AI In Hardware Market Size 2025-2029

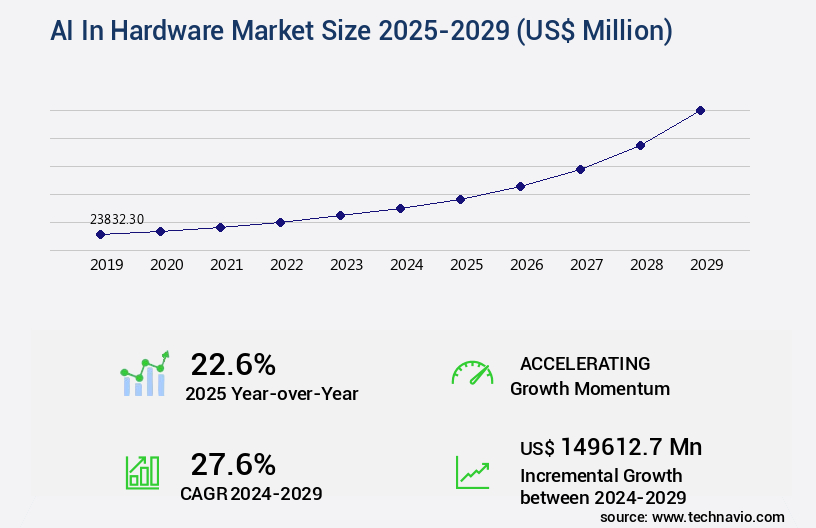

The AI in hardware market size is valued to increase by USD 149.61 billion, at a CAGR of 27.6% from 2024 to 2029. Explosive growth of generative AI and large language models will drive the ai in hardware market.

Major Market Trends & Insights

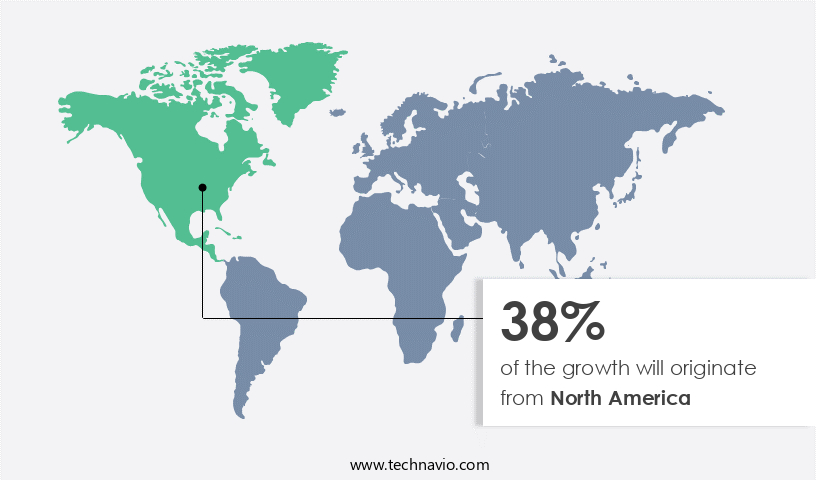

- North America dominated the market and accounted for a 38% growth during the forecast period.

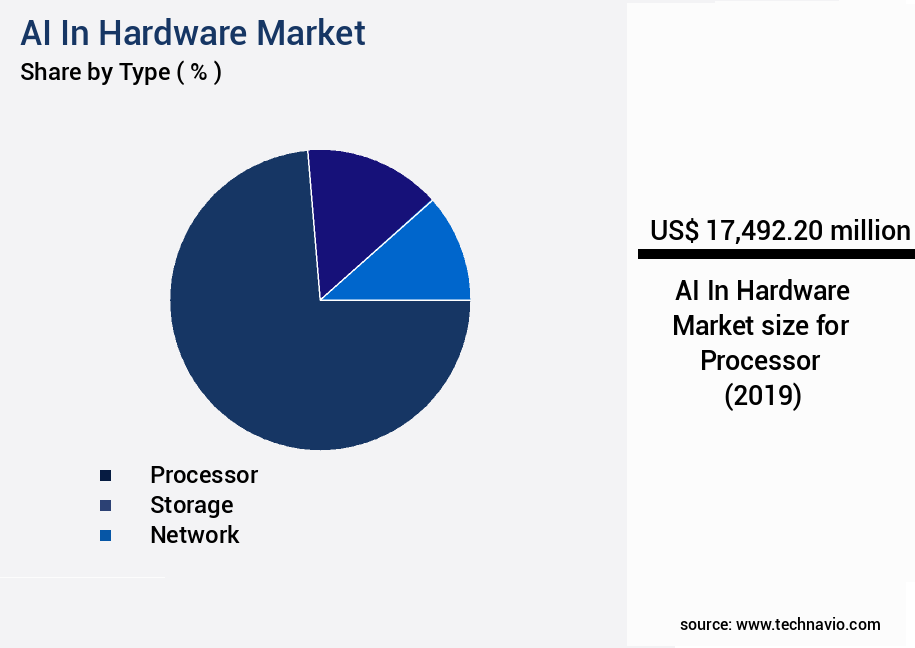

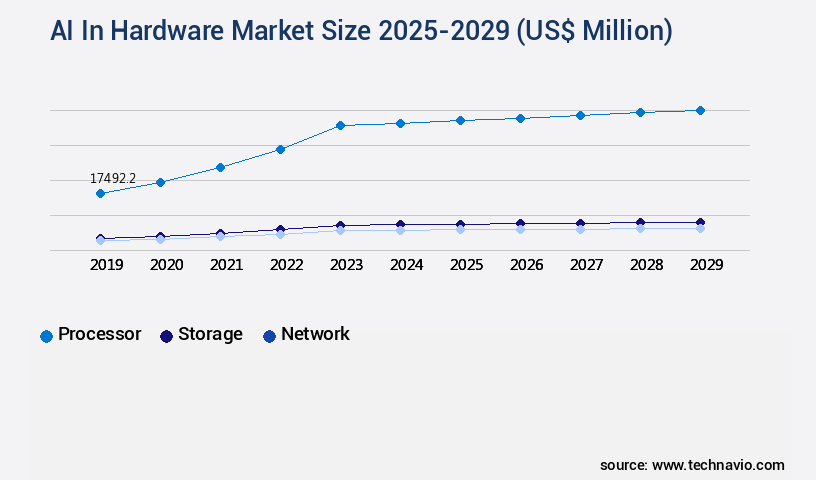

- By Type - Processor segment was valued at USD 17.49 billion in 2023

- By Technology - Machine learning segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 791.53 million

- Market Future Opportunities: USD 149612.70 million

- CAGR from 2024 to 2029 : 27.6%

Market Summary

- The market is experiencing explosive growth, with industry analysts projecting a value of USD190.67 billion by 2025. This expansion is driven by the shift towards domain-specific and application-specific architectures, enabling advanced capabilities in industries such as healthcare, finance, and manufacturing. Market growth is further fueled by the increasing demand for edge AI devices, cloud computing platforms, and data center infrastructure. However, this progress comes with challenges. Extreme power consumption and thermal management are major concerns, necessitating the development of more energy-efficient solutions.

- As AI applications become increasingly complex, hardware manufacturers must balance performance and power efficiency to meet the demands of businesses and consumers alike. This dynamic market requires continuous innovation and collaboration between hardware and software developers to deliver efficient, scalable, and reliable AI solutions.

What will be the Size of the AI In Hardware Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI In Hardware Market Segmented ?

The AI in hardware industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Processor

- Storage

- Network

- Technology

- Machine learning

- Deep learning

- Computer vision

- Generative AI

- Others

- End-user

- IT and telecom

- Healthcare

- Banking and finance

- Robotics

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The processor segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant advancements, with the processor segment spearheading innovation and competition. This sector includes GPUs, ASICs, FPGAs, and CPUs with dedicated AI acceleration. The performance of these processors plays a crucial role in the feasibility and capability of deploying intricate AI models. Currently, GPUs reign supreme due to their massively parallel architecture, which excels in the matrix multiplication and tensor operations essential for deep learning. NVIDIA, a market leader, continues to push boundaries, introducing the H200 GPU in November 2023 to cater to the memory-intensive inference process and later unveiling the Blackwell architecture in March 2024, a platform tailored for trillion-parameter scale generative AI.

Meanwhile, other technologies like ASIC design, FPGA implementation, algorithm optimization, and neuromorphic computing are gaining traction, contributing to the evolving landscape. A recent study reveals that The market is projected to reach a value of USD191.2 billion by 2027, underscoring its immense potential.

The Processor segment was valued at USD 17.49 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Hardware Market Demand is Rising in North America Request Free Sample

The market is experiencing a dynamic evolution, with North America, spearheaded by the United States, leading the charge. This region is the hub of innovation and industry standard-setting, hosting the largest consumers of advanced silicon. Notable AI accelerator designers, such as NVIDIA, AMD, and Intel, are headquartered here, shaping the technological trajectory for the entire ecosystem. In March 2024, NVIDIA solidified its market dominance with the introduction of its next-generation Blackwell architecture, specifically engineered for the generative AI era.

Competition remains fierce, as evidenced by AMD's December 2023 launch of its Instinct MI300 accelerator series and Intel's April 2024 announcement of its Gaudi 3 AI accelerator. This cutthroat competition fuels continuous innovation, as demonstrated by these companies' latest offerings.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as businesses and organizations seek to optimize AI inference chip performance for various applications. FPGA-based AI acceleration is gaining popularity due to its flexibility and ability to adapt to changing workloads. However, GPUs, long the go-to solution for high-performance computing clusters, face memory capacity limits when dealing with large deep learning models. Edge devices, with their power constraints, require AI hardware designs that prioritize efficiency. Deep learning model compression techniques, such as pruning and quantization, help reduce model size and power consumption. AI hardware thermal design challenges are also a major consideration, as high temperatures can impact performance and reliability.

Data centers, home to high-performance computing clusters and AI workloads, face cooling infrastructure challenges due to the heat generated by GPUs and other hardware components. Network latency is another concern, as it can significantly impact real-time AI processing frameworks and robotics hardware control systems. System-on-chip design for AI is a key trend, as it enables parallel processing for AI workloads and reduces power consumption. Reconfigurable hardware for AI, such as FPGAs and ASICs, offer customizable solutions for specific AI applications. Digital signal processing algorithms and computer vision hardware architecture are essential components of AI hardware design. Natural language processing chips and sensor data fusion techniques are also important areas of research and development in the market. Low-power AI hardware design is a priority for edge devices and robotics applications, ensuring long battery life and reliable operation. Overall, The market is a dynamic and innovative space, with ongoing research and development addressing the unique challenges of AI hardware design.

What are the key market drivers leading to the rise in the adoption of AI In Hardware Industry?

- The explosive growth of generative AI and large language models is the primary catalyst fueling market expansion in this domain.

- The market is experiencing a significant shift, fueled by the escalating demand for generative artificial intelligence and large language models. These advanced models, which can contain hundreds of billions to trillions of parameters, surpass the capabilities of general-purpose processors. Consequently, there is a growing need for specialized, massively parallel hardware to meet the demands of training and deploying these models. This requirement calls for hardware with immense computational power, memory bandwidth, and capacity.

- The semiconductor industry is responding to this trend by realigning product roadmaps to accommodate the unique needs of AI hardware. This dynamic underscores the importance of AI hardware in driving innovation and advancing applications across various sectors, including healthcare, finance, and manufacturing.

What are the market trends shaping the AI In Hardware Industry?

- Shifting toward domain-specific and application-specific architecture is the emerging trend in the technology market. This approach focuses on designing systems tailored to specific industries and applications.

- The market is experiencing a transformative phase, moving beyond the era of general-purpose GPUs towards domain-specific architectures. This shift reflects the maturation of the AI industry, which demands hardware optimized for specific workloads and applications to enhance efficiency and cost-effectiveness. Hyperscale cloud providers, such as Amazon Web Services, are leading this trend by designing application-specific integrated circuits (ASICs) to cater to their unique software ecosystems.

- For instance, Amazon introduced Inferentia2 and Trainium2 chips in November 2023, specifically designed for inference and training workloads, respectively. This strategic move underscores the growing importance of hardware customization in maximizing performance per watt and performance per dollar.

What challenges does the AI In Hardware Industry face during its growth?

- The significant challenges facing the industry's growth include the need to address extreme power consumption and effective thermal management.

- The market is undergoing significant evolution due to the escalating power consumption and thermal management challenges posed by high-performance accelerators. As AI models, specifically large language models, grow in intricacy, the hardware necessary to train and operate them demands an exponentially expanding electricity supply. A single advanced AI server rack can consume up to tens of kilowatts, and a complete data center cluster can draw power akin to a small city.

- This predicament raises operational concerns, as the substantial electricity costs become a substantial portion of the total cost of ownership for AI infrastructure. This issue affects the economic feasibility of certain applications, making it a pressing concern for the AI industry.

Exclusive Technavio Analysis on Customer Landscape

The ai in hardware market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in hardware market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Hardware Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in hardware market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - The company specializes in AI hardware technology, providing advanced solutions through Instinct MI300 series accelerators for efficient AI training and high-performance computing. These innovations significantly enhance machine learning capabilities and computing power for various industries.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Alibaba Cloud

- Amazon Web Services Inc.

- Apple Inc.

- Broadcom Inc.

- Cerebras

- Enfabrica Corp.

- Google LLC

- Graphcore Ltd.

- Huawei Technologies Co. Ltd.

- Intel Corp.

- International Business Machines Corp.

- Micron Technology Inc.

- Microsoft Corp.

- NVIDIA Corp.

- Qualcomm Inc.

- SambaNova Systems Inc.

- Samsung Electronics Co. Ltd.

- Shenzhen Intellifusion Technologies Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI In Hardware Market

- In January 2024, Intel introduced its new Neural Compute Stick 2.0, a compact AI accelerator designed for edge computing applications (Intel Press Release). This development marked a significant advancement in making AI capabilities more accessible to a broader range of industries and businesses.

- In March 2024, NVIDIA and Microsoft announced a strategic partnership to optimize Microsoft Azure services for NVIDIA GPUs, enabling seamless deployment of AI workloads in the cloud (NVIDIA Press Release). This collaboration aimed to strengthen the position of both companies in the AI market by offering enhanced computing power and cloud services to their clients.

- In April 2025, Google and Samsung announced a strategic investment of USD391 million in their joint AI chip development project, BrainChip (Google Press Release). This substantial investment signaled a commitment to advancing AI hardware technology and increasing their market presence in the competitive AI landscape.

- In May 2025, Qualcomm announced the acquisition of Cirrus Logic's wireless and wired audio and connectivity business for approximately USD4.5 billion (Qualcomm Press Release). This acquisition expanded Qualcomm's product portfolio and strengthened its position in the AI hardware market by adding expertise in audio and connectivity technologies, crucial components for edge AI devices.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Hardware Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

251 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 27.6% |

|

Market growth 2025-2029 |

USD 149612.7 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

22.6 |

|

Key countries |

US, China, Canada, Japan, Germany, UK, South Korea, Mexico, France, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI hardware market continues to evolve, driven by advancements in computer vision, ASIC design, and low-power computing. Power efficiency metrics and thermal management are paramount as AI model deployment expands into embedded systems and robotics hardware. AI inference engines are increasingly integrated into these applications, fueling growth in the market. For instance, the automotive industry is projected to witness a 25% compound annual growth rate (CAGR) in the adoption of AI inference engines by 2025. ASIC design plays a crucial role in enhancing the performance of AI accelerators, such as GPUs and FPGAs, through algorithm optimization and FPGA implementation.

- Neuromorphic computing and hardware security modules are emerging technologies, adding to the market's dynamism. Power efficiency and memory bandwidth are critical considerations in the design of deep learning hardware, with latency optimization and network bandwidth essential for real-time processing. The integration of AI in edge devices and cloud computing platforms necessitates the development of high-performance computing infrastructure. Digital signal processing and natural language processing are additional applications of AI hardware, further expanding its reach. Reconfigurable logic and sensor integration are also key areas of focus, enabling advancements in AI training systems and AI model deployment. In conclusion, the AI hardware market is a continuously unfolding landscape, with applications spanning various sectors.

- The ongoing development of computer vision hardware, ASIC design, and low-power computing are driving innovation and growth. Power efficiency metrics, thermal management, and algorithm optimization are essential considerations as AI inference engines and accelerators are integrated into embedded systems and robotics hardware. The market's evolution is marked by the emergence of new technologies, such as neuromorphic computing and hardware security modules, and the expansion of AI into new applications, such as digital signal processing and natural language processing.

What are the Key Data Covered in this AI In Hardware Market Research and Growth Report?

-

What is the expected growth of the AI In Hardware Market between 2025 and 2029?

-

USD 149.61 billion, at a CAGR of 27.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Processor, Storage, and Network), Technology (Machine learning, Deep learning, Computer vision, Generative AI, and Others), End-user (IT and telecom, Healthcare, Banking and finance, Robotics, and Others), and Geography (North America, APAC, Europe, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Explosive growth of generative AI and large language models, Extreme power consumption and thermal management

-

-

Who are the major players in the AI In Hardware Market?

-

Advanced Micro Devices Inc., Alibaba Cloud, Amazon Web Services Inc., Apple Inc., Broadcom Inc., Cerebras, Enfabrica Corp., Google LLC, Graphcore Ltd., Huawei Technologies Co. Ltd., Intel Corp., International Business Machines Corp., Micron Technology Inc., Microsoft Corp., NVIDIA Corp., Qualcomm Inc., SambaNova Systems Inc., Samsung Electronics Co. Ltd., and Shenzhen Intellifusion Technologies Co. Ltd.

-

Market Research Insights

- The market for AI in hardware is a dynamic and ever-evolving landscape. Two key statistics illustrate its continuous growth. First, the global spending on AI hardware is projected to reach USD125.1 billion by 2026, representing a compound annual growth rate (CAGR) of approximately 35% between 2021 and 2026. Second, a recent study showed that implementing AI in data centers can lead to a 10% increase in server utilization, translating to significant cost savings for organizations. Performance benchmarks, hardware reliability, maintenance procedures, memory hierarchy, neural network hardware, power consumption, processor architecture, debugging techniques, cost optimization, scalability issues, supply chain management, model quantization, development tools, software frameworks, data compression, ethical considerations, AI chipsets, security protocols, manufacturing process, energy efficiency, throughput optimization, fault tolerance, precision requirements, and cooling solutions are essential components shaping the market's development.

- Companies are constantly innovating to address these challenges and improve the efficiency, effectiveness, and accessibility of AI hardware solutions.

We can help! Our analysts can customize this AI in hardware market research report to meet your requirements.

RIA -

RIA -