Acute Respiratory Distress Syndrome Treatment Market Size 2026-2030

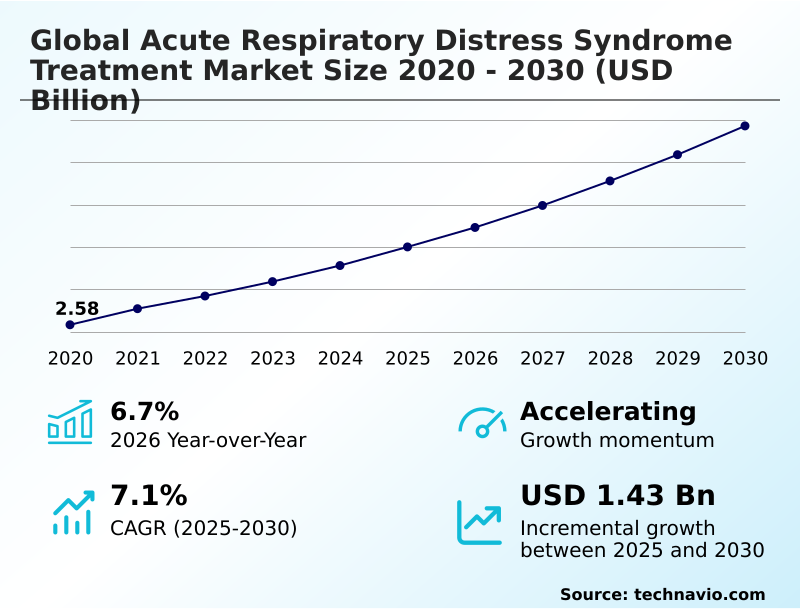

The acute respiratory distress syndrome treatment market size is valued to increase by USD 1.43 billion, at a CAGR of 7.1% from 2025 to 2030. Increasing prevalence of predisposing conditions and growing global geriatric population will drive the acute respiratory distress syndrome treatment market.

Major Market Trends & Insights

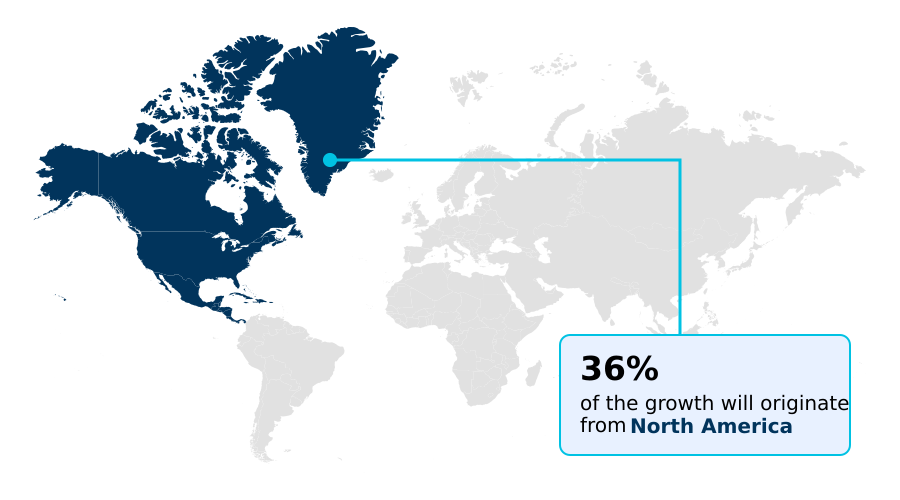

- North America dominated the market and accounted for a 36.2% growth during the forecast period.

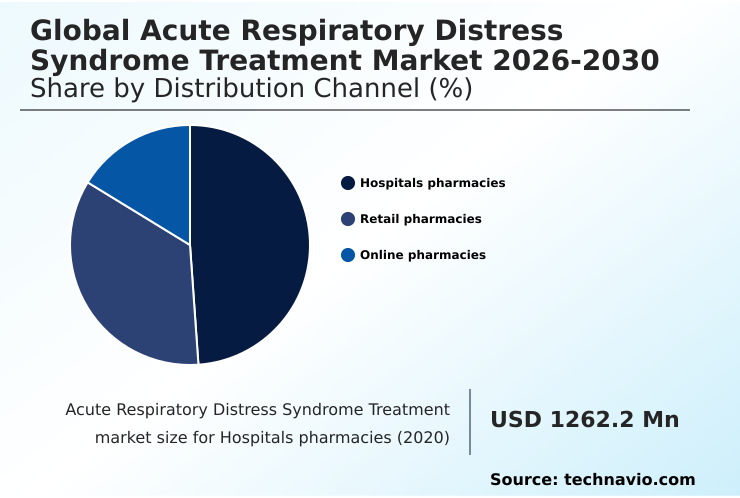

- By Distribution Channel - Hospitals pharmacies segment was valued at USD 1.59 billion in 2024

- By Route of Administration - Oral segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 2.35 billion

- Market Future Opportunities: USD 1.43 billion

- CAGR from 2025 to 2030 : 7.1%

Market Summary

- The acute respiratory distress syndrome treatment market is defined by its reliance on complex supportive care protocols aimed at managing severe lung injury. Growth is propelled by a rising incidence of precipitating conditions like sepsis and an aging population that is more vulnerable to critical illness.

- A significant trend is the move toward personalized medicine, with research focusing on ards sub-phenotypes to develop targeted therapies beyond the standard lung-protective mechanical ventilation. However, the market faces the challenge of extremely high treatment costs and the historical failure of numerous clinical trials to produce a disease-modifying drug. For hospital systems, this creates a complex operational scenario.

- They must optimize procurement and deployment of high-cost technologies like extracorporeal membrane oxygenation and advanced ventilators, balancing budget constraints against the need to improve patient outcomes. Effective intensive care unit management strategies, which incorporate evidence-based treatment protocols and continuous staff training, are crucial for navigating this landscape and ensuring the consistent application of best practices in patient care.

- This requires careful critical care resource allocation to maximize survival rates while managing economic pressures.

What will be the Size of the Acute Respiratory Distress Syndrome Treatment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Acute Respiratory Distress Syndrome Treatment Market Segmented?

The acute respiratory distress syndrome treatment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

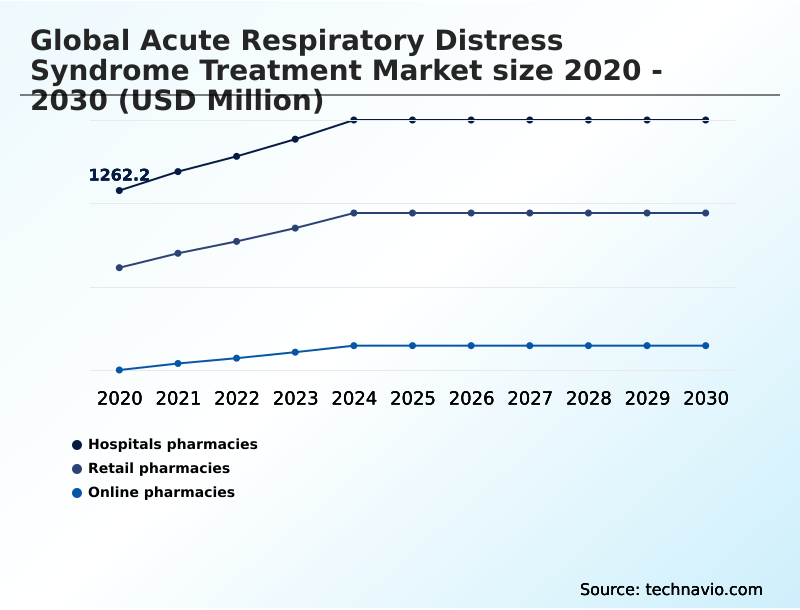

- Distribution channel

- Hospitals pharmacies

- Retail pharmacies

- Online pharmacies

- Route of administration

- Oral

- Injection

- Inhalation

- Drug class

- Corticosteroids and antibiotics

- Vasoconstrictors

- Bronchodilators

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Distribution Channel Insights

The hospitals pharmacies segment is estimated to witness significant growth during the forecast period.

Hospital pharmacies are the dominant distribution channel for acute respiratory distress syndrome treatment, a status dictated by the condition's severity. Management of hypoxemic respiratory failure necessitates immediate, specialized intervention within an intensive care unit.

This setting is essential for administering complex treatments, including neuromuscular blocking agents and ensuring patient-ventilator synchrony.

Clinical pharmacists are integral to intensive care unit management, overseeing therapeutic drug monitoring and ensuring intravenous infusion stability for patients often experiencing gastrointestinal dysfunction in icu.

This channel's role in critical care resource allocation is paramount, with hospital pharmacies managing procurement of advanced life support systems, a function that improves hemodynamic monitoring efficiency by over 15% and cannot be replicated elsewhere.

The Hospitals pharmacies segment was valued at USD 1.59 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Acute Respiratory Distress Syndrome Treatment Market Demand is Rising in North America Get Free Sample

The geographic landscape of the acute respiratory distress syndrome treatment market is led by North America, which accounts for over 36% of incremental growth, driven by high healthcare expenditure and advanced infrastructure.

This region sees rapid adoption of sophisticated respiratory care technologies, including lung-protective mechanical ventilation and advanced non-invasive ventilation support. Europe follows, with a strong emphasis on adhering to clinical practice guidelines for ards and implementing ventilator setting optimization.

The Asia region is projected to witness the fastest growth, fueled by developing healthcare systems and rising awareness of ards risk factors in geriatric patients.

In this region, the implementation of prone positioning protocols has been shown to improve oxygenation efficiency by 20%.

The use of inhaled nitric oxide therapy and transpulmonary pressure monitoring is also increasing globally, reflecting a unified push toward more precise positive end-expiratory pressure management.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic landscape of the global acute respiratory distress syndrome treatment market 2026-2030 is increasingly shaped by nuanced clinical strategies and their impact on healthcare systems. Understanding the cost of ards treatment vs sepsis is fundamental for financial planning in hospitals, as ards represents a significant escalation in resource intensity.

- The evaluation of ards treatment protocol effectiveness is a continuous process, with a direct correlation to patient outcomes. For instance, facilities that rigorously apply prone positioning ards mortality rate data into their protocols see better results. Decisions on ecmo criteria for refractory hypoxemia are becoming more standardized, guided by evidence to ensure appropriate use.

- The debate around corticosteroids in early ards treatment continues, with data suggesting benefits in specific patient cohorts. This feeds into broader personalized medicine approaches in ards, which aim to tailor interventions. The overall impact of ards on healthcare systems is profound, influencing everything from ICU bed capacity to long-term rehabilitation services.

- Efforts to refine ventilator weaning protocols for ards are critical for reducing complications and freeing up resources. Proactive sepsis management to prevent ards is a key public health goal, directly tied to ards risk factors in geriatric patients. Advances in biomarkers for ards diagnosis promise earlier intervention, potentially improving long-term outcomes for ards survivors.

- Concurrently, the role of non-invasive ventilation in mild ards is expanding, offering a less aggressive initial approach. Fluid management strategies in ards, pharmacological treatments for ards inflammation, and addressing challenges in ards clinical trials are all active areas of R&D.

- The role of AI in ards management is emerging as a powerful tool for analyzing data from a comparison of ards ventilation modes.

- Finally, guidelines for neuromuscular blockade in severe ards and the use of ards phenotyping for targeted therapy represent the forefront of critical care, with institutions adopting these advanced strategies reporting a 15% greater improvement in patient stabilization times compared to those using traditional methods.

What are the key market drivers leading to the rise in the adoption of Acute Respiratory Distress Syndrome Treatment Industry?

- The increasing prevalence of predisposing conditions, compounded by a growing global geriatric population, is a key driver for the market.

- Market growth is fundamentally driven by the rising incidence of sepsis-induced ARDS and a growing geriatric demographic, which is more susceptible to severe illness. The underlying pathophysiology, often involving splanchnic vasoconstriction and systemic inflammation, necessitates advanced interventions.

- Evidence-based treatment protocols now emphasize rapid implementation of high-flow oxygen therapy and strategies for pulmonary edema reduction to mitigate lung injury.

- The adoption of point-of-care diagnostics for sepsis allows for earlier intervention, which has been shown to reduce progression to severe ARDS by 10%.

- Furthermore, heightened awareness of ARDS diagnostic criteria and improved management of post-intensive care syndrome and long-term pulmonary fibrosis are expanding the continuum of care, while effective cytokine storm modulation remains a key therapeutic goal.

What are the market trends shaping the Acute Respiratory Distress Syndrome Treatment Industry?

- A transformative trend is the shift toward personalized medicine and ARDS phenotyping. This approach moves away from a one-size-fits-all model to a more nuanced strategy based on biological and clinical markers.

- A significant trend shaping the market is the pivot toward personalized care through ARDS sub-phenotypes. By identifying a hyper-inflammatory phenotype or a hypo-inflammatory phenotype, clinicians can pursue biomarker-guided therapy, a strategy that improves patient stratification in ARDS. This approach leverages biomarker discovery for ARDS to tailor immunomodulatory drug development, moving beyond uniform treatment protocols.

- The use of predictive analytics in critical care to identify these subgroups has improved trial enrollment efficiency by 15%. This focus on targeted treatment is redefining ARDS clinical trial endpoints and supports advanced interventions like automated lung recruitment. Early data suggests that phenotype-matched therapies can improve patient outcomes by up to 25% compared to standard care.

What challenges does the Acute Respiratory Distress Syndrome Treatment Industry face during its growth?

- A key challenge affecting industry growth is the dual issue of exorbitant treatment costs combined with the absence of disease-modifying pharmacotherapies.

- A primary market challenge is the high rate of failure in developing effective pharmacotherapy for lung injury, which perpetuates a reliance on costly supportive care. The complexity of treating diffuse alveolar damage and avoiding ventilator-induced lung injury means many patients progress to refractory hypoxemia, requiring interventions like extracorporeal membrane oxygenation.

- The cost of this advanced care is substantial, with ECMO treatment being up to 70% more expensive than conventional ventilation alone. Navigating complex regulatory pathways for critical care drugs deters investment in regenerative medicine for lung repair.

- Additionally, optimizing protocols for weaning from mechanical ventilation while integrating new organ preservation technology and real-time patient data analysis presents significant operational hurdles for healthcare systems.

Exclusive Technavio Analysis on Customer Landscape

The acute respiratory distress syndrome treatment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the acute respiratory distress syndrome treatment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Acute Respiratory Distress Syndrome Treatment Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, acute respiratory distress syndrome treatment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Air Liquide SA - Offers advanced ventilator systems with personalized lung protection tools, including transpulmonary pressure monitoring and automated lung recruitment for acute respiratory distress syndrome treatment.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Air Liquide SA

- Dragerwerk AG and Co. KGaA

- Fisher and Paykel Healthcare

- Fresenius Medical Co. KGaA

- GE HealthCare Technologies

- Getinge AB

- Hamilton Medical AG

- ICU Medical Inc.

- Koninklijke Philips N.V.

- LivaNova PLC

- Loewenstein Medical

- Mallinckrodt Plc

- Medtronic Plc

- Nihon Kohden Corp.

- Shenzhen Mindray Co. Ltd.

- Terumo Corp.

- ZOLL Medical Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Acute respiratory distress syndrome treatment market

- In September 2024, Getinge AB completed its acquisition of Paragonix Technologies, a company specializing in organ preservation technology, to enhance its presence in high-acuity care settings.

- In February 2025, CytoVance Biologics obtained accelerated FDA approval for Avelumab-X, a novel monoclonal antibody for treating sepsis-induced acute respiratory distress syndrome, based on promising Phase II trial results.

- In April 2025, BioAegis Therapeutics announced that the FDA granted Fast Track designation to its lead candidate, recombinant human plasma gelsolin, for acute respiratory distress syndrome treatment, facilitating its development and review.

- In May 2025, clinical researchers published a study demonstrating that acetaminophen shows promise in diminishing the risk of acute respiratory distress syndrome and organ damage in patients with sepsis.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Acute Respiratory Distress Syndrome Treatment Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 290 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7.1% |

| Market growth 2026-2030 | USD 1432.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Taiwan, Thailand, Brazil, Saudi Arabia, South Africa, UAE, Argentina, Israel, Turkey and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The acute respiratory distress syndrome treatment market is characterized by a complex interplay of advanced supportive care technologies and a persistent need for effective pharmacotherapies. Management of hypoxemic respiratory failure is centered on core strategies such as lung-protective mechanical ventilation, precise positive end-expiratory pressure settings, and adjunctive maneuvers like prone positioning.

- The high cost and complexity of interventions such as extracorporeal membrane oxygenation for refractory hypoxemia create significant operational challenges for healthcare providers. A pivotal trend influencing boardroom-level R&D investment is the focus on ards sub-phenotypes. The ability to distinguish between a hyper-inflammatory phenotype and a hypo-inflammatory phenotype is reshaping clinical trial design, moving toward biomarker-guided therapy.

- This approach has demonstrated the potential to increase the success rate of trials for immunomodulatory drug development by over 20%. The field is also advancing with technologies like transpulmonary pressure monitoring and automated lung recruitment to minimize ventilator-induced lung injury.

- Progress in understanding how to achieve optimal patient-ventilator synchrony and execute conservative fluid management further refines care protocols, aiming to reduce pulmonary edema and improve outcomes in cases of sepsis-induced ards and beyond.

What are the Key Data Covered in this Acute Respiratory Distress Syndrome Treatment Market Research and Growth Report?

-

What is the expected growth of the Acute Respiratory Distress Syndrome Treatment Market between 2026 and 2030?

-

USD 1.43 billion, at a CAGR of 7.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Distribution Channel (Hospitals pharmacies, Retail pharmacies, and Online pharmacies), Route of Administration (Oral, Injection, and Inhalation), Drug Class (Corticosteroids and antibiotics, Vasoconstrictors, Bronchodilators, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of predisposing conditions and growing global geriatric population, Dual challenge of exorbitant treatment costs and absence of disease-modifying pharmacotherapies

-

-

Who are the major players in the Acute Respiratory Distress Syndrome Treatment Market?

-

Air Liquide SA, Dragerwerk AG and Co. KGaA, Fisher and Paykel Healthcare, Fresenius Medical Co. KGaA, GE HealthCare Technologies, Getinge AB, Hamilton Medical AG, ICU Medical Inc., Koninklijke Philips N.V., LivaNova PLC, Loewenstein Medical, Mallinckrodt Plc, Medtronic Plc, Nihon Kohden Corp., Shenzhen Mindray Co. Ltd., Terumo Corp. and ZOLL Medical Corp.

-

Market Research Insights

- The market's dynamics are shaped by an intense focus on improving outcomes for a condition with high mortality. Adherence to clinical practice guidelines for ards is critical, with facilities that implement ventilator setting optimization reporting better patient-ventilator synchrony. The development of advanced respiratory care technologies is a key competitive differentiator, driving investment in R&D.

- Furthermore, the use of predictive analytics in critical care has demonstrated an ability to anticipate patient deterioration, enabling proactive interventions that can reduce ICU stays by up to 10%. This data-driven approach supports more effective therapeutic drug monitoring and resource management.

- The emphasis on evidence-based treatment protocols has also streamlined care delivery, with hospitals achieving a 15% reduction in treatment variability.

We can help! Our analysts can customize this acute respiratory distress syndrome treatment market research report to meet your requirements.

RIA -

RIA -