AI For Process Optimization Market Size 2025-2029

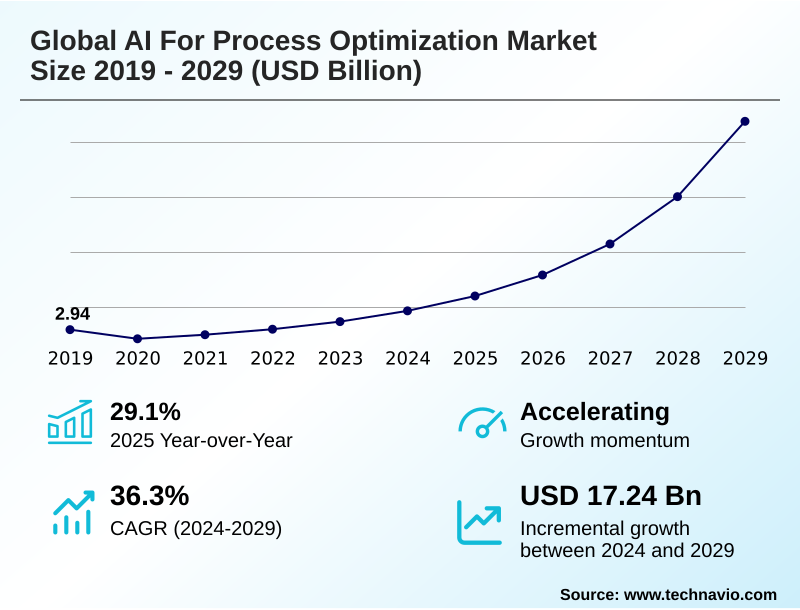

The ai for process optimization market size is valued to increase by USD 17.24 billion, at a CAGR of 36.3% from 2024 to 2029. Imperative for operational efficiency and cost reduction will drive the ai for process optimization market.

Major Market Trends & Insights

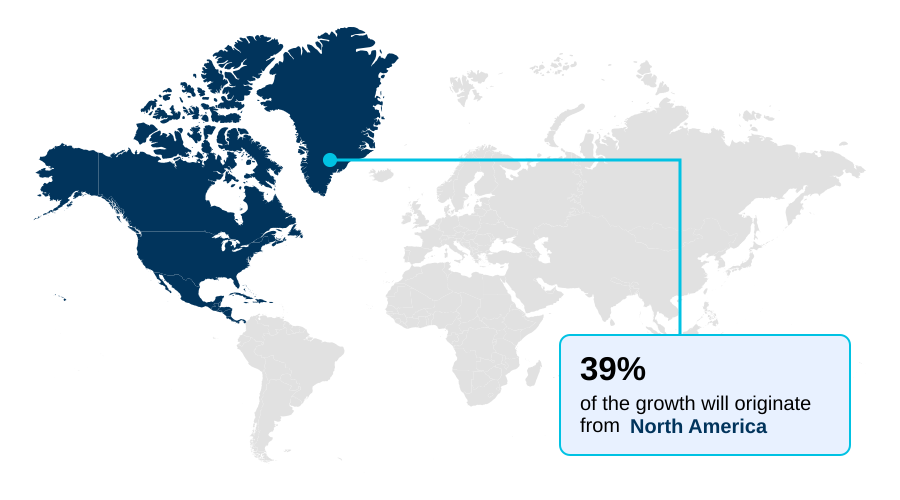

- North America dominated the market and accounted for a 38.6% growth during the forecast period.

- By Deployment - Clou-based segment was valued at in 2023

- By Sector - Large enterprises segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 18.94 billion

- Market Future Opportunities: USD 17.24 billion

- CAGR from 2024 to 2029 : 36.3%

Market Summary

- The AI for process optimization market is rapidly evolving from a niche technology to a cornerstone of enterprise strategy, driven by the intense pressure for enhanced productivity and cost containment. Organizations are deploying these solutions to automate and intelligently manage cross-departmental workflows, moving beyond simple task execution.

- A key trend is the adoption of hyperautomation architecture, which integrates cognitive automation and prescriptive analytics engines to build self-optimizing systems. For instance, in a complex supply chain, AI can analyze real-time data to anticipate disruptions, perform process bottleneck analysis, and automatically adjust logistics, thereby improving resilience and efficiency.

- However, significant challenges remain, including the need for robust data lineage and provenance to ensure model accuracy and the demand for explainable AI (XAI) to meet regulatory and ethical standards. Overcoming the scarcity of skilled talent and ensuring data quality are critical for leveraging these powerful tools for data-driven operational intelligence.

What will be the Size of the AI For Process Optimization Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI For Process Optimization Market Segmented?

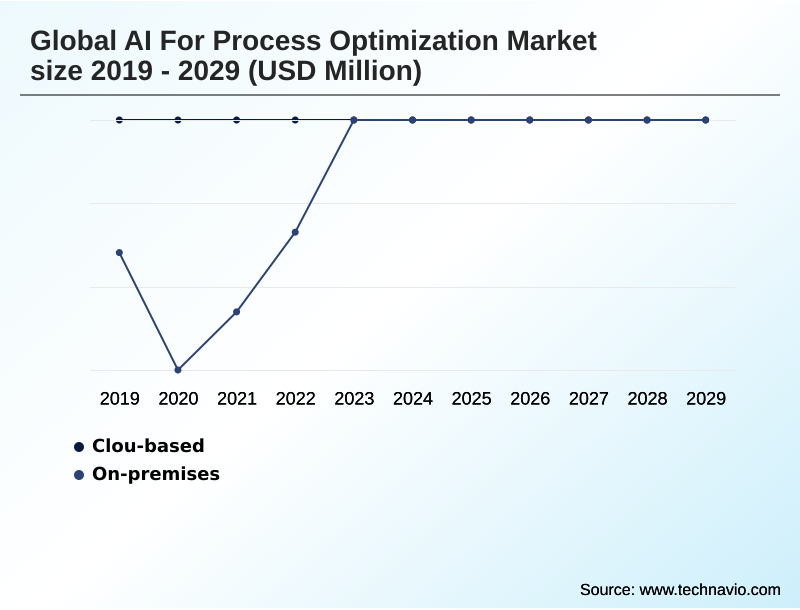

The ai for process optimization industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- Cloud-based

- On-premises

- Sector

- Large enterprises

- SME

- End-user

- BFSI

- IT and telecom

- Retail

- Manufacturing

- Healthcare

- Solution

- Automation

- Process modeling

- Monitoring and optimization

- Content and document management

- Integration

- Geography

- North America

- US

- Canada

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud-based segment is estimated to witness significant growth during the forecast period.

The market for AI for process optimization is segmented by deployment, with the cloud-based model being the dominant and most rapidly expanding choice.

This model's scalability is crucial for computationally intensive tasks like process mining and discovery and predictive process management. Cloud-native intelligent automation platforms provide the foundation for intelligent workflow automation and continuous process improvement, enabling organizations to achieve end-to-end process visibility.

By integrating technologies such as natural language processing and computer vision systems, these platforms support complex business process re-engineering.

This shift to an operational expenditure model democratizes access to advanced tools like AI-powered digital twins and robotic process automation, with adopters reporting significant operational efficiency gains, including an average 25% reduction in process cycle times.

The Cloud-based segment was valued at in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI For Process Optimization Market Demand is Rising in North America Get Free Sample

North America leads the market, leveraging advanced workflow orchestration tools and AI-driven decision support to drive innovation. In this region, enterprises have reported a 30% improvement in decision-making speed.

Europe follows, with Germany's industrial sector implementing real-time process monitoring and task automation scripts for manufacturing excellence. The APAC region shows the fastest growth, with investment in machine learning model training infrastructure increasing by over 40% annually.

A key focus across all geographies is operational risk mitigation, which is driving the adoption of tools for algorithmic bias detection and establishing clear data lineage and provenance.

This ensures process adherence monitoring and builds trust in intelligent task automation, with firms conducting automated root cause analysis to enhance system reliability.

Market Dynamics

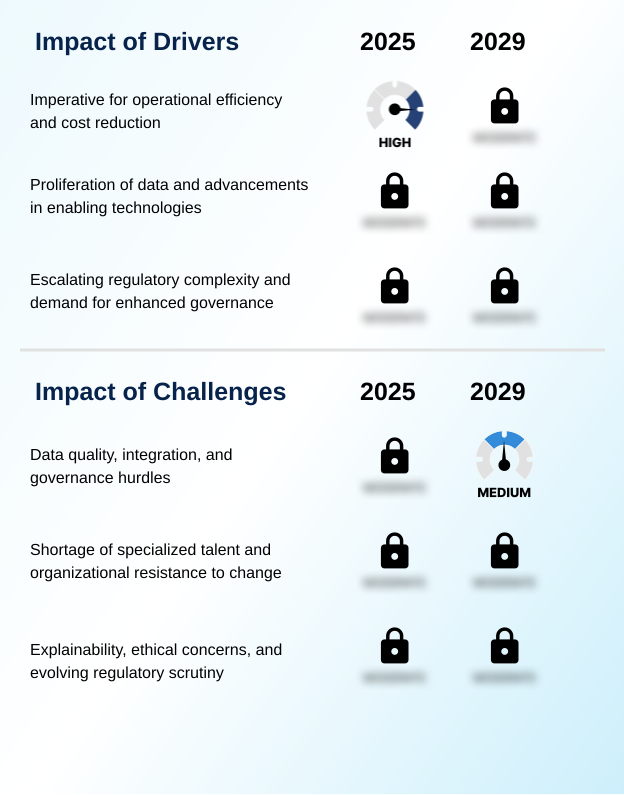

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of AI for process optimization is becoming increasingly nuanced, moving beyond broad-stroke automation to address highly specific operational challenges. For instance, using generative AI for hyperautomation is allowing business analysts, not just developers, to design and deploy complex workflows, democratizing innovation.

- In manufacturing, the benefits of digital twins in manufacturing are profound; these virtual replicas enable companies to simulate production changes, leading to efficiency improvements that are often double what traditional process modeling can achieve. This is particularly crucial for enhancing AI for supply chain resilience, where predictive models can now anticipate disruptions and reroute logistics in near real-time.

- In parallel, the focus on responsible AI in financial services is non-negotiable, with firms now required to prove the fairness of their algorithms. This has spurred demand for AI-powered process mining tools comparison to select solutions with robust explainability features.

- The imperative for automating compliance with AI extends to industries like energy, where AI-driven predictive maintenance in energy not only prevents downtime but also ensures adherence to safety protocols. However, challenges of AI in healthcare operations persist, particularly around data privacy and integration.

- As retailers adopt AI for process optimization in retail to refine inventory and pricing, and logistics firms leverage AI for optimizing last-mile delivery, the common thread is the need to overcome talent gaps for AI implementation.

- Implementing AIOps for network management has become standard for tech firms, while other sectors are exploring AI for personalized customer service and automating HR processes with AI. Success hinges on building transparent systems, as highlighted by the need for explainability in AI-driven lending and the intricate work of securing data for AI model training.

- The impact of AI on manufacturing quality is undeniable, just as the drive to optimize revenue cycle with AI and reduce operational costs with RPA shows clear ROI. Ultimately, tools for AI for optimizing patient flow demonstrate how targeted applications can yield significant societal and business benefits.

What are the key market drivers leading to the rise in the adoption of AI For Process Optimization Industry?

- The imperative for enhancing operational efficiency and achieving significant cost reduction across enterprises stands as a primary driver for market growth.

- The primary driver is the corporate mandate for operational efficiency. Intelligent business process management suites are central to achieving this, enabling predictive maintenance scheduling that reduces equipment downtime by up to 50%.

- In healthcare, patient flow optimization tools have cut wait times by 20%. The proliferation of data is accelerating the adoption of asset performance management and smart factory solutions.

- Technological advancements, particularly generative AI for code and automated code testing, democratize development, while sophisticated network traffic routing algorithms reduce latency.

- The need to manage energy consumption management and the entire AI model lifecycle management efficiently also propels investment, as does the demand for automating processes like automated invoice processing, claims processing automation, and loan underwriting automation.

What are the market trends shaping the AI For Process Optimization Industry?

- The proliferation of generative AI and the push toward hyperautomation are emerging as the most transformative trends. These are fundamentally reshaping process optimization by enabling more intelligent and comprehensive automation strategies.

- A key trend is the integration of generative AI within a hyperautomation framework, creating a more capable AI-augmented workforce. This includes the use of process simulation models for production line optimization, which has improved output by 18% in early adoptions. In manufacturing, automated quality inspection with computer vision detects defects with 99.9% accuracy.

- For logistics network optimization, sophisticated supply chain optimization algorithms enable dynamic resource allocation in real-time. In finance and healthcare, automated compliance checks for regulatory compliance automation and revenue cycle management automation are becoming standard. These fraud detection systems are improving customer journey optimization by reducing friction and enhancing security, leading to optimized resource utilization.

What challenges does the AI For Process Optimization Industry face during its growth?

- Significant challenges related to data quality, complex system integration, and stringent governance requirements present considerable hurdles to widespread market adoption.

- Despite strong market drivers, significant challenges impede widespread adoption. The lack of data readiness is a primary hurdle, as effective cognitive automation and prescriptive analytics engines depend on high-quality data, yet only about 20% of enterprise data is structured and readily usable. Integrating solutions into a cohesive hyperautomation architecture is complex, often hindered by legacy systems.

- A major concern is the 'black box' nature of some models, creating a demand for explainable AI (XAI) to ensure transparent context-aware decisioning, especially in regulated sectors. Organizational resistance and a persistent shortage of specialized talent capable of managing autonomous process optimization also constrain growth.

- Successfully navigating these issues requires not only technological solutions for unstructured data extraction but also robust change management to foster trust in data-driven operational intelligence and human-in-the-loop systems.

Exclusive Technavio Analysis on Customer Landscape

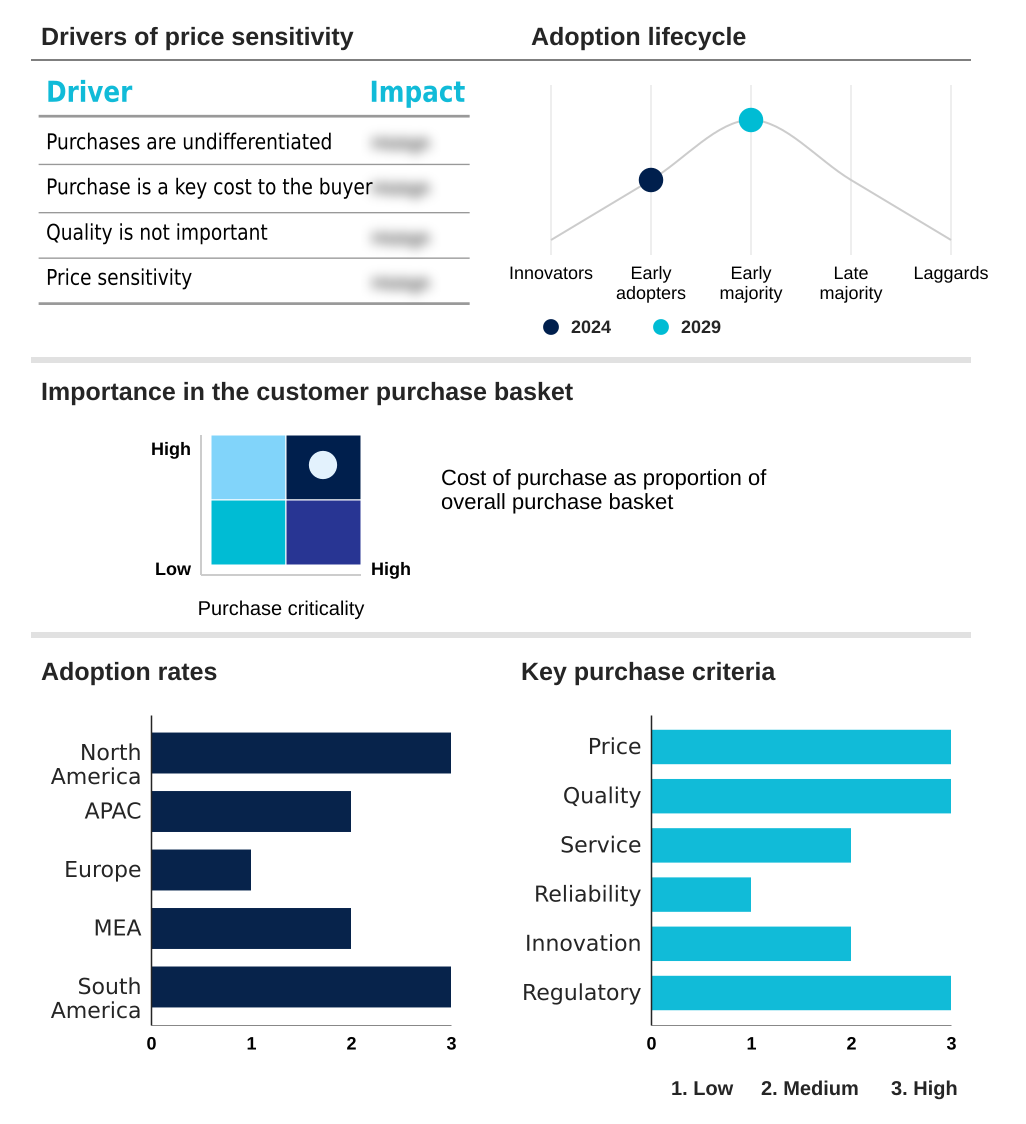

The ai for process optimization market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai for process optimization market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI For Process Optimization Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai for process optimization market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Offerings include AI-powered platforms designed for industrial analytics, asset performance management, and intelligent automation to optimize complex business and operational workflows across diverse enterprise environments.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- Accenture PLC

- Amazon Web Services Inc.

- Aspen Technology Inc.

- Cognizant Technology Solution

- Emerson Electric Co.

- Honeywell International Inc.

- Infosys Ltd.

- IBM Corp.

- KPMG International Ltd.

- Microsoft Corp.

- Oracle Corp.

- Robert Bosch GmbH

- Rockwell Automation Inc.

- SAP SE

- Schneider Electric SE

- Siemens AG

- TIBCO Software Inc.

- Yokogawa Electric Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai for process optimization market

- In October 2024, Oracle Corp. announced a strategic partnership with a leading automotive OEM to integrate its AI-driven supply chain management solutions, aiming to enhance real-time inventory visibility and predictive logistics.

- In January 2025, Siemens AG launched an enhanced version of its Siemens Xcelerator platform, incorporating advanced generative AI capabilities to create self-optimizing digital twins for complex manufacturing environments.

- In March 2025, Accenture PLC completed the acquisition of a specialized AI firm focused on responsible AI and algorithmic auditing, strengthening its consulting services for ethical process optimization in the financial services sector.

- In May 2025, Microsoft Corp. unveiled a new initiative to provide specialized training and AI-powered tools for SMEs, aiming to accelerate the adoption of process optimization solutions within this high-growth market segment.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI For Process Optimization Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 36.3% |

| Market growth 2025-2029 | USD 17237.9 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 29.1% |

| Key countries | US, Canada, China, Japan, India, South Korea, Germany, UK, France, UAE, Saudi Arabia, South Africa, Brazil and Argentina |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI for process optimization market has reached a pivotal stage, transitioning from isolated pilot projects to a fundamental component of corporate strategy. Boardroom decisions are now heavily influenced by the potential of intelligent business process management to drive enterprise-wide transformation.

- Companies are architecting sophisticated ecosystems combining robotic process automation with cognitive automation, underpinned by deep insights from process mining and discovery. Key technologies like natural language processing for unstructured data and computer vision systems for physical asset monitoring are becoming standard. The deployment of AI-powered digital twins is a significant trend, enabling advanced predictive process management and simulation.

- Organizations utilizing these digital replicas for production line optimization have reported a 30% reduction in changeover times. This evolution toward autonomous process optimization is driving demand for explainable AI (XAI) to ensure transparent governance, making algorithmic bias detection a critical capability for maintaining trust and compliance in a highly automated environment.

What are the Key Data Covered in this AI For Process Optimization Market Research and Growth Report?

-

What is the expected growth of the AI For Process Optimization Market between 2025 and 2029?

-

USD 17.24 billion, at a CAGR of 36.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Clou-based, and On-premises), Sector (Large enterprises, and SME), End-user (BFSI, IT and telecom, Retail, Manufacturing, and Healthcare), Solution (Automation, Process modeling, monitoring and optimization, content and document management, and integration) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Imperative for operational efficiency and cost reduction, Data quality, integration, and governance hurdles

-

-

Who are the major players in the AI For Process Optimization Market?

-

ABB Ltd., Accenture PLC, Amazon Web Services Inc., Aspen Technology Inc., Cognizant Technology Solution, Emerson Electric Co., Honeywell International Inc., Infosys Ltd., IBM Corp., KPMG International Ltd., Microsoft Corp., Oracle Corp., Robert Bosch GmbH, Rockwell Automation Inc., SAP SE, Schneider Electric SE, Siemens AG, TIBCO Software Inc. and Yokogawa Electric Corp.

-

Market Research Insights

- Market dynamics are shaped by an intense focus on achieving measurable business outcomes. The shift toward data-driven operational intelligence is compelling organizations to adopt solutions that provide end-to-end process visibility. This has led to a 40% increase in the adoption of platforms enabling intelligent workflow automation over the last two years.

- Implementations focused on supply chain resilience have demonstrated a 25% reduction in stockout incidents by using predictive models. Furthermore, the emphasis on regulatory compliance automation is critical, with firms in regulated industries reporting that automated systems align with compliance frameworks 99.5% of the time, compared to 85% for manual processes.

- This push for efficiency is balanced by the need for human-in-the-loop systems to manage exceptions and provide strategic oversight, ensuring that intelligent task automation augments rather than replaces human expertise, driving continuous process improvement.

We can help! Our analysts can customize this ai for process optimization market research report to meet your requirements.

RIA -

RIA -