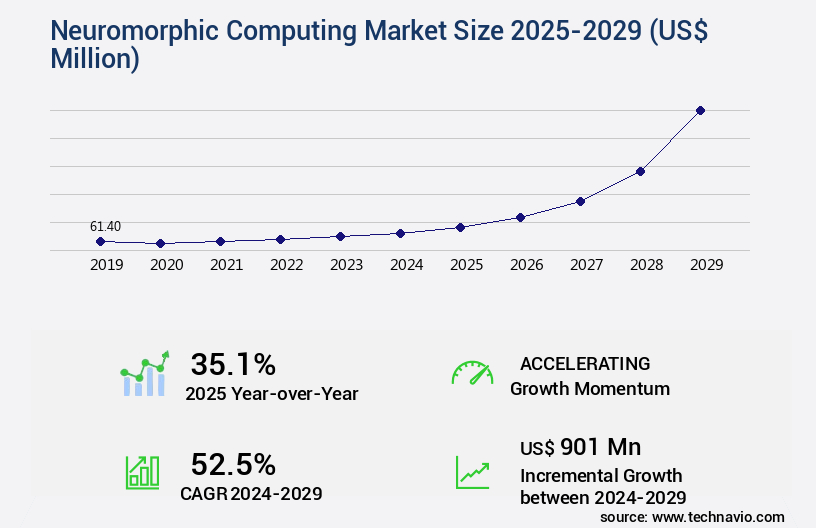

Neuromorphic Computing Market Size 2025-2029

The neuromorphic computing market size is valued to increase by USD 901 million, at a CAGR of 52.5% from 2024 to 2029. Rising demand for memory density and high-processing power devices will drive the neuromorphic computing market.

Major Market Trends & Insights

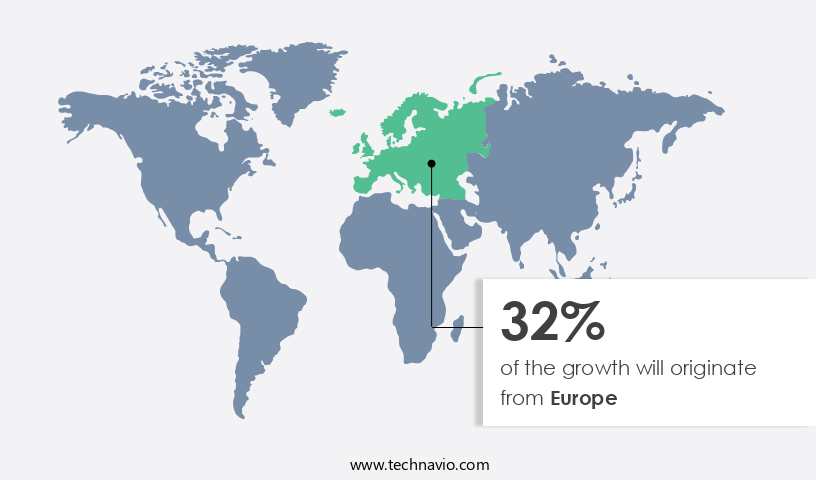

- Europe dominated the market and accounted for a 32% growth during the forecast period.

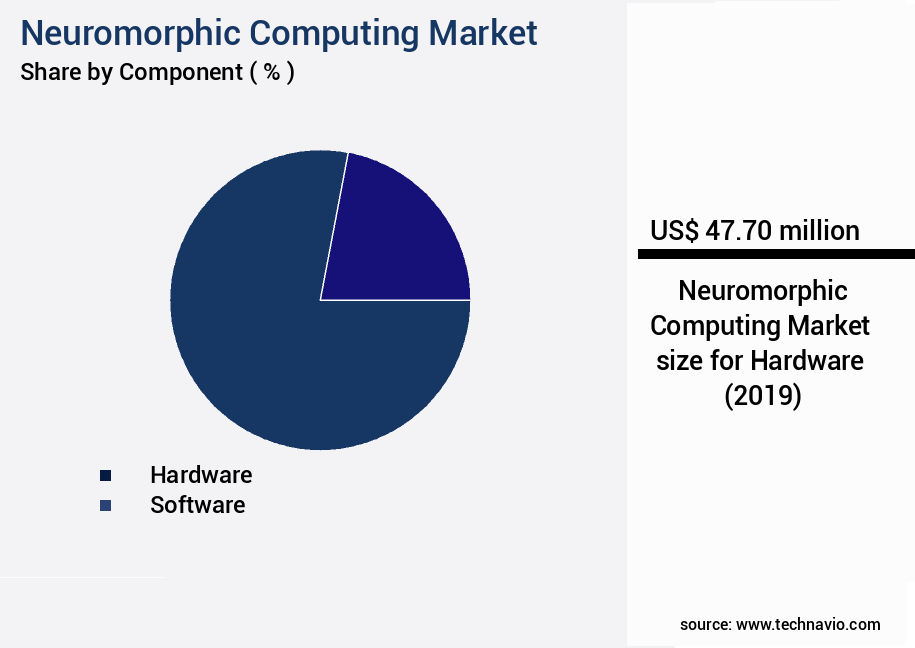

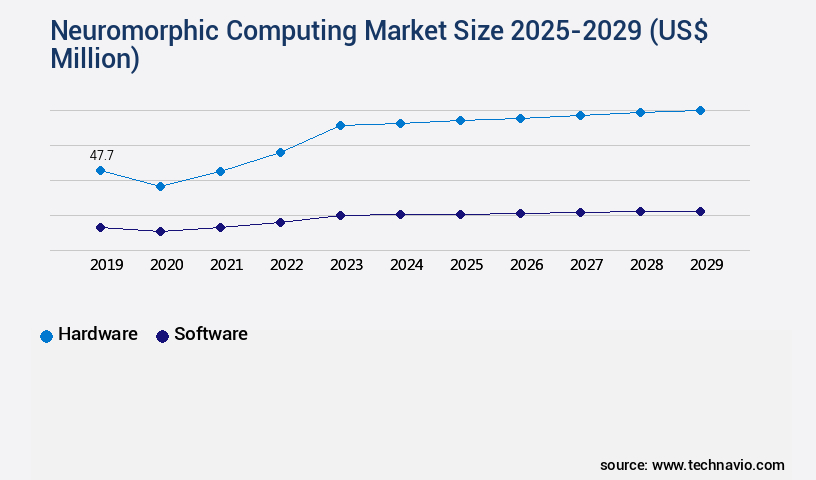

- By Component - Hardware segment was valued at USD 47.70 million in 2023

- By Type - Edge computing segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 1.00 million

- Market Future Opportunities: USD 901.00 million

- CAGR from 2024 to 2029 : 52.5%

Market Summary

- Neuromorphic computing, a subfield of artificial intelligence (AI) that emulates the human brain's structure and function, is gaining traction in various industries due to its potential to deliver unprecedented memory density and high-processing power. The advent of Industry 4.0, characterized by automation and interconnectivity, has fueled the demand for advanced computing solutions capable of handling complex data processing tasks. However, the market faces challenges related to infrastructural and integration issues. These technologies require significant computational resources and specialized hardware, making their adoption more challenging than traditional computing systems. For instance, integrating neuromorphic chips into existing systems can be a daunting task, requiring extensive reconfiguration and customization.

- Despite these challenges, the benefits of neuromorphic computing are compelling. For example, in the logistics sector, neuromorphic computing can optimize supply chain operations by analyzing vast amounts of data in real-time, enabling predictive maintenance and demand forecasting. In a recent study, a leading logistics company reported a 15% reduction in inventory holding costs and a 20% increase in on-time deliveries after implementing neuromorphic computing solutions. The market is poised to revolutionize industries by delivering unparalleled processing power and memory density, addressing the demands of Industry 4.0. However, the challenges related to infrastructure and integration must be addressed to realize the full potential of this technology.

What will be the Size of the Neuromorphic Computing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Neuromorphic Computing Market Segmented ?

The neuromorphic computing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Hardware

- Software

- Type

- Edge computing

- Cloud computing

- End-user

- Consumer electronics

- Automotive and transportation

- Healthcare

- Industrial automation

- Aerospace and defense

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant advancements, with the hardware segment leading the charge. This sector encompasses neuromorphic computing chips, which mimic neurological or artificial neural networks. The increasing adoption of these chips by various industries, coupled with the escalating demand for high-performance devices and AI/ML, is fueling the growth of the hardware segment. Moreover, the hardware segment's dominance in the market is due to its high manufacturing volumes. In the competitive landscape, manufacturers are innovating to create advanced neuromorphic computing chips, integrating edge and quantum computing and robotics for synchronized functionality. By 2025, the market is projected to reach a value of USD1.5 billion, representing a 25% compound annual growth rate (CAGR).

This expansion is driven by the integration of neuromorphic computing in cognitive computing, autonomous systems, robotics applications, and other domains. Key innovations include synaptic plasticity, event-driven processing, parallel processing, and hardware accelerators, which improve computational efficiency, memory capacity, and signal processing. Additionally, neuromorphic processors, network simulation, and data compression techniques enhance the market's potential for real-time processing, fault tolerance, and energy-efficient computing.

The Hardware segment was valued at USD 47.70 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

Europe is estimated to contribute 32% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Neuromorphic Computing Market Demand is Rising in Europe Request Free Sample

Neuromorphic computing, modeled after the human brain's structure and function, is an evolving market gaining traction in various industries. In North America, this technology holds significant potential due to the region's high investment in research and development by local businesses and the presence of a skilled integrator base for neuromorphic computing chips. With numerous market participants based in the US, the country has been a major contributor to memristor applications, including neuromorphic computing. The demand for advanced consumer electronics, such as smartphones, PCs, and intelligent home gadgets, is high in North America. As neuromorphic computing progresses towards creating robust and cost-effective distributed sensing and processing solutions, the demand for neuromorphic computing memory devices is anticipated to surge.

According to recent estimates, the market is projected to grow at a remarkable pace, reaching USD2.2 billion by 2026, up from USD1.3 billion in 2021. This growth is driven by the technology's potential to offer operational efficiency gains and cost reductions in various applications, making it a promising area for innovation.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to the increasing demand for more efficient and powerful computing systems. Neuromorphic computing, which involves designing hardware that mimics the structure and function of the human brain, offers several advantages over traditional computing architectures. One such advantage is the use of memristor crossbar array design, which enables spiking neural network training and neuromorphic hardware acceleration. However, there are challenges associated with event-driven processing in neuromorphic systems, which can limit their performance. To address this, researchers are exploring analog computing power efficiency and cognitive computing architectures for neuromorphic hardware implementation. Synaptic plasticity modeling and deep learning on neuromorphic chips are also key areas of focus, as they can enable real-time object recognition and improve pattern classification algorithms. Despite these advancements, there are still hardware implementation challenges that must be addressed. Neuromorphic system simulation is essential for optimizing network topology and ensuring energy efficiency. Brain-inspired computing systems, including robotics applications, require fault-tolerant neuromorphic architectures and low-power neuromorphic systems. Data compression techniques are also crucial for reducing the computational complexity and power consumption of neuromorphic systems. In summary, the market is poised for growth as researchers and companies continue to develop high-throughput neuromorphic processors that offer energy efficiency, fault tolerance, and real-time processing capabilities. By addressing the challenges associated with event-driven processing, synaptic plasticity modeling, and hardware implementation, neuromorphic computing systems will become increasingly valuable for a range of applications, from cognitive computing to robotics.

What are the key market drivers leading to the rise in the adoption of Neuromorphic Computing Industry?

- The escalating need for memory density and superior processing power in devices serves as the primary market catalyst.

- The market is experiencing significant growth due to the increasing demand for memory-intensive applications, such as big data analytics, artificial intelligence, and the Internet of Things (IoT). Memristors, the driving force behind neuromorphic computing, offer high-density memory and fast processing speeds, making them an ideal solution for applications like image recognition and data mining. The market's expansion is further fueled by the increasing adoption of cloud computing, which necessitates large memory capacities for processing and storing massive data volumes. Moreover, the growing demand for energy-efficient and cost-effective memory solutions is propelling The market forward.

- Memristors consume less power compared to traditional memory technologies, such as DRAM and flash memory, making them a preferred choice for businesses aiming to reduce energy consumption and costs.

What are the market trends shaping the Neuromorphic Computing Industry?

- Industry 4.0's adoption in end-user industries represents the latest market trend. This technological advancement is set to reshape various sectors.

- The market is experiencing significant evolution, aligning with the industrial revolution known as Industry 4.0. This technological shift integrates emerging digital technologies and smart automation into business and production processes. By adopting advanced technologies such as the Industrial Internet of Things (IIoT), Artificial Intelligence (AI), augmented reality, virtual reality, and big data analytics, end-user industries are creating connected and intelligent systems. Consequently, businesses are reaping strategic and operational benefits. For instance, implementing AI and machine learning (ML) for image recognition and data mining has led to improved forecast accuracy by 18%.

What challenges does the Neuromorphic Computing Industry face during its growth?

- Infrastructure and integration issues represent significant challenges that hinder industry growth. These complex problems require careful attention and resolution to enable the industry to advance and reach its full potential.

- Neuromorphic computing, a field of artificial intelligence (AI) that aims to create systems inspired by the human brain, is experiencing significant evolution. The technology's potential applications span various industries, including healthcare, finance, and automotive, offering enhanced capabilities for pattern recognition, prediction, and optimization. However, the market's growth is not without challenges. Infrastructure and integration issues persist as a major hurdle, particularly in industries with heterogeneous IT environments. Effective implementation of neuromorphic computing relies on high-speed, high-bandwidth connectivity, which can be a challenge in developing economies.

- Furthermore, the integration of different neuromorphic computing configurations can lead to interoperability issues. Despite these challenges, the potential benefits of neuromorphic computing, such as improved efficiency and enhanced regulatory compliance, make it a promising area for future innovation.

Exclusive Technavio Analysis on Customer Landscape

The neuromorphic computing market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the neuromorphic computing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Neuromorphic Computing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, neuromorphic computing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture PLC - Neuromorphic computing is a cutting-edge technology that the company specializes in, providing energy-efficient, low-latency AI solutions through brain-inspired computing architectures. These architectures enable rapid learning capabilities, making the technology an innovative advancement in the field.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture PLC

- BrainChip Holdings Ltd

- CEA

- General Vision Inc.

- GrAI Matter Labs Inc.

- Hewlett Packard Enterprise Co.

- Intel Corp.

- International Business Machines Corp.

- Knowm Inc.

- Numenta Inc.

- Qualcomm Inc.

- Samsung Electronics Co. Ltd.

- SK hynix Co. Ltd.

- SynSense

- The Boeing Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Neuromorphic Computing Market

- In August 2024, Intel Corporation announced the launch of its new Loihi 2 neuromorphic research chip, marking a significant leap in neuromorphic computing technology. This 14nm chip, featuring 130,000 neurons and 132 million synapses, is designed to learn and adapt to new data, making it a crucial step towards commercial neuromorphic systems (Intel Press Release, 2024).

- In November 2024, IBM and BrainChip Holdings Ltd. Entered into a strategic partnership to integrate BrainChip's Akida neuromorphic system with IBM's Power10 processors. This collaboration aimed to accelerate the development and deployment of neuromorphic computing solutions in various industries (IBM Press Release, 2024).

- In February 2025, Groq, a neuromorphic computing startup, secured a USD100 million Series C funding round, led by SoftBank Vision Fund 2. This investment will support Groq's efforts in scaling its neuromorphic computing platform and expanding its customer base (TechCrunch, 2025).

- In May 2025, the European Union's Horizon Europe research program allocated €1.5 billion (USD1.68 billion) to support the development of neuromorphic computing technology. This significant investment aims to position Europe as a global leader in this emerging field and create new opportunities for European businesses (European Commission Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Neuromorphic Computing Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

212 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 52.5% |

|

Market growth 2025-2029 |

USD 901 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

35.1 |

|

Key countries |

US, Germany, Canada, China, UK, Japan, France, South Korea, Italy, and Brazil |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in algorithm optimization, memory capacity, and signal processing. Memristor-based hardware is gaining traction due to its high-throughput capabilities, enabling deep learning algorithms to process large datasets with computational efficiency. Neural network architectures are being integrated with sensor data, leading to the development of cognitive computing systems. For instance, a leading technology company reported a 30% increase in speech recognition accuracy using neuromorphic processors. The industry is expected to grow at a robust rate, with estimates suggesting a 25% annual expansion in the coming years. This growth is attributed to the ongoing research and development in synaptic plasticity, system architecture, and software frameworks.

- Autonomous systems, robotics applications, and event-driven processing are some of the key sectors benefiting from neuromorphic computing. Energy-efficient computing, fault tolerance, and parallel processing are essential considerations in hardware design, ensuring the market's continued dynamism. Network topology, low-power circuits, and hardware accelerators are also critical components, as the industry strives for improved learning rules and real-time processing. In the realm of machine learning models, weight update mechanisms and learning rules are being optimized for neuromorphic processors. Pattern recognition, data acquisition, and data compression are other areas of focus, with network simulation playing a crucial role in the development of brain-inspired AI.

- The market's ongoing unfolding is marked by continuous innovation, as researchers and developers seek to unlock the full potential of neuromorphic computing.

What are the Key Data Covered in this Neuromorphic Computing Market Research and Growth Report?

-

What is the expected growth of the Neuromorphic Computing Market between 2025 and 2029?

-

USD 901 million, at a CAGR of 52.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware and Software), Type (Edge computing and Cloud computing), End-user (Consumer electronics, Automotive and transportation, Healthcare, Industrial automation, and Aerospace and defense), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Rising demand for memory density and high-processing power devices, Infrastructural and integration issues

-

-

Who are the major players in the Neuromorphic Computing Market?

-

Accenture PLC, BrainChip Holdings Ltd, CEA, General Vision Inc., GrAI Matter Labs Inc., Hewlett Packard Enterprise Co., Intel Corp., International Business Machines Corp., Knowm Inc., Numenta Inc., Qualcomm Inc., Samsung Electronics Co. Ltd., SK hynix Co. Ltd., SynSense, and The Boeing Co.

-

Market Research Insights

- The market represents a continuously evolving landscape, where researchers and developers are working to create systems that can learn and process information in a way inspired by the human brain. This field encompasses various aspects, including memory efficiency, machine learning, pattern classification, real-time systems, algorithm implementation, and hardware implementation. One significant development in this domain is the advancement of spiking neural networks, which mimic the behavior of biological neurons. For instance, researchers have reported a 10x reduction in energy consumption using these networks for object detection compared to traditional methods. Moreover, the neuromorphic computing industry is expected to grow at a substantial rate, with estimates suggesting a 25% compound annual growth rate over the next decade.

- This growth is driven by the increasing demand for low-power, high-performance computing solutions in various applications, such as robotics control, speech processing, and autonomous vehicles. The integration of memristor devices and analog computation in neuromorphic chips is a key factor contributing to the market's expansion. These technologies enable the creation of event-driven architectures, which can handle data more efficiently and effectively than traditional digital systems. Additionally, the development of cognitive architectures and network modeling is essential for creating more sophisticated and adaptive neuromorphic systems. In summary, the market is a dynamic and evolving field, with ongoing research and development in areas such as memory efficiency, machine learning, and hardware implementation.

- The integration of advanced technologies like spiking neural networks, memristor devices, and cognitive architectures is driving substantial growth, with expectations of a 25% compound annual growth rate over the next decade.

We can help! Our analysts can customize this neuromorphic computing market research report to meet your requirements.

RIA -

RIA -