AI In Industrial Machinery Market Size 2025-2029

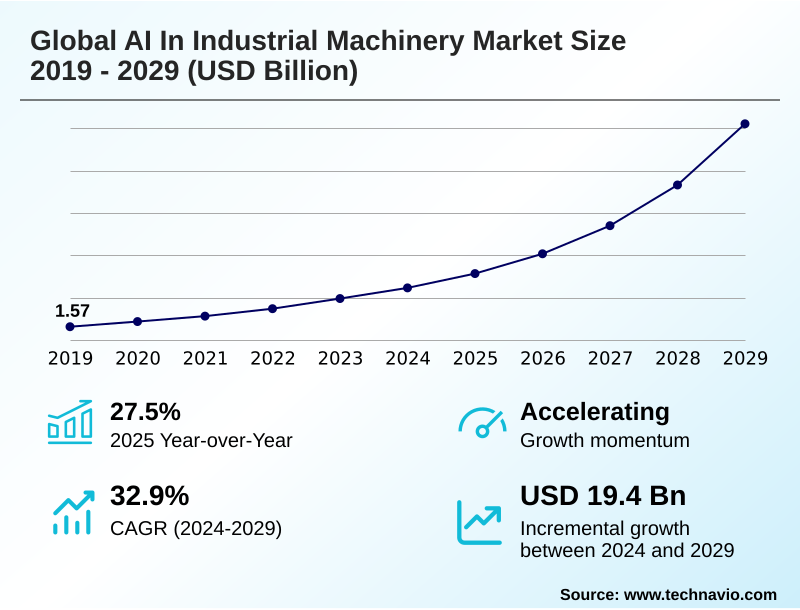

The ai in industrial machinery market size is valued to increase by USD 19.40 billion, at a CAGR of 32.9% from 2024 to 2029. Imperative for enhanced operational efficiency and predictive maintenance will drive the ai in industrial machinery market.

Major Market Trends & Insights

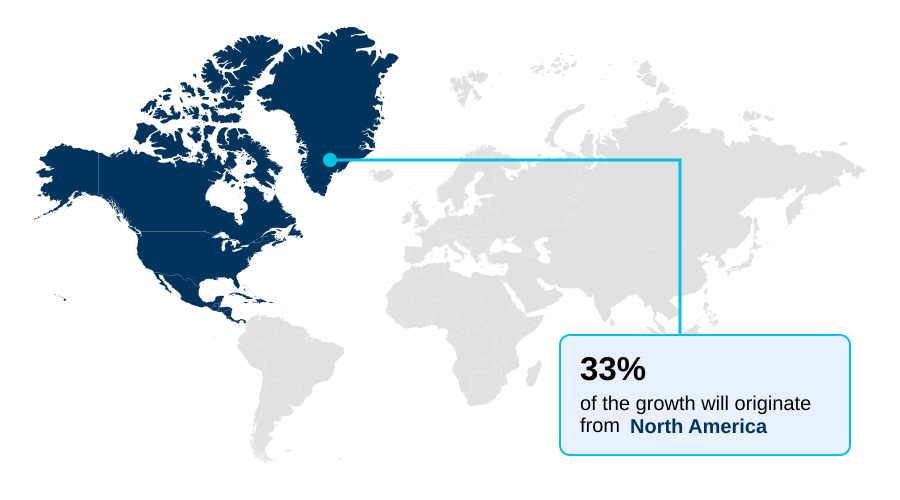

- North America dominated the market and accounted for a 33.1% growth during the forecast period.

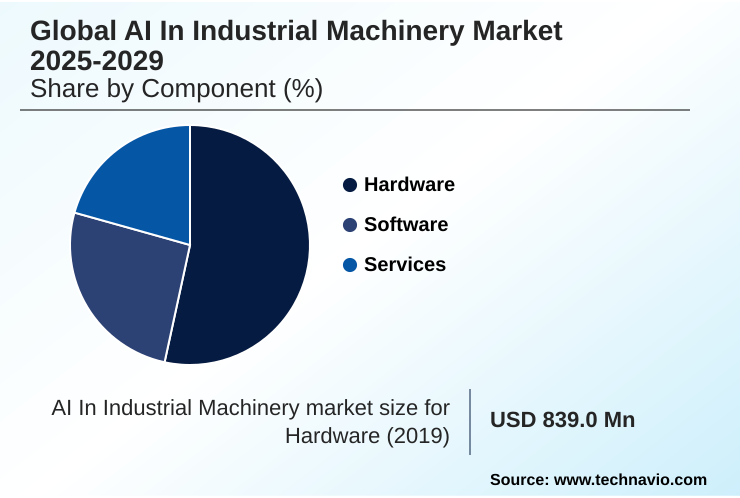

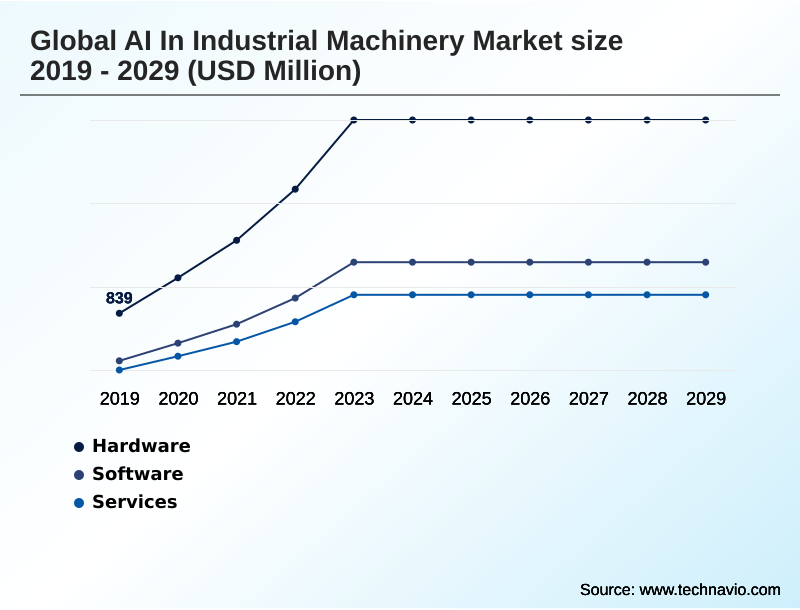

- By Component - Hardware segment was valued at USD 2.59 billion in 2023

- By Technology - Machine learning segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 23.98 billion

- Market Future Opportunities: USD 19.40 billion

- CAGR from 2024 to 2029 : 32.9%

Market Summary

- The AI in industrial machinery market is defined by the integration of intelligent systems to drive operational excellence and automation. This involves leveraging technologies like machine learning models and computer vision inspection to transform raw industrial internet of things (IIoT) data into actionable insights for real-time process optimization.

- A key application is condition-based maintenance, where predictive maintenance algorithms analyze sensor data to forecast equipment failures, minimizing costly downtime. For instance, a smart factory ecosystem can utilize AI-driven automation to dynamically adjust production schedules in response to an unexpected supply chain disruption, rerouting materials and reallocating AI-powered robotics to maintain output.

- This advanced human-machine interaction, powered by on-device computation and augmented worker capabilities, is crucial for building resilient and efficient manufacturing operations. The market is also seeing the rise of generative AI design and industrial copilots, which accelerate development cycles and enhance human-machine collaboration.

- As data integration for AI models becomes more streamlined through unified platforms, the potential for autonomous process control and more sophisticated big data analytics continues to expand, making AI an indispensable tool for modern industry.

What will be the Size of the AI In Industrial Machinery Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI In Industrial Machinery Market Segmented?

The ai in industrial machinery industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Hardware

- Software

- Services

- Technology

- Machine learning

- Computer vision

- Context awareness

- Natural language processing

- End-user

- Automotive

- Semiconductor

- Oil and gas

- Food processing

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The hardware segment is foundational to the global AI in industrial machinery market, enabling advanced on-device computation and real-time data analysis.

This domain is shifting toward edge AI processing, which utilizes specialized hardware like neural processing units to run complex predictive maintenance algorithms directly on machinery, reducing latency.

The development of sophisticated AI-enabled sensors is critical for capturing high-fidelity operational technology (OT) data. This allows for more accurate computer vision inspection systems, which have demonstrated the ability to improve defect detection accuracy by more than 15%.

This move to decentralized intelligence is a key enabler for creating a responsive smart factory ecosystem and supports AI for factory automation, enhancing both efficiency and safety through improved human-machine collaboration.

The Hardware segment was valued at USD 2.59 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Industrial Machinery Market Demand is Rising in North America Get Free Sample

The geographic landscape of the global AI in industrial machinery market is led by North America, which accounts for over 33% of the market opportunity, driven by early adoption in the US and Canada.

The region's focus on smart manufacturing AI solutions is bolstered by a strong technology infrastructure. Europe, another key region, is heavily influenced by Industrie 4.0 initiatives, promoting AI and robotics integration.

Meanwhile, APAC is the fastest-growing region, with countries like China and Japan advancing AI for factory automation to address rising labor costs and enhance production quality.

The use of autonomous industrial vehicles and AI in heavy machinery is particularly prominent in Australia's mining sector. Across these regions, the strategic deployment of big data analytics and AI-based asset management is critical for maintaining a competitive edge.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises evaluating the global AI in industrial machinery market are focused on quantifiable outcomes and strategic implementation. A critical question is how AI reduces industrial downtime, with many firms turning to AI solutions for labor shortages. The decision between edge AI versus cloud AI is pivotal, as it impacts latency, security, and cost.

- When firms implement AI predictive maintenance, they often see a greater than 20% improvement in equipment uptime compared to traditional methods. The role of AI in digital twins is expanding, allowing for complex simulations that de-risk new processes. A primary driver is optimizing industrial processes with AI, where AI computer vision for quality becomes essential.

- However, the ROI calculation for industrial AI remains a significant hurdle, as does integrating AI with legacy systems. Cybersecurity risks of industrial AI are also a major concern for boardroom-level discussions. Success hinges on understanding machine learning for asset performance and the specific data requirements for industrial AI.

- Furthermore, natural language processing industrial use is growing, particularly with generative AI for PLC programming. This is compelling a focus on training workforce for AI collaboration and leveraging AI-driven automation in logistics to improve overall equipment effectiveness (OEE). Firms using AI for energy consumption reduction are also finding significant operational savings, underscoring the technology's broad impact.

What are the key market drivers leading to the rise in the adoption of AI In Industrial Machinery Industry?

- The imperative to enhance operational efficiency and implement predictive maintenance strategies is a key driver for market growth.

- The primary driver for the global AI in industrial machinery market is the relentless pursuit of operational efficiency with AI.

- Predictive maintenance, a key application, has been shown to reduce unplanned machinery downtime by up to 40% and cut maintenance costs by 25%.

- The proliferation of the industrial internet of things (IIoT) serves as a fundamental catalyst, generating vast amounts of data that fuel machine learning models for real-time process optimization. This symbiotic relationship is enabling smarter, self-optimizing industrial ecosystems.

- Furthermore, the persistent global shortage of skilled labor is accelerating the adoption of AI-powered robotics and autonomous systems, which augment worker capabilities and automate hazardous tasks.

- The focus on AI for worker safety is a significant benefit, creating more resilient and sustainable industrial operations.

What are the market trends shaping the AI In Industrial Machinery Industry?

- The emergence of generative AI, manifested through industrial copilots, is a significant upcoming trend. This technology is fundamentally reshaping human-machine interaction within industrial settings.

- Key trends are reshaping the global AI in industrial machinery market, led by the emergence of generative AI design and industrial copilots. These AI assistants, integrated into engineering platforms, can reduce complex PLC code generation time by over 50%.

- Another dominant trend is the shift toward edge computing in industry, which enables real-time data analysis and lowers latency for critical tasks. This decentralized approach is essential for AI-driven quality control and is being adopted by over 60% of new smart factory initiatives. The integration of AI with digital twin for manufacturing creates sophisticated virtual models for simulation and optimization.

- This convergence of cyber-physical systems with AI-powered supply chain management allows for predictive modeling that enhances operational resilience and efficiency, forming a cornerstone of modern industrial strategy.

What challenges does the AI In Industrial Machinery Industry face during its growth?

- The high initial investment coupled with uncertain return on investment poses a significant challenge to industry growth.

- Significant challenges constrain the growth of the global AI in industrial machinery market, primarily the high initial investment and uncertain ROI for industrial AI. The total cost of ownership, including hardware, software, and integration services, can be substantial, with deployment costs often exceeding initial software licensing fees by a factor of three. Another major hurdle is data integration complexity.

- Integrating siloed operational technology (OT) data with IT systems is a resource-intensive task, and poor data quality can compromise the performance of machine learning models. Cybersecurity for industrial AI remains a critical concern, as connected systems expand the attack surface, making them vulnerable to disruptions that could halt production.

- Finally, the scarcity of skilled talent, with a 2-to-1 demand-to-supply ratio for data scientists with industrial expertise, makes it difficult to implement and manage AI initiatives.

Exclusive Technavio Analysis on Customer Landscape

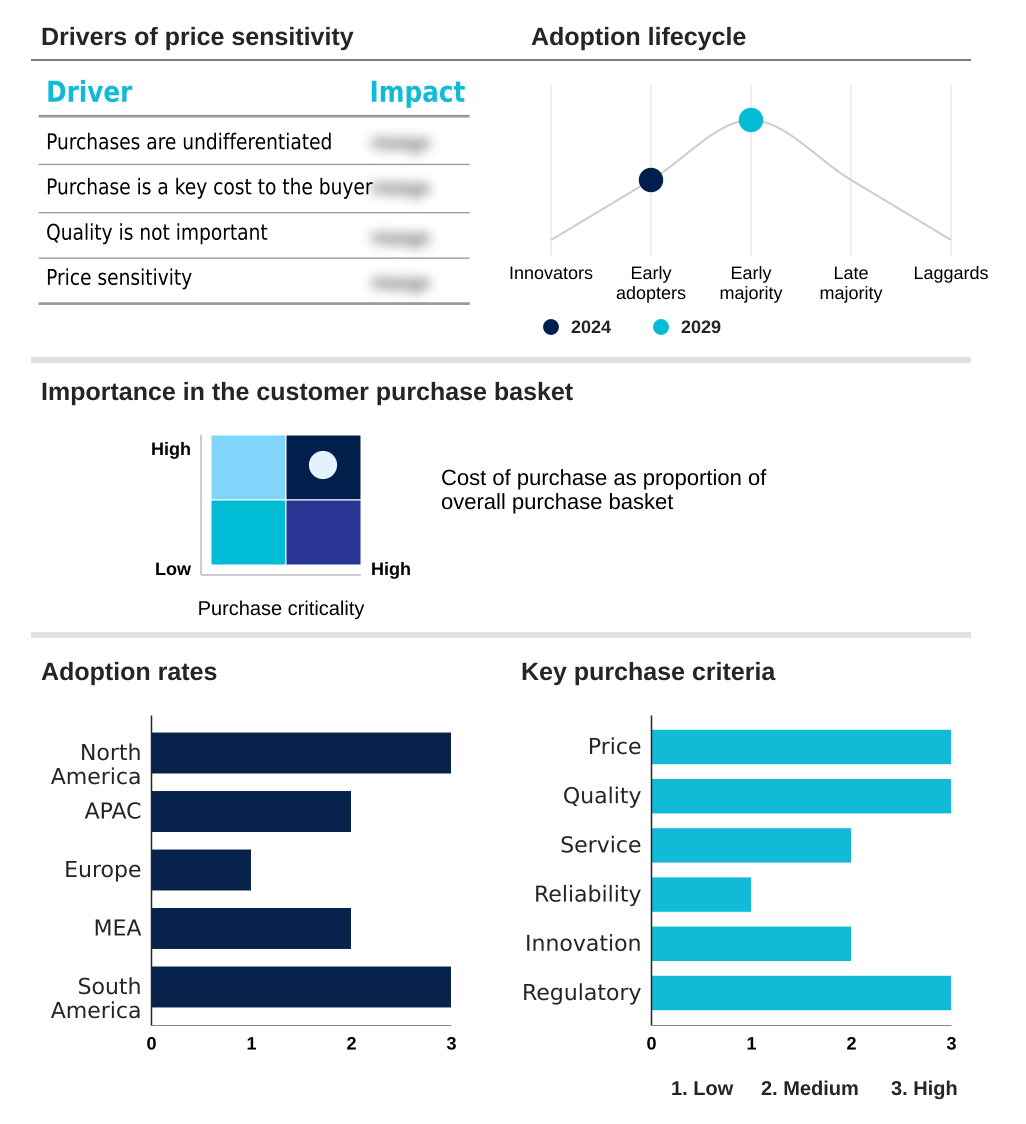

The ai in industrial machinery market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in industrial machinery market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Industrial Machinery Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in industrial machinery market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABB Ltd. - Analyzes integration of generative AI assistants for factory automation and AI-driven robotics for streamlined warehouse logistics.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- AVEVA Group Plc

- Bentley Systems Inc.

- Robert Bosch GmbH

- C3.ai Inc.

- Caterpillar Inc.

- Emerson Electric Co.

- FANUC Corp.

- General Electric Co.

- Hitachi Ltd.

- Honeywell International Inc.

- IBM Corp.

- KUKA AG

- Microsoft Corp.

- Mitsubishi Electric Corp.

- NVIDIA Corp.

- Oracle Corp.

- Rockwell Automation Inc.

- SAP SE

- Siemens AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in industrial machinery market

- In October 2024, Honeywell launched its AI-enabled Experion Operations Assistant, a new software solution designed to provide proactive insights to plant operators to improve decision-making and accelerate the move toward autonomous operations.

- In November 2024, Siemens announced the expansion of its Industrial Copilot, a generative AI assistant, to support maintenance teams by translating complex machine error codes into plain language and providing step-by-step repair guidance.

- In January 2025, Oracle introduced new generative AI agents for its Fusion Cloud Supply Chain and Manufacturing (SCM) suite, designed to automate routine tasks and provide data-driven insights for improved supply chain efficiency.

- In February 2025, Intel began the rollout of its next-generation Xeon processors with built-in AI acceleration, specifically engineered to power enterprise-grade AI applications at the industrial edge.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Industrial Machinery Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 339 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 32.9% |

| Market growth 2025-2029 | USD 19395.2 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 27.5% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI in industrial machinery market is advancing through the convergence of sophisticated software and intelligent hardware. The proliferation of the industrial internet of things (IIoT) provides the data foundation for powerful machine learning models and predictive maintenance algorithms, which are becoming standard for achieving operational excellence.

- Technologies such as computer vision inspection and natural language processing (NLP) are enabling new levels of AI-driven automation and enhanced human-machine interaction.

- The strategic integration of AI-integrated digital twins with photorealistic simulation is a critical development, impacting boardroom decisions on capital expenditure by allowing for virtual commissioning and process optimization, which has been shown to reduce project validation times by over 40%.

- The shift toward on-device computation, powered by advanced neural processing units and AI-enabled sensors, facilitates real-time data analysis and autonomous process control. This evolution is fostering a smart factory ecosystem where conversational interfaces and industrial copilots support augmented worker capabilities, moving the industry toward more resilient and efficient cyber-physical systems and data-driven automation.

What are the Key Data Covered in this AI In Industrial Machinery Market Research and Growth Report?

-

What is the expected growth of the AI In Industrial Machinery Market between 2025 and 2029?

-

USD 19.40 billion, at a CAGR of 32.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, Services), Technology (Machine learning, Computer vision, Context awareness, Natural language processing), End-user (Automotive, Semiconductor, Oil and gas, Food processing, Others) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Imperative for enhanced operational efficiency and predictive maintenance, High initial investment and uncertain return on investment

-

-

Who are the major players in the AI In Industrial Machinery Market?

-

ABB Ltd., AVEVA Group Plc, Bentley Systems Inc., Robert Bosch GmbH, C3.ai Inc., Caterpillar Inc., Emerson Electric Co., FANUC Corp., General Electric Co., Hitachi Ltd., Honeywell International Inc., IBM Corp., KUKA AG, Microsoft Corp., Mitsubishi Electric Corp., NVIDIA Corp., Oracle Corp., Rockwell Automation Inc., SAP SE and Siemens AG

-

Market Research Insights

- The dynamics of the AI in industrial machinery market are increasingly shaped by the pursuit of tangible business outcomes. The implementation of AI for worker safety has been shown to reduce workplace incidents by over 30% in high-risk environments.

- Meanwhile, ROI for industrial AI is becoming clearer, with firms deploying predictive analytics for machinery reporting up to a 25% reduction in unplanned downtime. These gains are driving adoption, but successful AI and robotics integration hinges on robust data integration for AI models and a strategic approach to AI workforce upskilling.

- The trend toward human-machine collaboration is central, empowering employees with tools that augment their skills rather than replace them. This creates a more resilient and efficient operational framework, justifying the investment in smart manufacturing AI solutions.

We can help! Our analysts can customize this ai in industrial machinery market research report to meet your requirements.

RIA -

RIA -