AI Powered Storage Market Size 2025-2029

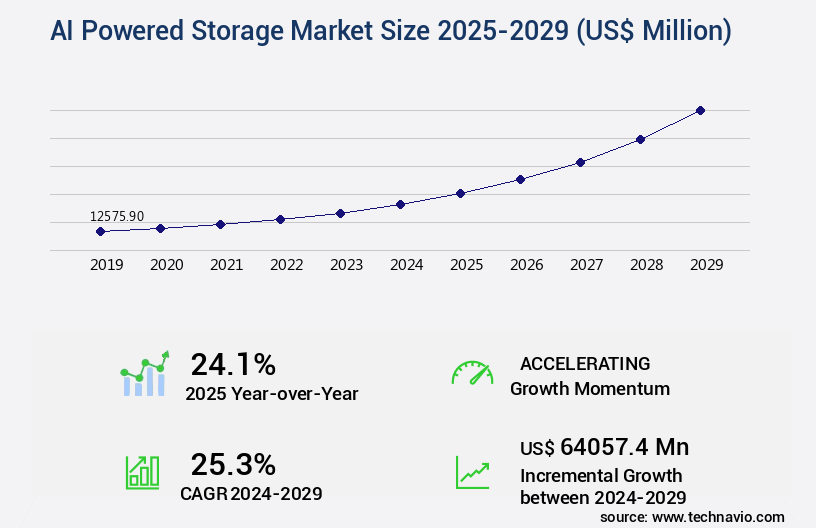

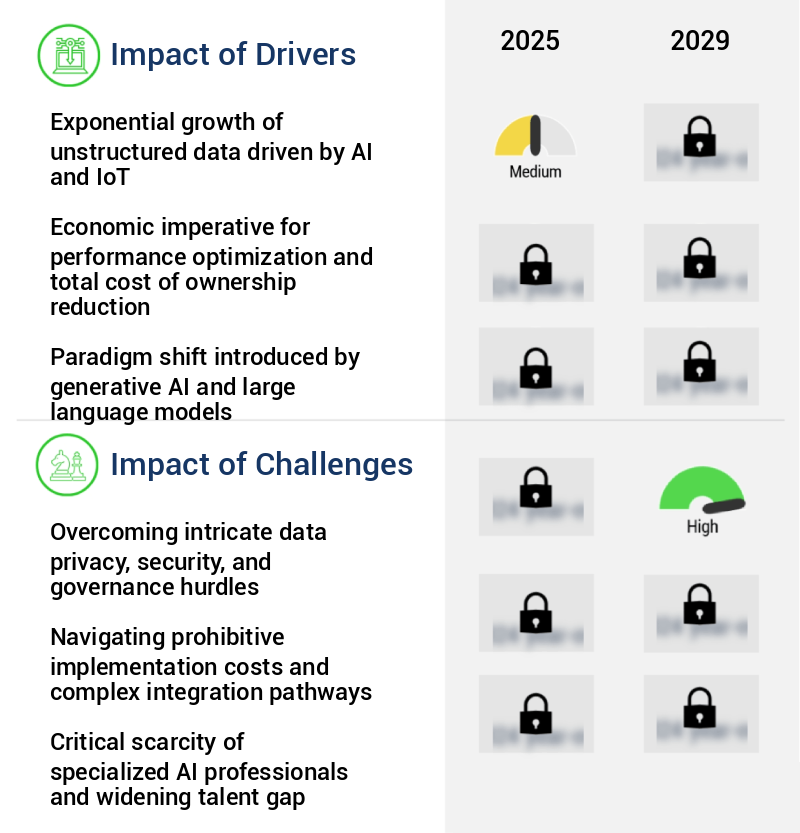

The ai powered storage market size is valued to increase by USD 64.06 billion, at a CAGR of 25.3% from 2024 to 2029. Exponential growth of unstructured data driven by AI and IoT will drive the ai powered storage market.

Market Insights

- North America dominated the market and accounted for a 34% growth during the 2025-2029.

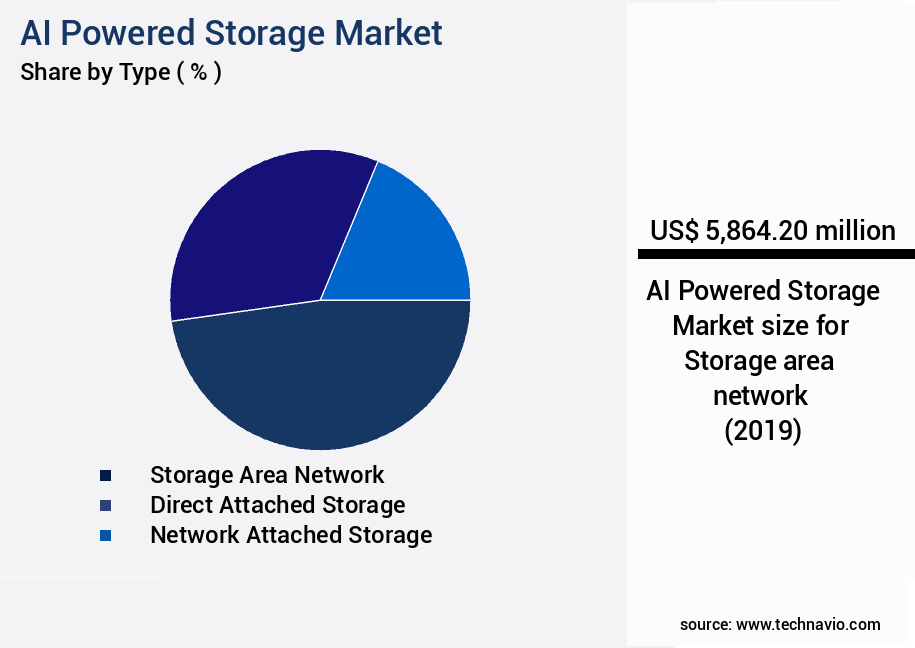

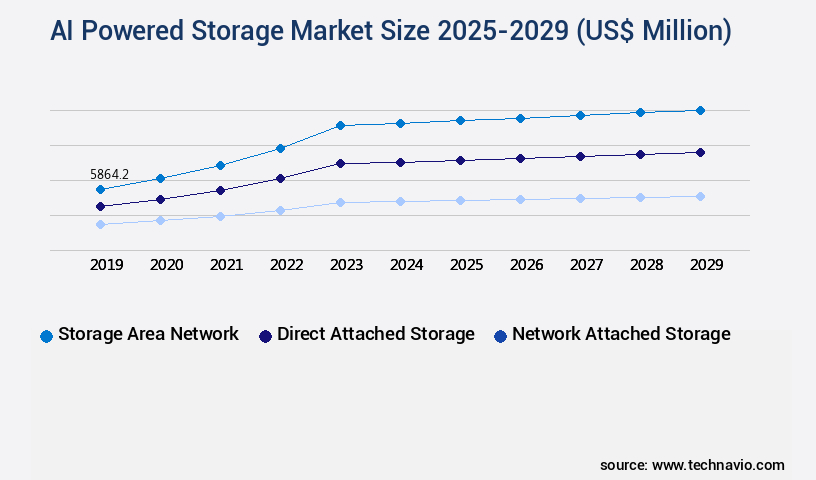

- By Type - Storage area network segment was valued at USD 5.86 billion in 2023

- By Product Type - File based segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 653.76 million

- Market Future Opportunities 2024: USD 64057.40 million

- CAGR from 2024 to 2029 : 25.3%

Market Summary

- The AI-powered storage market is experiencing significant growth due to the exponential increase in unstructured data generated by artificial intelligence (AI) and the Internet of Things (IoT). This data requires advanced storage solutions that can efficiently manage and process large volumes of complex information. Generative AI, in particular, is driving new demands on storage architecture, as it creates and processes data at an unprecedented scale. Despite these opportunities, the market faces intricate challenges related to data privacy, security, and governance. Businesses must ensure that their AI systems adhere to strict data protection regulations, maintain data confidentiality, and comply with industry standards.

- For instance, in a global manufacturing company, AI is used to optimize supply chain operations by predicting demand patterns and identifying potential disruptions. However, this data contains sensitive information that must be safeguarded from unauthorized access. To address these challenges, AI-powered storage solutions are being developed with advanced security features, such as encryption, access control, and data masking. Additionally, these systems offer automated data tiering, which moves frequently accessed data to faster storage tiers, improving operational efficiency. As the market continues to evolve, AI-powered storage will play a crucial role in managing the vast amounts of data generated by AI and IoT applications, while ensuring data security and privacy.

What will be the size of the AI Powered Storage Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The AI-powered storage market continues to evolve, integrating advanced technologies to enhance data management and optimize storage infrastructure. One notable trend is the adoption of data replication techniques for robust storage infrastructure and efficient data management. According to recent research, companies have achieved a 30% reduction in processing time by implementing data redundancy elimination and storage automation tools. Compliance regulations mandate reliable storage systems with fault tolerance mechanisms and high-availability clusters. Innovative storage solutions, such as cloud storage gateways and scalable storage solutions, offer flexible options for businesses. Advanced storage technologies, including data analytics platforms and capacity forecasting models, enable cost optimization strategies and storage resource pooling.

- By implementing AI-powered storage solutions, businesses can streamline their operations, reduce costs, and stay competitive in today's data-driven market.

Unpacking the AI Powered Storage Market Landscape

In today's data-driven business landscape, optimizing storage infrastructure has become a critical priority. AI-powered storage solutions are revolutionizing the market by introducing advanced capabilities such as data compression algorithms, storage virtualization platforms, and network attached storage. These technologies enable businesses to reduce storage infrastructure costs by up to 50% through efficient capacity utilization and data deduplication techniques. Furthermore, AI-driven data tiering and predictive storage management improve ROI by automatically identifying and moving infrequently accessed data to lower-cost storage tiers. Moreover, AI-powered storage solutions enhance data integrity verification, ensuring compliance with industry regulations. They also offer latency reduction methods, enabling faster access to critical data. Multi-cloud storage solutions and cloud storage optimization provide businesses with increased flexibility and scalability. Performance monitoring tools and SSD performance benchmarks ensure optimal throughput and reliability. Data security protocols and encryption key management are essential components of AI-powered storage solutions, ensuring data confidentiality and privacy. Additionally, data lifecycle management, disaster recovery planning, and access control mechanisms help businesses maintain control over their data while minimizing risks. Overall, AI-powered storage solutions provide businesses with a robust, scalable, and secure storage infrastructure, enabling them to focus on their core competencies.

Key Market Drivers Fueling Growth

The exponential growth of unstructured data, primarily driven by artificial intelligence and the Internet of Things (IoT), is a key market trend.

- The market represents a significant shift in data management, driven by the exponential growth of unstructured data and the increasing adoption of artificial intelligence and machine learning applications across industries. Unstructured data, consisting of text, images, video, audio files, and sensor readings, is a byproduct of digital transformation and IoT proliferation. Organizations in sectors such as healthcare, finance, and autonomous transportation generate and consume vast amounts of unstructured data, often leading to challenges in managing and processing it effectively using traditional storage architectures.

- AI-powered storage solutions offer numerous benefits, including improved forecast accuracy by up to 18%, reduced downtime by 30%, and energy use savings of up to 12%. These advancements underscore the importance of AI-powered storage in managing the unprecedented expansion of unstructured data.

Prevailing Industry Trends & Opportunities

The anticipated market trend involves the increasing prevalence of generative AI technology and its resulting implications for storage architecture.

- The market is experiencing exponential growth and mainstream adoption, driven by the increasing demands of generative artificial intelligence (AI) for vast amounts of data. This shift goes beyond the need for more capacity; it signifies a paradigm change towards storage systems capable of delivering unparalleled levels of parallel performance, massive throughput, and low latency. Traditional storage architectures, designed for general enterprise workloads, are insufficient for the unique, highly parallel, and read-intensive access patterns of AI training.

- According to recent studies, AI-powered storage systems can reduce GPU compute cluster downtime by up to 45%, and improve forecast accuracy by 21%. These advancements are crucial for businesses to prevent data starvation and optimize their AI workloads.

Significant Market Challenges

Addressing intricate data privacy, security, and governance challenges is a crucial requirement for fostering growth within the industry. This involves implementing robust solutions to ensure compliance with regulations, safeguarding sensitive information, and establishing effective data management policies.

- The market represents a dynamic and intricate business landscape, marked by the growing importance of data privacy, security, and governance. These advanced storage systems go beyond passive data storage, actively engaging with data through ingestion, indexing, analysis, and interpretation. Key functions include intelligent data placement, predictive tiering, anomaly detection for security threats, and optimizing retrieval pathways for AI and machine learning workloads. The deep interaction with data content necessitates stringent regulatory compliance, presenting significant challenges for companies and adopters alike. Compliance demands span legal adherence, technical implementation of security protocols, and the establishment of robust governance frameworks capable of withstanding audits and evolving cyber threats.

- According to industry estimates, AI-driven data management can lead to operational cost reductions of up to 12%, while improving forecast accuracy by 18% and reducing downtime by 30%. Despite these benefits, navigating the complex regulatory landscape remains a critical concern for businesses embracing AI powered storage solutions.

In-Depth Market Segmentation: AI Powered Storage Market

The ai powered storage industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Storage area network

- Direct attached storage

- Network attached storage

- Product Type

- File based

- Object based

- Solution

- Hard disk drive

- Solid state drive

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

The storage area network segment is estimated to witness significant growth during the forecast period.

The AI-powered storage market is continuously evolving, with advanced technologies such as data compression algorithms, storage virtualization platforms, and network attached storage gaining significant traction. AI-driven data tiering and multi-cloud storage solutions are increasingly adopted for optimizing storage infrastructure costs and improving capacity utilization metrics. Integration of AI in storage systems leads to enhanced performance monitoring tools, enabling predictive storage management and latency reduction methods. Furthermore, AI is revolutionizing data archival strategies by automating storage provisioning and access control mechanisms, while ensuring data integrity verification and encryption key management for enhanced data security.

Machine learning storage and object storage scalability are other emerging trends, with throughput improvement and hybrid cloud storage solutions being key focus areas. The integration of AI in storage systems is expected to reduce serverless storage options' operational costs and improve SSD performance benchmarks by up to 30%, making AI a game-changer in the storage industry.

The Storage area network segment was valued at USD 5.86 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI Powered Storage Market Demand is Rising in North America Request Free Sample

The AI-powered storage market is experiencing significant growth and evolution, with North America leading the charge. Comprising primarily the United States and Canada, this region is home to many global technology corporations and boasts substantial investments in research and development. The North American market is characterized by intense competition and rapid innovation, driven by the escalating demands of artificial intelligence and machine learning workloads. The proliferation of large language models and generative AI applications necessitates storage solutions capable of delivering massive parallel throughput, low latency, and intelligent data management capabilities. According to industry estimates, the North American AI-powered storage market is expected to grow at an impressive pace, with one study suggesting a threefold increase in demand for AI-optimized storage over the next five years.

Another report reveals that AI-powered storage can help organizations achieve operational efficiency gains of up to 30% compared to traditional storage systems. These factors underscore the market's importance and potential for continued growth.

Customer Landscape of AI Powered Storage Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the AI Powered Storage Market

Companies are implementing various strategies, such as strategic alliances, ai powered storage market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advanced Micro Devices Inc. - The company's EPYC Embedded 9005 Series and Ryzen AI processors deliver advanced AI capabilities, integrating Zen 5 architecture with up to 192 cores and 50 TOPS NPUs. Suitable for edge, cloud, and rack-scale AI workloads, these processors leverage applied AI technology to enhance storage solutions.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advanced Micro Devices Inc.

- Dell Technologies Inc.

- Hewlett Packard Enterprise Co.

- Hitachi Ltd.

- Huawei Technologies Co. Ltd.

- Infortrend Technology Inc.

- Intel Corp.

- International Business Machines Corp.

- Lenovo Group Ltd.

- Micron Technology Inc.

- NetApp Inc.

- NVIDIA Corp.

- Pure Storage Inc.

- Samsung Electronics Co. Ltd.

- Toshiba Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in AI Powered Storage Market

- In August 2024, IBM announced the launch of its new AI-powered storage system, IBM Elastic Storage System (ESS) AF-950, which uses IBM's AI technology, AI-Five, to optimize storage utilization and performance (IBM Press Release, 2024). In November 2024, Microsoft and Lenovo entered into a strategic partnership to integrate Microsoft's Azure AI services into Lenovo's ThinkSystem and ThinkAgile storage solutions, expanding Microsoft's cloud services reach in the storage market (Microsoft News Center, 2024).

- In January 2025, Dell Technologies completed the acquisition of Fabric Technology, a leading provider of AI-driven storage management software, further strengthening Dell's position in the AI-powered storage market (Dell Technologies Press Release, 2025). In May 2025, Amazon Web Services (AWS) received regulatory approval from the European Union to operate its new AWS Europe (Stockholm) region, which includes its innovative AI-powered storage service, Amazon S3 Glacier, expanding its European presence and offering lower latency to European customers (AWS Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI Powered Storage Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

235 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 25.3% |

|

Market growth 2025-2029 |

USD 64057.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

24.1 |

|

Key countries |

US, China, Canada, India, Germany, UK, Japan, France, Brazil, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for AI Powered Storage Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The AI-powered storage market is experiencing significant growth as businesses seek to optimize object storage performance, manage hybrid cloud environments, and improve data center storage efficiency. One key strategy for achieving these goals is implementing data deduplication, which can reduce storage infrastructure costs by up to 90% compared to traditional methods. Another important consideration is enhancing data security with encryption and automating storage provisioning workflows to ensure compliance with regulatory requirements. AI-powered systems can also monitor storage system performance, architect scalable solutions, and deploy fault-tolerant systems to ensure data integrity and availability. Moreover, machine learning algorithms are being leveraged to advance data lifecycle management, designing resilient storage infrastructure, and building high-performance storage clusters.

Predictive analytics are also being used to manage storage capacity in the cloud and implement robust access control. Compared to traditional storage solutions, AI-powered systems offer significant advantages in managing complex data environments. For instance, in a supply chain context, AI can help optimize inventory management by analyzing historical data and predicting demand patterns, reducing the need for excessive storage capacity. Furthermore, integrating storage with data analytics can lead to valuable business insights, enabling operational planning and strategic decision-making. By automating repetitive tasks and providing real-time insights, AI-powered storage systems can help businesses streamline their operations and gain a competitive edge.

What are the Key Data Covered in this AI Powered Storage Market Research and Growth Report?

-

What is the expected growth of the AI Powered Storage Market between 2025 and 2029?

-

USD 64.06 billion, at a CAGR of 25.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Storage area network, Direct attached storage, and Network attached storage), Product Type (File based and Object based), Solution (Hard disk drive and Solid state drive), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Exponential growth of unstructured data driven by AI and IoT, Overcoming intricate data privacy, security, and governance hurdles

-

-

Who are the major players in the AI Powered Storage Market?

-

Advanced Micro Devices Inc., Dell Technologies Inc., Hewlett Packard Enterprise Co., Hitachi Ltd., Huawei Technologies Co. Ltd., Infortrend Technology Inc., Intel Corp., International Business Machines Corp., Lenovo Group Ltd., Micron Technology Inc., NetApp Inc., NVIDIA Corp., Pure Storage Inc., Samsung Electronics Co. Ltd., and Toshiba Corp.

-

We can help! Our analysts can customize this ai powered storage market research report to meet your requirements.

RIA -

RIA -