AI IP And Licensing Market Size 2026-2030

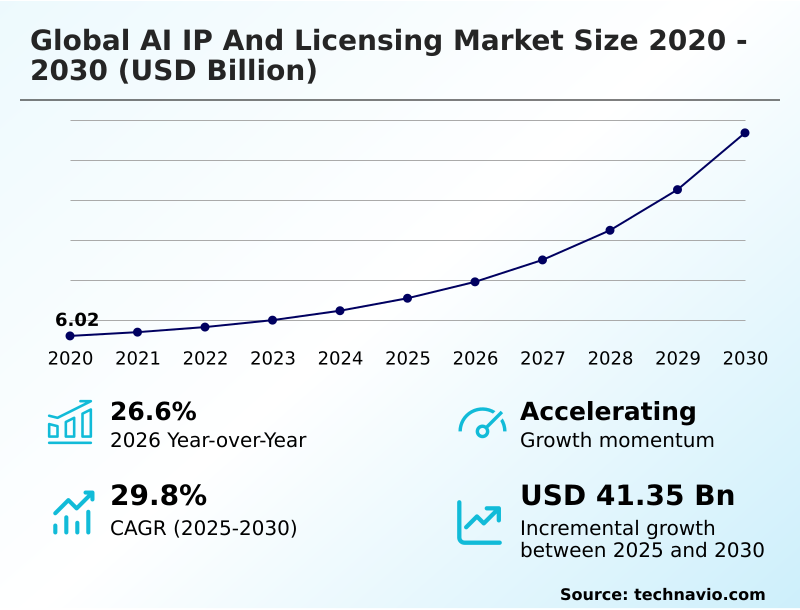

The AI IP And Licensing Market size was valued at USD 15.44 billion in 2025, growing at a CAGR of 29.8% during the forecast period 2026-2030.

Major Market Trends & Insights

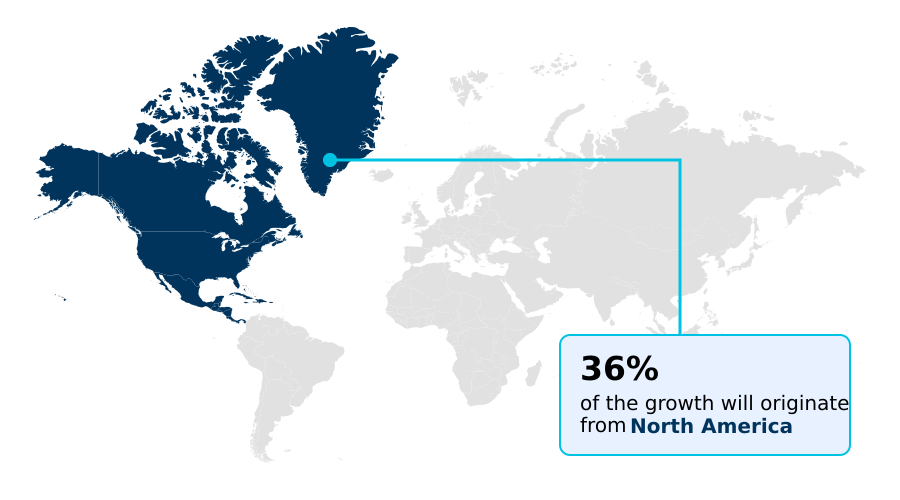

- North America dominated the market and accounted for a 36.1% growth during the forecast period.

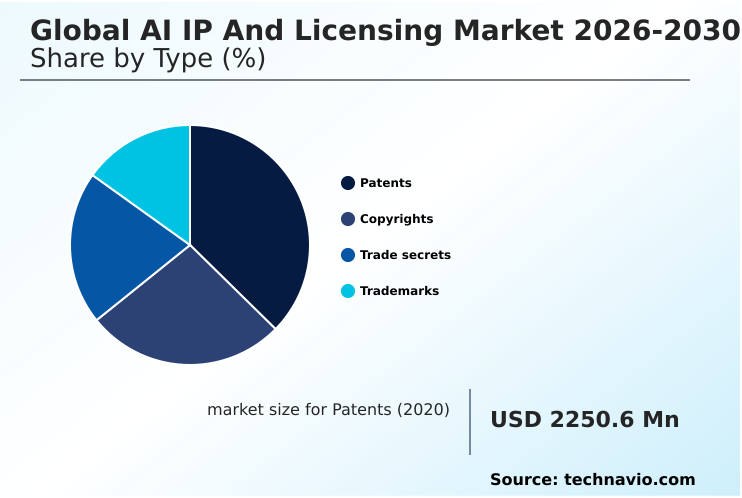

- By Type - Patents segment was valued at USD 4.68 billion in 2024

- By License Model - Proprietary licenses segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 50.76 billion

- Market Future Opportunities 2025-2030: USD 41.35 billion

- CAGR from 2025 to 2030 : 29.8%

Market Summary

- The AI IP and licensing market is defined by rapid innovation cycles where over 70% of large enterprises now integrate some form of licensed AI, reflecting a critical shift from research concepts to essential business tools. A primary driver is the massive investment in generative AI infrastructure, which provides the necessary foundation for developing and deploying intellectual property.

- For instance, a manufacturer licensing a predictive maintenance algorithm can reduce equipment downtime by up to 25%, directly improving operational efficiency. However, the market faces a significant challenge with the high procurement prices of computing resources, as the cost of a single high-end AI accelerator can exceed that of a small-scale pilot project, creating a barrier to entry.

- This dynamic forces a strategic balance between leveraging cutting-edge, resource-intensive models and adopting more efficient, cost-effective algorithms. Consequently, licensing models are evolving to offer greater flexibility to accommodate a wider range of enterprise needs and budgets.

What will be the Size of the AI IP And Licensing Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the AI IP And Licensing Market Segmented?

The ai ip and licensing industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

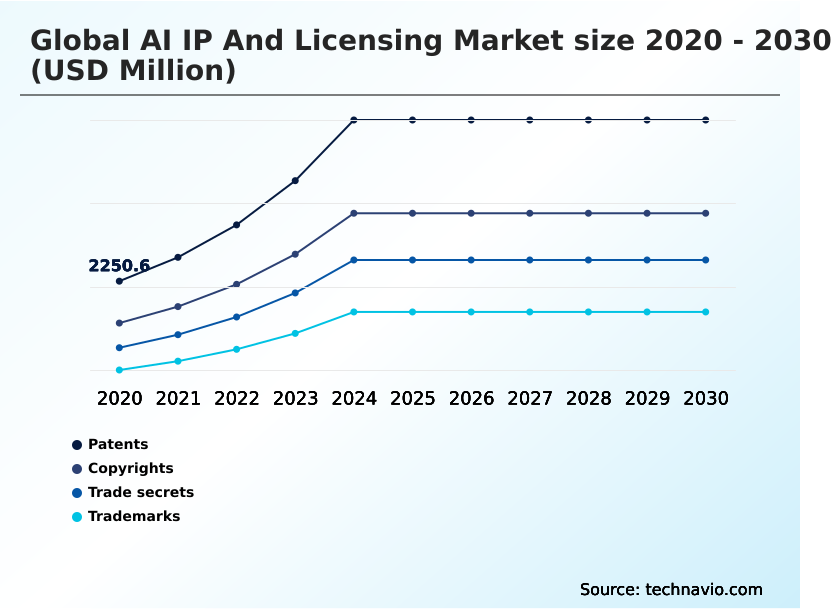

- Type

- Patents

- Copyrights

- Trade secrets

- Trademarks

- License model

- Proprietary licenses

- Subscription-based licenses

- Open-source licenses

- Hybrid licenses

- Others

- End-user

- BFSI

- Healthcare

- Automotive

- Retail and e-commerce

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- UAE

- Saudi Arabia

- Israel

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

How is the AI IP And Licensing Market Segmented by Type?

The patents segment is estimated to witness significant growth during the forecast period.

The patents segment is expanding, with patent filings for generative models increasing by over 40% as companies seek to protect proprietary algorithms.

This growth is driven by the need to secure intellectual property for neural network architectures, where a 15% improvement in processing efficiency can create a significant competitive advantage.

As a result, businesses are intensifying their patent portfolio management to defend against patent litigation and to capitalize on licensing opportunities.

The surge in enterprise automation software adoption is also compelling organizations to secure patents for unique workflow innovations, solidifying their market position through legally protected technological differentiation.

The Patents segment was valued at USD 4.68 billion in 2024 and showed a gradual increase during the forecast period.

How demand for the AI IP And Licensing market is rising in the leading region?

North America is estimated to contribute 36.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI IP And Licensing Market demand is rising in North America Request Free Sample

The global AI IP and licensing market exhibits distinct regional dynamics, with North America leading, contributing to over 36% of the incremental growth, driven by its mature venture capital ecosystem.

The US, in particular, dominates the region, accounting for more than 80% of its market value due to the high concentration of major technology firms and research institutions.

In contrast, the APAC market, projected to grow at the fastest rate, is characterized by a focus on integrating AI into manufacturing and consumer electronics, where technology transfer agreements are common.

This regional difference in adoption—industrial automation in APAC versus foundational model development in North America—shapes licensing strategies.

For example, licensing explainable AI is a higher priority in Europe to meet regulatory demands, while APAC focuses on licensing for high-volume production, impacting everything from computer vision patents to natural language processing algorithms.

What are the key Drivers, Trends, and Challenges in the AI IP And Licensing Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises evaluating AI model licensing agreement costs are navigating a complex market where value is tied to both technological sophistication and legal defensibility. The increasing adoption of federated learning IP protection strategies is a direct response to data privacy concerns, allowing companies to train models collaboratively without sharing sensitive raw data.

- This approach has proven to be over 20% more effective in certain regulated industries compared to centralized data models. Concurrently, edge AI software patent trends show a definitive shift toward on-device processing to reduce latency and enhance user privacy, a critical factor in the consumer electronics sector.

- However, this decentralized approach raises concerns about generative AI copyright infringement risks, as tracking the provenance of content created on millions of devices becomes a significant challenge. To mitigate these risks and ensure compliance, many organizations are adopting sovereign cloud data compliance for AI, which mandates that all data and processing adhere to the legal frameworks of a specific jurisdiction.

- This strategy ensures data sovereignty but can increase operational complexity, requiring a careful balance between legal security and technological agility.

What are the key market drivers leading to the rise in the adoption of AI IP And Licensing Industry?

- Substantial investment in generative AI infrastructure is the primary market driver, creating the foundational computational capacity needed for AI IP development and deployment.

- The rapid adoption of enterprise automation software is a primary driver, with over 70% of large corporations now licensing some form of AI to improve operational efficiency.

- This integration of autonomous agentic systems and intelligent document processing is delivering measurable returns, with some firms reporting a 30% reduction in operational expenses.

- A correlated driver is the cross-industry demand for digital transformation, which fuels the market for data licensing marketplaces and proprietary algorithms. The development of large language models is also accelerating growth, supported by massive investments in high-performance computing clusters.

- These models, which are often licensed, provide the foundation for a new generation of applications, from customer service bots to complex analytical tools, creating a self-reinforcing cycle of innovation and demand.

What are the market trends shaping the AI IP And Licensing Industry?

- The market is observing a significant trend toward sovereign AI model licensing. This shift is driven by nations seeking technological autonomy and data security within their jurisdictions.

- Sovereign AI models are becoming a dominant trend, with national governments driving demand for localized licensing frameworks to ensure data residency, reflecting a 30% increase in government-led AI initiatives. This shift necessitates the development of sovereign cloud infrastructures and the technology transfer of foundational architectures, allowing regional entities to customize models.

- Another key trend is the optimization of intellectual property for edge computing, where model pruning and quantization techniques are reducing model sizes by up to 90% to enable on-device generative tasks. This move to the edge is creating new patent opportunities in federated learning and hardware-accelerated security, allowing for privacy-preserving innovation.

- The adoption of digital watermarking is also growing as a method for tracking model weights and protecting intellectual property in decentralized environments.

What challenges does the AI IP And Licensing Industry face during its growth?

- The considerable expense and intricacy of complex global patent litigation represent a key challenge, restraining market growth by consuming resources and creating legal uncertainty.

- A primary challenge restraining the market is the high cost of AI accelerators and computing resources, which can represent over 50% of the total budget for developing a new large-scale model. This financial barrier limits entry for smaller firms and slows innovation.

- Compounding this issue are the complexities of global data sovereignty regulations, which require companies to maintain separate, localized infrastructures, increasing operational overhead by as much as 25% in certain regions. Furthermore, the risk of complex global patent litigation and the difficulty of protecting trade secrets in a fast-paced environment create significant legal and financial uncertainty.

- The lack of unified standards for copyright protection for AI-generated content adds another layer of legal ambiguity, deterring investment and complicating licensing negotiations.

Exclusive Technavio Analysis on Customer Landscape

The ai ip and licensing market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai ip and licensing market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI IP And Licensing Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai ip and licensing market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Key offerings include enterprise AI licensing, cloud-based AI services, and proprietary AI technologies embedded within devices and software frameworks.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Alibaba Group Holding Ltd.

- Amazon Web Services Inc.

- Apple Inc.

- Baidu Inc.

- CEVA Inc.

- Google LLC

- IBM Corp.

- Intel Corp.

- InterDigital Inc.

- Meta Platforms Inc.

- Microsoft Corp.

- NVIDIA Corp.

- Oracle Corp.

- Qualcomm Inc.

- Salesforce Inc.

- SAP SE

- Siemens AG

- SoftBank Group Corp.

- Tata Consultancy Services

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Application Software industry, the widespread adoption of cloud-native and SaaS delivery models is compelling AI IP licensors to shift from perpetual licenses to flexible, subscription-based licensing frameworks to align with enterprise consumption patterns.

- The increasing integration of low-code/no-code platforms within enterprise automation software is creating new demand for modular AI IP, requiring licensors to offer more granular and easily integrable proprietary algorithms.

- Stricter data privacy regulations, such as GDPR and similar frameworks, are forcing application software developers to seek out AI IP with built-in compliance features, particularly for federated learning and sovereign AI models, impacting licensing agreements.

- A significant push toward workflow interoperability in application software suites is driving demand for AI IP that supports open standards and APIs, facilitating easier integration of natural language processing algorithms into diverse enterprise ecosystems.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI IP And Licensing Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 322 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 29.8% |

| Market growth 2026-2030 | USD 41349.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 26.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Singapore, UAE, Saudi Arabia, Israel, South Africa, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI IP and licensing market ecosystem is a complex web of interdependent stakeholders, with technology suppliers providing the foundational AI accelerators and high-performance computing clusters that are essential for development. AI solution providers, ranging from large-cap tech firms to specialized startups, develop and license proprietary algorithms and neural network architectures.

- These providers engage with end-users across diverse sectors through various licensing frameworks, including proprietary and subscription-based models. A key dynamic is the role of regulatory bodies, which enforce data sovereignty and copyright protection, influencing how intellectual property is created and managed. For instance, compliance with regional data mandates can increase development costs by 15-20%.

- The value chain is completed by distribution channels, including cloud marketplaces and direct sales, which facilitate the commercialization of generative models and other AI assets, enabling widespread enterprise adoption.

What are the Key Data Covered in this AI IP And Licensing Market Research and Growth Report?

-

What is the expected growth of the AI IP And Licensing Market between 2026 and 2030?

-

The AI IP And Licensing Market is expected to grow by USD 41.35 billion during 2026-2030, registering a CAGR of 29.8%. Year-over-year growth in 2026 is estimated at 26.6%%. This acceleration is shaped by generative ai infrastructure investment, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Patents, Copyrights, Trade secrets, and Trademarks), License Model (Proprietary licenses, Subscription-based licenses, Open-source licenses, Hybrid licenses, and Others), End-user (BFSI, Healthcare, Automotive, Retail and e-commerce, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America). Among these, the Patents segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, Middle East and Africa and South America. North America is estimated to contribute 36.1% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Singapore, UAE, Saudi Arabia, Israel, South Africa, Turkey, Brazil, Argentina and Colombia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is generative ai infrastructure investment, which is accelerating investment and industry demand. The main challenge is complex global patent litigation costs, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the AI IP And Licensing Market?

-

Key vendors include Accenture Plc, Alibaba Group Holding Ltd., Amazon Web Services Inc., Apple Inc., Baidu Inc., CEVA Inc., Google LLC, IBM Corp., Intel Corp., InterDigital Inc., Meta Platforms Inc., Microsoft Corp., NVIDIA Corp., Oracle Corp., Qualcomm Inc., Salesforce Inc., SAP SE, Siemens AG, SoftBank Group Corp. and Tata Consultancy Services. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for AI IP and licensing is intensely active, with over 70% of large enterprises now integrating licensed AI into core workflows. Key vendors are shaping the market through strategic initiatives focused on accessibility and specialization.

- For instance, a major cloud provider recently launched a marketplace for pre-trained machine learning models, lowering the barrier to entry for smaller firms. This move directly addresses the demand for scalable AI solutions. Concurrently, a leading semiconductor firm finalized licensing agreements for its on-device generative AI, enabling advanced processing on smartphones and other edge devices.

- These actions reflect the broader industry trend of embedding AI capabilities across diverse hardware and software ecosystems. Companies are navigating the high costs of computing resources, which can account for up to 30% of an AI project's budget, by optimizing algorithms and exploring more efficient hardware.

We can help! Our analysts can customize this ai ip and licensing market research report to meet your requirements.

RIA -

RIA -