Anatomic Pathology Track And Trace Solutions Market Size 2026-2030

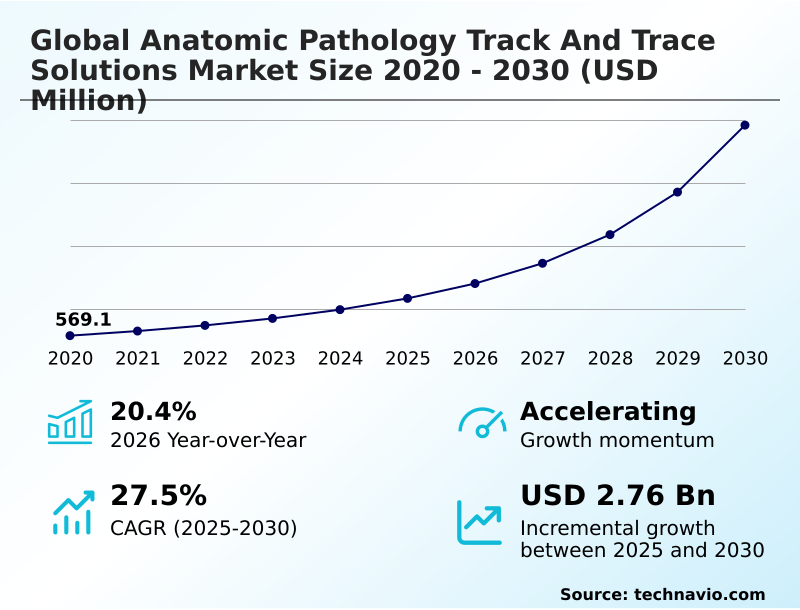

The anatomic pathology track and trace solutions market size is valued to increase by USD 2.76 billion, at a CAGR of 27.5% from 2025 to 2030. Escalating diagnostic volumes and need for enhanced laboratory efficiency will drive the anatomic pathology track and trace solutions market.

Major Market Trends & Insights

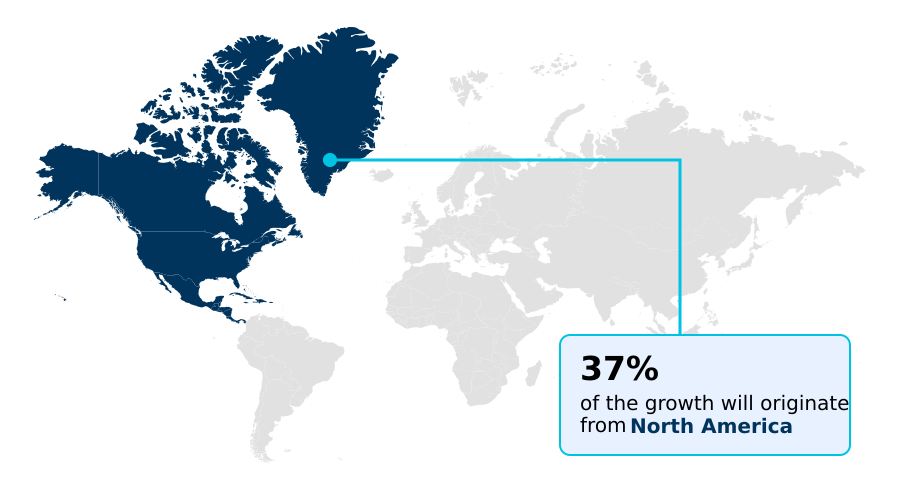

- North America dominated the market and accounted for a 37.3% growth during the forecast period.

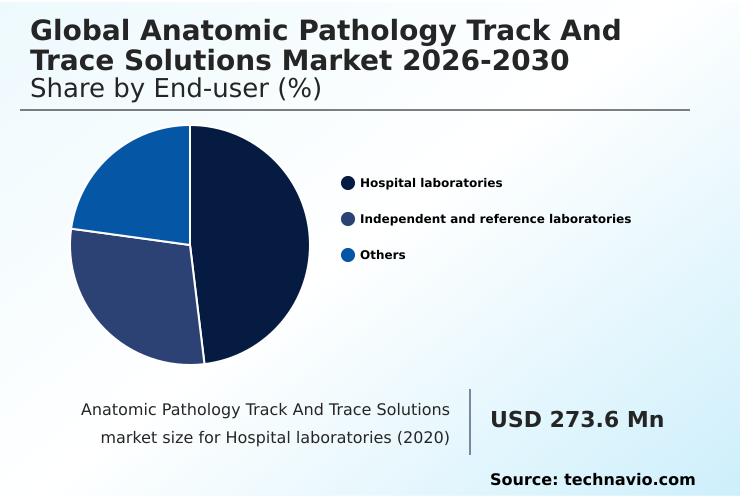

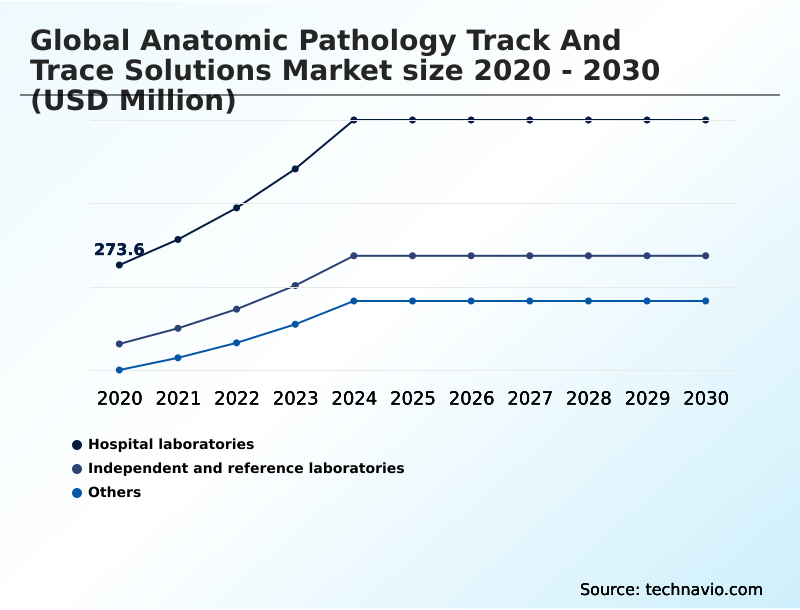

- By End-user - Hospital laboratories segment was valued at USD 472.2 million in 2024

- By Technology - Barcode segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.35 billion

- Market Future Opportunities: USD 2.76 billion

- CAGR from 2025 to 2030 : 27.5%

Market Summary

- The anatomic pathology track and trace solutions market is fundamentally shaped by the urgent need for diagnostic accuracy and operational efficiency. Escalating specimen volumes, driven by the rising prevalence of chronic diseases, have rendered manual tracking methods obsolete.

- Modern laboratories are compelled to adopt solutions that provide a verifiable digital chain of custody, ensuring each specimen is accurately identified and monitored from collection to diagnosis. For example, a large reference laboratory processing thousands of biopsies daily can leverage an integrated system to automate specimen accessioning, reducing the risk of human error and improving diagnostic turnaround times.

- The institutionalization of digital pathology further propels this market, as the integrity of a digital image is entirely dependent on the verifiable identity of the physical slide.

- Challenges such as the high cost of implementation and the complexities of integrating with legacy systems persist, but the push for regulatory compliance and patient safety continues to drive investment in these critical technologies.

What will be the Size of the Anatomic Pathology Track And Trace Solutions Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Anatomic Pathology Track And Trace Solutions Market Segmented?

The anatomic pathology track and trace solutions industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hospital laboratories

- Independent and reference laboratories

- Others

- Technology

- Barcode

- RFID

- Product

- Software

- Hardware

- Consumables

- Application

- Slides tracking

- Tissue cassettes and blocks tracking

- Specimen tracking

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By End-user Insights

The hospital laboratories segment is estimated to witness significant growth during the forecast period.

Hospital laboratories are a foundational end-user segment, where the primary goal of implementing track and trace technology is to eliminate pre-analytical errors.

These settings require a robust digital chain of custody, and the integration of these systems helps administrators optimize labor and monitor diagnostic turnaround time with precision.

The use of automated verification, a key component of specimen traceability systems, at each analytical workstation minimizes the risk of human error, which has been shown to reduce specimen misidentification by over 95%.

This focus on error reduction technology and patient safety protocols is critical in high-volume settings. The anatomic pathology workflow benefits from lab workflow optimization and positive patient identification, ensuring diagnostic accuracy and maintaining patient safety within the broader hospital ecosystem.

The Hospital laboratories segment was valued at USD 472.2 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Anatomic Pathology Track And Trace Solutions Market Demand is Rising in North America Get Free Sample

North America maintains a definitive leadership position, characterized by an advanced diagnostic infrastructure and early institutionalization of high-throughput digital workflows.

The regional focus on eliminating specimen misidentification has led to adoption rates of automated specimen tracking solutions that are 35% higher than in other developed regions.

European markets are also mature, with a strong emphasis on process standardization and interoperability standards to support large, consolidated laboratory networks. This has resulted in a 25% improvement in operational throughput in facilities that have fully integrated digital pathology integration.

Meanwhile, the Asia region is experiencing rapid growth, driven by massive government investments in healthcare modernization, creating significant opportunities for vendors providing end-to-end specimen tracking and real-time location systems.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of modern tracking solutions is reshaping laboratory operations, with a focus on delivering a verifiable and secure chain of custody for biopsies. The debate over barcode vs RFID in pathology labs continues, but the impact of RFID on specimen archival is undeniable, offering superior speed for inventory management.

- Stakeholders are conducting a thorough cost-benefit analysis of pathology automation to justify investments. Key to this is understanding the ROI of anatomic pathology tracking systems, which frequently demonstrate significant reductions in diagnostic errors. The adoption of anatomic pathology workflow optimization software is crucial for managing workloads, while software for tracking tissue blocks ensures sample integrity through processing.

- Integrating LIS with automated tracking hardware remains a technical focal point, overcoming challenges of legacy system integration. The goal is to achieve end-to-end traceability in cancer diagnostics, enhancing patient safety in lab diagnostics. This involves automated labeling for histology slides, workflow management for digital pathology, and real-time specimen location monitoring systems.

- The market is also driven by the need for compliance with CAP specimen handling standards, pushing laboratories toward hardware for positive patient identification. Ultimately, the move to cloud-based platforms for multi-site labs and the automation of quality control in histology are key trends improving turnaround time with tracking solutions.

What are the key market drivers leading to the rise in the adoption of Anatomic Pathology Track And Trace Solutions Industry?

- The escalating volume of diagnostic tests, coupled with the critical need for enhanced laboratory efficiency, serves as a primary driver for market growth.

- The primary market driver is the systemic increase in diagnostic volumes, compelling laboratories to adopt automated solutions to enhance operational throughput and laboratory efficiency.

- Adopting an automated accessioning system can increase a lab's processing capacity by up to 50% without a proportional increase in staff.

- A second powerful driver is the stringent regulatory landscape mandating a verifiable chain of custody verification to ensure patient safety and mitigate legal risks.

- Track and trace solutions provide a definitive audit trail creation, satisfying compliance with agencies that have reported a 30% increase in scrutiny over specimen integrity.

- Finally, the rapid institutionalization of digital pathology acts as a key enabler, requiring a clean, real-time data stream from automated tracking systems for effective data harmonization and workflow bottleneck identification.

What are the market trends shaping the Anatomic Pathology Track And Trace Solutions Industry?

- The integration of artificial intelligence for predictive quality control is an emerging market trend, allowing for the proactive identification of potential errors in specimen preparation.

- A dominant trend is the integration of artificial intelligence for predictive quality control, which moves beyond simple identification toward proactive error detection. Systems with vision-based AI can automatically verify tissue quality, with leading platforms reducing manual slide reworks by up to 60%. This shift toward intelligent, automated quality control is vital for achieving first-pass diagnostic confidence.

- Concurrently, the transition toward RFID and contactless tracking is gaining momentum in high-value applications, offering bulk reading capabilities that accelerate inventory management by over 75% compared to line-of-sight barcode systems. Furthermore, the deployment of cloud-based orchestration platforms is enabling interconnected diagnostic ecosystems, centralizing specimen tracking data for multi-site laboratory networks and ensuring a seamless digital thread for telepathology enablement.

What challenges does the Anatomic Pathology Track And Trace Solutions Industry face during its growth?

- Significant capital expenditure and the total cost of ownership present a key challenge, potentially impeding industry growth for smaller facilities.

- The primary market challenge remains the high capital expenditure and total cost of ownership, which can be a significant barrier for smaller facilities. A comprehensive system can require an upfront investment that is 2-3 times that of traditional equipment. Another significant hurdle is achieving seamless technical interoperability and legacy system integration.

- Many labs operate with disparate systems, and the absence of universal data security in healthcare and interoperability standards can lead to data silos, compromising the integrity of the digital thread for pathology. This lack of connectivity can increase implementation times by over 40%. Finally, complexities in workforce adaptation and process standardization present organizational challenges.

- The transition to automated protocols requires rigorous training and overcoming resistance to change, which can temporarily disrupt laboratory throughput and strain personnel resources.

Exclusive Technavio Analysis on Customer Landscape

The anatomic pathology track and trace solutions market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the anatomic pathology track and trace solutions market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Anatomic Pathology Track And Trace Solutions Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, anatomic pathology track and trace solutions market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agilent Technologies Inc. - Offers integrated solutions for anatomic pathology tracking, featuring automated workflow management and specimen identification to enhance diagnostic integrity and laboratory efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agilent Technologies Inc.

- Cerebrum Corp.

- Cirdan

- Clinisys Inc.

- CompuGroup Medical SE and Co.

- Computype Inc.

- Epredia

- F. Hoffmann La Roche Ltd.

- General Data Co. Inc.

- Leica Biosystems Nussloch GmbH

- LigoLab Information Systems

- NovoPath Inc.

- Powered Milestone Srl

- Psyche Systems Corp.

- Sakura Finetek USA Inc.

- Siemens Healthineers AG

- Soft Computer Consultants Inc.

- StatLab Medical Products

- XIFIN Inc.

- Zebra Technologies Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Anatomic pathology track and trace solutions market

- In September 2024, Agilent Technologies Inc. announced a strategic agreement to acquire Biocare Medical, a move designed to expand its portfolio of clinical and research pathology solutions and unify the tracking of advanced therapeutics.

- In November 2024, Sakura Finetek Europe and Hamamatsu Photonics K.K. announced a strategic global partnership to standardize the entire workflow from histology slide preparation to digital imaging, aiming to reduce specimen rework in European laboratories.

- In January 2025, Agilent Technologies Inc. launched the S540MD Slide Scanner System in key European markets, enhancing high-throughput digital workflows through automated barcode-driven scanning and AI-assisted tissue detection.

- In March 2025, Leica Biosystems, a Danaher company, introduced the Aperio GT Elite scanner and Aperio iQC software in the US, utilizing barcode-driven automation to accelerate slide processing and reduce manual quality control review times.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Anatomic Pathology Track And Trace Solutions Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 306 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 27.5% |

| Market growth 2026-2030 | USD 2756.2 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 20.4% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Indonesia, Thailand, Brazil, Argentina, South Africa, Saudi Arabia, Colombia, UAE, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is defined by a critical transition toward fully automated, interconnected laboratory environments. The core objective is mitigating diagnostic risk through a verifiable digital chain of custody, achieved with advanced specimen identification systems. This push is driven by the need for regulatory compliance documentation and enhanced anatomic pathology workflow.

- The adoption of barcode labeling systems and RFID specimen tracking is foundational, enabling pathology slide tracking and tissue cassette tracking. Laboratory information system integration with workflow orchestration software is central to achieving high-throughput digital workflows and lab workflow optimization. For executive decision-making, the pivot to digital pathology integration directly impacts budgeting for automated slide printing and other error reduction technology.

- This shift has enabled some leading institutions to reduce diagnostic turnaround time by over 40%. Ultimately, implementing end-to-end specimen tracking and automated quality control through robust specimen traceability systems provides the positive patient identification necessary for modern, high-volume diagnostics and ensures effective specimen lifecycle management.

What are the Key Data Covered in this Anatomic Pathology Track And Trace Solutions Market Research and Growth Report?

-

What is the expected growth of the Anatomic Pathology Track And Trace Solutions Market between 2026 and 2030?

-

USD 2.76 billion, at a CAGR of 27.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospital laboratories, Independent and reference laboratories, and Others), Technology (Barcode, and RFID), Product (Software, Hardware, and Consumables), Application (Slides tracking, Tissue cassettes and blocks tracking, and Specimen tracking) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Escalating diagnostic volumes and need for enhanced laboratory efficiency, High capital expenditure and total cost of ownership

-

-

Who are the major players in the Anatomic Pathology Track And Trace Solutions Market?

-

Agilent Technologies Inc., Cerebrum Corp., Cirdan, Clinisys Inc., CompuGroup Medical SE and Co., Computype Inc., Epredia, F. Hoffmann La Roche Ltd., General Data Co. Inc., Leica Biosystems Nussloch GmbH, LigoLab Information Systems, NovoPath Inc., Powered Milestone Srl, Psyche Systems Corp., Sakura Finetek USA Inc., Siemens Healthineers AG, Soft Computer Consultants Inc., StatLab Medical Products, XIFIN Inc. and Zebra Technologies Corp.

-

Market Research Insights

- The market's momentum is sustained by a push for greater laboratory efficiency and diagnostic accuracy. Adoption of automated systems has been shown to reduce specimen handling errors by up to 90%, while improving turnaround times by 40%.

- The shift toward telepathology enablement is also significant, with interconnected systems allowing for remote pathology consultation, which can expand diagnostic access by over 60% in underserved regions. This interconnectedness, facilitated by cloud-based orchestration, ensures a verifiable audit trail creation, critical for both patient safety protocols and regulatory adherence.

- The focus on process standardization and reducing the total cost of ownership drives companies to offer scalable asset traceability platforms, making advanced tracking accessible beyond large institutions.

We can help! Our analysts can customize this anatomic pathology track and trace solutions market research report to meet your requirements.

RIA -

RIA -