Application Platform Market Size 2024-2028

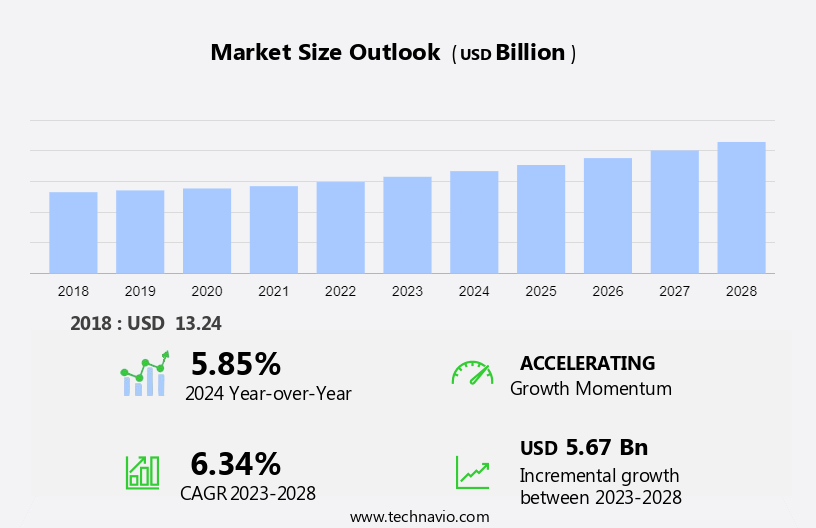

The application platform market size is forecast to increase by USD 5.67 billion at a CAGR of 6.34% between 2023 and 2028. The market is experiencing significant growth, driven by the increasing adoption of cloud services and the emergence of low-code application platforms. These trends enable organizations to streamline application codes release processes, ensuring superior infrastructure performances for their customized business applications. The use of paid software and open-source software, in conjunction with load balancers, auto-scaling orchestrators, and automated deployment tools, is becoming increasingly prevalent. This trend is driven by the increasing use of smartphones and wearable devices, leading to mobile app development.

However, challenges persist, such as the potential for company lock-in, which may limit the flexibility of organizations in choosing the best solution for their needs. Application Platform-as-a-Service (aPaaS) offerings continue to gain traction, providing businesses with cost-effective and efficient solutions to build, deploy, and manage their applications.

Market Analysis

The market is witnessing significant growth due to the increasing adoption of DevOps practices and cloud-based services. Cloud-based application platforms are becoming increasingly popular among developers as they offer easier deployment, scalability, and flexibility. These platforms provide development tools that run on various operating systems, including cloud solutions and CICS, enabling developers to create, test, and deploy application codes efficiently. Cloud computing technology plays a crucial role in the market, providing execution services, data services, and infrastructure performances. Application platform software offers diverse hardware support and integration with database management systems, making it an essential component of IT infrastructure.

Moreover, the market engineering process involves statistics and data triangulation to analyze market trends and forecast future growth. Application release processes are streamlined with managed services, ensuring seamless deployment and support and maintenance of applications. Overall, the market is expected to grow steadfastly, driven by the need for efficient development, deployment, and management of application codes in the IT industry.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Deployment

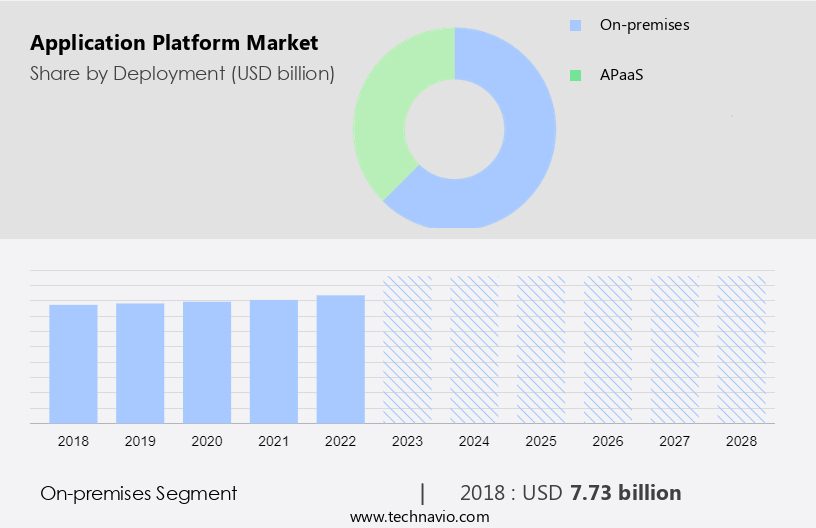

- On-premises

- aPaaS

- End-user

- Large enterprises

- SMEs

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- South America

- Middle East and Africa

- North America

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period. The market encompasses various deployment models, including Application Platform-as-Service (aPaaS) and on-premises. While aPaaS offers benefits such as easier application release processes and improved infrastructure performances through cloud services, on-premises deployment remains popular among large enterprises due to its enhanced security features. In the on-premises model, application codes are run on dedicated servers, providing greater control and security over data storage. This is in contrast to aPaaS, where data is spread across multiple servers, increasing potential vulnerabilities. The on-premises model's security advantages include physical access controls and customized security protocols, making it a preferred choice for businesses dealing with sensitive information.

Moreover, automated deployment tools, load balancers, and auto-scaling orchestrators further enhance the functionality of on-premises application platforms. Both paid software and open-source software options are available in the market to cater to diverse business needs.

Get a glance at the market share of various segments Request Free Sample

The on-premises segment was valued at USD 7.73 billion in 2018 and showed a gradual increase during the forecast period.

Regional Insights

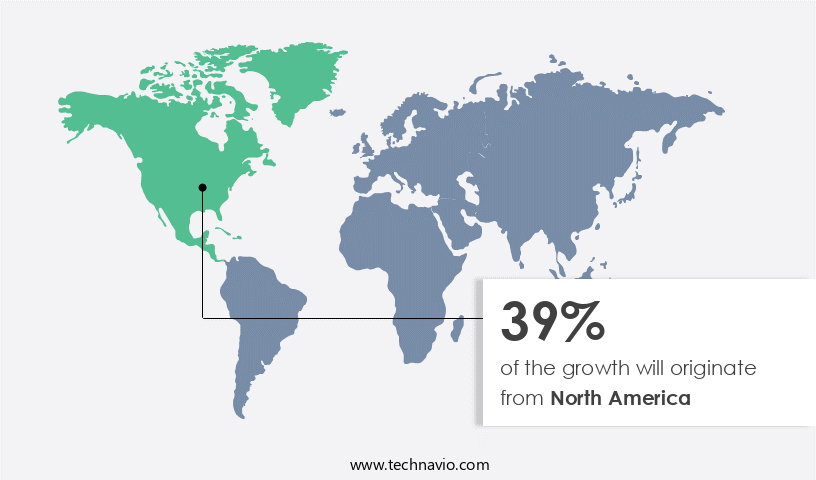

North America is estimated to contribute 39% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

North America's Early Adoption and Key Trends North America is currently leading the market due to the early adoption of application platform software, particularly in enterprise environments. Enterprises are leveraging Application Platform-as-a-Service (aPaaS) solutions and cloud services to build, test, and deploy applications quickly. Major companies, including SAP SE and International Business Machines Corp (IBM), offer mobile app development platforms, enabling businesses to customize applications to meet their unique requirements. Infrastructure performances, such as load balancers and auto-scaling orchestrators, are essential components of these platforms, ensuring optimal application release processes and user experiences.

Moreover, the market is segmented into paid software and open-source software. Paid software offers advanced features and support, while open-source software provides flexibility and cost savings. Regardless of the chosen option, automated deployment tools streamline the development process, ensuring efficient application codes deployment. In summary, the market in North America is thriving due to the early adoption of mobile technologies and the need for customized business applications. companies are offering innovative solutions to cater to the evolving demands of businesses, ensuring optimal application performance and user experiences.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

The growing popularity of cloud-based services is the key driver of the market. In today's business landscape, globally, enterprises are shifting towards Application Platform as a Service (aPaaS) solutions to minimize their capital expenditures (CAPEX) and reduce the complexities and expenses associated with building and maintaining on-premises applications. Traditional on-premises applications necessitate significant investments in hardware, operating systems (OS), databases, middleware, servers, and other software. Small and medium-sized enterprises (SMEs) are particularly drawn to aPaaS offerings as they offer on-demand access to hardware, middleware, OS, software, and resources. Cloud platforms, including those for iOS, Windows, and other operating systems, provide numerous benefits to organizations. By moving to the cloud, businesses can transition from CAPEX to operational expenditures (OPEX), significantly reducing the upfront costs for servers and network equipment.

Moreover, this cost shift is particularly advantageous for industries such as transportation and logistics, media and entertainment, and those requiring email, network, and web security. Furthermore, aPaaS solutions offer managed services and support and maintenance, enabling organizations to focus on their core competencies while ensuring the reliability and security of their applications.

Market Trends

The emergence of low-code application platforms is the upcoming trend in the market. Low-code application platforms have become essential tools for businesses seeking to quickly develop and deploy applications in response to evolving market demands and customer needs. These platforms offer visual interfaces, drag-and-drop components, and pre-built templates, enabling developers to create applications with minimal coding. This significantly reduces development time and accelerates time-to-market for new products and features. The use of low-code application platforms extends to various industries, including transportation and logistics, media and entertainment, and email and network security for IOS and Windows platforms. In the context of email and network security, these platforms can facilitate the development of applications that ensure data triangulation and enhance web and transport security. Moreover, low-code application platforms provide support and maintenance services, as well as managed services, ensuring that applications remain up-to-date and functioning optimally. This is crucial for businesses that require continuous application availability and performance.

Market Challenge

Issues associated with company lock-in is a key challenge affecting the market growth. The market: company lock-ins are a challenge in the rapidly evolving technology landscape, particularly in the realm of Application Platform as a Service (aPaaS). IOS and Windows users may find it difficult to switch aPaaS providers after developing applications using specific platform software and tools. This dependency arises due to the lack of compatibility with other companies' programming languages, APIs, architectures, libraries, or operating systems. Integration of various systems and technologies from diverse companies is a common requirement in application development, encompassing sectors like transportation and logistics, media and entertainment, and email and network security. Web security and data triangulation are additional critical aspects. However, the companies and solution providers offer support and maintenance, as well as managed services, to cater to these needs.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Alphabet Inc.: The company offers application platform such as Akamai Intelligent Edge Platform, which provide cloud services for delivering and securing digital experiences across web and mobile applications, content delivery, and cybersecurity solutions.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alphabet Inc.

- Amazon.com Inc.

- Appian Corp.

- Betty Blocks BV

- BMC Software Inc.

- Caucho Technology Inc

- Cisco Systems Inc.

- GigaSpaces

- Hewlett Packard Enterprise Co.

- Hitachi Ltd.

- International Business Machines Corp.

- Microsoft Corp.

- Open Text Corp.

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- Siemens AG

- VANTIQ Inc.

- Wipro Ltd.

- Zerone Consulting Pvt. Ltd.

- Akamai Technologies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is a significant segment of the information technology industry, driven by the increasing adoption of cloud-based services and the shift towards cloud-native applications. Application platform software includes development tools, execution services, data services, and cloud solutions that enable developers to build, deploy, and manage applications. Cloud-based application platforms are becoming increasingly popular due to their flexibility, scalability, and cost savings. These platforms offer a range of features such as automation, artificial intelligence, and integration with diverse hardware and operating systems including Android, iOS, and Windows. The market caters to various industries such as transportation and logistics, media and entertainment, and software services.

Moreover, the security services including email, network, and web security are essential components of application platforms. Platform-as-a-Service (PaaS) and Application Platform-as-a-Service (APaaS) are popular models in the market. APaaS platforms offer managed services, drag-and-drop interfaces, hot reloading, and 3rd party integrations. Infrastructure performances, customized business applications, database management, and microservices are key areas of focus for application platform companies. The market is segmented into software segment, deployment & integration, support & maintenance, and infrastructure performances. The market is characterized by a multi-cloud strategy, with organizations using a mix of paid software and open-source software. Load balancers, auto-scaling orchestrators, and automated deployment tools are essential components of application platforms. The market is expected to grow significantly due to the increasing demand for cloud services, the need for efficient deployment and integration, and the requirement for enhanced security features.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

174 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.34% |

|

Market growth 2024-2028 |

USD 5.67 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.85 |

|

Regional analysis |

North America, Europe, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

North America at 39% |

|

Key countries |

US, China, Australia, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Adobe Inc., Alphabet Inc., Amazon.com Inc., Appian Corp., Betty Blocks BV, BMC Software Inc., Caucho Technology Inc, Cisco Systems Inc., GigaSpaces, Hewlett Packard Enterprise Co., Hitachi Ltd., International Business Machines Corp., Microsoft Corp., Open Text Corp., Oracle Corp., Salesforce Inc., SAP SE, Siemens AG, VANTIQ Inc., Wipro Ltd., Zerone Consulting Pvt. Ltd., and Akamai Technologies Inc. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -