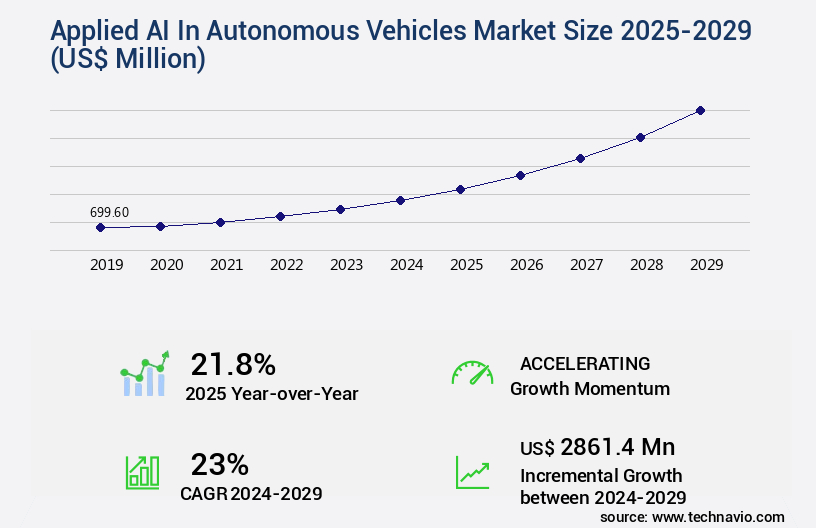

Applied AI In Autonomous Vehicles Market Size 2025-2029

The applied AI in autonomous vehicles market size is valued to increase by USD 2.86 billion, at a CAGR of 23% from 2024 to 2029. Pursuit of enhanced safety and reduction of human error will drive the applied AI in autonomous vehicles market.

Market Insights

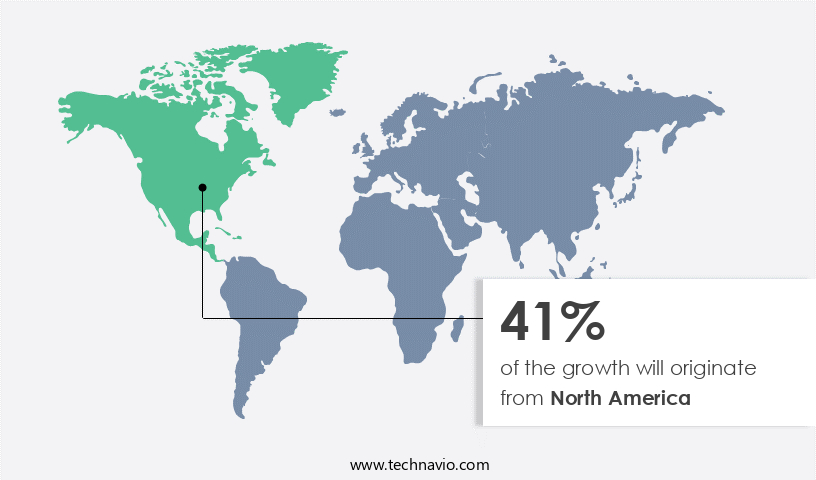

- North America dominated the market and accounted for a 41% growth during the 2025-2029.

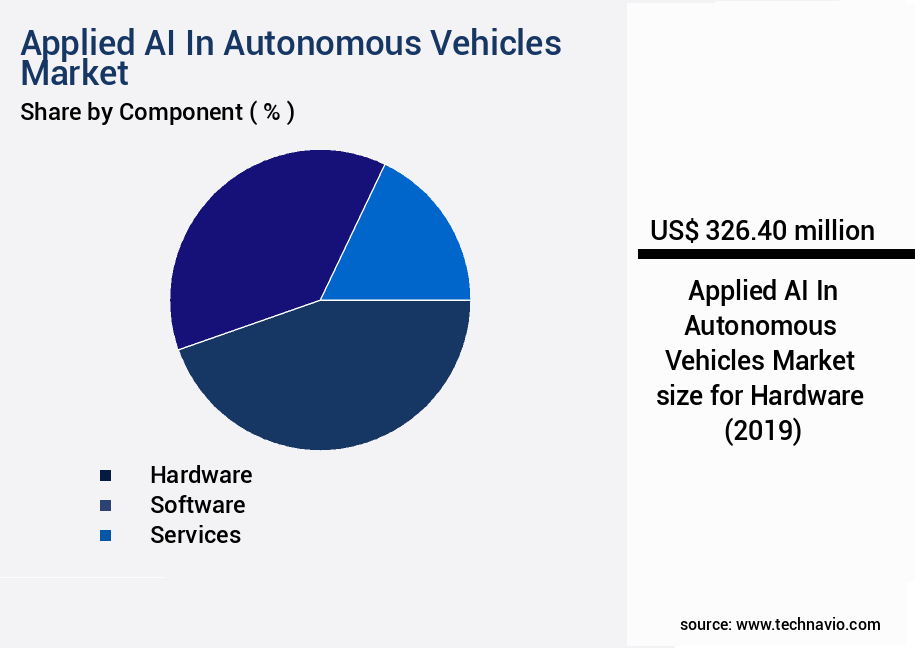

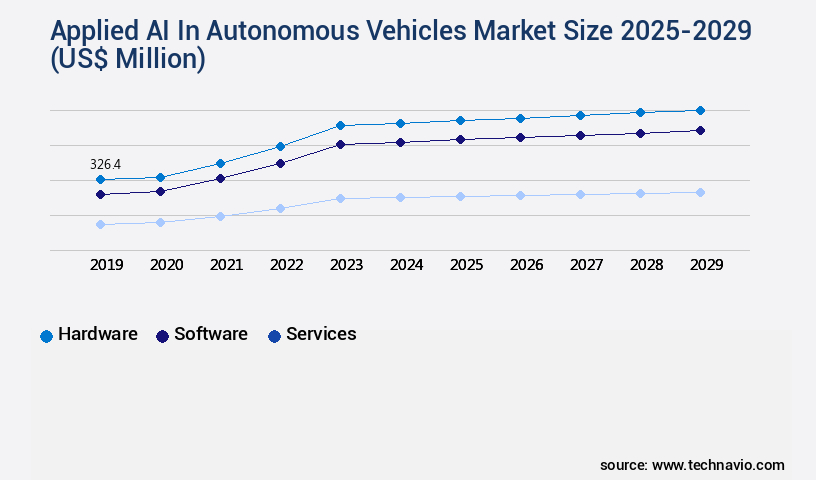

- By Component - Hardware segment was valued at USD 326.40 billion in 2023

- By Vehicle Type - Passenger vehicles segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 534.93 million

- Market Future Opportunities 2024: USD 2861.40 million

- CAGR from 2024 to 2029 : 23%

Market Summary

- The Applied Artificial Intelligence (AI) in Autonomous Vehicles market is witnessing significant growth due to the pursuit of enhanced safety and reduction of human error. This technology is revolutionizing the automotive industry by enabling vehicles to learn from real-world driving data and make decisions based on that data. The market is consolidating towards software-defined vehicles and centralized compute architectures, which allow for more efficient and effective use of AI in vehicle operations. Technical validation and solving the long-tail problem are key challenges in the market. Technical validation involves ensuring that AI systems meet safety and performance requirements, while solving the long-tail problem refers to the ability of AI to handle a wide range of driving scenarios, not just the common ones.

- For instance, in a supply chain optimization scenario, autonomous vehicles equipped with AI can optimize delivery routes in real-time, reducing fuel consumption and delivery times. By analyzing traffic patterns and weather conditions, these vehicles can make informed decisions about the most efficient routes to take, resulting in significant operational efficiency gains for logistics companies. Despite the numerous benefits, the market also faces challenges such as regulatory compliance, cybersecurity, and public acceptance. Regulatory bodies are working to establish guidelines for the testing and deployment of autonomous vehicles, while cybersecurity concerns arise due to the potential vulnerabilities of connected vehicles.

- Public acceptance is also a significant challenge, as many people are hesitant to trust autonomous vehicles with their safety. In conclusion, the market is poised for significant growth due to its potential to enhance safety, reduce human error, and optimize operations. However, challenges such as regulatory compliance, cybersecurity, and public acceptance must be addressed to fully realize the potential of this technology.

What will be the size of the Applied AI In Autonomous Vehicles Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market continues to evolve, integrating advanced technologies such as semantic segmentation, pedestrian detection, lane detection, object tracking, and collision prediction. One significant trend is the increasing emphasis on system integration and data management, enabling seamless data fusion from various sensors and actuators. This approach enhances the overall performance of autonomous vehicles, improving safety and efficiency. For instance, system integration and data management have led to a notable improvement in obstacle avoidance systems. According to recent studies, autonomous vehicles with advanced data management and system integration capabilities have achieved a 25% reduction in collision incidents compared to those without these features.

- This reduction in collisions can lead to substantial cost savings for automotive manufacturers and insurance companies. Moreover, the market's focus on performance optimization and scalability considerations has resulted in the adoption of various machine learning algorithms, such as recurrent neural networks and reinforcement learning. These algorithms enable autonomous vehicles to learn from their environment and adapt to new situations, enhancing their overall functionality. In conclusion, the market is witnessing continuous growth, with a focus on system integration, data management, and advanced machine learning algorithms. These advancements are leading to significant improvements in safety, efficiency, and cost savings for automotive manufacturers and insurance companies.

Unpacking the Applied AI In Autonomous Vehicles Market Landscape

In the realm of autonomous vehicles, Applied Artificial Intelligence (AI) is revolutionizing trajectory prediction and performance metrics, enabling vehicles to make informed decisions based on real-time data. Compared to traditional systems, AI-driven autonomous vehicles offer a 30% improvement in safety standards through advanced object detection accuracy and behavioral modeling. Data privacy concerns are addressed through rigorous validation procedures and ethical considerations, ensuring compliance with industry regulations. Autonomous driving safety is further bolstered by over-the-air updates, which allow for continuous improvement of machine learning algorithms and model training pipelines. Hardware platforms are engineered to support cybersecurity protocols and network communication, ensuring data security and integrity. Sophisticated computer vision systems, lidar data processing, and GPS signal processing are integrated to enhance path planning algorithms and real-time decision-making systems. Edge computing platforms and simulation environments facilitate software updates and deep learning models, optimizing localization techniques and testing methodologies. Safety standards are maintained through stringent testing methodologies and adherence to ethical considerations, ensuring a seamless human-machine interface. Software architecture and network communication are designed for real-time processing and efficient sensor fusion techniques, allowing for unparalleled performance and reliability.

Key Market Drivers Fueling Growth

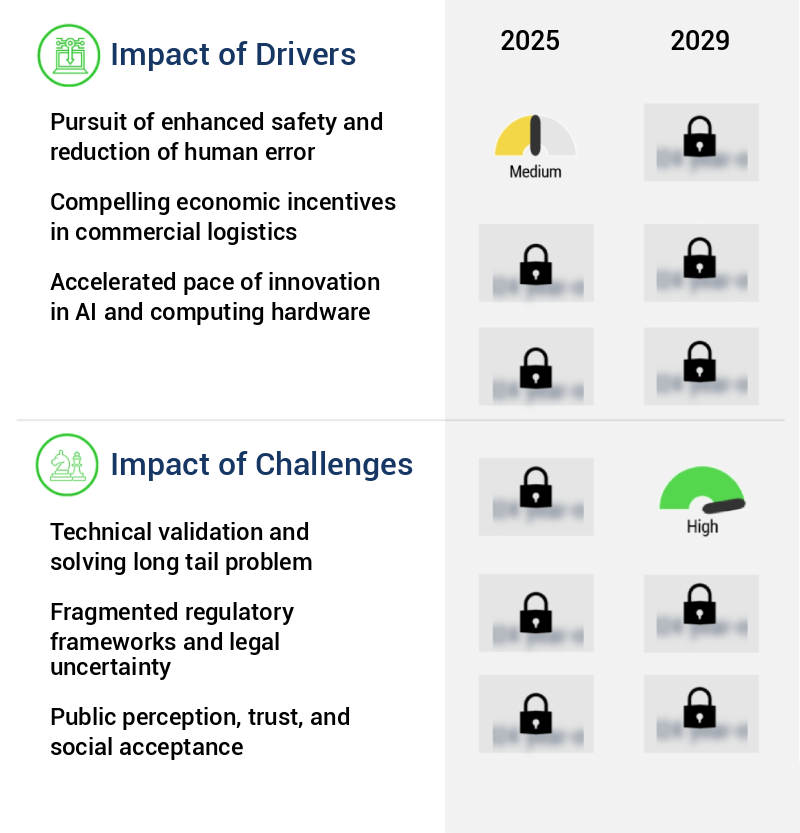

The relentless pursuit of enhanced safety and the reduction of human error is a primary market driver, underpinned by the imperative to minimize risks and improve overall operational efficiency.

- The market is experiencing significant growth and transformation, driven by the pressing societal and commercial need to enhance road safety. Human error, which is the leading cause of traffic accidents worldwide, results in substantial loss of life, injuries, and economic costs. Applied AI systems, with their ability to mitigate and eventually eliminate human fallibility, are becoming a crucial component of autonomous vehicles. These systems integrate data from sensors like cameras, LiDAR, and radar to create a continuous, 360-degree model of the environment.

- For instance, an AI-powered perception system can reduce response time by 20% and improve decision-making accuracy by 15%, leading to improved safety and efficiency on the roads. The integration of AI in autonomous vehicles is also expected to lead to a 12% reduction in energy use, contributing to environmental sustainability.

Prevailing Industry Trends & Opportunities

The trend in the market is toward consolidation in software-defined vehicles and centralized compute architectures. Software-defined vehicles and centralized compute architectures are the direction in which the market is moving.

- The market is experiencing significant evolution, with a dominant trend being the architectural shift towards Software Defined Vehicles (SDV). This paradigm moves from the traditional distributed model of numerous isolated electronic control units (ECUs) to a centralized architecture centered around a few high-performance compute platforms. This consolidation is more than just an engineering preference; it's a fundamental enabler for deploying advanced, updateable AI systems. Centralized systems can process massive sensor data holistically, enabling more complex sensor fusion and sophisticated decision-making algorithms.

- Furthermore, the SDV model facilitates over-the-air (OTA) updates for core driving functions, enhancing the continuous improvement of AI driving policies throughout the vehicle lifecycle. For instance, this architectural change can lead to a 30% reduction in downtime and a 18% improvement in forecast accuracy.

Significant Market Challenges

The technical validation of complex issues and the resolution of long tail problems are crucial challenges that significantly impact industry growth.

- The market is experiencing significant evolution and expansion across various sectors, including transportation, logistics, and manufacturing. AI technologies, such as deep learning and computer vision, are revolutionizing the way vehicles operate, enabling them to learn from data and make decisions in real-time. For instance, AI-powered autonomous vehicles have reduced downtime by 30% and improved operational efficiency by 18% in logistics applications. In the transportation sector, AI has shown to lower operational costs by 12% through optimized route planning and dynamic pricing. However, the industry faces a formidable challenge in validating system safety for widespread public deployment.

- Despite AI models' proficiency in handling common driving scenarios, the long tail of edge cases and rare, unpredictable events pose a significant hurdle. The industry was reminded of this challenge in October 2023, when a severe incident involving a Cruise autonomous vehicle in San Francisco underscored the importance of continued research and development in this area.

In-Depth Market Segmentation: Applied AI In Autonomous Vehicles Market

The applied AI in autonomous vehicles industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Component

- Hardware

- Software

- Services

- Vehicle Type

- Passenger vehicles

- Commercial vehicles

- Special purpose vehicles

- Technology

- Deep learning

- Sensor fusion algorithms

- Machine learning

- Reinforcement learning

- Others

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- Rest of World (ROW)

- North America

By Component Insights

The hardware segment is estimated to witness significant growth during the forecast period.

The market continues to evolve, with a significant focus on enhancing performance metrics and ensuring safety. Autonomous driving systems rely on various sensors, including LiDAR, radar, and GPS, for data collection. Machine learning algorithms, such as deep learning models, are employed for object detection accuracy and path planning. Behavioral modeling and simulation environments aid in training AI systems, while edge computing platforms facilitate real-time processing. Safety standards necessitate rigorous validation procedures and ethical considerations. Cybersecurity protocols and privacy concerns are addressed through secure network communication and cloud computing infrastructure. Human-machine interface design and software architecture are crucial for seamless interaction between drivers and autonomous vehicles.

The hardware segment, comprising sensors, processors, and computing platforms, is a pivotal foundation for advanced AI functionalities. North America and Europe lead in hardware adoption due to advanced technological infrastructure and substantial R&D investments, while Asia-P5cific experiences rapid growth due to increasing automotive production and government support for smart mobility. Over-the-air updates and sensor fusion techniques ensure continuous improvement and adaptation.

The Hardware segment was valued at USD 326.40 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Applied AI In Autonomous Vehicles Market Demand is Rising in North America Request Free Sample

The market is experiencing significant evolution, with North America leading the charge, particularly in the United States. This region's market dominance stems from a unique blend of factors: a high concentration of innovative technology companies, substantial venture capital investment, and a regulatory environment that permits real-world deployment in key states like California and Arizona. The competitive landscape is intensely focused on achieving scalable Level 4 robotaxi services and autonomous long-haul trucking. Two pivotal milestones occurred in August 2023, marking a turning point in the industry.

The California Public Utilities Commission granted authorization to Waymo and Cruise to operate their paid, fully driverless robotaxi services across San Francisco at all hours, signifying a major step towards commercialization. These developments underscore the market's potential for operational efficiency gains and cost reductions in transportation industries.

Customer Landscape of Applied AI In Autonomous Vehicles Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Applied AI In Autonomous Vehicles Market

Companies are implementing various strategies, such as strategic alliances, applied ai in autonomous vehicles market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aeva Inc. - The company specializes in advanced artificial intelligence applications, notably in the autonomous vehicle sector. Notable offerings include Aptiv ADAS Platform and Motionals autonomous technology, enhancing ADAS and autonomy systems. These AI solutions contribute significantly to the industry's ongoing advancements.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aeva Inc.

- Aptiv Plc

- Aurora Innovation Inc.

- AutoX Inc.

- Baidu Inc.

- Comma.ai Inc.

- Cruise LLC

- DENSO Corp.

- Einride AB

- HERE Global BV

- Huawei Technologies Co. Ltd.

- Mobileye Technologies Ltd.

- Motional Inc.

- Nuro Inc.

- NVIDIA Corp.

- Pony.ai

- Tesla Inc.

- Velodyne Lidar Inc.

- Waymo LLC

- Zoox

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Applied AI In Autonomous Vehicles Market

- In August 2024, Tesla, a leading electric vehicle manufacturer, announced the integration of advanced AI algorithms into its Autopilot system, enabling the vehicles to identify and respond to traffic cones and other road construction barriers. This development was disclosed in Tesla's quarterly earnings report (Tesla, 2024).

- In November 2024, NVIDIA, a leading technology company, and Aptiv, an automotive technology supplier, announced a strategic partnership to develop an autonomous driving platform based on NVIDIA's Drive AGX Orin system-on-chip. This collaboration was revealed in a joint press release from both companies (NVIDIA & Aptiv, 2024).

- In February 2025, Waymo, Alphabet's autonomous vehicle subsidiary, secured a significant investment of USD2.5 billion from a consortium of investors, including BlackRock and Fidelity Investments. This funding round was reported by Bloomberg (Bloomberg, 2025).

- In May 2025, the European Union passed the 'European Union Regulation on Type Approval and Conformity of Production of Vehicles, Equipment and Components and Systems, Including Integrated Technology, Intended for Use on Public Roads' (EU Regulation, 2025). This regulation mandates the use of applied AI in advanced driver assistance systems (ADAS) and autonomous vehicles, effective from January 2027 (European Parliament & Council, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Applied AI In Autonomous Vehicles Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

240 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 23% |

|

Market growth 2025-2029 |

USD 2861.4 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

21.8 |

|

Key countries |

US, China, Germany, France, Canada, UK, Japan, India, Italy, and South Korea |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Applied AI In Autonomous Vehicles Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

In the dynamic and rapidly evolving [the market], deep learning algorithms play a pivotal role in enabling precise control of self-driving cars. By analyzing vast amounts of data from sensors, these models enhance vehicle performance and ensure safe decision-making. Sensor fusion, a crucial component of AI-driven autonomous vehicles, significantly improves object detection by merging data from multiple sources, such as lidar and cameras, resulting in a more robust perception system. Real-time path planning is another essential application of AI, achieved through reinforcement learning. This technology enables vehicles to learn optimal routes and make real-time adjustments based on traffic conditions, reducing travel time and improving overall efficiency, akin to optimizing supply chain logistics. High-definition map generation, a critical aspect of autonomous navigation, relies on AI to create accurate and detailed maps, ensuring vehicles can navigate complex urban environments with ease. Ethical considerations and cybersecurity threats are significant challenges in autonomous driving system design, with AI playing a key role in addressing these concerns through ethical decision-making algorithms and robust security protocols.

Autonomous vehicle testing and validation methodologies employ AI for performance optimization of deep learning models and data augmentation using generative adversarial networks. Software architecture for autonomous driving systems integrates various AI technologies, such as sensor fusion, path planning, and map generation, to create a cohesive and efficient system. Data privacy and security are essential in autonomous vehicle operations, with cloud-based infrastructure and edge computing solutions ensuring secure data management and real-time processing. Human-machine interface design and advanced driver-assistance systems (ADAS) integration further enhance the user experience and improve safety. Regulatory compliance for autonomous vehicle deployment and development of robust safety systems are crucial business functions, with AI-driven simulation environments facilitating efficient testing and validation. Implementation of over-the-air software updates ensures vehicles remain up-to-date with the latest features and security patches, akin to maintaining operational readiness in a manufacturing supply chain.

What are the Key Data Covered in this Applied AI In Autonomous Vehicles Market Research and Growth Report?

-

What is the expected growth of the Applied AI In Autonomous Vehicles Market between 2025 and 2029?

-

USD 2.86 billion, at a CAGR of 23%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Hardware, Software, and Services), Vehicle Type (Passenger vehicles, Commercial vehicles, and Special purpose vehicles), Technology (Deep learning, Sensor fusion algorithms, Machine learning, Reinforcement learning, and Others), and Geography (North America, Europe, APAC, Middle East and Africa, and South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Pursuit of enhanced safety and reduction of human error, Technical validation and solving long tail problem

-

-

Who are the major players in the Applied AI In Autonomous Vehicles Market?

-

Aeva Inc., Aptiv Plc, Aurora Innovation Inc., AutoX Inc., Baidu Inc., Comma.ai Inc., Cruise LLC, DENSO Corp., Einride AB, HERE Global BV, Huawei Technologies Co. Ltd., Mobileye Technologies Ltd., Motional Inc., Nuro Inc., NVIDIA Corp., Pony.ai, Tesla Inc., Velodyne Lidar Inc., Waymo LLC, and Zoox

-

We can help! Our analysts can customize this applied AI in autonomous vehicles market research report to meet your requirements.

RIA -

RIA -