3D Printing Medical Devices Market Size 2024-2028

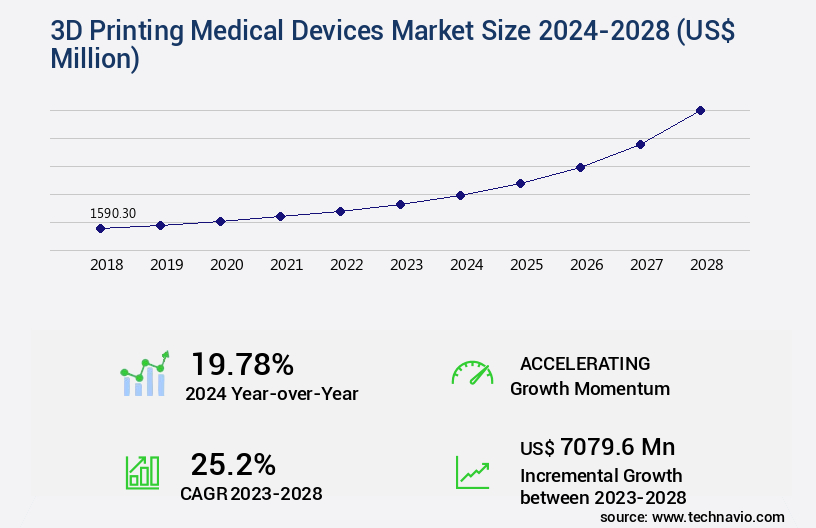

The 3d printing medical devices market size is valued to increase USD 7.08 billion, at a CAGR of 25.2% from 2023 to 2028. Increased demand for personalized or customized medical devices will drive the 3d printing medical devices market.

Major Market Trends & Insights

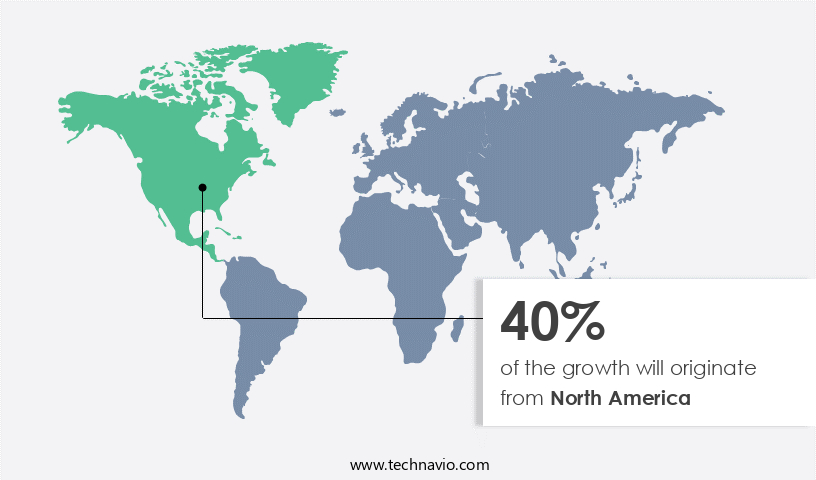

- North America dominated the market and accounted for a 40% growth during the forecast period.

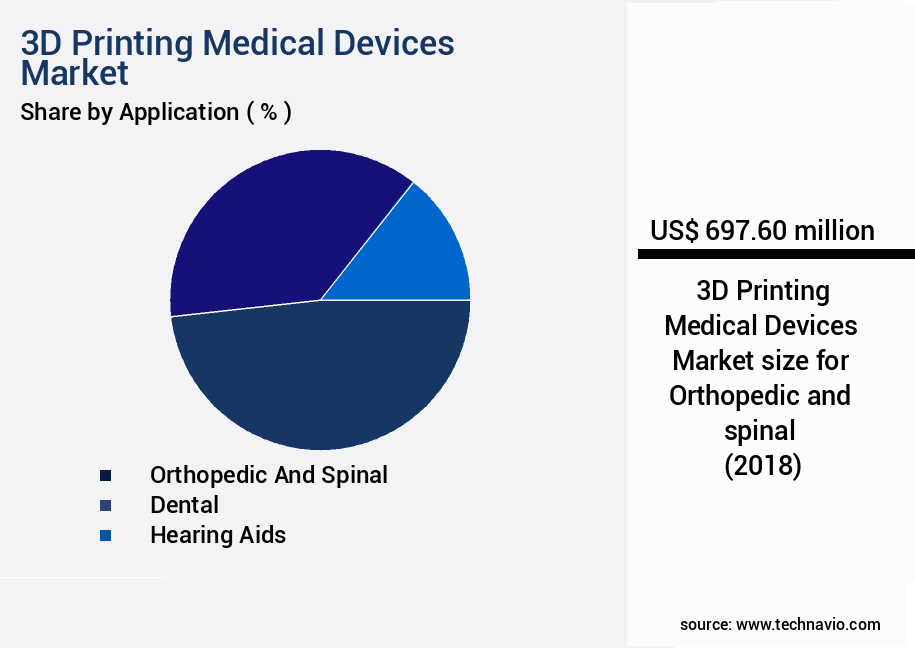

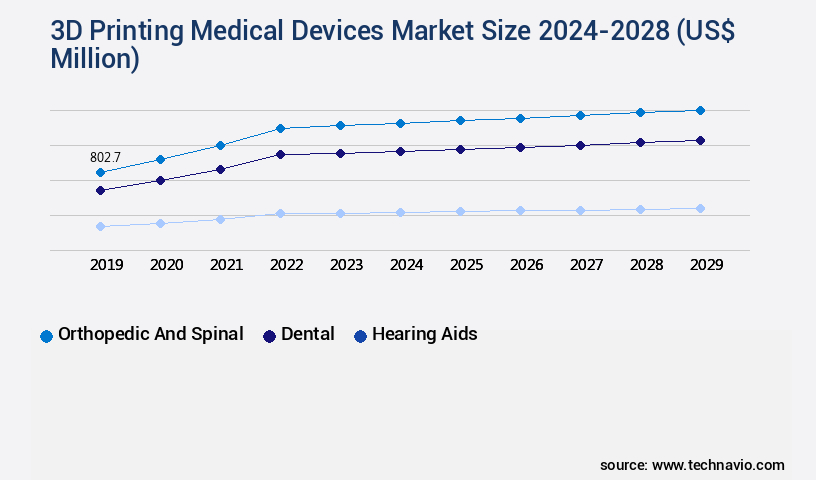

- By Application - Orthopedic and spinal segment was valued at USD 697.60 billion in 2022

- By End-user - Hospitals and clinics segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 559.58 million

- Market Future Opportunities: USD 7079.60 million

- CAGR from 2023 to 2028 : 25.2%

Market Summary

- The market represents a dynamic and evolving industry, driven by advancements in core technologies and applications. With the increasing demand for personalized or customized medical devices, the use of 3D printing technology in manufacturing healthcare solutions is gaining significant traction. According to a report by SmarTech Analysis, the global 3D printed medical device market is projected to reach a size of 2.3 billion units by 2027, growing at a steady pace. However, the high initial setup cost of 3D printing facilities remains a significant challenge for market growth. Rising focus on the research for the use of 3D printing process to manufacture living organs and cell structures presents a significant opportunity for market expansion.

- Regulations and standards set by regulatory bodies such as the FDA and European Commission play a crucial role in shaping the market landscape. Despite the challenges, the future of 3D printing in medical devices holds immense potential, with the technology offering cost-effective, efficient, and customizable solutions for various medical applications.

What will be the Size of the 3D Printing Medical Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the 3D Printing Medical Devices Market Segmented ?

The 3d printing medical devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Orthopedic and spinal

- Dental

- Hearing aids

- Others

- End-user

- Hospitals and clinics

- Academic institutes

- Pharma and biotech companies

- Others

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- Japan

- Rest of World (ROW)

- North America

By Application Insights

The orthopedic and spinal segment is estimated to witness significant growth during the forecast period.

In the realm of medical devices, 3D printing technology has emerged as a game-changer, particularly in the production of orthopedic implants and prosthetic devices. The market for these innovations is experiencing significant growth, with an increasing number of hospitals and ambulatory surgery centers adopting the technology. According to recent reports, the global market for 3D printed medical devices is projected to expand by 21% in the upcoming year, while the demand for patient-specific implants is expected to surge by 25%. Bioresorbable polymers and advanced manufacturing techniques, such as selective laser melting and material extrusion, are revolutionizing the industry. These technologies enable the creation of complex structures, including scaffold designs with surface modifications, and the optimization of mechanical properties through finite element analysis.

Moreover, 3D printing facilitates rapid prototyping, which is crucial in the development of craniofacial reconstruction, orthopedic implants, and tissue engineering applications. The integration of 3D printing in medical devices extends beyond implants and prosthetics. It is also employed in the fabrication of surgical guides, drug delivery systems, vascular grafts, and even in image-guided surgery. The technology's potential for personalized medicine and regenerative medicine is immense, with applications in cell culture, cell seeding, and bioprinting. Quality control measures, including biocompatibility testing, bioactivity testing, and regulatory compliance, are essential to ensure the safety and efficacy of these devices. As the market continues to evolve, process optimization and the use of biocompatible materials, such as those derived from computer-aided design, will become increasingly important.

The future of 3D printing in medical devices is promising, with its potential to revolutionize the healthcare industry and improve patient outcomes.

The Orthopedic and spinal segment was valued at USD 697.60 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How 3D Printing Medical Devices Market Demand is Rising in North America Request Free Sample

The market in North America is experiencing significant expansion due to enhanced healthcare infrastructure and the widespread adoption of these technologies in medical facilities. In 2022, 3D Systems, a leading player, reported a substantial portion of its revenue from this region. The presence of influential professional societies, such as the Society for Manufacturing Engineers and the Radiological Society of North America, advocating for 3D printing in healthcare further bolsters the market's growth.

These organizations are dedicated to building evidence for the clinical utility of 3D printing, contributing to its increasing acceptance in the medical sector.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing rapid growth as this advanced technology revolutionizes the healthcare industry. Biocompatible polymers, such as those used in selective laser melting for titanium implants, are a key focus in 3d printing medical devices due to their ability to mimic natural tissue structures. Design validation is paramount in medical printing, ensuring the production of accurate, functional devices. One of the most promising applications is in the field of bioprinting, where human tissues and organs are being developed for transplants. Three-dimensional printed drug delivery scaffolds and personalized cranial implants are already in use, demonstrating the potential for patient-specific treatments.

Additive manufacturing is also transforming the dental industry with the production of custom restorations. Quality control and regulatory compliance are essential in medical device printing. Computer-aided design and surgical guides, along with finite element analysis of bioprinted scaffolds, ensure the mechanical properties of 3d printed implants meet the required standards. In vivo testing of biocompatible materials, such as bioresorbable polymers, is crucial for understanding degradation rates and cell seeding efficiency. The market for 3d printed medical devices is diverse, with applications ranging from orthopedic implants to bioprinted scaffolds. More than 70% of new product developments focus on personalized medicine and regenerative medicine strategies.

While the market is competitive, a minority of players dominate the high-end instrument segment, offering advanced features and superior bioactivity. Image-guided surgery planning software is a critical component of the 3d printing medical devices ecosystem, enabling precise and efficient surgical procedures. As the market continues to evolve, it is essential to stay informed about the latest trends and developments to capitalize on the opportunities presented by this transformative technology.

What are the key market drivers leading to the rise in the adoption of 3D Printing Medical Devices Industry?

- The surge in demand for personalized and customized medical devices is the primary market driver, as patients increasingly seek solutions tailored to their unique health needs.

- 3D printing technology is revolutionizing the healthcare sector by enabling the production of patient-matched devices and surgical equipment. With additive layer manufacturing, physicians can create complex and intricately designed implants, incorporating porosity structures, tortuous internal channels, and internal support structures that are difficult, if not impossible, to achieve through traditional subtractive manufacturing. This customization leads to significant advancements in various applications, particularly in the development of customized prosthetic limbs. Traditional prosthetic manufacturing has relied on a limited number of standard sizes, which reduces costs but compromises patient comfort and hardware longevity.

- The adoption of 3D printing technology addresses these limitations, allowing for the creation of personalized implants tailored to individual patients' unique anatomies. This innovation is transforming the healthcare industry, offering improved patient outcomes and expanded possibilities for medical applications.

What are the market trends shaping the 3D Printing Medical Devices Industry?

- The emerging trend in research involves a heightened focus on utilizing the 3D printing process for manufacturing living organs and cell structures. (Alternatively: The 3D printing process is increasingly being researched for its potential in manufacturing living organs and cell structures, representing an upcoming market trend.)

- 3D bioprinting, an advanced technological development, enables the creation of living tissues through the precise layering of cells, biologic scaffolds, and growth factors. This innovative process, distinct from traditional 3D printers utilizing plastic or metals, employs a computer-guided pipette to deposit bioink, or living cells, to generate artificial living tissues. A notable achievement of 3D bioprinting technology is its application in organ replacement. This groundbreaking advancement offers the potential to produce bioidentical tissues, such as stem cells, skin grafts, and bone and cartilage, providing significant implications for medical research and healthcare.

- The field of organ replacement, historically limited by donor availability and transplant rejection, stands to benefit immensely from this technological advancement. The ongoing evolution of 3D bioprinting technology continues to unfold, offering promising possibilities across various sectors.

What challenges does the 3D Printing Medical Devices Industry face during its growth?

- The high initial setup costs associated with establishing a 3D printing facility pose a significant challenge and hinder the industry's growth.

- The 3D printing market for medical devices faces significant challenges due to high costs, which hinder its broader adoption. Equipment costs are a significant contributor, with desktop Fused Deposition Modeling (FDM) and Stereolithography Apparatus (SLA) machines costing less than USD5,000, while high-end Selective Laser Sintering (SLS), material jetting, and metal printing machines ranging from USD200,000 to USD850,000. Advanced software for post-processing also adds to the expenses. Additionally, proprietary raw materials sold by manufacturers contribute to high costs. End-users must invest in skilled personnel for training or hiring to ensure the production of high-quality medical devices.

- Despite these challenges, the 3D printing market for medical devices continues to evolve, offering potential benefits such as customization, reduced lead times, and improved patient outcomes.

Exclusive Technavio Analysis on Customer Landscape

The 3d printing medical devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the 3d printing medical devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of 3D Printing Medical Devices Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, 3d printing medical devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3D Systems Corp. - This research focuses on 3D printing technology in the medical device industry. Notable offerings include the ProJet 360, ProJet 460 Plus, ProJet 5500X, and ProJet 3500 HDMax. These advanced printers enable production of customized, high-quality medical devices, contributing significantly to the sector's growth and innovation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3D Systems Corp.

- Anatomics Pty Ltd.

- Autodesk Inc.

- Biomerics LLC

- Boston Scientific Corp.

- Desktop Metal Inc.

- EOS GmbH

- Exail Technologies

- Formlabs Inc.

- General Electric Co.

- INTAMSYS TECHNOLOGY CO. LTD.

- MATERIALISE NV

- Mecuris GmbH

- Medtronic Plc

- Organovo Holdings Inc.

- Qualtech Consulting Corp.

- Renishaw Plc

- Schultheiss GmbH

- SLM Solutions Group AG

- Stratasys Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in 3D Printing Medical Devices Market

- In January 2024, Stratasys, a leading 3D printing solutions provider, announced the FDA clearance for its J750 3D Printer, enabling it to produce complex, anatomically accurate medical models and devices (Stratasys Press Release). In March 2024, 3D Systems and United Technologies' Pratt & Whitney signed a collaboration agreement to develop 3D-printed aircraft parts for medical applications using 3D Systems' Figure 4 technology (3D Systems Press Release).

- In April 2024, GE Healthcare and Formlabs partnered to integrate Formlabs' 3D printers into GE Healthcare's medical facilities for rapid production of custom medical devices and models (Formlabs Press Release). In May 2025, Stryker, a leading medical technology company, completed the acquisition of Additive Manufacturing Partners, a medical device 3D printing services provider, expanding its additive manufacturing capabilities (Stryker Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled 3D Printing Medical Devices Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

181 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 25.2% |

|

Market growth 2024-2028 |

USD 7079.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

19.78 |

|

Key countries |

US, Germany, UK, Japan, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, with innovative technologies and applications shaping its landscape. Bioresorbable polymers, a key material in this sector, is gaining traction due to their ability to mimic natural tissue and dissolve over time. Clinical trials are underway to assess their effectiveness in various applications, including prosthetic devices and tissue engineering. Selective laser melting and material extrusion are two prominent additive manufacturing techniques used in creating these devices. Cytotoxicity testing and in vivo testing are crucial steps in ensuring their biocompatibility and safety. Scaffold design and surface modification play a pivotal role in optimizing the mechanical properties of these devices for specific applications.

- Finite element analysis and rapid prototyping enable process optimization and quality control. Craniofacial reconstruction and orthopedic implants are among the most common applications of 3D printed medical devices. Cell culture, cell seeding, and personalized medicine are other areas where this technology is making a significant impact. Surgical guides, drug delivery systems, vascular grafts, image-guided surgery, dental applications, and tissue engineering are some of the other domains where 3D printing is revolutionizing medical devices. Quality control measures, such as bioactivity testing and regulatory compliance, are essential to maintaining the integrity and safety of these devices. Biocompatible materials and computer-aided design are critical components in the development of 3D printed medical devices.

- Bioprinting techniques and regenerative medicine are emerging areas of research, offering promising advancements in the field. The ongoing unfolding of market activities and evolving patterns in the market underscore its dynamic and innovative nature.

What are the Key Data Covered in this 3D Printing Medical Devices Market Research and Growth Report?

-

What is the expected growth of the 3D Printing Medical Devices Market between 2024 and 2028?

-

USD 7.08 billion, at a CAGR of 25.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Orthopedic and spinal, Dental, Hearing aids, and Others), End-user (Hospitals and clinics, Academic institutes, Pharma and biotech companies, and Others), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increased demand for personalized or customized medical devices, High initial setup cost of 3D printing facility

-

-

Who are the major players in the 3D Printing Medical Devices Market?

-

3D Systems Corp., Anatomics Pty Ltd., Autodesk Inc., Biomerics LLC, Boston Scientific Corp., Desktop Metal Inc., EOS GmbH, Exail Technologies, Formlabs Inc., General Electric Co., INTAMSYS TECHNOLOGY CO. LTD., MATERIALISE NV, Mecuris GmbH, Medtronic Plc, Organovo Holdings Inc., Qualtech Consulting Corp., Renishaw Plc, Schultheiss GmbH, SLM Solutions Group AG, and Stratasys Ltd.

-

Market Research Insights

- The market encompasses a diverse range of applications, from surgical simulation and patient-specific design to implant manufacturing and biomedical engineering. According to industry estimates, this market is projected to reach USD3.6 billion by 2025, growing at a compound annual growth rate of 17.4% between 2020 and 2025. Selective laser sintering and powder bed fusion are two prominent 3D printing technologies used in the production of medical devices, with the former accounting for 35% of the market share in 2020. In contrast, polyjet printing and inkjet printing hold smaller market shares of 15% and 5%, respectively. Biocompatibility testing, mechanical testing, surface finishing, support structures, image processing, data analysis, and sterilization methods are essential aspects of the 3D printing process for medical devices.

- Machine learning and artificial intelligence are increasingly being integrated into the design validation and pre-operative planning stages to improve accuracy and efficiency. Implant osseointegration, achieved through techniques such as digital light processing and binder jetting, is a critical factor in the long-term success of 3D-printed medical devices.

We can help! Our analysts can customize this 3d printing medical devices market research report to meet your requirements.

RIA -

RIA -