Ambient Food Packaging Market Size 2024-2028

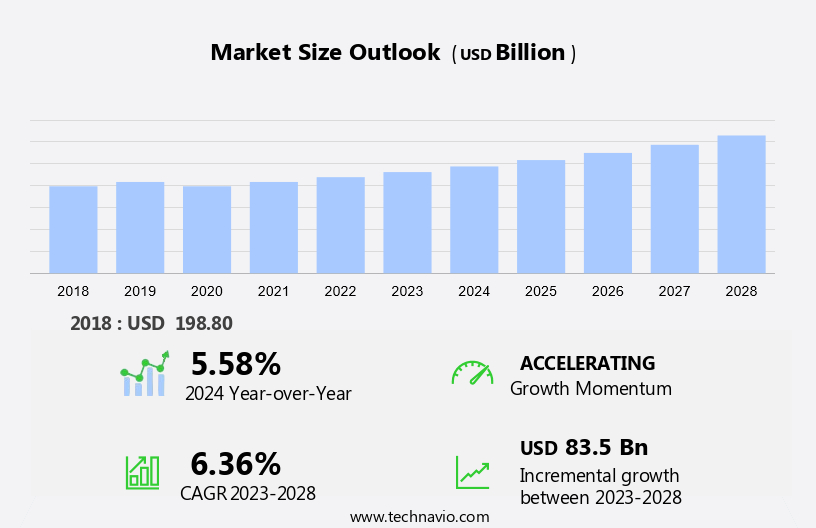

The ambient food packaging market size is forecast to increase by USD 83.5 billion at a CAGR of 6.36% between 2023 and 2028. The market is experiencing significant growth due to several key factors. Firstly, the increasing demand for long shelf life in packaged food, including Fruit and vegetables and Pasta, is driving market expansion. Additionally, the rise of e-commerce and online grocery shopping has led to a higher need for packaging that can maintain product freshness during transportation, particularly in the case of MPS (Modified Atmosphere Packaging) solutions. Sustainability is also a major trend in the market, with consumers and businesses increasingly favoring eco-friendly packaging solutions. Lastly, high processing requirements in ambient food packaging are another market growth factor. Sustainability is a growing concern in the ambient food packaging market, with consumers expressing a preference for eco-friendly and sustainable packaging alternatives. In terms of materials, both plastic and paper-based packaging are popular choices, with the latter gaining traction due to its sustainable properties. Barrier properties are a crucial consideration for ambient food packaging, as they help maintain product freshness and prevent contamination.

What will be the Size of the Market During the Forecast Period?

The market is witnessing significant advancements driven by the growing demand for non-refrigerated food, convenience, and on-the-go snacks. This market is experiencing transformative changes with the integration of smart packaging technologies, IoT, sensors, and data analytics to ensure product quality, food safety, and sustainability. Smart packaging solutions are increasingly gaining traction in the market as they offer real-time monitoring of food freshness, temperature, and humidity levels. These advanced packaging systems utilize sensors and data analytics to provide valuable insights into the condition of the food and enable proactive measures to maintain product quality and safety.

Furthermore, the integration of IoT in ambient food packaging is revolutionizing the industry by enabling seamless communication between the packaging and various stakeholders. This technology enables real-time tracking of the food supply chain, ensuring efficient inventory management, and reducing product wastage. Food safety and product quality are critical factors in the market. Advanced packaging techniques such as sterilized packs and pasteurized packs are gaining popularity due to their ability to extend the shelf life of food products while maintaining their quality and safety. E-commerce and online grocery shopping are driving the growth of the market.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

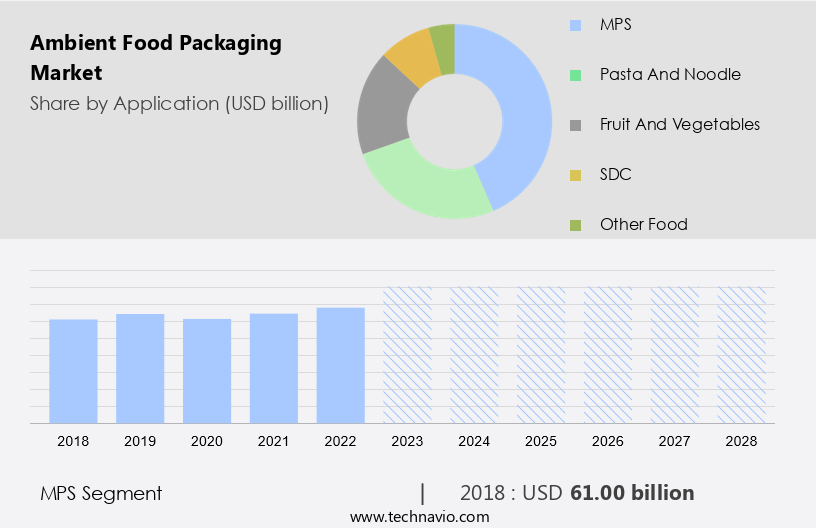

- Application

- MPS

- Pasta and noodle

- Fruit and vegetables

- SDC

- Other food

- Geography

- APAC

- China

- Japan

- Europe

- Germany

- UK

- North America

- US

- South America

- Middle East and Africa

- APAC

By Application Insights

The MPS segment is estimated to witness significant growth during the forecast period. The market in the United States is primarily driven by the increasing demand for food safety and convenience, particularly in the context of e-commerce and online grocery shopping. Sustainable packaging, including paper and paperboard, is gaining popularity due to its eco-friendly nature and barrier properties that maintain food freshness. In the US market, the meat, poultry, and seafood segment dominates, accounting for the largest share, due to the busy lifestyles of urban consumers. This segment's growth is fueled by the convenience offered by these packaged products.

Furthermore, the other significant segments include pasta and noodles, sauces, dressings, condiments, fruits and vegetables, and other food products. By focusing on these trends and consumer preferences, businesses can tap into the growing market.

Get a glance at the market share of various segments Request Free Sample

The MPS segment accounted for USD 61.00 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

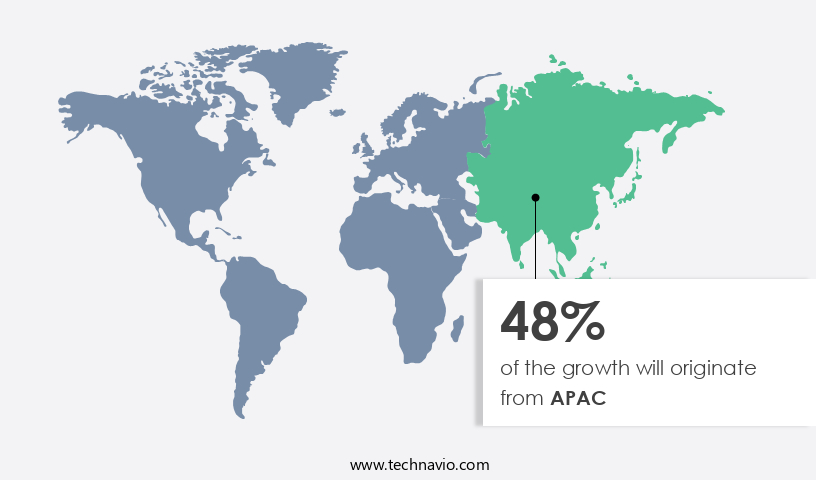

APAC is estimated to contribute 48% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market in Asia Pacific (APAC) is experiencing significant growth due to the increasing demand for convenient and safe packaged food options. Factors such as the expanding urban population and rising disposable income in countries like China and India are driving this trend. Additionally, there is a growing awareness among consumers in APAC regarding the importance of food safety and product quality. Packaged food refers to processed food items that offer extended shelf life and ease of preparation. In terms of packaging materials, flexible packaging is expected to dominate the market in APAC, accounting for over half of the market share.

Furthermore, a significant portion of this demand comes from the pasta and noodle segment. Environmental impact is a critical consideration in the ambient food packaging industry. Manufacturers are focusing on reducing the use of preservatives and opting for eco-friendly materials. Product protection is another key concern, with the use of sterilized and pasteurized packs becoming increasingly common. Consumer preferences for sustainable and healthy food options are also influencing the market.

Moreover, the market is expected to be driven by factors such as the increasing urban population, rising disposable income, and changing consumer preferences. The use of innovative packaging technologies and materials is also expected to contribute to market growth. In conclusion, the market in APAC is witnessing significant growth due to the rising demand for convenient, safe, and sustainable packaged food options. Flexible packaging is currently the dominant segment, but there is a growing focus on eco-friendly materials and reducing the use of preservatives. The market is expected to continue growing in the coming years, driven by factors such as urbanization, changing consumer preferences, and the use of innovative packaging technologies.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Demand for long shelf life in packaged food is the key driver of the market. The global food packaging industry is undergoing significant transformation, particularly in the ambient food segment, as refrigeration technology advances and consumer preferences shift towards lightweight packaging. The intricacies of the supply chain for perishable food items pose unique challenges, with the bullwhip effect leading to increased inventory levels and higher shipping costs. Online shopping's growing popularity further complicates matters, as packaging wastage becomes a significant concern. To mitigate these issues, production techniques are being refined to meet high standards and protocol requirements. By implementing efficient supply chain management strategies and investing in innovative packaging solutions, businesses can reduce waste, improve product freshness, and maintain consumer satisfaction.

Market Trends

Adoption to ecofriendly packaging is the upcoming trend in the market. The demand for ambient food packaging, particularly for non-refrigerated convenience foods and on-the-go snacks, has significantly increased in recent years due to consumers' busy lifestyles and growing health consciousness. However, the use of traditional packaging materials, such as plastic, raises concerns regarding environmental impact and potential food contamination. According to various studies, including those by the Environmental Working Group and the American Water Works Association, the presence of plastic pollutants in water sources, including in the US, poses health risks. To mitigate these issues, smart packaging technologies, such as Internet of Things (IoT) sensors and data analytics, are being adopted to ensure product quality and freshness.

Furthermore, these advanced solutions enable real-time monitoring of temperature, humidity, and other factors that can affect food quality, ensuring that consumers receive safe and high-quality products. Additionally, the integration of these technologies with product data analytics can provide valuable insights into consumer behavior and preferences, enabling companies to make informed decisions and optimize their supply chains. By investing in these innovative solutions, the market can address environmental concerns while meeting the growing demand for convenient and healthy food options.

Market Challenge

High processing requirement in ambient food packaging is a key challenge affecting the market growth. Ambient food packaging is essential for preserving food items without refrigeration, making it an ideal solution for the e-commerce sector. However, the production process involves additional costs due to extensive preservation techniques such as pasteurization and sterilization, which increase production costs by approximately 2-3%.

These processes ensure the food's safety from contamination during transportation and storage. Failure to undergo these processes can lead to spoilage due to environmental factors, including bacteria like aciduric and thermoduric. These bacteria can alter the food's pH levels, reducing its shelf life. Moreover, metal cans used for ambient food packaging pose a risk of food poisoning due to oxidation, which can corrode the can and mix with the food.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Amcor Plc - The company provides high-quality ambient food packaging solutions, including decanter narrow neck PET bottles, ensuring product freshness and protection from external elements.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ball Corp.

- Berry Global Inc.

- DuPont de Nemours Inc.

- FFP Packaging Ltd.

- KM Packaging Services Ltd

- Marsden Packaging Ltd.

- Mondi Plc

- ProAmpac Holdings Inc.

- SIG Group AG

- Tetra Laval SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is witnessing significant growth due to the increasing demand for non-refrigerated food, convenience foods, and on-the-go snacks. Smart packaging technologies, including sensors and data analytics, are revolutionizing the food industry by ensuring product quality and food safety. The Internet of Things (IoT) is playing a crucial role in the development of advanced packaging solutions. Sustainability is a major concern in the packaging industry, with consumers preferring eco-friendly alternatives to plastic packaging. Paper and paperboard, rigid packaging, and flexible packaging are popular choices for sustainable packaging. Sensors and data analytics help in monitoring product shelf life, ensuring freshness, and reducing wastage.

The e-commerce sector and online grocery shopping have led to an increase in the demand for ambient food packaging. FFP packaging solutions are gaining popularity due to their lightweight properties and cost-effectiveness, reducing shipping costs. Production sites need to adhere to high standards and protocol requirements to meet the increasing demand for ambient food packaging. The market is dominated by key players such as Berry Global and Amcor, who offer customized packaging solutions for various industries, including bakery, confectionery, sauces, and condiments. Tetra Pak is another major player in the market, known for its sustainable alternatives and high production capacities.

The environmental impact of packaging is a significant concern, and companies are focusing on reducing production techniques' environmental footprint while ensuring product protection and preservation.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

152 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.36% |

|

Market growth 2024-2028 |

USD 83.5 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

5.58 |

|

Regional analysis |

APAC, Europe, North America, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 48% |

|

Key countries |

US, China, UK, Japan, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Amcor Plc, Ball Corp., Berry Global Inc., DuPont de Nemours Inc., FFP Packaging Ltd., KM Packaging Services Ltd, Marsden Packaging Ltd., Mondi Plc, ProAmpac Holdings Inc., SIG Group AG, and Tetra Laval SA |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -