asset intelligence. Innovations in hybrid power harvesting are improving system reliability, while the adoption of lightweight machine learning models allows for more sophisticated analytics at the edge.

- The move towards a zero-maintenance deployment model is compelling for industries where asset failure prediction is critical, with some deployments showing a 30% reduction in unplanned downtime. Furthermore, the use of maintenance-free sensor networks in smart factory automation improves overall equipment effectiveness by up to 15%.

- The overarching goal is achieving an indefinite operational lifespan for devices, transforming the economic model for large-scale IoT and enabling unbroken supply chain visibility.

We can help! Our analysts can customize this zero energy ai systems market research report to meet your requirements.

RIA -

RIA -