AI In Supply Chain Optimization Market Size 2025-2029

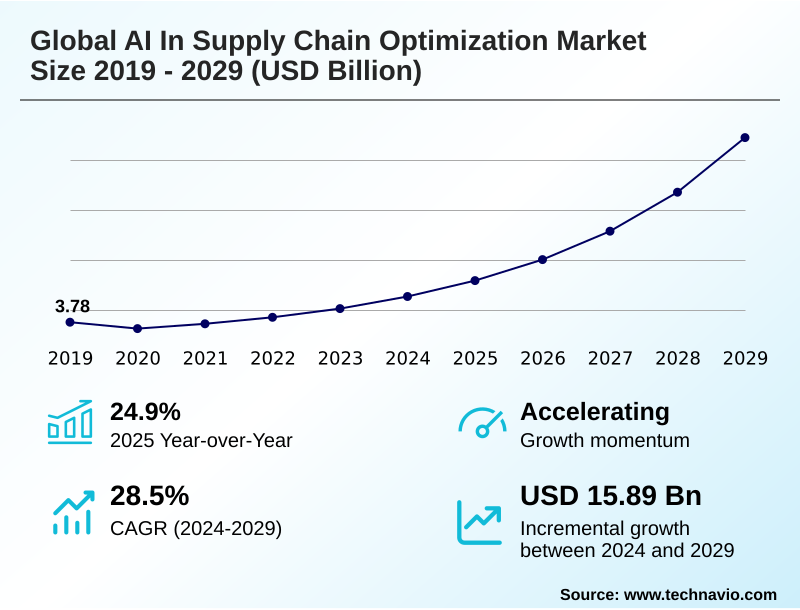

The ai in supply chain optimization market size is valued to increase by USD 15.89 billion, at a CAGR of 28.5% from 2024 to 2029. Increasing demand for enhanced supply chain visibility and agility will drive the ai in supply chain optimization market.

Major Market Trends & Insights

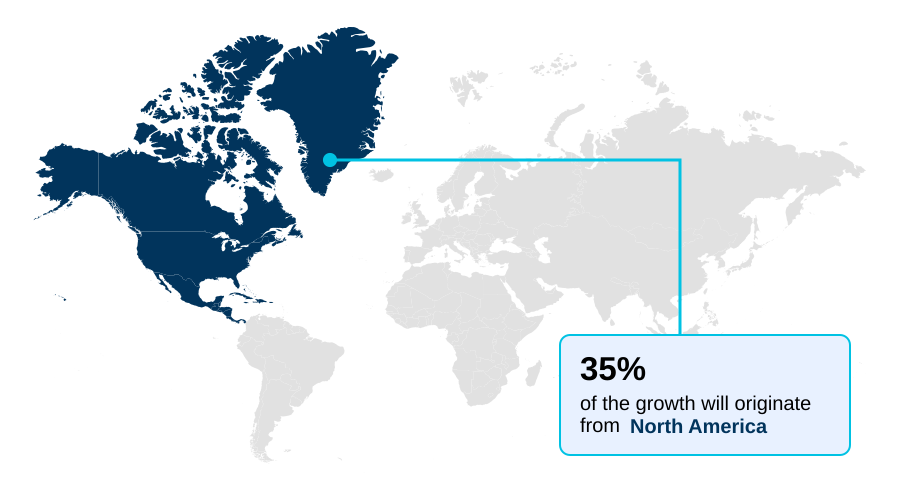

- North America dominated the market and accounted for a 34.6% growth during the forecast period.

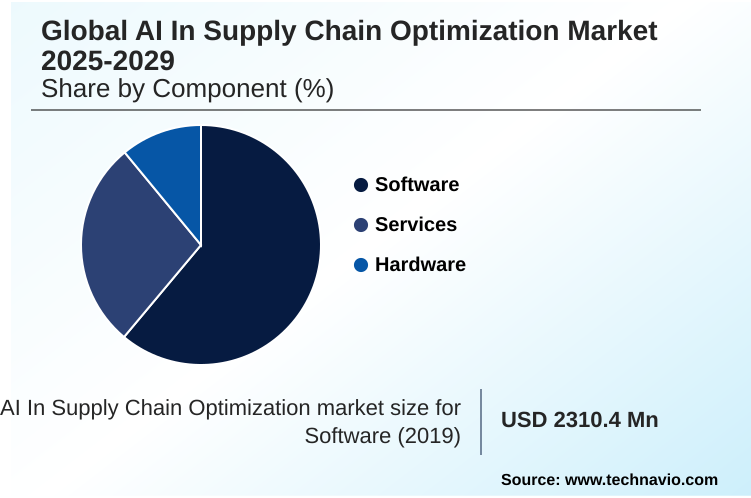

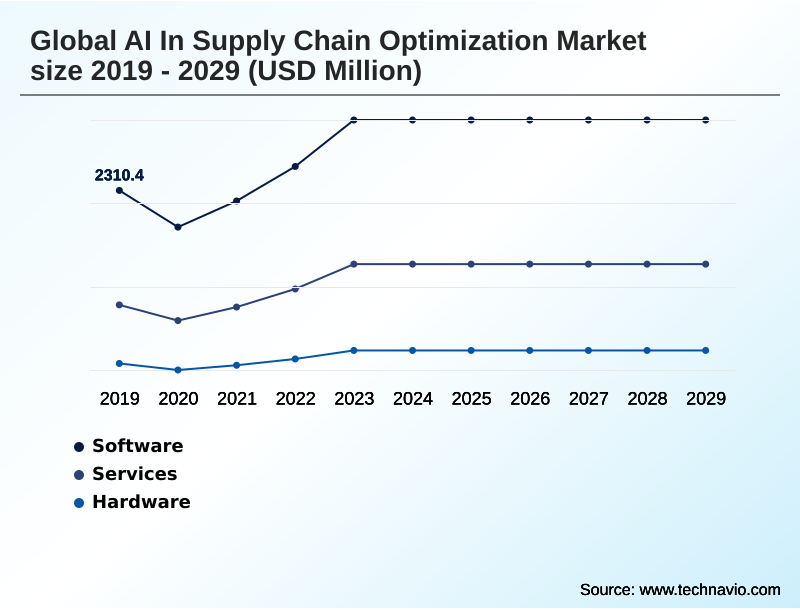

- By Component - Software segment was valued at USD 3.08 billion in 2023

- By Technology - Machine learning segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 18.46 billion

- Market Future Opportunities: USD 15.89 billion

- CAGR from 2024 to 2029 : 28.5%

Market Summary

- The AI in supply chain optimization market is defined by the strategic application of advanced computational technologies to enhance operational efficiency and resilience. Key drivers include the pressing need for greater supply chain visibility and agility in navigating global disruptions, alongside the imperative to reduce operational costs.

- AI-powered forecasting models and machine learning models are central to this transformation, enabling more accurate demand forecasting and predictive maintenance scheduling. For example, a manufacturer can utilize real-time data analytics from IoT sensor data integration to anticipate equipment failures, scheduling maintenance proactively to avoid costly production stoppages.

- However, significant challenges persist, including complexities in data quality, integration with legacy systems, and a pervasive shortage of specialized talent. Trends such as the rise of AI-powered digital twins and generative AI for creating supply chain network designs are shaping the future, offering unprecedented levels of end-to-end supply chain visibility and proactive risk mitigation.

- These intelligent workflow automation tools are moving organizations from reactive problem-solving to a state of autonomous planning and dynamic operational control.

What will be the Size of the AI In Supply Chain Optimization Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI In Supply Chain Optimization Market Segmented?

The ai in supply chain optimization industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Software

- Services

- Hardware

- Technology

- Machine learning

- Computer vision

- NLP

- Others

- End-user

- Retail and e-commerce

- Manufacturing

- Automotive

- Healthcare

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is fundamental to the AI in supply chain optimization market, providing the intelligence for data-driven decision making. These AI-powered logistics platforms are vital for addressing operational challenges, from predictive demand planning to logistics network optimization.

Innovations in machine learning models are producing more sophisticated tools, enabling AI-powered forecasting models to analyze historical sales data alongside market trends for enhanced demand forecasting accuracy.

For instance, some AI-driven fleet management solutions have demonstrated the ability to reduce millions of miles in delivery routes through dynamic route optimization.

The adoption of AI for inventory control and intelligent workflow automation allows businesses to maintain optimal stock levels, which is crucial for minimizing carrying costs and preventing stockouts, showcasing the power of prescriptive analytics recommendations.

The Software segment was valued at USD 3.08 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Supply Chain Optimization Market Demand is Rising in North America Request Free Sample

The geographic landscape of the market is characterized by varied adoption rates and strategic priorities.

North America currently accounts for the largest market share at over 34%, driven by mature technology infrastructure and a focus on AI-driven supplier collaboration and last-mile delivery optimization.

In Europe, the emphasis is on sustainability and efficiency, with initiatives like carbon footprint modeling and circular economy initiatives gaining traction.

Ports in the region have seen vessel turnaround times fall by over 20% after implementing AI-powered logistics platforms for intelligent route planning and operations management.

Meanwhile, the APAC region is the fastest-growing market, leveraging smart factory AI integration and real-time data analytics to manage its vast manufacturing and logistics hubs.

AI in production planning and AI for returns management are key applications driving growth and efficiency gains across these diverse regions.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Achieving superior performance in the AI in supply chain optimization market requires moving beyond generic applications to address specific operational pain points. A key focus is using AI to reduce the bullwhip effect, where advanced algorithms for route optimization and more accurate forecasting stabilize inventory levels across tiers.

- For instance, AI-based demand forecasting for retail has shown it can improve accuracy from 70% with traditional methods to over 90%, directly enabling AI-powered inventory stock level optimization. Another critical area is generative AI for supplier onboarding automation, which streamlines validation processes.

- Companies are also building autonomous and self-correcting supply chains by integrating AI with legacy ERP systems, a complex but highly valuable endeavor. This involves leveraging natural language processing for shipping documents to accelerate data extraction and reduce errors. Furthermore, firms are utilizing digital twin simulations for cost reduction and AI-powered risk modeling for supply chains to test resilience.

- AI-powered tools for supply chain resilience and AI for managing volatile material supplies are becoming standard for proactive management. The scope extends to using AI for carbon footprint modeling, improving last-mile delivery efficiency with AI, and AI-driven quality inspection in manufacturing.

- Even warehousing is being transformed by optimizing warehouse layouts with generative AI and implementing AI for predictive maintenance in logistics, all tracked via real-time tracking with AI platforms.

What are the key market drivers leading to the rise in the adoption of AI In Supply Chain Optimization Industry?

- The increasing demand for enhanced supply chain visibility and agility stands as a key driver for market growth.

- Market growth is significantly driven by the imperative for reducing operational expenditures and the rapid evolution of AI technologies.

- AI algorithms are instrumental in optimizing transportation routes in real time by analyzing variables like traffic, weather, and fuel costs, leading to substantial fuel savings and enhanced efficiency.

- Some companies have saved up to 10,000 hours of manual work annually by deploying AI-powered platforms. In warehouse automation systems, AI-powered robots handle picking and sorting with greater speed and accuracy, directly cutting labor costs and error rates.

- The convergence of powerful machine learning models and rich data sources from IoT sensor data integration creates a virtuous cycle, where more data improves AI for logistics optimization and demand forecasting AI tools.

- This dynamic is a powerful catalyst, driving further AI for resource allocation and procurement automation with AI to gain a competitive edge.

What are the market trends shaping the AI In Supply Chain Optimization Industry?

- The proliferation of generative AI in supply chain operations is emerging as a significant market trend. This technology is enabling more proactive and creative approaches to logistics and operational problem-solving.

- Key market trends are centered on leveraging advanced AI for proactive and intelligent operations. The adoption of AI-powered digital twins provides a dynamic, virtual replica of physical assets, allowing for comprehensive end-to-end supply chain visibility and data-driven decision making. The use of a digital twin for supply chain can lead to significant savings by simulating various sourcing and transport strategies.

- Another major trend is the use of predictive analytics for disruptions, where AI-driven platforms analyze millions of data points to flag potential risks, from geopolitical instability to natural disasters, before they escalate. This proactive approach is critical for improving supply chain resilience.

- Furthermore, the proliferation of generative AI in operations is reshaping core functions by creating novel content, such as optimized supply chain network designs, and automating sophisticated decision-making, which is particularly useful for AI-based risk modeling and AI-driven procurement.

What challenges does the AI In Supply Chain Optimization Industry face during its growth?

- Complexities related to data quality, integration, and security present a key challenge affecting industry growth.

- Significant challenges hinder the widespread adoption of AI, primarily stemming from data and talent issues. The pervasive talent shortage, with 66% of executives rating their teams' AI proficiency as medium to low, creates a major bottleneck in implementation.

- This pervasive talent shortage and workforce skills gap necessitates aggressive reskilling, with high-performing firms being three times more likely to retrain over 30% of their workforce due to AI adoption.

- Concurrently, data quality, integration, and security complexities are a primary cause of failure, with some research attributing up to 73% of unsuccessful AI projects to incomplete data visibility rather than flawed algorithms.

- The challenge of data integration for AI is compounded by the difficulty of merging legacy systems with modern AI-powered logistics platforms, which obstructs efforts in AI-driven supplier collaboration and creating intelligent fleet management systems.

Exclusive Technavio Analysis on Customer Landscape

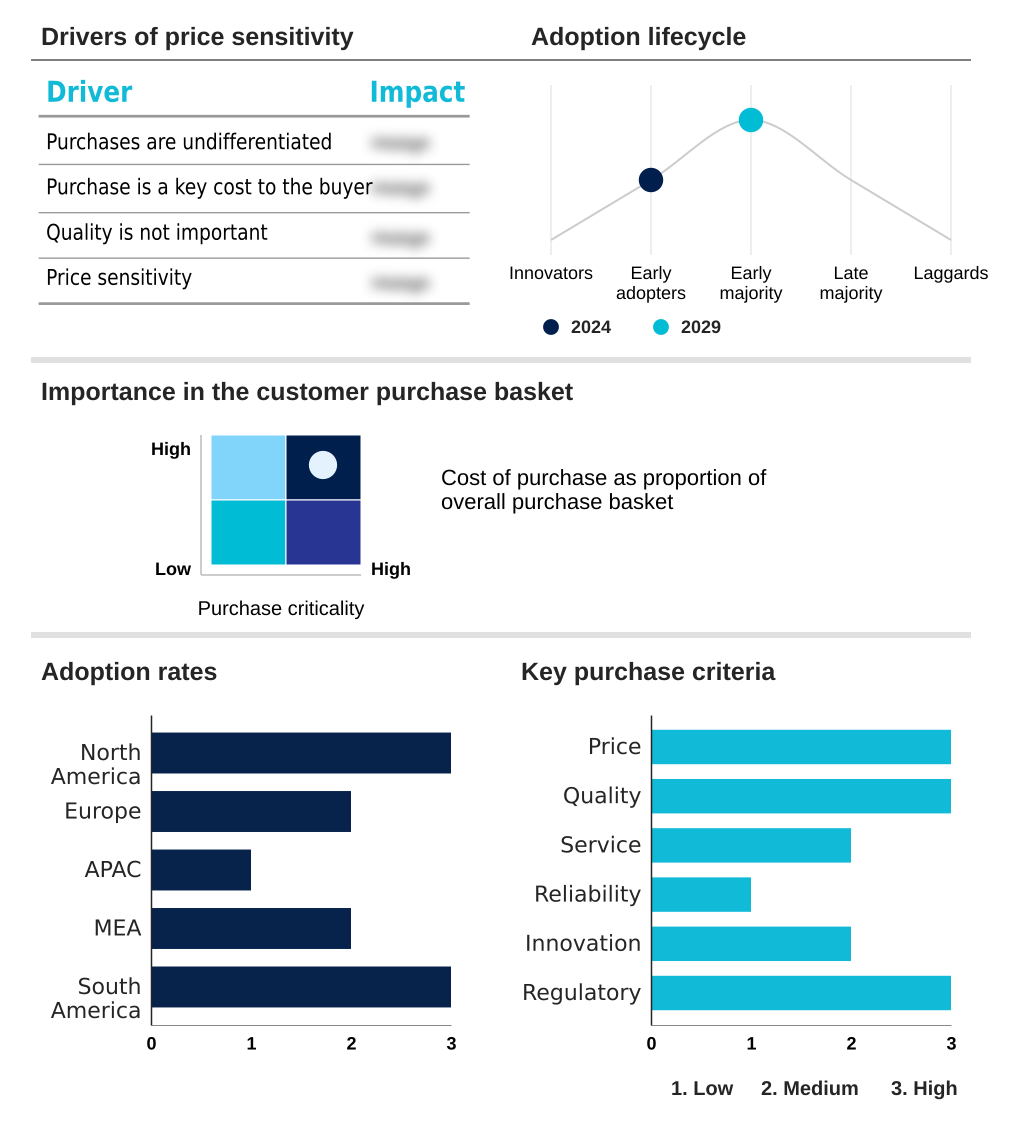

The ai in supply chain optimization market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in supply chain optimization market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Supply Chain Optimization Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in supply chain optimization market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Amazon Web Services Inc. - Offers a cloud infrastructure platform leveraging machine learning services to automate procurement, logistics planning, and invoice processing for enhanced supply chain optimization.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Amazon Web Services Inc.

- Blue Yonder Group Inc.

- Celonis SE

- Coupa Software Inc.

- Descartes Systems Group Inc.

- Fourkites Inc.

- Google LLC

- Honeywell International Inc.

- Infor Inc.

- IBM Corp.

- Kinaxis Inc.

- Manhattan Associates Inc.

- Microsoft Corp.

- Oracle Corp.

- PTC Inc.

- SAP SE

- Zebra Technologies Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in supply chain optimization market

- In August 2025, United Parcel Service announced the launch of an AI-driven predictive maintenance system for its trucking fleet, designed to minimize vehicle downtime and reduce operational expenditures.

- In September 2025, FedEx implemented an AI-powered route optimization solution across its North American operations, leading to tangible reductions in delivery times and fuel consumption.

- In September 2025, IBM Japan launched its Supply Chain Ensemble, an AI-powered solution that leverages the Watsonx platform to analyze data from sales, demand, production, procurement, and logistics.

- In September 2025, Avetta announced an expansion of its AI-powered capabilities, including a generative AI risk assistant that provides instant, context-aware answers to compliance and safety questions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Supply Chain Optimization Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 309 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 28.5% |

| Market growth 2025-2029 | USD 15885.1 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 24.9% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, India, Japan, Australia, South Korea, Indonesia, UAE, Saudi Arabia, South Africa, Turkey, Israel, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI in supply chain optimization market is fundamentally reshaping enterprise operations by embedding intelligence into core processes. The adoption of technologies like machine learning models and computer vision systems is enabling unprecedented levels of warehouse automation systems and automated sorting systems. This shift facilitates proactive risk mitigation and dynamic route optimization, moving beyond static planning.

- A critical boardroom consideration is the impact of generative AI on operational strategy, particularly regarding workforce allocation optimization and the need for new skills in human-robot collaboration. The technology is enabling functions like automated data extraction, with some logistics firms processing orders six times faster. The integration of predictive maintenance scheduling and AI-powered forecasting models delivers tangible efficiency gains.

- Firms are creating cognitive supply chains through end-to-end supply chain visibility and real-time disruption response. This is achieved through AI-powered digital twins and logistics network optimization, all driven by real-time data analytics and autonomous planning capabilities. Ultimately, the focus is on creating resilient, agile, and cost-effective supply networks.

What are the Key Data Covered in this AI In Supply Chain Optimization Market Research and Growth Report?

-

What is the expected growth of the AI In Supply Chain Optimization Market between 2025 and 2029?

-

USD 15.89 billion, at a CAGR of 28.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, Services, and Hardware), Technology (Machine learning, Computer vision, NLP, and Others), End-user (Retail and e-commerce, Manufacturing, Automotive, Healthcare, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for enhanced supply chain visibility and agility, Data quality, integration, and security complexities

-

-

Who are the major players in the AI In Supply Chain Optimization Market?

-

Amazon Web Services Inc., Blue Yonder Group Inc., Celonis SE, Coupa Software Inc., Descartes Systems Group Inc., Fourkites Inc., Google LLC, Honeywell International Inc., Infor Inc., IBM Corp., Kinaxis Inc., Manhattan Associates Inc., Microsoft Corp., Oracle Corp., PTC Inc., SAP SE and Zebra Technologies Corp.

-

Market Research Insights

- Market dynamics are increasingly shaped by the pursuit of tangible business outcomes through technology adoption. Organizations implementing predictive analytics for disruptions report up to 40% faster recovery times during crises compared to traditional methods. Similarly, the use of demand forecasting AI tools has led to improvements in forecasting accuracy of up to 87%, directly impacting inventory costs and service levels.

- The strategic focus on improving supply chain resilience and reducing operational expenditures is evident, with some AI-driven initiatives demonstrating a potential 20% reduction in logistics costs.

- This push for efficiency extends to workforce upskilling for AI, as companies recognize that realizing the full value of AI in warehouse management and procurement automation with AI depends on aligning human capital with new technological capabilities. The development of a supply chain control tower is also becoming a priority.

We can help! Our analysts can customize this ai in supply chain optimization market research report to meet your requirements.

RIA -

RIA -