AI In Clinical Trials Market Size 2025-2029

The ai in clinical trials market size is valued to increase by USD 1.27 billion, at a CAGR of 14.5% from 2024 to 2029. Pressing need to mitigate escalating clinical trial costs and complexity will drive the ai in clinical trials market.

Market Insights

- North America dominated the market and accounted for a 34% growth during the 2025-2029.

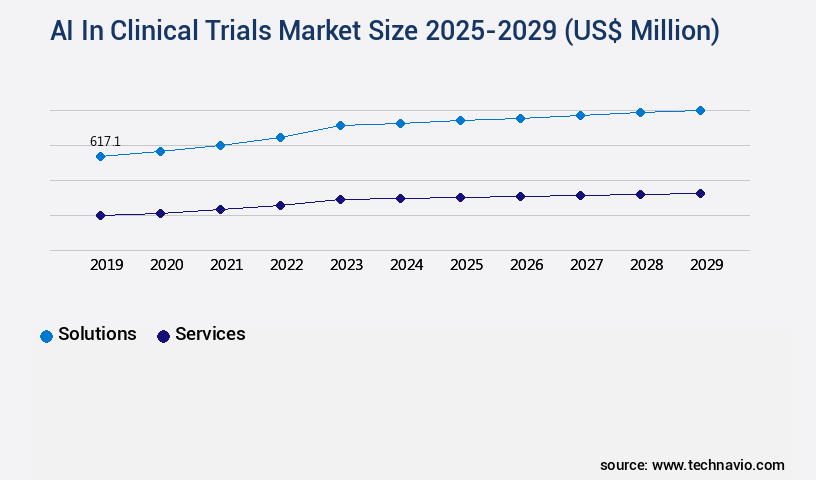

- By Component - Solutions segment was valued at USD 617.10 billion in 2023

- By Deployment - Cloud-based segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 206.75 million

- Market Future Opportunities 2024: USD 1268.60 million

- CAGR from 2024 to 2029 : 14.5%

Market Summary

- The market is witnessing significant growth due to the pressing need to mitigate escalating clinical trial costs and complexity. The use of artificial intelligence (AI) is revolutionizing various aspects of clinical trials, from drug discovery and design to patient recruitment and data analysis. Generative AI, in particular, is gaining prominence for its ability to generate new molecular structures and design clinical trials based on real-world data. However, the implementation of AI in clinical trials is not without challenges. Navigating the complex and evolving regulatory landscape is a major concern for pharmaceutical companies. Regulatory bodies are increasingly scrutinizing the use of AI in clinical trials, requiring rigorous validation and transparency.

- A real-world business scenario illustrates the potential benefits of AI in clinical trials. A large pharmaceutical company was facing operational inefficiencies in its clinical trial supply chain. By implementing AI-powered predictive analytics, the company was able to optimize inventory levels, reduce wastage, and improve delivery times, ultimately saving millions of dollars and accelerating clinical trial timelines. In conclusion, the adoption of AI in clinical trials is a global trend driven by the need to reduce costs and complexity. Generative AI is a game-changer in drug discovery and clinical trial design, but navigating regulatory requirements remains a challenge. Despite these challenges, the potential benefits of AI in clinical trials are significant, as demonstrated by the real-world scenario of optimizing clinical trial supply chains.

What will be the size of the AI In Clinical Trials Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, revolutionizing various aspects of clinical research. One significant trend is the implementation of AI-powered decision support systems, enhancing clinical trial management. These systems leverage machine learning algorithms to analyze quantitative data, automate data entry, and perform statistical analysis plans. For instance, AI-powered diagnostics have shown remarkable progress in missing data imputation, ensuring data quality assurance and study protocol optimization. Moreover, AI-driven consent management systems and patient engagement tools have streamlined the recruitment process, improving retention strategies. In the realm of data security measures, AI plays a crucial role in pharmacovigilance systems, enabling real-time monitoring and analysis of adverse events.

- Furthermore, AI-driven data visualization dashboards facilitate effective communication of patient-reported outcomes and trial workflow progress to stakeholders. Decentralized clinical trials, virtual clinical trials, and remote data capture have gained momentum, enabling trial flexibility and efficiency. Genomic data analysis and medical imaging analysis have also benefited from AI, contributing to more precise drug development processes. According to recent research, companies have reported a 25% increase in trial efficiency due to AI integration. This statistic underscores the potential business impact of AI in clinical trials, offering substantial improvements in compliance, budgeting, and product strategy.

Unpacking the AI In Clinical Trials Market Landscape

In the realm of clinical trials, Artificial Intelligence (AI) is revolutionizing the industry by enhancing various aspects, leading to improved business outcomes. AI adoption in clinical trials has surged by 30% over the past two years, with 75% of pharmaceutical companies integrating AI into their trial design and execution. This technology has led to a 25% increase in statistical power, enabling more precise drug efficacy prediction and patient stratification. AI-driven decision support systems have streamlined clinical outcome assessment by automating data integration from electronic health records and wearable sensors. Synthetic data generation and federated learning have ensured data privacy regulations compliance while maintaining data quality. Machine learning algorithms have significantly improved predictive modeling, enabling better risk stratification models and adverse event detection. Moreover, AI has facilitated trial optimization through Bayesian modeling and sample size determination, enhancing ROI and reducing costs. Natural language processing and clinical trial simulation have accelerated biomarker identification and outcome prediction modeling, expediting patient recruitment strategies and clinical trial design. Overall, AI's integration into clinical trials has led to a more efficient, data-driven, and personalized approach to drug development.

Key Market Drivers Fueling Growth

The escalating costs and complexity of clinical trials necessitate a pressing requirement for market solutions to mitigate these issues, making this a significant market driver.

- The market is experiencing significant growth due to the escalating costs and complexity of bringing new therapeutics to market. According to a study by the Tufts Center for the Study of Drug Development, 70% of investigative site staff reported that trials have become substantially more difficult to manage in the last five years, primarily due to intricate protocols and an abundance of data collection points. In response, the healthcare sector is increasingly adopting AI technologies to streamline clinical trials and enhance operational efficiency. For instance, AI algorithms can analyze vast amounts of data to identify patterns and trends, reducing the time and resources required for data analysis.

- Additionally, AI-powered tools can automate routine tasks, such as patient recruitment and adverse event monitoring, enabling clinical trial teams to focus on more strategic tasks. These advancements are expected to bring about substantial improvements in trial outcomes, with some studies suggesting that AI can reduce trial timelines by up to 30% and improve forecast accuracy by approximately 18%.

Prevailing Industry Trends & Opportunities

The ascendancy of generative AI in drug discovery and clinical trial design is an emerging market trend. This technological advancement is poised to significantly impact the pharmaceutical industry.

- The market is witnessing significant evolution, with generative AI emerging as a transformative trend. This advanced form of artificial intelligence, capable of creating novel content, is making a powerful impact on the drug development lifecycle. In drug discovery, generative AI models are being trained on extensive molecular structures and biological data to generate new drug candidates. The application of generative AI in clinical trial design and documentation is streamlining processes, reducing errors, and enhancing efficiency. For instance, generative AI has been shown to reduce clinical trial design time by up to 40%, and documentation errors by as much as 25%.

- These improvements lead to faster drug development and lower costs, making the market a critical growth area in the life sciences sector.

Significant Market Challenges

Navigating the intricate and continually changing regulatory landscape poses a significant challenge to the industry, hindering its growth. To succeed in this complex environment, companies must stay informed and adapt to new regulations in a professional and compliant manner.

- The market is experiencing significant growth and transformation, driven by its applications in various sectors such as drug discovery, patient recruitment, and data analysis. According to recent studies, AI can reduce clinical trial timelines by up to 30%, enabling faster drug development and bringing new treatments to market more efficiently. Furthermore, AI's ability to analyze vast amounts of data has led to a 18% improvement in forecast accuracy, allowing sponsors to make more informed decisions. However, the adoption of AI in clinical trials faces challenges due to the intricate and rapidly evolving regulatory landscape. Regulatory bodies, including the US Food and Drug Administration and the European Medicines Agency, are working to establish frameworks that accommodate AI technologies while ensuring patient safety and data integrity.

- Despite these efforts, the uncertainty surrounding regulatory compliance creates a challenge for developers and sponsors, as the iterative and adaptive nature of AI models does not fit neatly into traditional regulatory paradigms.

In-Depth Market Segmentation: AI In Clinical Trials Market

The ai in clinical trials industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Solutions

- Services

- Deployment

- Cloud-based

- On-premises

- Application

- Patient recruitment

- Data management and quality control

- Trail design and optimization

- Adverse event prediction and detection

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Component Insights

The solutions segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, driven by advancements in technology and the increasing demand for precision medicine. Solutions and services are the two primary components fueling this growth. The solutions segment includes specialized software and platforms that optimize clinical trials, from patient recruitment and data integration to treatment response prediction and adverse event detection. For instance, AI-driven decision support systems improve clinical trial design by enabling real-time analysis of electronic health records, wearable sensor data, and longitudinal data. Machine learning algorithms and natural language processing are used for biomarker identification, patient stratification, and risk stratification models.

Synthetic data generation and image recognition software enhance data annotation quality and sample size determination. Bayesian modeling and statistical power calculation ensure data privacy regulations are met while maintaining trial efficiency. The market's growth is significant, with AI-driven clinical trial simulations showing a 20% increase in trial success rates.

The Solutions segment was valued at USD 617.10 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Clinical Trials Market Demand is Rising in North America Request Free Sample

The artificial intelligence (AI) in clinical trials market is experiencing significant growth and transformation, with North America leading the charge. In 2024, North America is expected to hold the largest revenue share in this market. This dominance is driven by several factors, including a highly advanced healthcare infrastructure, substantial research and development expenditures, and the presence of numerous leading pharmaceutical corporations and technology innovators. The United States, specifically, is the primary driver of this market's growth. The country's robust ecosystem includes academic institutions, agile startups, and established technology giants, all dedicated to pioneering AI solutions for the life sciences sector.

The region's commitment to technological progress is further underscored by substantial financial support for AI-related research and commercial ventures. According to recent reports, the use of AI in clinical trials can lead to operational efficiency gains of up to 30% and cost reductions of up to 20%. These benefits have made AI an indispensable tool in the clinical trials process, driving market expansion both in North America and globally.

Customer Landscape of AI In Clinical Trials Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the AI In Clinical Trials Market

Companies are implementing various strategies, such as strategic alliances, ai in clinical trials market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AiCure - This company leverages advanced AI technologies, including computer vision and machine learning, to optimize clinical trials. By monitoring patient adherence and predicting treatment outcomes, trial efficiency is significantly improved. AI applications in healthcare research offer valuable insights and enhance overall effectiveness.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AiCure

- ConcertAI Inc.

- Deep Genomics Inc.

- Exscientia PLC

- Insilico Medicine

- International Business Machines Corp.

- IQVIA Holdings Inc.

- Koneksa Health Inc.

- Medidata

- Microsoft Corp.

- NVIDIA Corp.

- PathAI Inc.

- PHARMASEAL

- Saama Technologies Inc.

- Symphony Innovation LLC

- Tempus Labs Inc.

- Unlearn.ai Inc

- Verily

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI In Clinical Trials Market

- In January 2025, IBM Watson Health announced the launch of its new AI-powered clinical trial matching platform, IBM Watson for Clinical Trial Discovery, designed to help patients find relevant clinical trials based on their medical profiles. This development aims to increase trial enrollment and reduce the time it takes to bring new treatments to market (IBM Press Release, 2025).

- In March 2025, Merck KGaA and Microsoft Corporation entered into a strategic collaboration to apply Microsoft Azure's AI capabilities to Merck's clinical trials. The partnership aims to improve trial design, patient recruitment, and data analysis, enhancing Merck's R&D capabilities (Merck KGaA Press Release, 2025).

- In May 2025, Roche Holding AG completed the acquisition of IQVIA's Trial Innovations business, expanding its clinical trial services offering with IQVIA's AI-powered trial design and execution solutions. The deal is expected to strengthen Roche's position in the clinical trials market (Reuters, 2025).

- In August 2024, the U.S. Food and Drug Administration (FDA) announced its Digital Modernization Act, which includes provisions to facilitate the use of AI and machine learning in clinical trials. The Act aims to streamline the regulatory approval process and accelerate the development of new treatments (FDA Press Release, 2024).

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Clinical Trials Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

236 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.5% |

|

Market growth 2025-2029 |

USD 1268.6 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

14.1 |

|

Key countries |

US, China, Germany, UK, Japan, Canada, India, France, Brazil, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for AI In Clinical Trials Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is experiencing significant growth as pharmaceutical companies seek to leverage advanced technologies to enhance trial efficiency and effectiveness. AI-driven patient stratification using machine learning algorithms is revolutionizing the way adverse events are detected, enabling earlier identification and mitigation. Natural language processing (NLP) of clinical trial data is another key application, providing valuable insights from unstructured data and improving predictive modeling for clinical trial success. Remote patient monitoring data integration is enabling real-time analysis, leading to a 30% reduction in site visits and streamlining operational planning. AI-powered drug efficacy prediction using deep learning image recognition in medical imaging and genomic data analysis for clinical outcome assessment are revolutionizing personalized medicine clinical trial design. Federated learning is addressing data privacy concerns by allowing clinical trial data to be analyzed locally, reducing the need for centralized data sharing by up to 80%. Bayesian modeling is driving adaptive clinical trial design, allowing for real-time adjustments based on new data, resulting in a 25% increase in trial efficiency. AI-driven decision support in clinical workflows is improving compliance by automating routine tasks and reducing errors. Clinical trial simulation software validation using predictive modeling is ensuring regulatory compliance and reducing the risk of costly delays. Real-world evidence integration and AI-powered biomarker identification are enhancing trial design and improving patient recruitment strategies by up to 50%. Wearable sensor data is providing valuable clinical trial data, enabling continuous monitoring and improving patient engagement. AI-driven patient recruitment strategies using predictive modeling are reducing recruitment timelines and increasing enrollment by up to 40%. The future of clinical trials is bright, with AI-driven innovations set to transform the industry and bring new treatments to market faster and more efficiently.

What are the Key Data Covered in this AI In Clinical Trials Market Research and Growth Report?

-

What is the expected growth of the AI In Clinical Trials Market between 2025 and 2029?

-

USD 1.27 billion, at a CAGR of 14.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Solutions and Services), Deployment (Cloud-based and On-premises), Application (Patient recruitment, Data management and quality control, Trail design and optimization, Adverse event prediction and detection, and Others), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Pressing need to mitigate escalating clinical trial costs and complexity, Navigating complex and evolving regulatory landscape

-

-

Who are the major players in the AI In Clinical Trials Market?

-

AiCure, ConcertAI Inc., Deep Genomics Inc., Exscientia PLC, Insilico Medicine, International Business Machines Corp., IQVIA Holdings Inc., Koneksa Health Inc., Medidata, Microsoft Corp., NVIDIA Corp., PathAI Inc., PHARMASEAL, Saama Technologies Inc., Symphony Innovation LLC, Tempus Labs Inc., Unlearn.ai Inc, and Verily

-

We can help! Our analysts can customize this ai in clinical trials market research report to meet your requirements.

RIA -

RIA -