Ai Inference Hardware Market Size and Growth Forecast 2026-2030

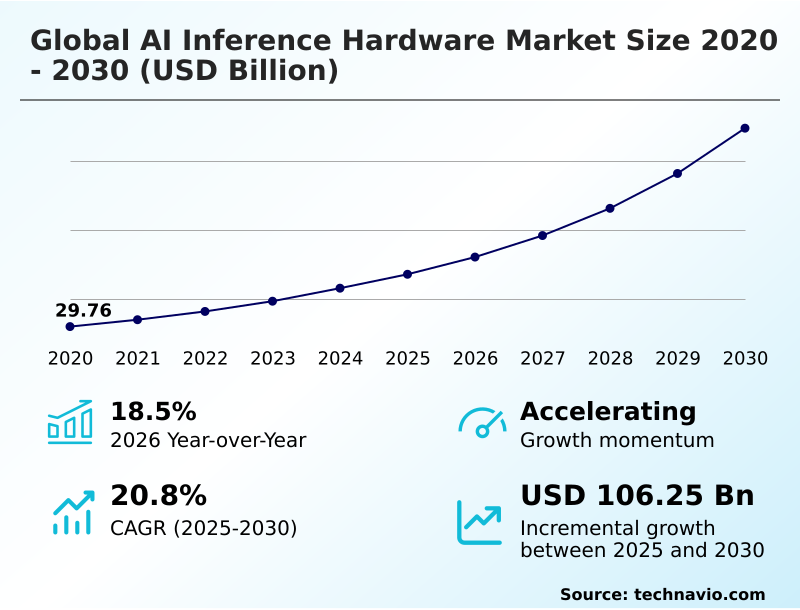

The Ai Inference Hardware Market size was valued at USD 67.80 billion in 2025 growing at a CAGR of 20.8% during the forecast period 2026-2030.

North America accounts for 39.8% of incremental growth during the forecast period. The GPU segment by Type was valued at USD 30.79 billion in 2024, while the Cloud inference segment holds the largest revenue share by Deployment.

The market is projected to grow by USD 144.29 billion from 2020 to 2030, with USD 106.25 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Ai Inference Hardware Market Overview

The AI inference hardware market is defined by the escalating need for specialized processors that can execute complex machine learning models with high efficiency and low latency. This demand is driven by the proliferation of applications requiring real-time data analysis, from industrial automation to autonomous systems. In a typical smart factory deployment, for instance, computer vision systems powered by edge AI processor designs are used for in-line quality inspection, where low-latency inference solutions are critical for identifying defects on a high-speed production line without causing bottlenecks. This shift toward localized processing is a global phenomenon, with North America contributing to nearly 39.8% of the market's incremental growth, largely due to investments by hyperscale data centers and technology leaders in custom silicon for AI. The development of power-efficient AI chips and advancements in AI hardware acceleration are crucial for supporting these deployments, enabling organizations to scale their AI capabilities from the cloud to the edge while managing operational costs and energy consumption.

Drivers, Trends, and Challenges in the Ai Inference Hardware Market

Strategic decisions regarding AI infrastructure are increasingly centered on balancing the total cost of AI inference hardware against performance and future-proofing against algorithmic shifts. For data center operators, evaluating the energy consumption of AI hardware is a critical step toward achieving compliance with energy management standards like ISO 50001 and developing sustainable AI computing hardware.

The choice between on-premises vs cloud AI inference often dictates the hardware selection process, where factors like the impact of the memory wall on AI and the need for AI hardware for real-time applications come into play.

A typical evaluation in a financial services firm might compare deploying Intel Gaudi for enterprise AI against a custom on-premises cluster using FPGA for low-latency AI tasks to process real-time transaction data.

This decision is complicated by challenges in AI hardware design, as the debate of NVIDIA vs AMD for AI inference is now broadened by the rise of specialized solutions. Companies are now exploring chiplet architectures for AI processors and the potential of silicon photonics in AI hardware to overcome performance bottlenecks.

Optimizing ASICs for neural networks remains a viable strategy for large-scale, static workloads, but it represents a significant upfront investment and risk if the underlying models evolve.

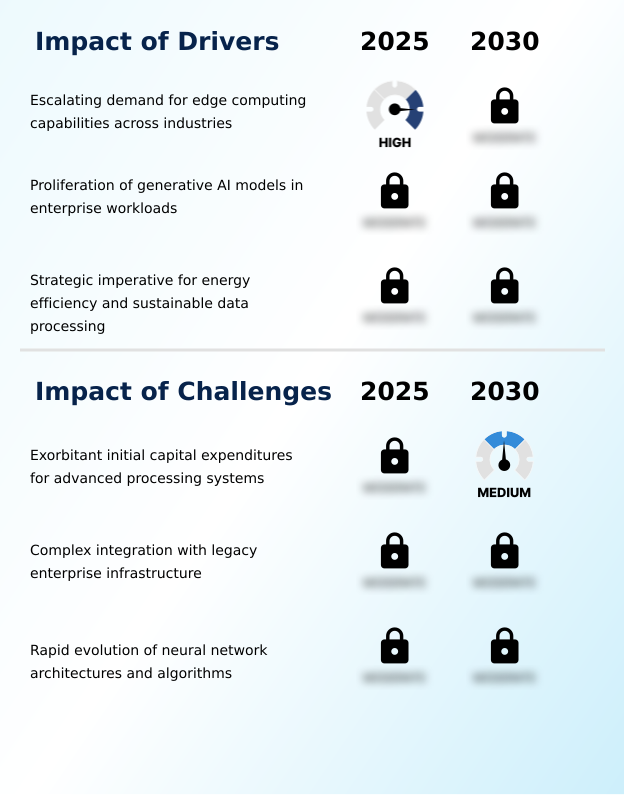

Primary Growth Driver: The escalating demand for edge computing capabilities across various industries serves as a key driver for the market's expansion.

The market's robust 18.5% year-over-year growth is propelled by three primary forces. First, the escalating demand for edge computing is pushing processing capabilities closer to data sources to enable low-latency applications in sectors like industrial automation and autonomous systems.

This requires a new class of low-power AI vision and processing hardware. Second, the widespread integration of generative AI into enterprise workflows has created an insatiable demand for high-throughput inference servers capable of running large language models efficiently.

Finally, a strategic imperative for sustainability is forcing a transition toward more power-efficient AI chips and data center AI hardware, as organizations seek to reduce the spiraling energy costs and environmental impact associated with large-scale AI deployments.

Emerging Market Trend: A primary market trend is the accelerated shift toward application-specific integrated circuits, which are increasingly favored for their efficiency in dedicated inference workloads.

Key market trends are centered on achieving greater efficiency and modularity in AI hardware design. The accelerated shift toward application specific integrated circuits continues as organizations prioritize performance-per-watt for large-scale inference deployments.

This is complemented by the growing adoption of chiplet based architectures, which allows for more flexible and cost-effective silicon design by combining different process nodes in a single package. This move towards heterogeneous computing for AI is crucial for optimizing performance for specific tasks.

Furthermore, to address the persistent data transfer limitations known as the memory wall, the industry is increasingly integrating silicon photonics and co-packaged optics. This technology uses light to transmit data, enabling significantly higher bandwidth and lower power consumption, which is critical for scaling high-performance AI workloads in data centers.

Key Industry Challenge: Exorbitant initial capital expenditures required for procuring advanced processing systems present a key challenge affecting industry-wide adoption and growth.

Significant challenges constrain market growth, beginning with the high initial cost of AI inference hardware, which is a major barrier for many enterprises, as reflected by the high criticality of R&D and Capex in the industry. Beyond procurement, the complex process of AI hardware and software co-design and integration into legacy IT environments creates significant operational friction.

The AI hardware supply chain also presents risks related to component availability and geopolitical factors. Perhaps the most persistent challenge is the rapid evolution of AI processor architecture. The constant emergence of new neural network models creates a risk of hardware obsolescence, forcing a difficult balance between designing highly optimized, specialized chips and more flexible, future-proof platforms.

Explore Full Market Dynamics Analysis Request Free Sample

Ai Inference Hardware Market Segmentation

The ai inference hardware industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Type Segment Analysis

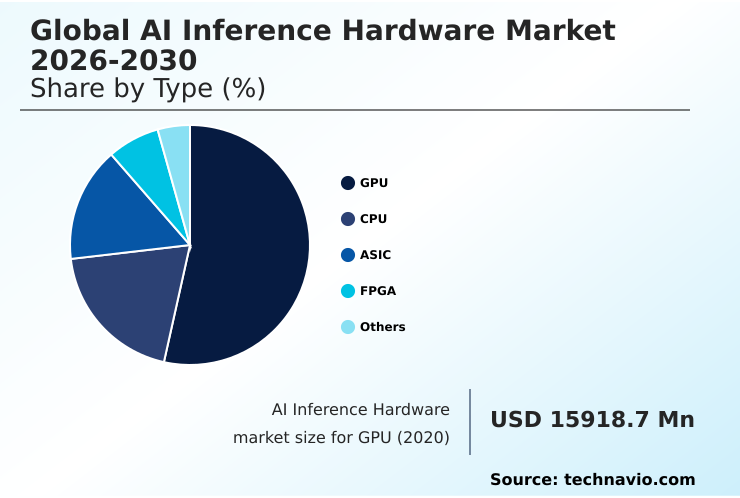

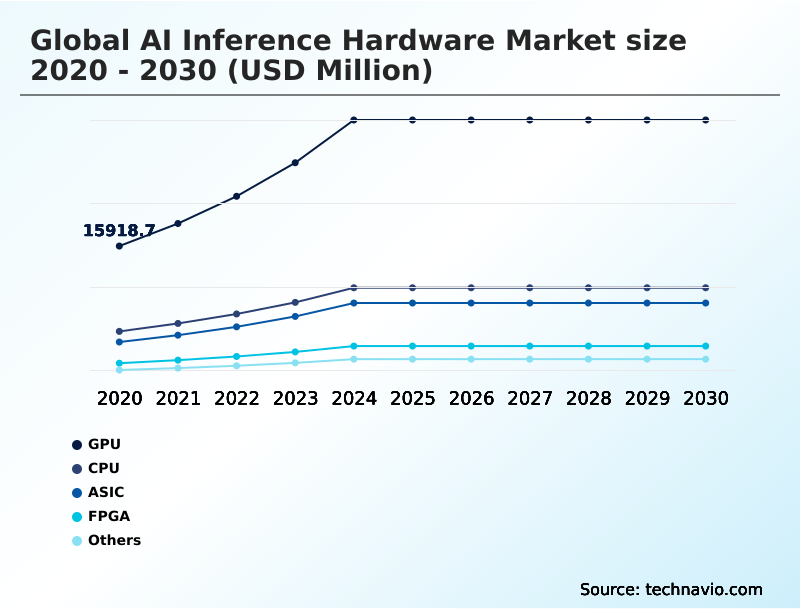

The gpu segment is estimated to witness significant growth during the forecast period.

Graphics processing units represent the foundational hardware for computational inference, with their highly parallel structure being ideal for deep learning inference.

These processors, featuring specialized tensor core GPUs and high bandwidth memory, are optimized for inference workloads by accelerating lower-precision mathematics. The mature software ecosystem surrounding these processors provides a significant competitive advantage, enabling rapid deployment from research to production.

Data centers rely on these accelerators to serve massive language models and complex computer vision systems. While procurement costs are high, the throughput for large batch sizes justifies the investment for hyperscale providers.

This segment's dominance is reflected in its market value, accounting for USD 25804.9 in 2025, underscoring its critical role in the AI hardware ecosystem.

The GPU segment was valued at USD 30.79 billion in 2024 and showed a gradual increase during the forecast period.

Ai Inference Hardware Market by Region: North America Leads with 39.8% Growth Share

North America is estimated to contribute 39.8% to the growth of the global market during the forecast period.

The geographic landscape of the AI inference hardware market is characterized by distinct regional specializations and growth drivers.

North America currently leads, contributing 39.8% of the market's incremental growth, primarily fueled by massive investments in data center AI hardware by hyperscale cloud providers.

In contrast, the APAC region is projected to have the highest CAGR of 21.7%, driven by its dominance in semiconductor manufacturing and the widespread integration of AI in telecommunications and smart city infrastructure.

Meanwhile, Europe's market is heavily influenced by data privacy regulations such as GDPR, which promotes the adoption of on-device AI processing and localized compute solutions to ensure data sovereignty.

This regulatory pressure, combined with a strong industrial automation sector, fosters a growing demand for edge-focused hardware solutions across the continent.

Customer Landscape Analysis for the Ai Inference Hardware Market

The ai inference hardware market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai inference hardware market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Ai Inference Hardware Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the ai inference hardware market industry.

Advanced Micro Devices Inc. - The company's offerings include a range of AI inference hardware, from advanced accelerators and adaptive compute cards to specialized AI processors for diverse applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Amazon.com Inc.

- Apple Inc.

- Arm Ltd.

- Cerebras

- Google LLC

- Groq Inc.

- Hailo Technologies Ltd.

- IBM Corp.

- Intel Corp.

- Kneron Inc.

- MediaTek Inc.

- NVIDIA Corp.

- NXP Semiconductors NV

- Qualcomm Inc.

- SambaNova Systems Inc.

- SiMa Technologies Inc.

- STMicroelectronics NV

- Syntiant Corp.

- Tenstorrent Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Ai Inference Hardware Market

- In May 2025, AMD Inc. and OpenAI announced a strategic partnership aimed at significantly scaling AI infrastructure capacity through the deployment of up to 6 gigawatts of AMD GPU-based compute systems.

- In April 2025, NVIDIA Corp. and Intel Corp. announced a strategic collaboration to co-develop multiple generations of custom data center and PC products designed to accelerate computing workloads across hyperscale, enterprise, and consumer markets.

- In February 2025, Qualcomm Inc. announced the introduction of its next-generation AI inference-optimized solutions for data centers, including the Qualcomm AI200 and AI250 chip-based accelerator cards and rack-scale systems.

- In January 2025, Dell Technologies introduced the PowerEdge XE8712 server, positioning it as a high-density AI infrastructure solution for complex workloads.

Research Analyst Overview: Ai Inference Hardware Market

The market is undergoing a fundamental transition away from reliance on general-purpose hardware toward a more fragmented and specialized landscape. Boardroom decisions now involve complex trade-offs between the flexibility of graphics processing units and the superior total cost of ownership offered by application specific integrated circuits for high-volume workloads.

This strategic calculus is further complicated by supply chain considerations influenced by trade policies governing advanced semiconductor exports. The adoption of chiplet based architectures and advanced packaging techniques is lowering the barrier to entry for custom silicon, enabling more companies to develop bespoke solutions.

As a result, the market is seeing a proliferation of novel designs, including reconfigurable dataflow units and RISC-V-based AI accelerators. This trend is happening alongside the development of next-generation technologies like co-packaged optics and neuromorphic computing, which promise to address long-term bottlenecks in data movement and power consumption.

While GPUs still dominate in terms of market value, the faster growth of custom and specialized hardware signals a clear directional shift for procurement strategies.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ai Inference Hardware Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 314 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 20.8% |

| Market growth 2026-2030 | USD 106251.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 18.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, The Netherlands, Sweden, Spain, China, Japan, India, South Korea, Taiwan, Indonesia, UAE, Saudi Arabia, Israel, South Africa, Qatar, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Ai Inference Hardware Market: Key Questions Answered in This Report

-

What is the expected growth of the Ai Inference Hardware Market between 2026 and 2030?

-

The Ai Inference Hardware Market is expected to grow by USD 106.25 billion during 2026-2030, registering a CAGR of 20.8%. Year-over-year growth in 2026 is estimated at 18.5%%. This acceleration is shaped by escalating demand for edge computing capabilities across industries, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (GPU, CPU, ASIC, FPGA, and Others), Deployment (Cloud inference, Edge inference, and On-premises), Application (Computer vision, Robotics, Generative AI, NLP, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America). Among these, the GPU segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, Middle East and Africa and South America. North America is estimated to contribute 39.8% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, The Netherlands, Sweden, Spain, China, Japan, India, South Korea, Taiwan, Indonesia, UAE, Saudi Arabia, Israel, South Africa, Qatar, Brazil, Argentina and Chile, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is escalating demand for edge computing capabilities across industries, which is accelerating investment and industry demand. The main challenge is exorbitant initial capital expenditures for advanced processing systems , creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Ai Inference Hardware Market?

-

Key vendors include Advanced Micro Devices Inc., Amazon.com Inc., Apple Inc., Arm Ltd., Cerebras, Google LLC, Groq Inc., Hailo Technologies Ltd., IBM Corp., Intel Corp., Kneron Inc., MediaTek Inc., NVIDIA Corp., NXP Semiconductors NV, Qualcomm Inc., SambaNova Systems Inc., SiMa Technologies Inc., STMicroelectronics NV, Syntiant Corp. and Tenstorrent Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Ai Inference Hardware Market Research Insights

Market dynamics are increasingly shaped by the complex interplay between deployment strategies and the AI hardware supply chain. The necessity for data sovereignty, governed by frameworks like GDPR, is compelling enterprises to adopt on-premises and edge solutions over purely cloud-based inference as a service (IaaS).

This trend is particularly evident in the automotive sector, where AI hardware for automotive systems requires localized processing for safety-critical functions. This shift influences the demand for different types of semiconductor for AI, with the growth of ASICs outpacing GPUs, reflecting a move toward workload-specific optimization.

As a result, procurement decisions are becoming more nuanced, balancing the flexibility of general-purpose hardware against the superior performance-per-watt of custom-designed chips for specific, high-volume inference tasks.

We can help! Our analysts can customize this ai inference hardware market research report to meet your requirements.

RIA -

RIA -