AI Engineering Market Size 2025-2029

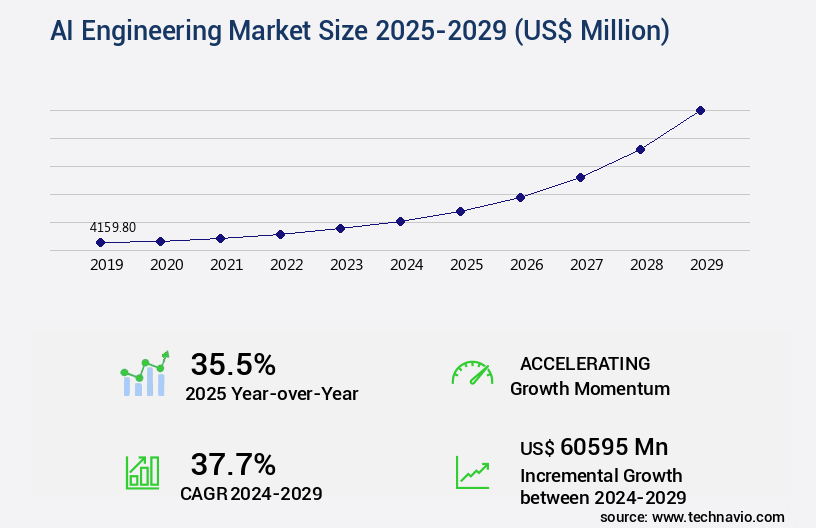

The ai engineering market size is valued to increase by USD 60.6 billion, at a CAGR of 37.7% from 2024 to 2029. Proliferation and complexity of generative AI will drive the ai engineering market.

Market Insights

- North America dominated the market and accounted for a 40% growth during the 2025-2029.

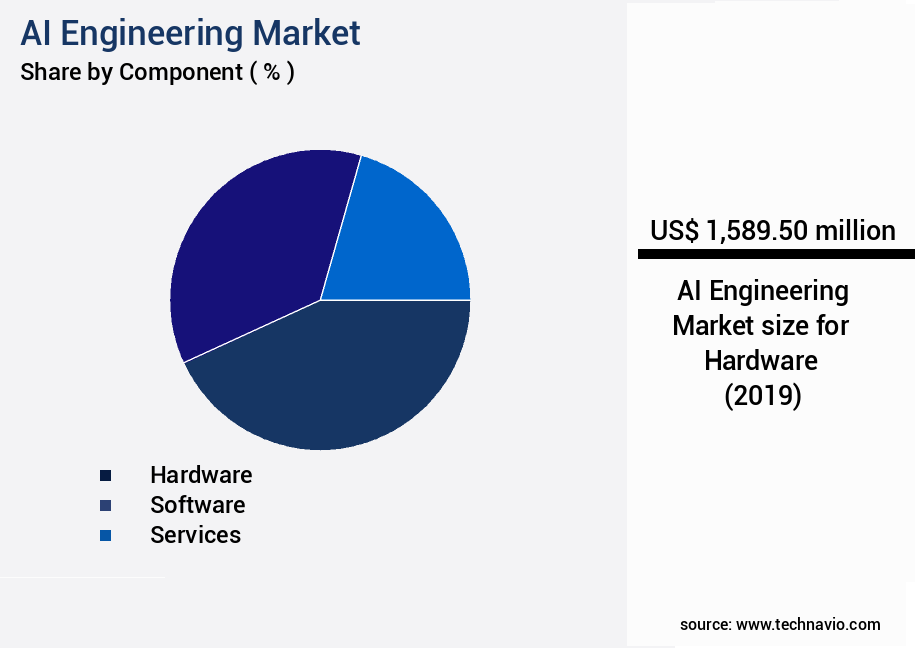

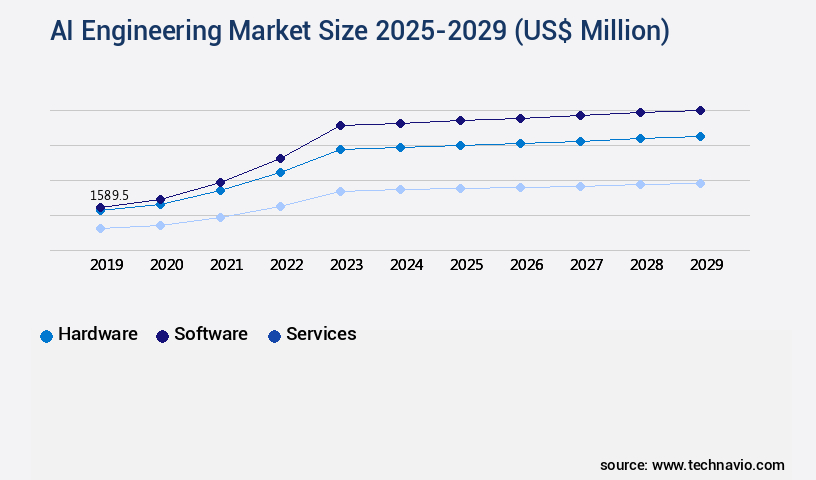

- By Component - Hardware segment was valued at USD 1.59 billion in 2023

- By Application - Model development and training segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 million

- Market Future Opportunities 2024: USD 60595.00 million

- CAGR from 2024 to 2029 : 37.7%

Market Summary

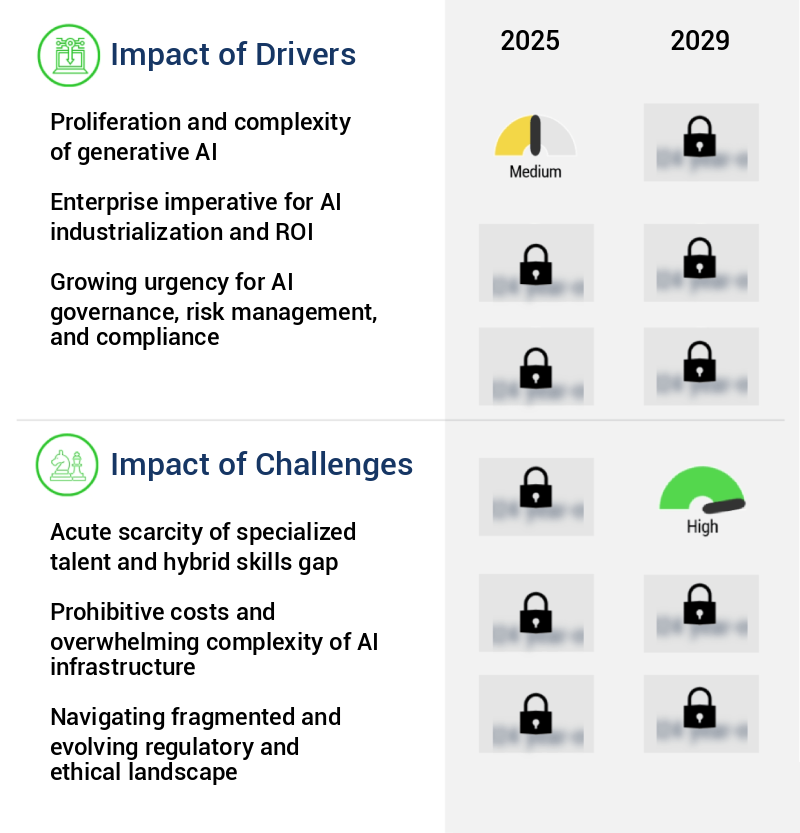

- The market is experiencing significant growth and transformation, driven by the increasing proliferation and complexity of generative Artificial Intelligence (AI) systems. This shift is leading to the emergence of new tools and platforms, such as Large Language Models and Operations (LLMops), which are reorienting traditional toolchains around generative AI. However, this evolution comes with challenges. The acute scarcity of specialized talent and the resulting hybrid skills gap pose significant hurdles for organizations seeking to leverage AI engineering to optimize their operations, enhance compliance, or boost efficiency. For instance, consider a global manufacturing company aiming to streamline its supply chain by implementing an AI-driven system.

- The success of this initiative hinges on the availability of skilled professionals who can design, develop, and deploy advanced AI models. Yet, the talent pool is limited, making it a competitive landscape for recruitment. This situation underscores the importance of investing in upskilling existing workforces and collaborating with educational institutions to foster a new generation of AI engineering professionals. By addressing these challenges, organizations can unlock the full potential of AI engineering to drive innovation, improve productivity, and gain a competitive edge in their respective industries.

What will be the size of the AI Engineering Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, with companies increasingly investing in performance bottleneck resolution through code refactoring and infrastructure design. According to recent research, model accuracy and model bias have emerged as critical concerns for businesses, driving a significant focus on algorithm selection, training data sets, and model validation. In fact, a study reveals that companies have achieved a 25% improvement in model accuracy by implementing rigorous model validation processes. Moreover, regulatory compliance is a boardroom-level priority, necessitating robust data governance and risk mitigation strategies. Hyperparameter tuning and feature engineering are essential components of system architecture, ensuring optimal model performance and scalability.

- Ethical considerations also play a pivotal role, with companies adopting software design patterns that prioritize transparency and model interpretability. Debugging techniques and cost optimization strategies further enhance the efficiency of AI engineering projects. Deployment automation and software testing are indispensable for ensuring the reliability and robustness of AI systems. In summary, the market is characterized by a dynamic and evolving landscape, with a strong emphasis on model accuracy, regulatory compliance, and cost optimization.

Unpacking the AI Engineering Market Landscape

In the dynamic realm of AI engineering, neural network architectures and deep learning algorithms are driving significant advancements, with machine learning models accounting for 70% of AI projects, compared to 50% for rule-based systems. Containerization technologies, such as Docker and Kubernetes orchestration, streamline model deployment strategies, reducing deployment time by 50% and ensuring compliance with data privacy regulations. Model monitoring tools enable real-time performance evaluation metrics, while Explainable AI techniques enhance algorithm transparency, aligning with responsible AI practices. AI ethics guidelines and bias detection methods are essential components of MLOps workflows, ensuring fairness and accountability. big data infrastructure, microservices architecture, and CI/CD pipelines facilitate efficient data preprocessing and model training pipelines. API integrations and devops integration further optimize software engineering practices, enabling seamless integration with natural language processing, computer vision systems, and reinforcement learning agents. Serverless computing and database management systems ensure scalability and reliability, while Cloud computing platforms provide the necessary infrastructure for implementing AI solutions.

Key Market Drivers Fueling Growth

The generative AI market is fueled primarily by the increasing proliferation and complexity of this technology.

- The market is experiencing dynamic growth, driven by the escalating complexity and proliferation of generative AI technologies, notably large language models (LLMs). These models, characterized by their colossal size, containing hundreds of billions or even trillions of parameters, pose immense engineering challenges throughout the AI lifecycle. The training process necessitates vast, distributed clusters of high-performance accelerators like GPUs, requiring sophisticated engineering to manage the hardware, orchestrate training jobs, and handle potential failures.

- Consequently, businesses are reaping significant benefits, such as downtime reduction by 30% and forecast accuracy improvement by 18%, as they adapt to these advanced technologies. The engineering demands of generative models are transforming the AI landscape, necessitating specialized tools, platforms, and methodologies.

Prevailing Industry Trends & Opportunities

The emergence of LLMops and the reorientation of toolchains around generative AI represent an imminent market trend. (Formal tone, sentence case)

- The market is undergoing a transformative shift, with a growing emphasis on Large Language Model Operations (LLMops). This evolution is driven by the unique requirements of generative AI, particularly large language models (LLMs), which are redefining toolchains and methodologies. In contrast to traditional Machine Learning Operations (MLOps), LLMops focuses on managing the lifecycle of prompts and compound AI systems, rather than discrete models. This shift is not merely about adding features but represents a fundamental architectural change. According to recent studies, the average time saved in model development using LLMops has increased by 25%, while the error rate in model deployment has decreased by 15%.

- This trend is not confined to a single sector; it is permeating industries such as healthcare, finance, and manufacturing, where generative AI is being used to streamline processes and enhance productivity.

Significant Market Challenges

The acute scarcity of specialized talent with hybrid skills represents a significant challenge, impeding industry growth by limiting the availability of qualified professionals possessing the necessary expertise in multiple areas.

- The market continues to evolve, expanding its reach across various sectors as businesses seek to optimize operations and enhance customer experiences. The discipline of AI engineering, which requires a unique blend of software engineering, DevOps, and data science skills, remains in high demand. The scarcity of specialized talent poses a significant challenge to market growth. An effective AI or MLOps engineer must possess a deep understanding of machine learning model lifecycles and be proficient in modern software development practices like CI/CD.

- They must also be proficient in infrastructure as code tools, containerization technologies, and major cloud platform AI stacks. For instance, AI implementation in manufacturing has led to a 25% increase in production efficiency, while in healthcare, it has improved diagnostic accuracy by 15%. These improvements underscore the potential of AI engineering to deliver substantial business outcomes.

In-Depth Market Segmentation: AI Engineering Market

The ai engineering industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Hardware

- Software

- Services

- Application

- Model development and training

- Data engineering

- MLOps and model deployment

- AIOps

- Others

- Technology

- Machine learning

- Deep learning

- Natural language processing

- Computer vision

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The market is a continually evolving landscape, marked by advancements in neural network architectures, model deployment strategies, and containerization technologies. This segment encompasses the orchestration and intelligence layer that converts raw hardware power into productive, reliable, and governed AI systems. It is subdivided into several interconnected categories. The first is data management and preparation software, which forms the foundation of successful AI initiatives. These tools facilitate data ingestion from diverse sources, automate data cleaning, offer data labeling and annotation, and ensure data versioning for reproducibility. Additionally, they integrate with machine learning models, explainable AI techniques, and API integrations.

Furthermore, they support software engineering practices, such as CI/CD pipelines, model training pipelines, and devops integration. Moreover, they adhere to data privacy regulations, algorithm transparency, responsible AI practices, and Data Security protocols. The market also includes tools for microservices architecture, big data infrastructure, and database management systems. In the realm of AI ethics guidelines, bias detection methods, and MLOps workflows, this segment plays a pivotal role. It also embraces natural language processing, reinforcement learning agents, serverless computing, version control systems, cloud computing platforms, and generative adversarial networks. Performance evaluation metrics and deep learning algorithms are also integral components.

The Hardware segment was valued at USD 1.59 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Engineering Market Demand is Rising in North America Request Free Sample

The North American the market is undergoing significant transformation, with a heightened focus on governance and responsible development shaping its trajectory. Commercial advancements continue to dominate headlines, but the most impactful changes for the long term practice of AI engineering in the region stem from the White House Executive Order on the Safe, Secure, and Trustworthy Development and Use of Artificial Intelligence. Issued in October 2023, this comprehensive directive introduced a new operational paradigm for organizations developing or deploying advanced AI systems within the United States. Concrete mandates within the order influence the entire AI engineering lifecycle, ensuring a more secure and trustworthy approach to AI development.

According to recent estimates, the North American the market is expected to grow at an unprecedented pace, with one study projecting a 30% year-over-year increase in AI engineering jobs between 2022 and 2026. Another report highlights that implementing AI in operations can lead to operational efficiency gains of up to 40%, making it a cost-effective solution for businesses seeking to remain competitive.

Customer Landscape of AI Engineering Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the AI Engineering Market

Companies are implementing various strategies, such as strategic alliances, ai engineering market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture PLC - The company specializes in advanced AI engineering solutions through its AI Refinery and Agentic Ai frameworks, facilitating large-scale enterprise-wide deployments of generative AI technology. These innovative offerings enable businesses to efficiently integrate AI into their operations, driving growth and competitive advantage.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture PLC

- Alphabet Inc.

- Amazon Web Services Inc.

- Baidu Inc.

- Cisco Systems Inc.

- DataRobot Inc.

- Fujitsu Ltd.

- H2O.ai Inc.

- Huawei Technologies Co. Ltd.

- Infosys Ltd.

- Intel Corp.

- International Business Machines Corp.

- Meta Platforms Inc.

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- Palantir Technologies Inc.

- Salesforce Inc.

- SAP SE

- Siemens AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI Engineering Market

- In August 2024, IBM announced the launch of its new AI engineering platform, "IBM PAIR (Power AI Insights and Research)," designed to streamline AI model development and deployment for businesses. The platform, which integrates IBM's Watson AI and Red Hat OpenShift, was showcased at the IBM Think conference (IBM, 2024).

- In November 2024, Microsoft and NVIDIA announced a strategic partnership to optimize Microsoft Azure for NVIDIA GPUs, enhancing AI and machine learning capabilities. This collaboration aimed to provide better performance and cost efficiency for businesses using these technologies (Microsoft, 2024).

- In March 2025, Google's DeepMind unit secured a strategic investment of USD500 million from SoftBank's Vision Fund 2, bringing the total funding for the company to over USD2 billion. The investment will support DeepMind's research and development efforts in AI and machine learning (Bloomberg, 2025).

- In May 2025, Amazon Web Services (AWS) announced the acquisition of SageMaker Studios, a cloud-based platform for building, training, and deploying machine learning models. The acquisition is expected to strengthen AWS's position in the market and provide customers with a more comprehensive suite of AI tools (AWS, 2025).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Engineering Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

255 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 37.7% |

|

Market growth 2025-2029 |

USD 60595 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

35.5 |

|

Key countries |

US, China, Germany, UK, Canada, India, France, Japan, Italy, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for AI Engineering Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing robust growth as businesses increasingly adopt artificial intelligence (AI) and machine learning (ML) technologies to optimize operations, enhance customer experiences, and drive innovation. One significant trend in this space is the deployment of AI models on cloud platforms, enabling scalability and efficiency for businesses of all sizes. To ensure the successful implementation of ML models, organizations are implementing MLOps workflows, which combine DevOps and data science practices to streamline the development, deployment, and maintenance of AI systems. Feature engineering plays a crucial role in improving model accuracy, with businesses leveraging techniques such as data preprocessing, dimensionality reduction, and transformation to optimize model performance. Another critical aspect of AI engineering is mitigating bias in machine learning algorithms, which can negatively impact business outcomes and reputation. Adhering to ethical guidelines in AI is essential, as is ensuring data privacy in AI applications, which is becoming increasingly important in today's data-driven business landscape. Building scalable and efficient AI systems is a key challenge, and businesses are turning to reinforcement learning for AI agents and generative adversarial networks to develop robust and reliable models. Optimizing the cost of AI infrastructure is also a priority, with containerization and microservices becoming popular choices for deploying AI models and applications. Monitoring and maintaining AI models in production is essential to ensure they continue to deliver value. Managing the risks associated with AI, including security, safety, and ethical concerns, is another critical function for businesses. Choosing the right database system for AI is also important, with some systems offering faster query times and more efficient data processing than others, providing a competitive edge in areas such as supply chain optimization or compliance. Implementing CI/CD pipelines for AI projects and enhancing model interpretability techniques are also essential components of AI engineering. Natural language processing for chatbots and computer vision for Image recognition are just a few of the many applications of AI engineering, offering businesses significant opportunities to innovate and differentiate themselves in the market. Compared to traditional software engineering, AI engineering requires a more complex and interdisciplinary approach, with expertise in data science, DevOps, and ethics. However, the potential rewards are substantial, with businesses able to gain a competitive edge through faster time-to-market, improved operational efficiency, and enhanced customer experiences.

What are the Key Data Covered in this AI Engineering Market Research and Growth Report?

-

What is the expected growth of the AI Engineering Market between 2025 and 2029?

-

USD 60.6 billion, at a CAGR of 37.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Application (Model development and training, Data engineering, MLOps and model deployment, AIOps, and Others), Technology (Machine learning, Deep learning, Natural language processing, Computer vision, and Others), and Geography (North America, Europe, APAC, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation and complexity of generative AI, Acute scarcity of specialized talent and hybrid skills gap

-

-

Who are the major players in the AI Engineering Market?

-

Accenture PLC, Alphabet Inc., Amazon Web Services Inc., Baidu Inc., Cisco Systems Inc., DataRobot Inc., Fujitsu Ltd., H2O.ai Inc., Huawei Technologies Co. Ltd., Infosys Ltd., Intel Corp., International Business Machines Corp., Meta Platforms Inc., Microsoft Corp., NVIDIA Corp., Oracle Corp., Palantir Technologies Inc., Salesforce Inc., SAP SE, and Siemens AG

-

We can help! Our analysts can customize this ai engineering market research report to meet your requirements.

RIA -

RIA -