AI-Based Surgical Robots Market Size 2025-2029

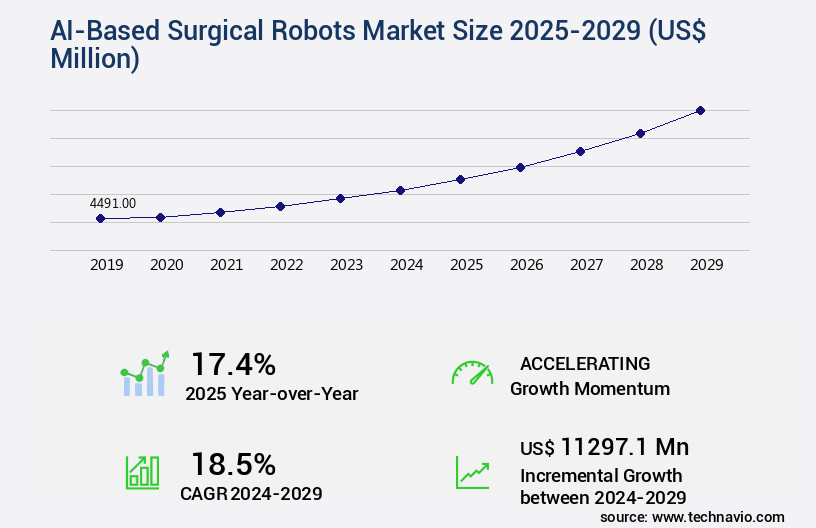

The ai-based surgical robots market size is valued to increase by USD 11.3 billion, at a CAGR of 18.5% from 2024 to 2029. Increasing preference for minimally invasive procedures and pursuit of superior surgical outcomes will drive the ai-based surgical robots market.

Major Market Trends & Insights

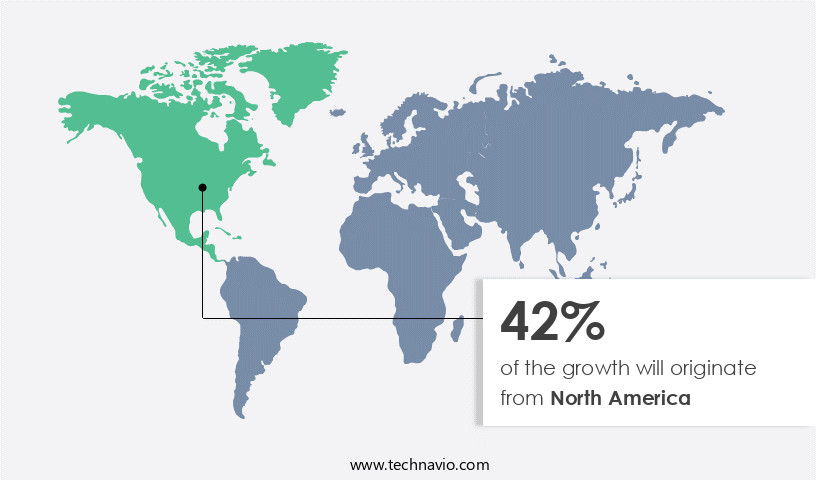

- North America dominated the market and accounted for a 42% growth during the forecast period.

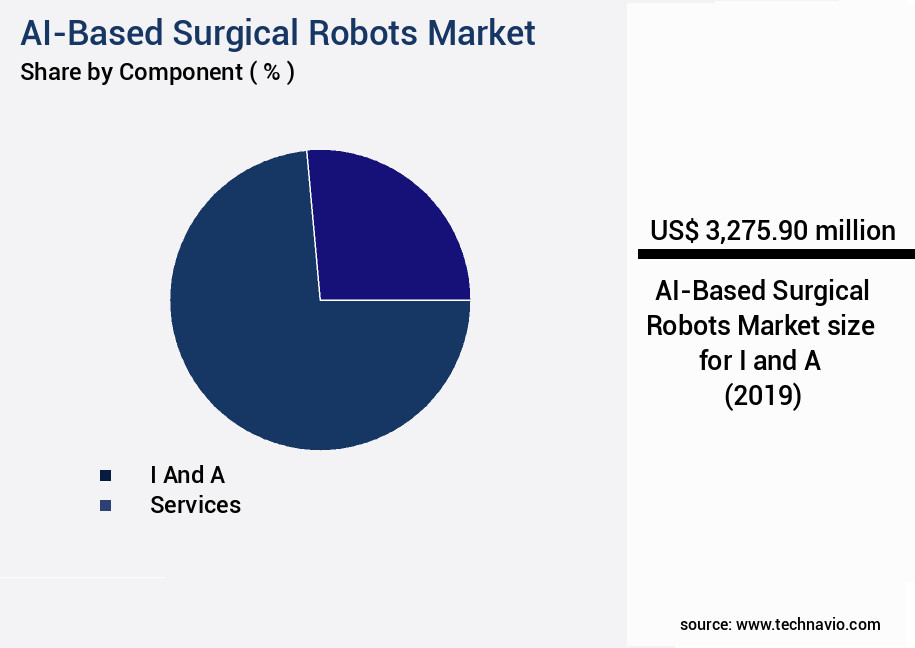

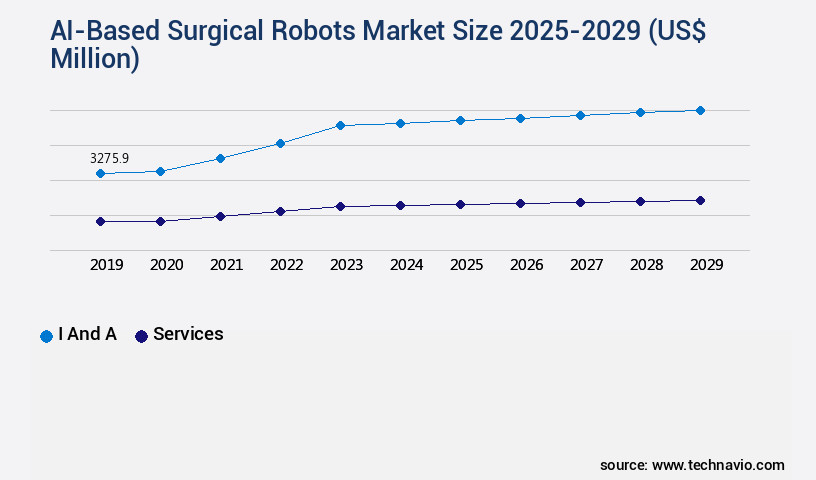

- By Component - I and A segment was valued at USD 3.28 billion in 2023

- By Application - Orthopedics segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 339.24 million

- Market Future Opportunities: USD 11297.10 million

- CAGR from 2024 to 2029 : 18.5%

Market Summary

- In the realm of advanced medical technology, the market is experiencing significant growth, fueled by the increasing demand for minimally invasive procedures and the pursuit of superior surgical outcomes. This burgeoning sector is witnessing the emergence of miniaturized and procedure-specific robotic platforms, which offer enhanced precision and flexibility to surgeons. Computer hardware advancements facilitate voice recognition, robot vision, facial recognition, and object tracking. However, the high capital investment and total cost of ownership remain challenges for market expansion.

- According to a recent report, the global market for AI-based surgical robots is projected to reach a value of USD11.1 billion by 2026, underscoring its potential for substantial growth. As this technology continues to evolve, it is poised to revolutionize the healthcare industry, offering improved patient outcomes and increased operational efficiency.

What will be the Size of the AI-Based Surgical Robots Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI-Based Surgical Robots Market Segmented ?

The ai-based surgical robots industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- I and A

- Services

- Application

- Orthopedics

- Urology

- Gynecology

- Neurology

- Others

- End-user

- Hospitals

- Ambulatory surgical centers

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Component Insights

The i and a segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth, driven by the integration of advanced technologies such as surgical simulation, real-time image processing, and 3D surgical planning. AI-powered surgical tools, including surgical robotics systems, are revolutionizing minimally invasive surgery by enhancing surgical dexterity, precision, and surgical navigation. Robot-assisted surgery enables remote surgery and robotic surgical training, offering benefits in terms of surgical error reduction and improved patient safety protocols. Precision robotics, haptic feedback systems, and motion tracking sensors are essential components of these advanced systems, enabling instrument articulation and image-guided surgery. According to a recent study, The market is projected to reach a value of USD21.3 billion by 2025, growing at a compound annual growth rate of 17.5% during the forecast period.

This growth is attributed to the increasing adoption of computer vision algorithms and medical image processing in surgical procedures, as well as ongoing research in force feedback control and surgical workflow optimization. The market's continued evolution is set to transform the surgical landscape, offering enhanced surgical outcomes assessment and redefining the future of surgical instrumentation and dexterity training.

The I and A segment was valued at USD 3.28 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI-Based Surgical Robots Market Demand is Rising in North America Request Free Sample

The global market for AI-based surgical robots is experiencing significant growth and innovation, with North America leading the charge. This region, spearheaded by the United States, boasts the highest per capita healthcare expenditure worldwide and a sophisticated healthcare infrastructure, enabling widespread adoption of advanced robotic surgical systems. Major players, including Intuitive Surgical, Stryker, and Johnson & Johnson, call North America home, fostering a competitive and dynamic industry landscape. These companies invest heavily in research and development, resulting in a steady stream of new product introductions and technological advancements.

The market is projected to reach a value of over USD11 billion by 2027, growing at a compound annual growth rate of approximately 15%. This expansion is driven by the increasing demand for minimally invasive surgeries and the integration of AI technologies to enhance surgical precision and efficiency.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the integration of advanced technologies such as AI algorithms for surgical planning, computer vision for surgical guidance, and surgical robot control algorithms. These innovations enable more precise and efficient surgical procedures, improving patient outcomes and reducing the risk of complications. Haptic feedback in robotic surgery provides surgeons with a tactile sense during operations, enhancing their ability to perform minimally invasive surgical techniques with greater dexterity. Performance metrics for robotic surgery allow for continuous monitoring and analysis of surgical data, ensuring optimal surgical workflow efficiency and reducing surgical site infections.

Surgical robotic arm design and control have advanced significantly, with AI-powered surgical tool calibration ensuring accurate and consistent performance. Robotic surgical system safety protocols and remote surgery technological advancements have also been crucial in expanding the reach and accessibility of robotic surgical procedures. Surgical simulation for improved dexterity and surgical data analytics for improved outcomes are essential components of AI-integrated surgical robotic platforms. Robotic surgical system architecture design focuses on integrating these advanced technologies seamlessly, while surgical data management and security are prioritized to maintain patient confidentiality and data integrity. As the complexity of robotic surgical procedures continues to increase, the demand for advanced AI-based surgical robots is expected to grow. With ongoing research and development, the future of surgical robotics holds great promise for revolutionizing the healthcare industry.

What are the key market drivers leading to the rise in the adoption of AI-Based Surgical Robots Industry?

- The growing demand for minimally invasive procedures and the pursuit of superior surgical outcomes are the primary factors driving market growth in this sector.

- The market is experiencing significant growth due to the increasing preference for minimally invasive surgeries within the medical community and among patients. Characterized by small incisions, these procedures offer numerous advantages over traditional surgeries, including reduced postoperative pain, lower infection risk, diminished blood loss, and shorter hospital stays. This trend is leading to improved patient experiences, faster recoveries, and a substantial reduction in healthcare system costs through decreased readmission rates and minimized long-term care requirements.

- AI-integrated surgical robots represent the pinnacle of this evolution, empowering human surgeons with unparalleled precision and control. This shift towards advanced surgical technologies is a critical development in the healthcare sector, enhancing patient care and driving economic efficiency.

What are the market trends shaping the AI-Based Surgical Robots Industry?

- The emergence of miniaturized robotic platforms, tailored for specific procedures, represents a significant market trend. (Alternatively) Miniaturized robotic platforms, designed for procedure-specific applications, are becoming increasingly prevalent in the market.

- A significant trend transforming the market involves the transition from large, multipurpose robotic systems to smaller, specialized platforms. Early surgical robots were known for their extensive footprints and versatile applications, catering to a wide range of intricate procedures. However, these systems, while effective, necessitated dedicated operating rooms and substantial financial investments, restricting their usage to major healthcare facilities. The current market trajectory is marked by a focus on specialization and miniaturization.

- Companies are now engineering robots customized for specific surgical sectors, including orthopedics, neurosurgery, ophthalmology, and endoluminal interventions. This shift towards niche applications and compact designs is expanding accessibility and affordability, making AI-based surgical robots increasingly popular in various healthcare settings.

What challenges does the AI-Based Surgical Robots Industry face during its growth?

- The high capital investment and total cost of ownership represent significant challenges that can hinder industry growth. These expenses, which include both the initial investment required for major assets and the ongoing costs for maintenance and operation, can pose substantial financial hurdles for businesses in this sector.

- The integration of AI technology in surgical robots is revolutionizing the healthcare sector, offering enhanced precision and minimally invasive procedures. However, the significant financial investment required for acquiring and maintaining these advanced systems poses a substantial barrier to entry for numerous healthcare providers worldwide. The high initial cost of purchasing a modern AI-based surgical robot system often reaches into the millions of dollars, making it an unattainable expense for many hospitals and surgical centers, particularly those in developing regions and smaller facilities in North America and Europe.

- The total cost of ownership further adds to the financial strain. Despite these challenges, the benefits of AI-based surgical robots, such as improved patient outcomes and reduced recovery time, continue to attract interest and investment.

Exclusive Technavio Analysis on Customer Landscape

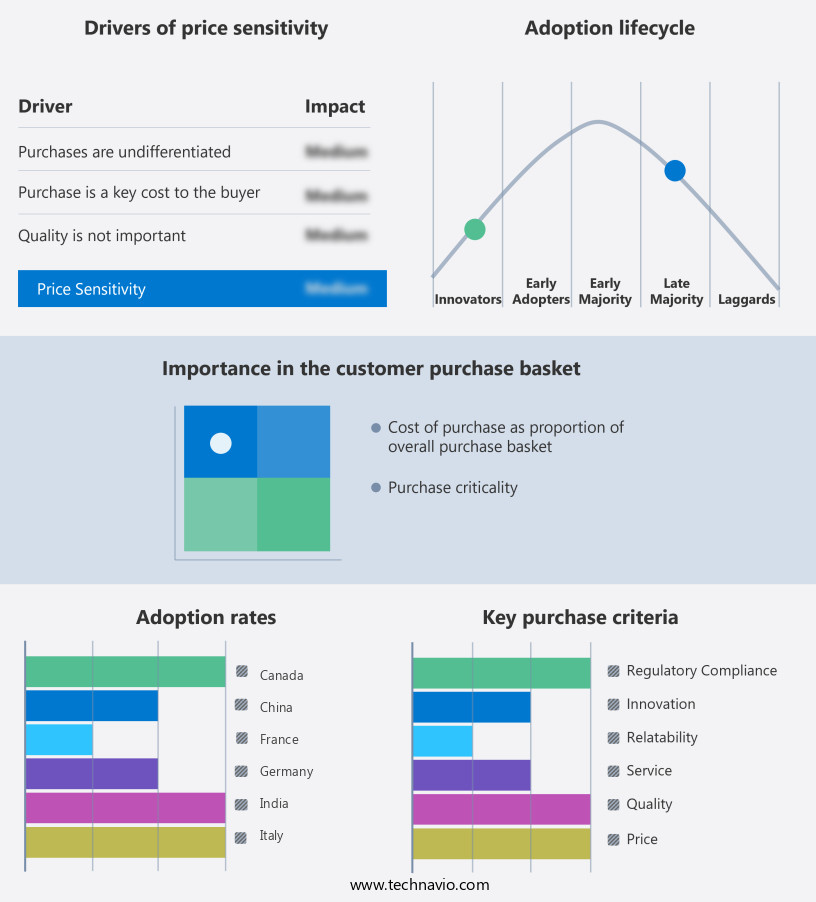

The ai-based surgical robots market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai-based surgical robots market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI-Based Surgical Robots Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai-based surgical robots market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Activ Surgical - The company specializes in advanced AI-driven surgical robots, including the Senhance and Luna platforms. These systems incorporate augmented intelligence and haptic feedback, enhancing surgical precision and effectiveness. By leveraging cutting-edge technology, the company sets new standards in minimally invasive surgeries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Activ Surgical

- Asensus Surgical US Inc.

- CMR Surgical Ltd.

- Globus Medical Inc.

- Intuitive Surgical Inc.

- Johnson and Johnson Services Inc.

- Medicaroid Corp.

- Medtronic Plc

- Moon Surgical

- Neocis Inc.

- Quantum

- Renishaw Plc

- Robocath

- Smith and Nephew plc

- Stereotaxis Inc.

- Stryker Corp.

- Synaptive Medical Inc.

- THINK Surgical Inc.

- Vicarious Surgical

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI-Based Surgical Robots Market

- In January 2024, Intuitive Surgical, a leading player in the market, announced the FDA approval of its new da Vinci Xi+ System, which incorporates AI algorithms to assist surgeons in performing complex procedures more accurately and efficiently (Intuitive Surgical Press Release, 2024).

- In March 2024, Medtronic and Google Cloud entered into a strategic partnership to develop AI-powered surgical tools and expand their offerings in the robotic-assisted surgery space (Medtronic Press Release, 2024).

- In May 2024, Zimmer Biomet Holdings completed the acquisition of Medtech's Spine and Neuro Technologies business, enhancing its portfolio with AI-assisted surgical solutions for spine procedures (Zimmer Biomet Press Release, 2024).

- In April 2025, the European Commission granted marketing authorization to Stryker's Mako Robotic-Arm Assisted Total Knee Replacement System, featuring advanced AI algorithms to personalize treatment plans for patients (Stryker Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI-Based Surgical Robots Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

236 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 18.5% |

|

Market growth 2025-2029 |

USD 11297.1 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

17.4 |

|

Key countries |

US, Germany, China, UK, Japan, Canada, France, South Korea, Italy, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The surgical robots market continues to evolve, driven by advancements in technology and the growing demand for minimally invasive procedures. AI-powered surgical tools, such as those utilizing real-time image processing and 3D surgical planning, are revolutionizing the field. For instance, a study published in the Journal of the American College of Surgeons found that the use of robot-assisted surgery for prostatectomies resulted in a 50% reduction in blood loss and a 29% shorter hospital stay compared to traditional open procedures. Precision robotics, surgical navigation, and instrument articulation are key components of these systems, enabling surgeons to perform procedures with greater dexterity and accuracy.

- Surgical simulation and robotic surgical training are also crucial, allowing for haptic feedback systems and motion tracking sensors to enhance surgical skills. AI-assisted surgery, surgical planning software, and computer vision algorithms are further advancing the capabilities of surgical robotics systems. Patient safety protocols and endoscope integration are also essential features, ensuring optimal outcomes and minimizing surgical errors. Industry growth in surgical robotics is expected to reach double digits in the coming years, with continuous research and development in areas such as force feedback control, surgical precision, and surgical instrumentation. The potential for remote surgery and image-guided surgery is also opening new avenues for application across various sectors.

What are the Key Data Covered in this AI-Based Surgical Robots Market Research and Growth Report?

-

What is the expected growth of the AI-Based Surgical Robots Market between 2025 and 2029?

-

USD 11.3 billion, at a CAGR of 18.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (I and A and Services), Application (Orthopedics, Urology, Gynecology, Neurology, and Others), End-user (Hospitals, Ambulatory surgical centers, and Others), and Geography (North America, Europe, APAC, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing preference for minimally invasive procedures and pursuit of superior surgical outcomes, High capital investment and total cost of ownership

-

-

Who are the major players in the AI-Based Surgical Robots Market?

-

Activ Surgical, Asensus Surgical US Inc., CMR Surgical Ltd., Globus Medical Inc., Intuitive Surgical Inc., Johnson and Johnson Services Inc., Medicaroid Corp., Medtronic Plc, Moon Surgical, Neocis Inc., Quantum, Renishaw Plc, Robocath, Smith and Nephew plc, Stereotaxis Inc., Stryker Corp., Synaptive Medical Inc., THINK Surgical Inc., Vicarious Surgical, and Zimmer Biomet Holdings Inc.

-

Market Research Insights

- The market for AI-driven surgical robots continues to evolve, with advancements in robot programming, precision control, and data management driving innovation. Robotic surgical procedures have gained significant traction, with surgical robot design incorporating advanced sensors and actuators for enhanced accuracy and safety. According to industry reports, the market is expected to grow by over 15% annually, reflecting the increasing adoption of these technologies in healthcare institutions. For instance, a recent study demonstrated a 30% reduction in complications and a 25% shorter hospital stay for patients undergoing robotic-assisted surgeries compared to traditional methods.

- This trend is set to continue as the field of computer-aided surgery and remote surgery technology advances, offering new possibilities for surgical workflow automation and calibration. The development of surgical simulation software and robotic interfaces further expands the potential applications of these technologies, making them an integral part of modern surgical practices.

We can help! Our analysts can customize this AI-based surgical robots market research report to meet your requirements.

RIA -

RIA -